|

市場調查報告書

商品編碼

1801828

可吸收手術縫線市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Absorbable Surgical Sutures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

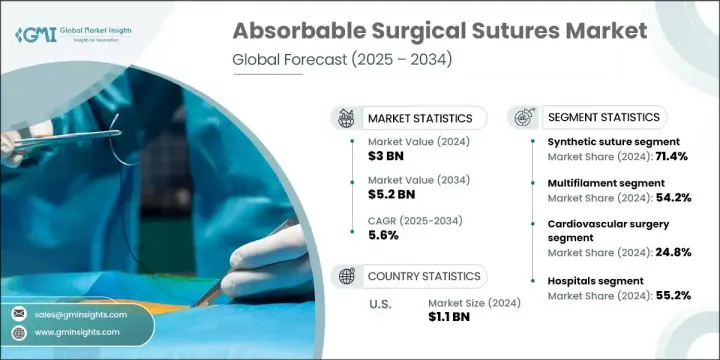

2024年,全球可吸收手術縫線市場規模達30億美元,預計2034年將以5.6%的複合年成長率成長,達到52億美元。市場成長的驅動力包括全球外科手術數量的急劇上升、慢性病發病率的上升、縫合技術的進步以及婦科手術數量的激增。隨著醫療保健系統更加重視微創技術、更快的復原時間和更佳的患者預後,可吸收縫線的需求也不斷成長。材料和技術的持續改進,包括塗層和線結構的創新,正在全球醫院、外科中心和門診機構中擴大可吸收縫線的使用率方面發揮著重要作用。

可吸收手術縫線旨在體內自然分解,無需手動拆除,並簡化術後護理。其抗菌性能、倒鉤線結構和高性能聚合物共混物等增強特性有助於降低感染風險並加速癒合。隨著越來越多的臨床實踐採用這些先進的工具,整體效率和患者體驗得到提升,進一步增強了該產品在現代醫療保健中的相關性。對患者舒適度和手術最佳化的日益關注,使可吸收縫合線成為多個外科專業的首選。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 30億美元 |

| 預測值 | 52億美元 |

| 複合年成長率 | 5.6% |

2024年,合成縫合線市場佔71.4%的市場佔有率,這得益於其可靠的吸收特性、高強度維持性和較低的生物反應性。聚二噁烷酮(PDO)、聚乳酸(PLA)和聚乙醇酸(PGA)等材料能夠幫助外科醫生精確控制分解時間,從而在傷口癒合的每個階段提供個人化支持。它們在開放性手術和微創手術中的適應性使其成為高精度環境中值得信賴的解決方案。

2024年,醫院板塊佔據了55.2%的市場。這種主導地位與醫院基礎設施的擴張(尤其是在高成長國家)、慢性病負擔的增加以及外科技術可近性的提高息息相關。隨著醫療體系的不斷發展,新建和現有醫院都優先考慮先進的縫合技術,以改善療效、降低併發症發生率並滿足現代外科標準。

2024年,美國可吸收手術縫線市場規模達11億美元。慢性病的增多以及對先進外科護理的需求持續推高了市場需求。隨著每年心血管、腫瘤和一般手術數量的不斷成長,人們越來越傾向於選擇能夠促進快速康復、降低感染風險並透過自然吸收最大程度減輕患者不適的縫線。

全球可吸收手術縫合線市場的主要參與者包括 Demetech、Corza Medical、Futura Surgicare、B. Braun、美敦力、Unisur、Vitrex Medical Group、Healthium Medtech、Genesis MedTech、Vital Sutures、Advanced Medical Solutions、Lotus Surgicals、Integra Lifesciences、強生和 CONMEDs。可吸收手術縫線市場中的公司正透過生物材料設計和抗菌技術的創新來鞏固其市場地位。各公司正專注於研發具有更高抗張強度、可控分解速率且與微創技術相容的縫合線。公司正在積極進行併購和策略合作,以擴大產品組合和全球影響力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病盛行率不斷上升

- 全球範圍內外科手術數量不斷增加

- 縫合材料的進步

- 婦科手術數量不斷增加

- 產業陷阱與挑戰

- 手術費用高昂

- 嚴格的監管框架

- 市場機會

- 微創手術的需求不斷成長

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 技術進步

- 當前的技術趨勢

- 新興技術

- 供應鏈分析

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按材料,2021 - 2034 年

- 主要趨勢

- 自然縫合

- 合成縫合線

- Vicryl

- 聚對二氧環己酮縫合線(PDS)

- 聚卡普龍縫合線(Monocryl)

第6章:市場估計與預測:依結構,2021 - 2034 年

- 主要趨勢

- 單絲

- 複絲

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 心血管外科

- 婦科手術

- 骨科手術

- 眼科手術

- 神經外科

- 其他外科手術應用

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 專科診所

- 門診手術中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Advanced Medical Solutions

- B. Braun

- Corza Medical

- CONMED

- Demetech

- Futura Surgicare

- Genesis MedTech

- Healthium Medtech

- Integra Lifesciences

- Johnson & Johnson

- Medtronic

- Lotus Surgicals

- Unisur

- Vital Sutures

- Vitrex Medical Group

The Global Absorbable Surgical Sutures Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 5.2 billion by 2034. Market growth is being driven by a sharp rise in the number of surgical procedures worldwide, increasing incidences of chronic illnesses, advancements in suture technology, and a surge in gynecological surgeries. The demand for absorbable sutures is also growing as healthcare systems focus more on minimally invasive techniques, faster recovery timelines, and improved patient outcomes. Continuous improvements in materials and technologies, including innovations in coatings and thread structures, are playing a major role in expanding usage across hospitals, surgical centers, and outpatient facilities globally.

