|

市場調查報告書

商品編碼

1801864

灌漿與錨固市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Grouts and Anchors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

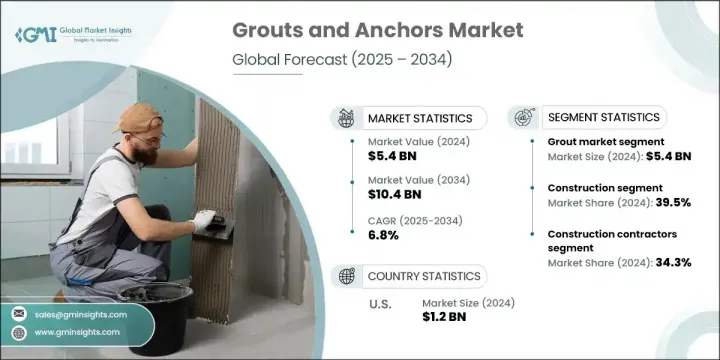

2024年,全球灌漿料和錨固材料市場價值為54億美元,預計到2034年將以6.8%的複合年成長率成長,達到104億美元。市場擴張與城鎮化進程加快、建築活動激增以及對基礎設施韌性的日益重視密切相關。灌漿料和錨固材料是確保結構完整性的重要材料,它們能夠穩定地基、固定裝置並填補現代建築和改造項目中的空隙。這些部件是商業建築、橋樑、隧道等民用基礎設施安全和使用壽命的基礎。

隨著全球對住宅、商業和公共基礎設施的投資加速,對高性能耐用建築材料的需求也日益成長。人們對技術先進且易於應用的錨固和灌漿解決方案的日益青睞也正在塑造該行業的發展。此外,無論是在已開發經濟體還是新興經濟體,對不斷演變的建築規範和安全法規的合規要求也持續推動市場的發展動能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 54億美元 |

| 預測值 | 104億美元 |

| 複合年成長率 | 6.8% |

2024年,灌漿料佔據了54.3%的市場佔有率,佔據主導地位。這類材料被廣泛用於穩定結構、填充空腔和改善荷載分佈。灌漿料以其強度和適應性而聞名,對於結構修復、地基加固以及對耐久性和精度要求極高的施工任務至關重要。其長期可靠性使其成為小型維修和大型基礎設施專案的首選解決方案。

由於全球對住宅、工業和商業開發項目的需求持續成長,建築業在2024年的市佔率為39.5%。由於建築商追求更持久耐用、符合規範的建築,他們正在轉向高品質的灌漿和錨固產品,以滿足性能和安全方面的期望。向永續建築材料的轉變也在加強先進灌漿和錨固產品在現代建築實踐中的應用。

美國灌漿和錨固市場佔88.7%的市場佔有率,2024年產值達12億美元。這一領先地位源於全國範圍內對基礎設施升級和新建項目的大規模投資。正在進行的聯邦基礎設施計劃持續推動對可靠的灌漿和錨固材料的需求,這些材料具有強度高、使用壽命長和更強的韌性。隨著基礎設施老化和氣候適應能力變得至關重要,建築商持續尋求能夠滿足不斷變化的結構需求的高性能產品。

影響全球灌漿和錨固市場的關鍵參與者包括喜利得股份公司 (Hilti AG)、馬貝股份公司 (MAPEI SpA)、西卡股份公司 (Sika AG)、巴斯夫股份公司 (BASF SE) 和富斯樂國際 (Fosroc International)。為了鞏固市場地位,灌漿和錨固領域的領先公司正專注於多項策略措施。這些措施包括擴大研發規模,開發固化時間更快、耐久性更高、永續性更強的創新材料。許多公司正在投資產品客製化和先進的化學配方,以滿足特定建築應用的需求。策略性合併、區域合作和收購也是擴大地域覆蓋範圍的常用方法。此外,各公司也強調對承包商的培訓計劃,以促進產品採用並確保其正確應用,同時整合數位工具,提供精準的配方建議和專案規劃。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 轉向永續建築

