|

市場調查報告書

商品編碼

1801904

旋風分離器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cyclone Separator Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

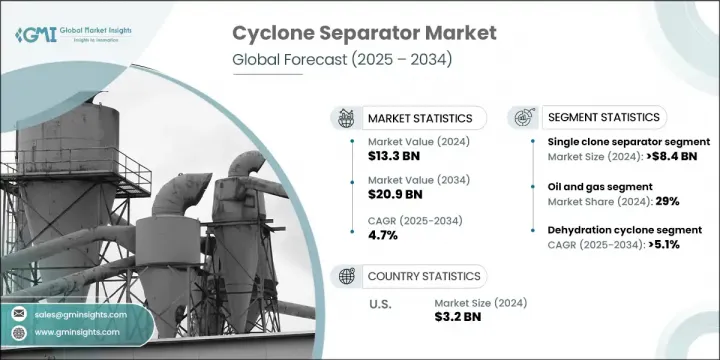

2024年,全球旋風分離器市場規模達133億美元,預計到2034年將以4.7%的複合年成長率成長,達到209億美元。隨著清潔能源解決方案的日益普及以及全球環境法規的日益嚴格,該市場的發展勢頭強勁。隨著對生質能、太陽能和其他替代能源的需求不斷成長,對高性能空氣過濾系統的需求也隨之成長,以減少排放並保護設備。旋風分離器因其高效處理顆粒物、支援多個產業永續發展目標而成為至關重要的解決方案。

多級過濾、CFD最佳化設計和混合系統等技術進步顯著提高了性能和能源效率。它們的作用正在迅速演變,尤其是在化學、電子和製藥等精密密集型行業。在亞太地區,由於排放法規日益嚴格,正在經歷快速工業化的國家正在推動需求成長。為了應對日益成長的基礎設施和製造業活動,旋風分離器正被廣泛採用。在當今競爭激烈的環境中,產品客製化和材料耐用性等特性對於買家的決策至關重要,尤其是在各行各業都優先考慮長期可靠性和低維護成本的情況下。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 133億美元 |

| 預測值 | 209億美元 |

| 複合年成長率 | 4.7% |

單旋風分離器市場規模在2024年達到84億美元,預計2034年將以4.6%的複合年成長率成長。其廣泛應用歸因於較低的前期成本、簡單的機械結構和極低的維護要求。由於沒有活動部件,這些系統在需要持續正常運作和預算控制的環境中提供了一種經濟高效的解決方案,因此在注重運作可靠性的重工業中尤其具有吸引力。

2024年,石油和天然氣產業佔據29%的市場佔有率,預計2025年至2034年期間的複合年成長率將達到5.2%。旋風分離器在整個價值鏈中都至關重要——從需要除砂和液氣分離設備的上游作業,到涉及天然氣加工、精煉和管道維護的下游應用。這些分離器在降低顆粒物負荷、保護高價值機械設備以及確保高壓、大流量環境下不間斷的運作方面發揮著至關重要的作用。

美國旋風分離器市場佔79%的市場佔有率,2024年市場規模達32億美元。這一成長主要得益於嚴格的環境政策,這些政策要求採用先進的空氣品質管理解決方案。相關法規要求各行業部署高效率的顆粒物去除技術。旋風分離器通常用作預過濾工具,可有效減輕最終過濾系統的負擔,確保合規性,並最佳化整體運作效率。

積極影響旋風分離器市場的關鍵參與者包括 Mikropor、Sulzer、FLSmidth、Gulf Coast Air & Hydraulics、Cyclone Engineering Projects、Multotec、The Weir Group、KREBS、Exterran Corporation、Air Dynamics、Cyclotech、Haiwang Hydrocyclone、Mahleparator, Seirginal Solutions。旋風分離器市場的領先製造商正專注於策略性產品創新和區域擴張,以增強其競爭地位。公司擴大整合 CFD 等先進模擬工具來最佳化分離器設計,從而提高效率並降低能耗。產品多樣化也不斷成長,以服務製藥、電子和清潔能源等高精度產業。參與者正在與工業客戶建立合作夥伴關係,以提供符合嚴格排放和營運標準的客製化解決方案。許多公司正在擴大其全球製造和分銷網路,以服務新興市場,尤其是亞太地區。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按類型

