|

市場調查報告書

商品編碼

1801891

智慧電錶市場機會、成長動力、產業趨勢分析及2025-2034年預測Smart Electric Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

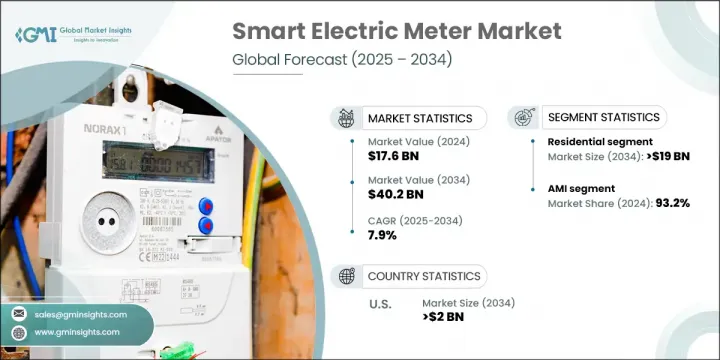

2024年,全球智慧電錶市場規模達176億美元,預計到2034年將以7.9%的複合年成長率成長,達到402億美元。這一成長主要得益於全球對先進電網技術投資的不斷增加。隨著各國努力改造老舊電力基礎設施、減少停電事故並支持再生能源併網,智慧電錶正成為這些現代化系統的核心組成部分。這些電錶為公用事業公司提供精細的用電資料,有助於最佳化電網效率、即時識別服務問題並降低整體營運成本。

物聯網、無線技術和資料分析領域的持續創新正在提升智慧電錶的經濟性和效能。消費者現在可以即時洞察能源使用情況,從而改善需求管理,降低能源成本,並更好地支持電網平衡。智慧電錶也正與家庭自動化和需量反應平台一起被採用,進一步提升其在現代能源生態系統中的作用。隨著減少碳排放的緊迫性日益增強,這些設備在實現高效配電和推廣清潔能源方面正發揮著重要作用。財政激勵措施、政策強制措施以及公用事業驅動的推廣活動持續加速全球各地區的智慧電錶應用,進一步鞏固了智慧電錶市場的整體格局。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 176億美元 |

| 預測值 | 402億美元 |

| 複合年成長率 | 7.9% |

到2034年,住宅領域市場規模將達到190億美元,這得益於個人住宅和多戶住宅對智慧電錶需求的不斷成長。對能源效率、太陽能整合和精準計費的日益重視是該領域擴張的主要因素。隨著太陽能光電裝置的增加,尤其是在住宅領域,智慧電錶有助於簡化能源監控,並允許用戶做出數據驅動的消費決策。公用事業公司也擴大安裝智慧電錶,以加強與客戶的溝通,並實現社區日益成長的永續發展目標。

從技術角度來看,市場分為先進計量基礎設施 (AMI) 和自動抄表 (AMR)。 AMI 領域在 2024 年佔據了 93.2% 的市場佔有率,並憑藉其提供雙向通訊、即時資料傳輸以及與公用事業管理系統無縫整合的能力繼續保持領先地位。 AMR 可以提高效率並減少人為錯誤,而 AMI 則可以實現能源網路的全面數位轉型,並增強對能源流的控制。

到2034年,美國智慧電錶市場規模將達到20億美元,這得益於不斷演變的法規,這些法規要求現代電網系統能夠管理日益成長的再生能源投入。作為全球最發達的經濟體之一,美國在全球貿易中扮演著重要角色,這也影響著智慧電網技術(例如智慧電錶)的開發和部署。對穩定電力傳輸的追求,尤其是在電動車普及率和再生能源併網率不斷上升的各州,正在推動更廣泛的電錶安裝。

