|

市場調查報告書

商品編碼

1801918

超大規模資料中心市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Hyperscale Data Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024年,全球超大規模資料中心市場規模達583億美元,預計到2034年將以26.3%的複合年成長率成長,達到5,910億美元。這一成長主要源於對數位服務、雲端運算、人工智慧 (AI) 和巨量資料分析需求的激增。超大規模資料中心旨在實現大規模可擴展性、能源效率和高效能運算,對技術提供者、企業和政府機構都至關重要。隨著社交媒體、物聯網設備和企業應用程式等各種來源的資料消費不斷成長,全球各地對這些先進資料中心的需求也日益成長。

新冠疫情在加速市場成長方面發揮了關鍵作用。儘管2020年初期建設和設備供應中斷,但由於全球轉向遠距辦公、電子學習和線上服務,2021年需求激增。這促使超大規模資料中心供應商加大對網路、邊緣運算和混合雲端基礎設施的投資。此外,為了在勞動力短缺的情況下維持營運,他們採用了自動化和遠端管理工具。因此,諸如人工智慧驅動的資料管理平台、邊緣主機託管和工作負載編排等服務對於市場差異化至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 583億美元 |

| 預測值 | 5910億美元 |

| 複合年成長率 | 26.3% |

2024年,解決方案細分市場佔據78.8%的市場佔有率,預計到2034年成長率將達到27.1%。由於對可擴展、高效能IT基礎設施(例如伺服器、儲存、網路硬體以及電源和冷卻解決方案)的需求不斷成長,該細分市場引領市場,這些基礎設施對於超大規模環境至關重要。雲端運算、人工智慧、巨量資料分析和串流媒體等行業的蓬勃發展,推動了企業對更強大、更節能的系統的需求。

企業級市場佔最大佔有率,2024 年將達到 55%,預計 2025 年至 2034 年的複合年成長率將達到 24.8%。這種主導地位反映出私有雲和混合雲端基礎架構的日益普及,這些基礎架構對於支援關鍵任務工作負載、法規遵循和資料控制至關重要。銀行、醫療保健、電信和製造等行業的企業正在部署超大規模系統,以實現 IT 框架的現代化,提高敏捷性並增強網路安全。

2024年,美國超大規模資料中心市場佔81.6%的市場佔有率,市場規模達175億美元。美國佔據主導地位的動力源於其強大的雲端運算生態系統、廣泛的數位基礎設施以及來自大型科技公司的大量投資。美國仍然是超大規模資料營運的主要樞紐,也是雲端運算應用和企業數位轉型的關鍵市場。

全球超大規模資料中心市場的領先公司包括微軟、IBM、亞馬遜網路服務、華為技術、Alphabet、博通和Equinix。為了鞏固市場地位,超大規模資料中心領域的公司正致力於擴大全球業務範圍、投資創新技術並實現服務多元化。雲端服務供應商優先考慮自動化和人工智慧驅動的資料管理解決方案,以提高營運效率並降低管理成本。他們還大力投資邊緣運算,以提高資料處理速度並減少客戶延遲。此外,與產業參與者的合作以及混合雲端架構的實施正在成為滿足客戶對靈活性和可擴展性需求的標準策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 更重視研發投資與產品創新