- 監管格局

- 標準和合規性要求

- 區域監理框架

- 認證標準

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 軸流

- 逆流

第6章:市場估計與預測:按克隆類型,2021 - 2034 年

- 主要趨勢

- 單克隆分離器

- 多克隆分離器

第7章:市場估計與預測:依產能,2021 - 2034 年

- 主要趨勢

- 高達 2000 公斤/小時

- 2000公斤/小時 - 3000公斤/小時

- 3000公斤/小時以上

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 脫水旋風器

- 脫泥旋流器

- 除渣旋風器

- 其他(濃縮旋風器、旋風器組等)

第9章:市場估計與預測:依最終用途產業,2021 - 2034 年

- 主要趨勢

- 石油和天然氣

- 化學

- 採礦和礦物加工

- 發電

- 食品和飲料

- 其他(紙漿及造紙、紡織、製藥等)

第 10 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 直銷

- 間接銷售

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- Air Dynamics

- Cyclone Engineering Projects

- Cyclone Separator Australia

- Cyclotech

- Elgin Separation Solutions

- Exterran Corporation

- FLSmidth

- Gulf Coast Air & Hydraulics

- Haiwang Hydrocyclone

- KREBS

- Mahle Industrial Filtration

- Mikropor

- Multotec

- Sulzer

- The Weir Group

The Global Cyclone Separator Market was valued at USD 13.3 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 20.9 billion by 2034. The market is gaining traction due to the increasing push toward clean energy solutions and stringent global environmental regulations. As the demand for biomass, solar, and other alternative energy sources increases, so does the requirement for high-performance air filtration systems to reduce emissions and protect equipment. Cyclone separators have emerged as vital solutions due to their efficiency in handling particulates, supporting sustainability goals across multiple industries.

Technological advancements such as multi-stage filtration, CFD-optimized designs, and hybrid systems have significantly improved performance and energy efficiency. Their role is rapidly evolving, especially in precision-intensive sectors like chemicals, electronics, and pharmaceuticals. In the Asia-Pacific region, countries experiencing fast industrialization are driving demand due to tighter emission regulations. Cyclone separators are being widely adopted in response to growing infrastructure and manufacturing activity. In today's competitive landscape, features such as product customization and material durability are becoming critical for buyer decision-making, especially as industries prioritize long-term reliability and low maintenance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.3 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 4.7% |

Single cyclone separators reached USD 8.4 billion in 2024 and is anticipated to grow at a CAGR of 4.6% through 2034. Their widespread adoption is attributed to low upfront costs, simple mechanical structure, and minimal maintenance requirements. With no moving parts, these systems offer a cost-efficient solution in environments where continuous uptime and budget control are essential, making them especially appealing in heavy industries seeking operational reliability.

The oil & gas sector held a 29% share in 2024 and is set to grow at a CAGR of 5.2% between 2025 and 2034. Cyclone separators are critical throughout the entire value chain-from upstream operations requiring devices for desanding and liquid-gas separation to downstream applications involving gas processing, refining, and pipeline maintenance. These separators play a crucial role in reducing particulate load, safeguarding high-value machinery, and ensuring uninterrupted operations in high-pressure, high-volume environments.

United States Cyclone Separator Market held a 79% share generating USD 3.2 billion in 2024. This growth is fueled by strict environmental policies requiring advanced air quality management solutions. Regulations compel industries to deploy efficient particulate removal technologies. Cyclone separators are commonly used as pre-filtration tools, effectively decreasing the burden on final filtration systems, ensuring regulatory compliance, and optimizing overall operational efficiency.