積極影響全球智慧電錶市場的關鍵參與者包括西門子、蘭吉爾、施耐德電氣、霍尼韋爾國際和 Itron。智慧電錶產業的領先公司正致力於透過與公用事業供應商和智慧電網專案的合作來擴大其地理覆蓋範圍。各公司正大力投資研發,以提高其電錶的準確性、連接性和功能性,並整合人工智慧、邊緣運算和物聯網功能,以保持競爭力。客製化以滿足區域合規性以及與電網基礎設施的互通性也是一項核心優先事項。 Itron 和施耐德電氣等公司優先考慮基於 AMI 的解決方案,以滿足即時監控和數位電網管理的需求。策略性收購、與政府機構簽訂的長期合約以及參與再生能源推廣正在進一步鞏固其市場地位。此外,企業正在強調網路安全和資料隱私,以在公用事業公司和最終消費者之間建立信任。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 進出口貿易分析

- 各地區價格趨勢分析(美元/單位)

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買家的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL分析

- 新興機會和趨勢

- 數位化和物聯網整合

- 新興市場滲透

- 投資分析及未來展望

第4章:競爭格局

- 介紹

- 按地區分析公司市場佔有率

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 策略舉措

- 競爭性基準描述

- 策略儀表板

- 創新與技術格局

第5章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 住宅

- 單身家庭

- 多戶家庭

- 商業的

- 教育

- 衛生保健

- 零售

- 物流與運輸

- 辦公室

- 飯店業

- 其他

- 公用事業

第6章:市場規模及預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 急性心肌梗塞

- 射頻

- PLC

- 蜂巢

- 抗腫瘤藥物

第7章:市場規模及預測:依階段,2021 - 2034

- 主要趨勢

- 單身的

- 三

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 瑞典

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第9章:公司簡介

- ABB

- Aclara Technologies LLC

- Advanced Electronics Company (AEC)

- Apator SA

- Circutor

- Cisco Systems, Inc.

- CyanConnode

- Enel Spa.

- General Electric

- Honeywell International Inc.

- Iskraemeco Group

- Itron Inc.

- Kamstrup

- Landis + Gyr

- Larsen & Toubro Limited

- Mitsubishi Electric Corporation

- Osaki Electric Co., Ltd.

- Schneider Electric

- Sensus

- Siemens

- Toshiba

- Trinity Energy Systems

The Global Smart Electric Meter Market was valued at USD 17.6 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 40.2 billion by 2034. This growth is largely propelled by increasing global investments in advanced grid technologies. As nations work to modernize outdated power infrastructure, reduce blackouts, and support renewable integration, smart meters are becoming a core component of these modern systems. These meters provide utilities with granular consumption data that helps optimize grid efficiency, identify service issues in real time, and lower overall operating expenses.

Continuous innovation in IoT, wireless technology, and data analytics is improving the affordability and performance of smart meters. Consumers now benefit from real-time insights into energy usage, leading to better demand management, reduced energy costs, and greater support for grid balancing. Smart meters are also being adopted alongside home automation and demand-response platforms, further increasing their role in modern energy ecosystems. As the urgency to cut carbon emissions grows, these devices are becoming instrumental in enabling efficient power distribution and promoting cleaner energy. Financial incentives, policy mandates, and utility-driven rollouts continue to accelerate adoption across global regions, reinforcing the overall smart electric meter market landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $40.2 Billion |

| CAGR | 7.9% |

The residential sector will reach USD 19 billion by 2034, driven by the rising demand for smart meters in individual homes and multifamily dwellings. Increasing emphasis on energy efficiency, solar energy integration, and accurate billing are major factors behind this segment's expansion. As solar PV installations rise, particularly in residential spaces, smart meters help streamline energy monitoring and allow users to make data-driven consumption decisions. Utilities are also increasingly installing smart meters to enhance communication with customers and meet growing sustainability goals across neighborhoods.

Technologically, the market is split into advanced metering infrastructure (AMI) and automatic meter reading (AMR). The AMI segment held a 93.2% share in 2024 and continues to lead due to its ability to provide two-way communication, real-time data transmission, and seamless integration with utility management systems. While AMR improves efficiency and reduces human error, AMI enables full digital transformation of energy networks and enhances control over energy flows.

United States Smart Electric Meter Market will reach USD 2 billion by 2034, supported by evolving regulations that require modern grid systems to manage growing renewable energy inputs. With one of the world's most sophisticated economies, the US plays a major role in global trade, which also influences the development and deployment of smart grid technologies like these meters. The push for stable power delivery, especially in states with rising electric vehicle adoption and renewable integration, is driving broader meter installations.

