|

市場調查報告書

商品編碼

1801916

電動車平台市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測EV Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

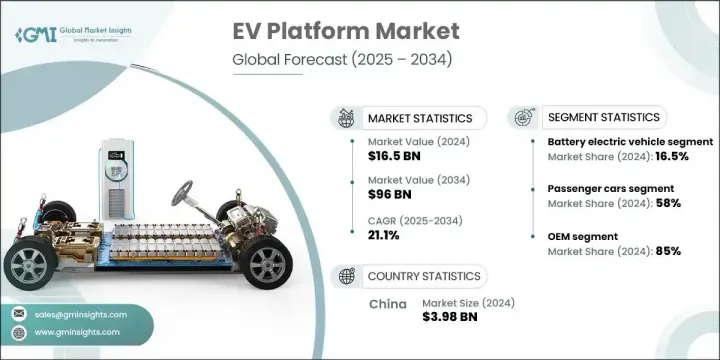

2024年,全球電動車平台市場規模達1,65億美元,預計到2034年將以21.1%的複合年成長率成長,達到960億美元。人們日益轉向永續和零排放出行解決方案,這推動了電動車平台的快速創新。這些平台目前正在演變為模組化、軟體定義的系統,支援自動駕駛、電池整合和可擴展動力系統等高級功能。汽車製造商正在設計平台,以實現跨車型的靈活架構,同時實現經濟高效的生產和更高的能源效率。

人工智慧驅動的功能和無線更新在最佳化續航里程和性能方面發揮著至關重要的作用。疫情加速了人們對數位優先車輛體驗的需求,促使企業將非接觸式功能和即時連接工具整合到平台設計中。遠端診斷、語音輔助控制和智慧路線管理的進步,已將電動車平台從基礎結構部件提升為下一代出行的智慧化、適應性強的骨幹。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 165億美元 |

| 預測值 | 960億美元 |

| 複合年成長率 | 21.1% |

純電動車市場佔16.5%的市場佔有率,預計到2034年將以21%的複合年成長率成長。純電動車因其簡潔的架構和與滑板式平台的兼容性而備受青睞,該平台可最大限度地利用內部空間、最佳化電池佈局和設計靈活性。純電動特性無需內燃機系統,使製造商能夠設計出流線型結構,降低生產成本,並提高性能效率。

乘用車市場在2024年佔據最高佔有率,達到58%,預計2025年至2034年將維持強勁成長,複合年成長率達20%。不斷成長的消費者需求,以及OEM在平台開發方面的大量投資,推動了電動乘用車的廣泛普及。各大汽車廠商正在打造針對轎車、掀背車和小型SUV最佳化的專用電動車架構,提供靈活的設計、更長的續航里程和對連網功能的支援。這種廣泛的適應性使汽車製造商能夠以更好的續航里程、更高的安全性和更強大的數位整合度瞄準大眾市場。

中國電動車平台市場佔69%的市場佔有率,2024年市場規模達39.8億美元。作為主要的電動車製造商和消費者,中國在電動車市場中扮演著舉足輕重的角色。政府透過補貼、強制生產和充電基礎設施投資等策略性支持,為平台創新註入了強勁動力。國內企業持續研發可擴展且價格合理的電動車平台,在性能和續航里程之間取得平衡,同時滿足日益成長的電動車用戶群的需求。

塑造全球電動車平台市場的領先公司包括福特、特斯拉、豐田、福斯、寶馬、通用汽車和沃爾沃。為了鞏固其市場地位,電動車平台領域的公司正在優先考慮一系列策略性投資和合作夥伴關係。原始設備製造商正在大力投資研發,以開發支援各種車輛尺寸和功能的模組化平台,同時確保與新興軟體驅動技術的兼容性。汽車製造商還與電池生產商和科技公司合作,創建用於連接、充電和自動駕駛的整合生態系統。此外,許多公司正在採用垂直整合模式來控制馬達、控制器和電池組等關鍵零件,從而提高性能和成本控制。這些策略有助於確保在不斷發展的電動車領域中的可擴展性、適應性和長期競爭力。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 零件供應商

- 平台開發者

- 製造商

- 配銷通路

- 最終用戶

- 產業衝擊力

- 成長動力

- 全球電動車普及率激增

- 電池技術的進步

- OEM轉向模組化電動車架構

- 擴大電動車充電基礎設施

- 產業陷阱與挑戰

- 電動車平台的初始投資高

- 新興地區基礎設施低度開發

- 市場機會

- 電動汽車即服務 (EVaaS) 模式的成長

- 與自主和互聯技術的整合

- 商業車隊電氣化

- 城市微型交通解決方案需求不斷成長

- 成長動力

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利分析

- 價格趨勢

- 按地區

- 搭車

- 利潤率分析

- 成本細分分析

- 原料成本構成

- 製造和機械成本

- 物流和配送成本

- 勞動力和組裝成本

- 研發和測試成本

- 電動車平台市場演變與成熟度分析

- 從 ICE 改裝到專用平台的歷史發展

- 平台架構演進時間表

- 技術採用生命週期分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 純電動車(BEV)