- 採用混合和智慧技術

- 注射黏合劑錨引領成長

- 產業陷阱與挑戰

- 原物料供應不穩定

- 監理合規壓力

- 市場機會

- 模組化和預製建築的興起

- 客製化和特色產品

- 與建築技術公司合作

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 粗糧市場

- 水泥基灌漿料

- 環氧灌漿料

- 化學灌漿

- 其他灌漿類型

- 聚氨酯灌漿料

- 丙烯酸灌漿

- 錨市場

- 機械錨

- 化學錨栓

- 黏接錨栓

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 建造

- 住宅

- 商業的

- 工業的

- 基礎設施

- 運輸

- 橋樑和高速公路

- 隧道和地下

- 鐵路基礎設施

- 機場建設

- 實用工具

- 水和廢水

- 發電

- 電信

- 能源基礎設施

- 運輸

- 海洋和近海

- 港口和港灣建設

- 海上平台

- 海岸保護

- 船舶維修保養

- 採礦和地下應用

- 礦井支護系統

- 地下開挖

- 隧道穩定

- 地基改良

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 建築承包商

- 總承包商

- 專業承包商

- 基礎設施開發商

- 工業最終用途

- 分銷商和零售商

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- MEA 其餘地區

第9章:公司簡介

- Arkema Group (via Bostik)

- BASF SE (Master Builders Solutions)

- Fosroc International Limited

- HB Fuller Company

- Henkel AG & Co. KGaA (Loctite brand)

- Hilti AG

- Laticrete International

- MAPEI SpA

- Saint-Gobain Weber

- Sika AG

- Stanley Black & Decker

- Wurth Group

The Global Grouts and Anchors Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 10.4 billion by 2034. Market expansion is strongly tied to increased urbanization, a surge in construction activity, and the growing emphasis on infrastructure resilience. Grouts and anchors are essential materials that ensure structural integrity by stabilizing foundations, securing fixtures, and filling gaps across both modern construction and retrofitting projects. These components are foundational to the safety and longevity of civil infrastructure, including commercial buildings, bridges, tunnels, and more.

As global investments in residential, commercial, and public infrastructure accelerate, so does the demand for high-performance and durable construction materials. The growing preference for technologically advanced and easy-to-apply anchoring and grouting solutions is also shaping the industry. Additionally, the push for compliance with evolving building codes and safety regulations continues to drive market momentum across both developed and emerging economies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.4 Billion |

| Forecast Value | $10.4 Billion |

| CAGR | 6.8% |

The grouts segment dominated with a 54.3% market share in 2024, as these materials are widely used to stabilize structures, fill cavities, and improve load distribution. Known for their strength and adaptability, grouts are essential for structural rehabilitation, foundation reinforcements, and demanding construction tasks requiring durability and precision. Their long-term reliability makes them the go-to solution in both small-scale repairs and large-scale infrastructure projects.

The construction segment held a 39.5% share in 2024, owing to constant global demand for residential, industrial, and commercial developments. As builders aim for longer-lasting, code-compliant buildings, they are turning to high-quality grouting and anchoring products to meet performance and safety expectations. The shift toward sustainable construction materials is also playing a role in reinforcing the use of advanced grouts and anchors in modern building practices.

U.S. Grouts and Anchors Market held an 88.7% share and generated USD 1.2 billion in 2024. This leadership position stems from large-scale investments in infrastructure upgrades and new construction across the country. Ongoing federal infrastructure initiatives are sustaining the demand for reliable grouting and anchoring materials that offer strength, longevity, and improved resilience. As infrastructure ages and climate resilience becomes critical, builders continue to seek high-performance products that align with evolving structural demands.

Key players shaping the Global Grouts and Anchors Market include Hilti AG, MAPEI S.p.A., Sika AG, BASF SE, and Fosroc International. To strengthen their market position, leading companies in the grouts and anchors space are focusing on several strategic initiatives. These include expanding R&D to develop innovative materials with faster curing times, higher durability, and sustainability features. Many are investing in product customization and advanced chemical formulations to meet the needs of specific construction applications. Strategic mergers, regional partnerships, and acquisitions are also common approaches to widen their geographical footprint. Furthermore, companies are emphasizing on training programs for contractors to boost product adoption and ensure proper application, while integrating digital tools for precise formulation recommendations and project planning.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward sustainable construction