- 電動運動車介紹

- 越來越傾向於休閒活動

- 越野賽事數量不斷增加

- 產業陷阱與挑戰

- 動力運動車輛的初始成本高

- 安全和環境影響問題日益嚴重

- 市場機會

- 電動跑車細分市場的擴張

- 探險旅遊和生態旅遊蓬勃發展

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 技能差距分析與勞動發展

- 目前資料中心技能短缺評估

- 未來勞動力需求

- 技能再培訓和技能提升計劃

- 企業培訓與個人認證

- 學術機構合作夥伴關係

- 政府培訓項目

- 資料中心管理的職業道路發展

- 定價分析與成本模型

- 基礎設施成本結構分析

- 供應商定價策略

- 訂閱模式與消費模式

- 主機託管定價套餐

- 電力使用成本明細

- 超大規模投資的投資報酬率評估

- 跨地區成本比較

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 用例

- 最佳情況

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 解決方案

- 冷卻

- 力量

- IT 機架與機櫃

- LV/MV分佈

- 網路裝置

- 資料中心基礎設施管理

- 服務

- 安裝和部署

- 維護與支援

- 監控服務

第6章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 雲端提供者

- 主機託管提供者

- 企業

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 金融服務業

- 零售與電子商務

- 政府

- IT和電信

- 娛樂與媒體

- 其他

第8章:市場估計與預測:依發電容量,2021 - 2034 年

- 主要趨勢

- 20兆瓦至50兆瓦

- 50兆瓦至100兆瓦

第9章:市場估計與預測:按資料中心,2021 - 2034 年

- 主要趨勢

- 企業/超大規模自建

- 超大規模主機託管

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- ABB

- Alibaba Cloud

- Alphabet

- Amazon Web Services

- Broadcom

- Cisco Systems

- Dell

- Digital Realty Trust

- Equinix

- HPE

- Huawei

- IBM

- Inspur

- Intel

- Lenovo

- Marvell Technology

- Microsoft

- NVIDIA

- Oracle

- Schneider Electric

- Vertiv

- Western Digital

- 區域參與者

- Colt

- Corning

- Fujitsu

- Nlyte Software

- Quanta Computer

- Sify Technologies

- Telefonaktiebolaget LM Ericsson

- Tencent

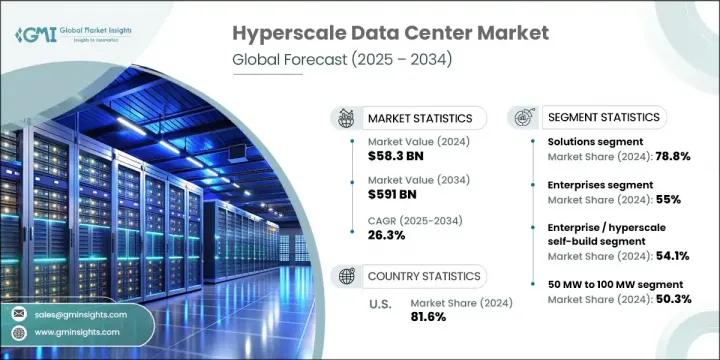

The Global Hyperscale Data Center Market was valued at USD 58.3 billion in 2024 and is estimated to grow at a CAGR of 26.3% to reach USD 591 billion by 2034. This expansion is driven by the surge in demand for digital services, cloud computing, artificial intelligence (AI), and big data analytics. Hyperscale data centers, designed for massive scalability, energy efficiency, and high-performance computing, are becoming critical for technology providers, corporations, and government agencies alike. As data consumption grows from various sources like social media, IoT devices, and enterprise applications, the need for these advanced data centers intensifies across global regions.

The COVID-19 pandemic played a pivotal role in accelerating market growth. While there were initial disruptions in construction and equipment supply in 2020, demand soared in 2021 due to the global shift towards remote work, e-learning, and online services. This led hyperscale providers to ramp up investments in expanding their networks, edge computing, and hybrid cloud infrastructures. Additionally, automation and remote management tools were adopted to maintain operations amid workforce challenges. As a result, services like AI-powered data management platforms, edge colocation, and workload orchestration have become increasingly crucial for market differentiation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $58.3 Billion |

| Forecast Value | $591 Billion |

| CAGR | 26.3% |

In 2024, the solutions segment accounted for 78.8% share, with a growth rate of 27.1% expected through 2034. This segment leads the market due to the increasing demand for scalable, high-performance IT infrastructure, such as servers, storage, networking hardware, and power and cooling solutions, which are essential for hyperscale environments. The booming sectors of cloud computing, AI, big data analytics, and streaming are driving the need for more robust, energy-efficient systems that enterprises are investing in.

The enterprise segment held the largest share, with 55% in 2024, and is forecasted to grow at a CAGR of 24.8% from 2025 to 2034. This dominance reflects the growing adoption of private and hybrid cloud infrastructure, essential for supporting mission-critical workloads, regulatory compliance, and data control. Enterprises in sectors such as banking, healthcare, telecom, and manufacturing are deploying hyperscale systems to modernize their IT frameworks, boost agility, and fortify cybersecurity.

U.S. Hyperscale Data Center Market held 81.6% share in 2024, generating USD 17.5 billion. The country's dominance is driven by a strong cloud computing ecosystem, extensive digital infrastructure, and substantial investments from major technology companies. The U.S. remains both a primary hub for hyperscale data operations and a key market for cloud adoption and enterprise digital transformation.

Leading companies in the Global Hyperscale Data Center Market include Microsoft, IBM, Amazon Web Services, Huawei Technologies, Alphabet, Broadcom, and Equinix. To strengthen their market presence, companies in the hyperscale data center sector are focusing on expanding their global footprints, investing in innovative technologies, and diversifying their service offerings. Cloud service providers are prioritizing automation and AI-driven data management solutions to enhance operational efficiency and reduce overhead costs. They are also investing heavily in edge computing to improve data processing speeds and reduce latency for customers. Additionally, collaboration with industry players and the implementation of hybrid cloud architectures are becoming standard strategies to meet customer demands for flexibility and scalability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 End use

- 2.2.4 Application

- 2.2.5 Power Capacity

- 2.2.6 Data Center

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing focus on R&D investments and product innovation