Key players actively shaping the Global Smart Electric Meter Market include Siemens, Landis + Gyr, Schneider Electric, Honeywell International, and Itron. Leading companies in the smart electric meter industry are focusing on expanding their geographic reach through partnerships with utility providers and smart grid projects. Firms are investing heavily in R&D to enhance the accuracy, connectivity, and functionality of their meters, integrating AI, edge computing, and IoT capabilities to stay competitive. Customization for regional compliance and interoperability with grid infrastructure is also a core priority. Players like Itron and Schneider Electric are prioritizing AMI-based solutions to cater to demand for real-time monitoring and digital grid management. Strategic acquisitions, long-term contracts with government bodies, and participation in renewable energy rollouts are further strengthening market positions. Additionally, businesses are emphasizing cybersecurity and data privacy to build trust among utilities and end consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Import/Export trade analysis

- 3.4 Price trend analysis, by region (USD/Unit)

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.2.1 Single family

- 5.2.2 Multi family

- 5.3 Commercial

- 5.3.1 Education

- 5.3.2 Healthcare

- 5.3.3 Retail

- 5.3.4 Logistics & transportation

- 5.3.5 Offices

- 5.3.6 Hospitality

- 5.3.7 Others

- 5.3.8 Utility

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 AMI

- 6.2.1 RF

- 6.2.2 PLC

- 6.2.3 Cellular

- 6.3 AMR

Chapter 7 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Single

- 7.3 Three

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Sweden

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 South Africa

- 8.5.4 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Mexico

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Aclara Technologies LLC

- 9.3 Advanced Electronics Company (AEC)

- 9.4 Apator SA

- 9.5 Circutor

- 9.6 Cisco Systems, Inc.

- 9.7 CyanConnode

- 9.8 Enel Spa.

- 9.9 General Electric

- 9.10 Honeywell International Inc.

- 9.11 Iskraemeco Group

- 9.12 Itron Inc.

- 9.13 Kamstrup

- 9.14 Landis + Gyr

- 9.15 Larsen & Toubro Limited

- 9.16 Mitsubishi Electric Corporation

- 9.17 Osaki Electric Co., Ltd.

- 9.18 Schneider Electric

- 9.19 Sensus

- 9.20 Siemens

- 9.21 Toshiba

- 9.22 Trinity Energy Systems

智慧電錶市場:2026-2032年全球市場預測(按階段、通訊技術、測量基礎設施、部署、應用和分銷管道分類)

智慧電錶市場:2026-2032年全球市場預測(按階段、通訊技術、測量基礎設施、部署、應用和分銷管道分類) 2026年智慧電網電力分錶計量全球市場報告

2026年智慧電網電力分錶計量全球市場報告 智慧電錶市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測2026年全球三相智慧電錶市場報告2026年全球智慧電錶市場報告全球電動車充電智慧電錶市場(按充電器額定功率、連接方式、功率類型、電錶類型、最終用戶、應用和分銷管道分類)預測(2026-2032年)

智慧電錶市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測2026年全球三相智慧電錶市場報告2026年全球智慧電錶市場報告全球電動車充電智慧電錶市場(按充電器額定功率、連接方式、功率類型、電錶類型、最終用戶、應用和分銷管道分類)預測(2026-2032年) 智慧電錶市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測

智慧電錶市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測 日本智慧電錶市場報告:按類型、相位、最終用戶和地區分類(2026-2034年)

日本智慧電錶市場報告:按類型、相位、最終用戶和地區分類(2026-2034年) 智慧電錶市場規模、佔有率及成長分析(按類型、技術、組件、最終用戶、通訊類型和地區分類)-2026-2033年產業預測全球智慧電錶市場-2025-2030年預測

智慧電錶市場規模、佔有率及成長分析(按類型、技術、組件、最終用戶、通訊類型和地區分類)-2026-2033年產業預測全球智慧電錶市場-2025-2030年預測