|

市場調查報告書

商品編碼

1801875

水下無人機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Underwater Drones Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

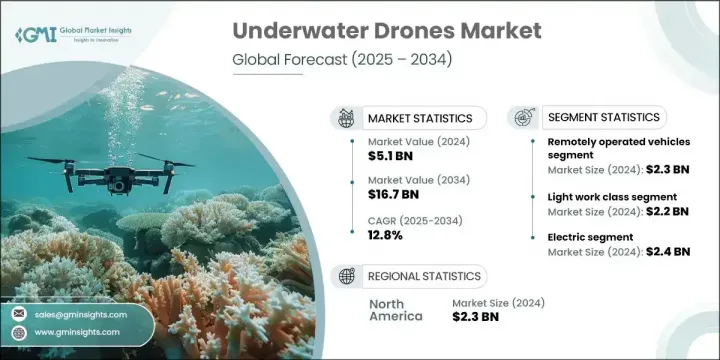

2024年,全球水下無人機市場規模達51億美元,預估年複合成長率達12.8%,2034年將達167億美元。這一成長主要得益於海底探勘需求的不斷成長、海上油氣項目投資的不斷增加、海上安全形勢的改善以及可再生能源項目的整合。此外,自主性、推進系統和成像技術的不斷改進,也推動了水下無人機在商業和國防領域的更廣泛應用。

重塑這一領域的關鍵趨勢是人們對電力推進系統的日益青睞。這些升級增強了任務範圍,減少了噪音,並提高了能源效率,使電動水下無人機成為一系列應用的理想選擇。透過整合鋰離子電池、無刷直流馬達和超級電容器,現代電動無人機在某些任務中可以運行超過72小時。這種轉變在中層水域和近岸作業中尤其重要,因為低噪音和高效率的表現至關重要。同時,人們對自主水下航行器(AUV)的興趣也日益濃厚,它們利用機載導航、感測器和任務軟體獨立運行,無需操作員即時輸入即可實現精確定位。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 51億美元 |

| 預測值 | 167億美元 |

| 複合年成長率 | 12.8% |

2024年,遙控潛水器 (ROV) 市場價值達23億美元。由於石油天然氣、國防和基礎設施檢查領域對即時水下作業的需求日益成長,該市場正在快速成長。 ROV 配備多功能工具系統,具有強大的有效載荷能力,並為操作員提供全手動控制,使其成為深水檢查、維護工作和水下打撈任務的理想選擇。

2024年,輕型工作級無人機市場規模達22億美元。這類無人機因其操作靈活性、經濟實惠以及在執行巡檢和輕型干預任務方面的高效性而被廣泛採用。它們與感測器和機械臂的良好相容性,加上較低的部署複雜性和極低的地面支撐需求,使其非常適合在狹窄和惡劣的環境中作業。為了滿足不斷變化的營運需求,製造商正專注於即插即用設計、邊緣AI整合和改進的繫繩控制系統,以服務港口管理、基礎設施監控和海上承包等行業。

到2034年,加拿大水下無人機市場規模將達到7.751億美元。這一成長主要得益於加拿大不斷擴張的海上能源業務、不斷加強的海域監測以及不斷深化的海洋科學投資。無人機在冰下導航、遠端海底監測和棲息地測繪的應用持續成長。建議設備開發人員優先考慮堅固耐用、能夠在冷水下作業的無人機系統,並配備模組化感測器配置,以滿足科學探索和國防應用的需求。

全球水下無人機市場的主要參與者包括PowerRay、Gavia AUV、SRV-8 ROV、Neptune ROV、Phantom ROV系列、FIFISH V6、Flying Nodes AUV、Marlin AUV、HUGIN AUV、Seaeye Falcon ROV、Sibiu Pro、SeaDrone ROV、SeaCat AUV、Seunye Falcon ROV、Sibiu Pro、SeaDrone ROV、SeaCat AUV1 ROV、Eelume 海底機器人和 Absolute Ocean AUV。

水下無人機領域的公司正透過多管齊下的策略來鞏固其競爭地位。他們高度重視研發,以提升自主性、感測器整合、電池壽命和推進技術。製造商優先考慮模組化設計,以便針對特定任務(例如探勘、國防、檢查或科學研究)進行快速客製化。與政府機構、能源公司和海洋研究所建立的策略合作夥伴關係有助於公司獲得長期合約。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 海洋探索需求不斷成長

- 擴大海上石油和天然氣活動

- 海上安全和監視需求

- 再生能源項目投資不斷成長

- 自主性和成像技術的進步

- 陷阱與挑戰

- 有限的電池壽命和電源管理

- 先進水下無人機成本高昂

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 遙控車輛

- 自主水下航行器

- 混合動力水下航行器

第6章:市場估計與預測:依產品類別,2021 - 2034 年

- 主要趨勢

- 微課

- 中小型班

- 輕工班

- 重工班

第7章:市場估計與預測:按推進系統,2021 - 2034 年

- 主要趨勢

- 電的

- 機械的

- 混合

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 國防和安全

- 海軍監視

- 地雷對策

- 反潛戰

- 水下情報與偵察

- 搜救任務

- 其他

- 科學研究與探索

- 海洋學研究

- 海洋生物多樣性監測

- 海底測繪

- 氣候與環境研究

- 基礎設施檢查和維護

- 管道和鑽機檢查

- 水下電纜監測

- 大壩和橋樑檢查

- 港口和港灣維護

- 核設施檢查

- 其他

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- 全球關鍵參與者

- General Dynamics Mission Systems

- Deep Ocean Engineering, Inc.