Key players actively shaping the Cyclone Separator Market include Mikropor, Sulzer, FLSmidth, Gulf Coast Air & Hydraulics, Cyclone Engineering Projects, Multotec, The Weir Group, KREBS, Exterran Corporation, Air Dynamics, Cyclotech, Haiwang Hydrocyclone, Mahle Industrial Filtration, Elgin Separation Solutions, and Cyclone Separator Australia. Leading manufacturers in the cyclone separator market are focusing on strategic product innovation and regional expansion to strengthen their competitive positions. Companies are increasingly integrating advanced simulation tools like CFD to optimize separator designs for greater efficiency and lower energy consumption. Product diversification to serve high-precision industries such as pharmaceuticals, electronics, and clean energy is also on the rise. Players are forming partnerships with industrial clients to deliver tailored solutions that meet strict emission and operational standards. Many firms are expanding their global manufacturing and distribution networks to serve emerging markets, especially in Asia-Pacific.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 By type

- 2.2.3 By clone type

- 2.2.4 By capacity

- 2.2.5 By application

- 2.2.6 By end use industry

- 2.2.7 By distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Axial flow

- 5.3 Reverse flow

Chapter 6 Market Estimates & Forecast, By Clone type, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Single clone separator

- 6.3 Multi-clone separator

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Up to 2000 kg/hr

- 7.3 2000 kg/hr. - 3000 kg/hr

- 7.4 Above 3000 kg/hr

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Dehydration cyclone

- 8.3 Desliming cyclone

- 8.4 Slag removal cyclones

- 8.5 Others (concentration cyclone, cyclone group etc.)

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Oil and gas

- 9.3 Chemical

- 9.4 Mining and mineral processing

- 9.5 Power generation

- 9.6 Food and beverages

- 9.7 Others (pulp & paper, textiles, pharmaceutical etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Air Dynamics

- 12.2 Cyclone Engineering Projects

- 12.3 Cyclone Separator Australia

- 12.4 Cyclotech

- 12.5 Elgin Separation Solutions

- 12.6 Exterran Corporation

- 12.7 FLSmidth

- 12.8 Gulf Coast Air & Hydraulics

- 12.9 Haiwang Hydrocyclone

- 12.10 KREBS

- 12.11 Mahle Industrial Filtration

- 12.12 Mikropor

- 12.13 Multotec

- 12.14 Sulzer

- 12.15 The Weir Group

水力旋流器市場:按類型、材質、壓力等級、技術、終端用戶產業、應用和銷售管道分類-2026-2032年全球市場預測

水力旋流器市場:按類型、材質、壓力等級、技術、終端用戶產業、應用和銷售管道分類-2026-2032年全球市場預測 沉澱和離心分離市場報告:按產品和地區分類 2026-2034 年工業離心分離機市場:按類型、物質分離、速度與應用分類-2026-2032年全球市場預測離心分離器市場:按類型、容量、材質、設計、最終用戶和銷售管道分類-2026-2032年全球市場預測澱粉回收系統市場:按設備類型、終端用戶產業、分銷管道和應用分類的全球預測,2026-2032年濕式離心離合器市場:依產品類型、摩擦材料、額定功率、銷售管道、應用、最終用戶分類,全球預測(2026-2032年)鑽井液減速器市場:按類型、設備配置、技術、鑽井應用、最終用戶分類,全球預測(2026-2032年)旋風乾燥機市場:依技術、運作模式、產能、終端用戶產業及通路分類,全球預測,2026-2032年鑽井泥漿界面活性劑市場按應用、化學成分、功能類型和最終用途產業分類,全球預測(2026-2032年)離心式油分離器市場按類型、材料、流量、終端用戶產業、應用和銷售管道,全球預測,2026-2032年

沉澱和離心分離市場報告:按產品和地區分類 2026-2034 年工業離心分離機市場:按類型、物質分離、速度與應用分類-2026-2032年全球市場預測離心分離器市場:按類型、容量、材質、設計、最終用戶和銷售管道分類-2026-2032年全球市場預測澱粉回收系統市場:按設備類型、終端用戶產業、分銷管道和應用分類的全球預測,2026-2032年濕式離心離合器市場:依產品類型、摩擦材料、額定功率、銷售管道、應用、最終用戶分類,全球預測(2026-2032年)鑽井液減速器市場:按類型、設備配置、技術、鑽井應用、最終用戶分類,全球預測(2026-2032年)旋風乾燥機市場:依技術、運作模式、產能、終端用戶產業及通路分類,全球預測,2026-2032年鑽井泥漿界面活性劑市場按應用、化學成分、功能類型和最終用途產業分類,全球預測(2026-2032年)離心式油分離器市場按類型、材料、流量、終端用戶產業、應用和銷售管道,全球預測,2026-2032年