- 混合動力電動車(HEV)

- 插電式混合動力車(PHEV)

第6章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- SUV/跨界車

- 掀背車

- 商用車

- 輕型商用車

- 重型商用車

第7章:市場估計與預測:依平台,2021 - 2034 年

- 主要趨勢

- P0

- P1

- P2

- P3

- P4

第8章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 電池

- 懸吊系統

- 運動系統

- 機殼

- 電子控制單元(ECU)

- 其他

第9章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 全球參與者

- BMW

- Ford

- General Motors

- Hyundai Motor

- Nissan Motor

- Renault

- Stellantis

- Tesla

- Toyota Motor

- Volkswagen

- 區域參與者

- Avatar Technology

- BYD Auto

- Leapmotor

- Mahindra Electric

- Seres

- Tata Motors

- Zeekr

- 新興玩家

- Bollinger Motors

- Canoo

- Cenntro

- Foxconn

- Geely

- Gaussin

- Lucid Motors

- NIO

- OSVehicle

- REE Automotive

- Rivian Automotive

- XPeng Motors

- Zero Labs Automotive

The Global EV Platform Market was valued at USD 16.5 billion in 2024 and is estimated to grow at a CAGR of 21.1% to reach USD 96 billion by 2034. The increasing shift toward sustainable and zero-emission mobility solutions has sparked rapid innovation in EV platforms. These platforms are now evolving into modular, software-defined systems that support advanced features like autonomous driving, battery integration, and scalable powertrains. Automakers are designing platforms that allow flexible architecture across vehicle classes while enabling cost-efficient production and improved energy efficiency.

AI-driven features and over-the-air updates play a crucial role in optimizing range and performance. The pandemic accelerated demand for digital-first vehicle experiences, pushing companies to integrate contactless functionalities and real-time connectivity tools into platform design. Advancements in remote diagnostics, voice-assisted controls, and intelligent route management have elevated EV platforms from basic structural components to intelligent, adaptable backbones for next-gen mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.5 Billion |

| Forecast Value | $96 Billion |

| CAGR | 21.1% |

The battery electric vehicles segment held 16.5% share and is forecasted to grow at a CAGR of 21% through 2034. BEVs are favored due to their clean architecture and compatibility with skateboard-style platforms that maximize interior space, battery placement, and design flexibility. Their pure electric nature eliminates combustion systems, allowing manufacturers to engineer streamlined structures, reduce production costs, and boost performance efficiency.

The passenger car segment held the highest share at 58% in 2024 and is projected to maintain strong growth with a CAGR of 20% from 2025 to 2034. Widespread adoption of electric passenger vehicles has been fueled by growing consumer demand, paired with substantial OEM investment in platform development. Companies are creating dedicated EV architectures optimized for sedans, hatchbacks, and compact SUVs, offering flexible designs, enhanced battery life, and support for connected features. This broad adaptability enables automakers to target a mass-market audience with improved range, safety, and digital integration.

China EV Platform Market held 69% share, generating USD 3.98 billion in 2024. The country plays a pivotal role in the market as both a major EV manufacturer and consumer. Strategic government support through subsidies, production mandates, and charging infrastructure investments has created strong momentum in platform innovation. Domestic firms continue to engineer scalable, affordable EV platforms that balance performance and range while catering to the needs of their expanding electric vehicle user base.

Leading companies shaping the Global EV Platform Market include Ford, Tesla, Toyota, Volkswagen, BMW, General Motors, and Volvo. To reinforce their market position, companies in the EV platform sector are prioritizing a mix of strategic investments and partnerships. OEMs are heavily investing in R&D to develop modular platforms that support a wide range of vehicle sizes and functions, while ensuring compatibility with emerging software-driven technologies. Automakers are also collaborating with battery producers and tech firms to create integrated ecosystems for connectivity, charging, and autonomy. Furthermore, many are adopting vertical integration models to control key components such as motors, controllers, and battery packs, which enhances performance and cost control. These strategies help ensure scalability, adaptability, and long-term competitiveness in the evolving EV landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Propulsion