- Nido Robotics

- Oceanbotics

- Neptune Robotics

- Terradepth

- SeaDrone Inc.

- Edgerov (Notilo Plus)

- Autonomous Robotics Ltd.

- 區域關鍵參與者

- 北美洲

- Oceaneering International, Inc.

- Lockheed Martin Corporation

- Teledyne Marine

- 歐洲

- Kongsberg Maritime

- Saab Group

- Atlas Elektronik

- Asia-Pacific

- QYSEA Technology

- PowerVision Inc.

- Youcan Robotics(Shanghai) Co., Ltd.

- 北美洲

- 顛覆者/利基市場參與者

- Blueye Robotics

- Eelume AS

The Global Underwater Drones Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 16.7 billion by 2034. The expansion is largely supported by increasing demand for subsea exploration, rising investments in offshore oil and gas projects, maritime security enhancements, and the integration of renewable energy ventures. Additionally, constant improvements in autonomy, propulsion systems, and imaging technologies are driving broader market adoption across both commercial and defense sectors.

A key trend reshaping this space is the growing preference for electric propulsion systems. These upgrades enhance mission range, reduce acoustic footprint, and improve energy efficiency, making electric-powered underwater drones ideal for a range of applications. With the integration of lithium-ion batteries, brushless DC motors, and supercapacitors, modern electric drones now operate over 72 hours in certain missions. This transformation is especially valuable in mid-water and nearshore operations where low-noise and high-efficiency performance is essential. At the same time, there's a surge in interest for autonomous underwater vehicles (AUVs), which operate independently using onboard navigation, sensors, and mission software, enabling precision without real-time operator input.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 billion |

| Forecast Value | $16.7 billion |

| CAGR | 12.8% |

In 2024, the remotely operated vehicle (ROV) segment was valued at USD 2.3 billion. This segment is growing rapidly due to the rising need for real-time underwater operations in oil and gas, defense, and infrastructure inspections. ROVs are equipped with versatile tool systems, have strong payload capacities, and provide operators with full manual control, making them ideal for deepwater inspections, maintenance work, and underwater recovery tasks.

The light work-class drone segment generated USD 2.2 billion in 2024. These drones are widely adopted due to their operational flexibility, affordability, and effectiveness in performing inspection and light intervention missions. Their adaptability with sensors and manipulators, along with low deployment complexity and minimal surface support needs, makes them suitable for confined and harsh environments. To support evolving operational needs, manufacturers are focusing on plug-and-play designs, edge AI integration, and improved tether control systems to serve industries such as port management, infrastructure surveillance, and offshore contracting.

Canada Underwater Drones Market will reach USD 775.1 million by 2034. This growth is driven by the nation's expanding offshore energy operations, increased maritime territorial monitoring, and deepening investments in marine science. The use of drones for under-ice navigation, remote subsea monitoring, and habitat mapping continues to rise. Equipment developers are advised to prioritize ruggedized, cold-water-capable drone systems with modular sensor configurations suitable for both scientific exploration and defense applications.

Key players in the Global Underwater Drones Market include PowerRay, Gavia AUV, SRV-8 ROV, Neptune ROV, Phantom ROV Series, FIFISH V6, Flying Nodes AUV, Marlin AUV, HUGIN AUV, Seaeye Falcon ROV, Sibiu Pro, SeaDrone ROV, SeaCat AUV, Seasam ROV, BW Space Pro, Blueye X3, Bluefin-21 AUV, Oceaneering ROVs, Eelume Subsea Robot, and Absolute Ocean AUV.