Absorbable surgical sutures are designed to naturally break down within the body, removing the need for manual removal and simplifying postoperative care. Enhanced features such as antimicrobial properties, barbed thread structures, and high-performance polymer blends are helping reduce infection risks and accelerate healing. As more clinical practices adopt these advanced tools, the overall efficiency and patient experience improve, reinforcing the product's relevance in modern healthcare. Increasing focus on patient comfort and procedure optimization is positioning absorbable sutures as a preferred choice across multiple surgical specialties.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.6% |

The synthetic sutures segment held 71.4% share in 2024, supported by their reliable absorption profiles, high strength retention, and reduced biological reactivity. Materials like polydioxanone (PDO), polylactic acid (PLA), and polyglycolic acid (PGA) offer surgeons precise control over degradation timelines, allowing tailored support during each phase of wound healing. Their adaptability in both open and minimally invasive procedures makes them a trusted solution in high-precision environments.

The hospitals segment held a 55.2% share in 2024. This dominance is linked to expanding hospital infrastructure, especially in high-growth countries, alongside rising chronic disease burdens and enhanced access to surgical technologies. As healthcare systems evolve, newly built and existing hospitals are prioritizing advanced suturing options to improve outcomes, reduce complication rates, and meet modern surgical standards.

United States Absorbable Surgical Sutures Market generated USD 1.1 billion in 2024. Rising chronic conditions and the need for advanced surgical care continue to elevate demand. With a growing number of cardiovascular, oncological, and general surgeries performed annually, there's a strong shift toward sutures that promote faster recovery, lower infection risks, and minimize patient discomfort through natural absorption.

Key players dominating the Global Absorbable Surgical Sutures Market include Demetech, Corza Medical, Futura Surgicare, B. Braun, Medtronic, Unisur, Vitrex Medical Group, Healthium Medtech, Genesis MedTech, Vital Sutures, Advanced Medical Solutions, Lotus Surgicals, Integra Lifesciences, Johnson & Johnson, and CONMED. Companies operating in the absorbable surgical sutures market are strengthening their positions through innovation in biomaterial design and antimicrobial technologies. Firms are focusing on R&D to develop sutures with enhanced tensile strength, controlled degradation rates, and compatibility with minimally invasive techniques. Mergers, acquisitions, and strategic collaborations are being pursued to expand product portfolios and global reach.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Material trends

- 2.2.3 Structure trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases

- 3.2.1.2 Rising surgical procedures worldwide

- 3.2.1.3 Advancements in suture materials

- 3.2.1.4 Increasing number of gynecological procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of procedures

- 3.2.2.2 Stringent regulatory framework

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for minimally invasive surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Natural suture

- 5.3 Synthetic suture

- 5.3.1 Vicryl

- 5.3.2 Polydioxanone suture (PDS)

- 5.3.3 Poliglecaprone suture (Monocryl)

Chapter 6 Market Estimates and Forecast, By Structure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Monofilament

- 6.3 Multifilament

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Cardiovascular surgery

- 7.3 Gynaecology surgery

- 7.4 Orthopaedic surgery

- 7.5 Ophthalmic surgery

- 7.6 Neurological surgery

- 7.7 Other surgical applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Ambulatory surgical centres

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Medical Solutions

- 10.2 B. Braun

- 10.3 Corza Medical

- 10.4 CONMED

- 10.5 Demetech

- 10.6 Futura Surgicare

- 10.7 Genesis MedTech

- 10.8 Healthium Medtech

- 10.9 Integra Lifesciences

- 10.10 Johnson & Johnson

- 10.11 Medtronic

- 10.12 Lotus Surgicals

- 10.13 Unisur

- 10.14 Vital Sutures

- 10.15 Vitrex Medical Group

2026年全球心臟縫線市場報告2026年全球縫線和吻合器市場報告

2026年全球心臟縫線市場報告2026年全球縫線和吻合器市場報告 全球外科縫合線市場規模、佔有率、趨勢和成長分析報告(2026-2034年)外科縫合線市場-2026-2031年預測關節間隔物市場 - 2026-2031 年預測

全球外科縫合線市場規模、佔有率、趨勢和成長分析報告(2026-2034年)外科縫合線市場-2026-2031年預測關節間隔物市場 - 2026-2031 年預測 一次性無菌縫合包市場(按產品類型、形狀、針型、應用、最終用戶和銷售管道分類),全球預測(2026-2032年)自鎖倒刺縫線市場:按成分、材料、最終用戶、分銷管道和應用分類,全球預測(2026-2032年)

一次性無菌縫合包市場(按產品類型、形狀、針型、應用、最終用戶和銷售管道分類),全球預測(2026-2032年)自鎖倒刺縫線市場:按成分、材料、最終用戶、分銷管道和應用分類,全球預測(2026-2032年) 心臟縫線市場規模、佔有率和成長分析(按類型、材質、應用、最終用戶和地區分類)-2026-2033年產業預測

心臟縫線市場規模、佔有率和成長分析(按類型、材質、應用、最終用戶和地區分類)-2026-2033年產業預測 日本外科縫線市場規模、佔有率、趨勢和預測(按類型、線材、應用、最終用途和地區分類),2026-2034年外科縫合線市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2025-2034)

日本外科縫線市場規模、佔有率、趨勢和預測(按類型、線材、應用、最終用途和地區分類),2026-2034年外科縫合線市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察與預測(2025-2034)