- 2.2.3 Vehicle

- 2.2.4 Platform

- 2.2.5 Component

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Component suppliers

- 3.1.3 Platform developers

- 3.1.4 Manufacturers

- 3.1.5 Distribution channel

- 3.1.6 End users

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in global electric vehicle adoption

- 3.2.1.2 Advancements in battery technology

- 3.2.1.3 OEM shift to modular EV architectures

- 3.2.1.4 Expansion of EV charging infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment in EV platforms

- 3.2.2.2 Underdeveloped infrastructure in emerging regions

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in EV-as-a-service (EVaaS) models

- 3.2.3.2 Integration with autonomous & connected tech

- 3.2.3.3 Electrification of commercial fleets

- 3.2.3.4 Rising demand for urban micro-mobility solutions

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter’s analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Price Trend

- 3.8.1 By region

- 3.8.2 By Vehicle

- 3.9 Profit margin analysis

- 3.10 Cost breakdown analysis

- 3.10.1 Raw material cost components

- 3.10.2 Manufacturing and machinery costs

- 3.10.3 Logistics and distribution costs

- 3.10.4 Labor and assembly costs

- 3.10.5 R&D and testing costs

- 3.11 EV platform market evolution and maturity analysis

- 3.11.1 Historical development from ICE adaptations to dedicated platforms

- 3.11.2 Platform architecture evolution timeline

- 3.11.3 Technology adoption lifecycle analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Battery electric vehicles (BEV)

- 5.3 Hybrid electric vehicles (HEV)

- 5.4 Plug-in hybrid electric vehicles (PHEV)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 SUVs/crossovers

- 6.2.3 Hatchbacks

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Heavy commercial vehicles

Chapter 7 Market Estimates & Forecast, By Platform, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 P0

- 7.3 P1

- 7.4 P2

- 7.5 P3

- 7.6 P4

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery

- 8.3 Suspension system

- 8.4 Motor system

- 8.5 Chassis

- 8.6 Electronic Control Units (ECUs)

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BMW

- 11.1.2 Ford

- 11.1.3 General Motors

- 11.1.4 Hyundai Motor

- 11.1.5 Nissan Motor

- 11.1.6 Renault

- 11.1.7 Stellantis

- 11.1.8 Tesla

- 11.1.9 Toyota Motor

- 11.1.10 Volkswagen

- 11.2 Regional Players

- 11.2.1 Avatar Technology

- 11.2.2 BYD Auto

- 11.2.3 Leapmotor

- 11.2.4 Mahindra Electric

- 11.2.5 Seres

- 11.2.6 Tata Motors

- 11.2.7 Zeekr

- 11.3 Emerging Players

- 11.3.1 Bollinger Motors

- 11.3.2 Canoo

- 11.3.3 Cenntro

- 11.3.4 Foxconn

- 11.3.5 Geely

- 11.3.6 Gaussin

- 11.3.7 Lucid Motors

- 11.3.8 NIO

- 11.3.9 OSVehicle

- 11.3.10 REE Automotive

- 11.3.11 Rivian Automotive

- 11.3.12 XPeng Motors

- 11.3.13 Zero Labs Automotive

電動車平台市場 - 全球預測,2026-2032年

電動車平台市場 - 全球預測,2026-2032年 電動車平台市場規模、佔有率、成長、全球產業分析、區域洞察及2026-2034年預測

電動車平台市場規模、佔有率、成長、全球產業分析、區域洞察及2026-2034年預測 2026年全球電動車平台市場報告小型電動車平台市場:策略性洞察與預測(2026-2031年)多用途電動車平台市場:依動力型、最終用戶、電池容量等級、車輛類型分類,全球預測,2026-2032年全球電動車平台市場規模、佔有率、趨勢和成長分析報告(2026-2034)

2026年全球電動車平台市場報告小型電動車平台市場:策略性洞察與預測(2026-2031年)多用途電動車平台市場:依動力型、最終用戶、電池容量等級、車輛類型分類,全球預測,2026-2032年全球電動車平台市場規模、佔有率、趨勢和成長分析報告(2026-2034) 電動車平台市場規模、佔有率和成長分析(按車輛類型、電動車類型、組件、動力系統和地區分類)-2026-2033年產業預測

電動車平台市場規模、佔有率和成長分析(按車輛類型、電動車類型、組件、動力系統和地區分類)-2026-2033年產業預測 全球電動車平台市場

全球電動車平台市場 電動車平台市場報告:2030 年趨勢、預測與競爭分析

電動車平台市場報告:2030 年趨勢、預測與競爭分析 電動車平台市場 - 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢與預測

電動車平台市場 - 2024-2034 年全球產業分析、規模、佔有率、成長、趨勢與預測