Companies in the underwater drones space are reinforcing their competitive position through multi-faceted strategies. A strong emphasis is placed on R&D to advance autonomy, sensor integration, battery longevity, and propulsion technology. Manufacturers are prioritizing modular designs to enable rapid customization for specific missions, such as exploration, defense, inspection, or scientific research. Strategic partnerships with government bodies, energy firms, and marine institutes are helping companies secure long-term contracts.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type trends

- 2.2.2 Product class trends

- 2.2.3 Propulsion system trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising Demand for Ocean Exploration

- 3.3.1.2 Expansion of Offshore Oil & Gas Activities

- 3.3.1.3 Maritime Security and Surveillance Needs

- 3.3.1.4 Growing Investment in Renewable Energy Projects

- 3.3.1.5 Technological Advancements in Autonomy & Imaging

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 Limited Battery Life and Power Management

- 3.3.2.2 High Cost of Advanced Underwater Drones

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Defense budget analysis

- 3.14 Global defense spending trends

- 3.15 Regional defense budget allocation

- 3.15.1 North america

- 3.15.2 Europe

- 3.15.3 Asia Pacific

- 3.15.4 Middle East and Africa

- 3.15.5 Latin america

- 3.16 Key defense modernization programs

- 3.17 Budget forecast (2025-2034)

- 3.17.1 Impact on industry growth

- 3.17.2 Defense budgets by country

- 3.18 Supply chain resilience

- 3.19 Geopolitical analysis

- 3.20 Workforce analysis

- 3.21 Digital transformation

- 3.22 Mergers, acquisitions, and strategic partnerships landscape

- 3.23 Risk assessment and management

- 3.24 Major contract awards (2021-2024)

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Type, 2021 - 2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Remotely operated vehicles

- 5.3 Autonomous underwater vehicles

- 5.4 Hybrid underwater vehicles

Chapter 6 Market estimates and forecast, by Product Class, 2021 - 2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Micro class

- 6.3 Small and medium class

- 6.4 Light work class

- 6.5 Heavy work class

Chapter 7 Market estimates and forecast, by Propulsion System, 2021 - 2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Electric

- 7.3 Mechanical

- 7.4 Hybrid

Chapter 8 Market estimates and forecast, by Application, 2021 - 2034 (USD Billion & Units)

- 8.1 Key trends

- 8.2 Defense and security

- 8.2.1 Naval surveillance

- 8.2.2 Mine countermeasures

- 8.2.3 Anti-submarine warfare

- 8.2.4 Underwater intelligence and reconnaissance

- 8.2.5 Search and rescue missions

- 8.2.6 Others

- 8.3 Scientific research and exploration

- 8.3.1 Oceanographic studies

- 8.3.2 Marine biodiversity monitoring

- 8.3.3 Seabed mapping

- 8.3.4 Climate and environmental studies

- 8.4 Infrastructure inspection and maintenance

- 8.4.1 Pipeline and rig inspection

- 8.4.2 Underwater cable monitoring

- 8.4.3 Dam and bridge inspection

- 8.4.4 Port and harbour maintenance

- 8.4.5 Nuclear facility inspection

- 8.4.6 Others

- 8.5 Others

Chapter 9 Market estimates and forecast, by Region, 2021 - 2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 General Dynamics Mission Systems

- 10.1.2 Deep Ocean Engineering, Inc.

- 10.1.3 Nido Robotics

- 10.1.4 Oceanbotics

- 10.1.5 Neptune Robotics

- 10.1.6 Terradepth

- 10.1.7 SeaDrone Inc.

- 10.1.8 Edgerov (Notilo Plus)

- 10.1.9 Autonomous Robotics Ltd.

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Oceaneering International, Inc.

- 10.2.1.2 Lockheed Martin Corporation

- 10.2.1.3 Teledyne Marine

- 10.2.2 Europe

- 10.2.2.1 Kongsberg Maritime

- 10.2.2.2 Saab Group

- 10.2.2.3 Atlas Elektronik

- 10.2.3 Asia-Pacific

- 10.2.3.1 QYSEA Technology

- 10.2.3.2 PowerVision Inc.

- 10.2.3.3 Youcan Robotics(Shanghai) Co., Ltd.

- 10.2.1 North America

- 10.3 Disruptors / Niche Players

- 10.3.1 Blueye Robotics

- 10.3.2 Eelume AS

2026年全球水下無人機市場報告

2026年全球水下無人機市場報告 水下雷射雷達市場:按技術、範圍、組件、用例、部署和應用分類,全球預測(2026-2032年)

水下雷射雷達市場:按技術、範圍、組件、用例、部署和應用分類,全球預測(2026-2032年) 水下無人機市場規模、佔有率和成長分析(按類型、推進系統、應用和地區分類)-2026-2033年產業預測

水下無人機市場規模、佔有率和成長分析(按類型、推進系統、應用和地區分類)-2026-2033年產業預測 水下無人機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、推進系統、地區和競爭格局分類,2020-2030年預測水下雷射雷達和聲納解決方案市場(按技術、組件、部署模式、頻率範圍、深度能力和應用)—2025-2030 年全球預測

水下無人機市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、應用、推進系統、地區和競爭格局分類,2020-2030年預測水下雷射雷達和聲納解決方案市場(按技術、組件、部署模式、頻率範圍、深度能力和應用)—2025-2030 年全球預測 全球水下無人機市場:依類型、應用、最終用戶、地區、機會及預測,2018-2032

全球水下無人機市場:依類型、應用、最終用戶、地區、機會及預測,2018-2032 水下無人機市場按類型、應用和地區分類

水下無人機市場按類型、應用和地區分類