- 3.2.1.2 Adoption of hybrid and smart technologies

- 3.2.1.3 Injectable adhesive anchors leading growth

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material supply instability

- 3.2.2.2 Regulatory compliance pressure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in modular and prefabricated construction

- 3.2.3.2 Customization and specialty products

- 3.2.3.3 Collaboration with construction technology firms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Grouts market

- 5.2.1 Cementitious grouts

- 5.2.2 Epoxy grouts

- 5.2.3 Chemical grouts

- 5.2.4 Other grout types

- 5.2.4.1 Polyurethane grouts

- 5.2.4.2 Acrylic grouts

- 5.3 Anchors market

- 5.3.1 Mechanical anchors

- 5.3.2 Chemical anchors

- 5.3.3 Adhesive anchors

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Construction

- 6.2.1 Residential

- 6.2.2 Commercial

- 6.2.3 Industrial

- 6.3 Infrastructure

- 6.3.1 Transportation

- 6.3.1.1 Bridges and highways

- 6.3.1.2 Tunnels and underground

- 6.3.1.3 Railway infrastructure

- 6.3.1.4 Airport construction

- 6.3.2 Utilities

- 6.3.2.1 Water and wastewater

- 6.3.2.2 Power generation

- 6.3.2.3 Telecommunications

- 6.3.2.4 Energy infrastructure

- 6.3.1 Transportation

- 6.4 Marine and offshore

- 6.4.1 Port and harbor construction

- 6.4.2 Offshore platforms

- 6.4.3 Coastal protection

- 6.4.4 Marine repair and maintenance

- 6.5 Mining and underground applications

- 6.5.1 Mine support systems

- 6.5.2 Underground excavation

- 6.5.3 Tunnel stabilization

- 6.5.4 Ground improvement

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Construction Contractors

- 7.2.1 General Contractors

- 7.2.2 Specialty Contractors

- 7.3 Infrastructure Developers

- 7.4 Industrial End Use

- 7.5 Distributors and Retailers

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

- 8.6.4 Rest of MEA

Chapter 9 Company Profiles

- 9.1 Arkema Group (via Bostik)

- 9.2 BASF SE (Master Builders Solutions)

- 9.3 Fosroc International Limited

- 9.4 H.B. Fuller Company

- 9.5 Henkel AG & Co. KGaA (Loctite brand)

- 9.6 Hilti AG

- 9.7 Laticrete International

- 9.8 MAPEI S.p.A.

- 9.9 Saint-Gobain Weber

- 9.10 Sika AG

- 9.11 Stanley Black & Decker

- 9.12 Wurth Group

錨固與水泥漿市場-2026-2032年全球市場預測

錨固與水泥漿市場-2026-2032年全球市場預測 2026年全球聚氨酯填充服務市場報告低黏度環氧水泥漿市場(依樹脂類型、應用、最終用戶和銷售管道)——2026-2032年全球預測水泥基瓷磚接縫化合物市場按產品類型、分銷管道、包裝規格、應用和最終用戶分類-2026-2032年全球預測環氧樹脂瓷磚接縫化合物市場按產品類型、產品形態、接縫寬度、應用、最終用戶和配銷通路分類——2026-2032年全球預測

2026年全球聚氨酯填充服務市場報告低黏度環氧水泥漿市場(依樹脂類型、應用、最終用戶和銷售管道)——2026-2032年全球預測水泥基瓷磚接縫化合物市場按產品類型、分銷管道、包裝規格、應用和最終用戶分類-2026-2032年全球預測環氧樹脂瓷磚接縫化合物市場按產品類型、產品形態、接縫寬度、應用、最終用戶和配銷通路分類——2026-2032年全球預測 磁磚接縫市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測

磁磚接縫市場規模、佔有率及成長分析(按類型、應用和地區分類)-2026-2033年產業預測 環氧水泥漿市場規模、佔有率和成長分析(按類型、產業、應用、最終用途產業和地區分類)-2026-2033年產業預測2025年環氧水泥漿全球市場報告

環氧水泥漿市場規模、佔有率和成長分析(按類型、產業、應用、最終用途產業和地區分類)-2026-2033年產業預測2025年環氧水泥漿全球市場報告 全球即用型水泥漿和黏合劑市場

全球即用型水泥漿和黏合劑市場 水泥基灌漿料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

水泥基灌漿料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測