- 3.2.1.2 Introduction of electric power sport vehicles

- 3.2.1.3 Growing inclination towards recreational activities

- 3.2.1.4 Rising number of off-roading events

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of power sports vehicles

- 3.2.2.2 Increasing safety and environmental impact concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric power sports vehicle segment

- 3.2.3.2 Growing adventure tourism and eco-tourism

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Skills gap analysis and workforce development

- 3.8.1 Current data center skills shortage assessment

- 3.8.2 Future workforce requirements

- 3.8.3 Reskilling and upskilling initiatives

- 3.8.4 Corporate training vs individual certification

- 3.8.5 Academic institution partnerships

- 3.8.6 Government training programs

- 3.8.7 Career path development in data center management

- 3.9 Pricing analysis and cost models

- 3.9.1 Infrastructure cost structure analysis

- 3.9.2 Vendor pricing strategies

- 3.9.3 Subscription vs consumption-based models

- 3.9.4 Colocation pricing packages

- 3.9.5 Power usage cost breakdown

- 3.9.6 ROI assessment for hyperscale investment

- 3.9.7 Cost comparison across regions

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use cases

- 3.13 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Cooling

- 5.2.2 Power

- 5.2.3 IT racks & enclosures

- 5.2.4 LV/MV distribution

- 5.2.5 Networking equipment

- 5.2.6 DCIM

- 5.3 Service

- 5.3.1 Installation & deployment

- 5.3.2 Maintenance & support

- 5.3.3 Monitoring services

Chapter 6 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud providers

- 6.3 Colocation providers

- 6.4 Enterprises

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Retail & e-commerce

- 7.4 Government

- 7.5 IT & telecom

- 7.6 Entertainment & media

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Power Capacity, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 20 MW To 50 MW

- 8.3 50 MW To 100 MW

Chapter 9 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Enterprise / Hyperscale Self-Build

- 9.3 Hyperscale Colocation

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ABB

- 11.1.2 Alibaba Cloud

- 11.1.3 Alphabet

- 11.1.4 Amazon Web Services

- 11.1.5 Broadcom

- 11.1.6 Cisco Systems

- 11.1.7 Dell

- 11.1.8 Digital Realty Trust

- 11.1.9 Equinix

- 11.1.10 HPE

- 11.1.11 Huawei

- 11.1.12 IBM

- 11.1.13 Inspur

- 11.1.14 Intel

- 11.1.15 Lenovo

- 11.1.16 Marvell Technology

- 11.1.17 Microsoft

- 11.1.18 NVIDIA

- 11.1.19 Oracle

- 11.1.20 Schneider Electric

- 11.1.21 Vertiv

- 11.1.22 Western Digital

- 11.2 Regional Players

- 11.2.1 Colt

- 11.2.2 Corning

- 11.2.3 Fujitsu

- 11.2.4 Nlyte Software

- 11.2.5 Quanta Computer

- 11.2.6 Sify Technologies

- 11.2.7 Telefonaktiebolaget LM Ericsson

- 11.2.8 Tencent

超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季)

超大規模資料中心業者資料中心超大規模資料中心業者資料中心:市場資料概覽(2026 年第二季) 超大規模資料中心市場:按組件、電力容量、冷卻解決方案、所有權、部署模式、應用領域和最終用戶產業分類-2026-2032年全球市場預測

超大規模資料中心市場:按組件、電力容量、冷卻解決方案、所有權、部署模式、應用領域和最終用戶產業分類-2026-2032年全球市場預測 超大規模資料中心市場分析及預測(至2035年):按類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶和解決方案分類

超大規模資料中心市場分析及預測(至2035年):按類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶和解決方案分類 2026年全球超大規模資料中心市場報告超級資料中心市場:按組件、電力容量、冷卻技術、能源來源、最終用戶和部署模式分類-2026-2032年全球預測

2026年全球超大規模資料中心市場報告超級資料中心市場:按組件、電力容量、冷卻技術、能源來源、最終用戶和部署模式分類-2026-2032年全球預測 超級資料中心市場規模、佔有率和成長分析:按資料中心類型、服務類型、部署模式、技術和地區分類-2026-2033年產業預測

超級資料中心市場規模、佔有率和成長分析:按資料中心類型、服務類型、部署模式、技術和地區分類-2026-2033年產業預測 2026-2030年全球超大規模資料中心市場

2026-2030年全球超大規模資料中心市場 超大規模資料中心市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年)

超大規模資料中心市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034 年) 超大規模資料中心市場規模、佔有率和成長分析(按組件、資料中心類型、基礎設施、垂直產業、部署模式和地區分類)-2026-2033年產業預測

超大規模資料中心市場規模、佔有率和成長分析(按組件、資料中心類型、基礎設施、垂直產業、部署模式和地區分類)-2026-2033年產業預測