|

市場調查報告書

商品編碼

1801823

脊椎機器人手術市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Spine Robotic Surgery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

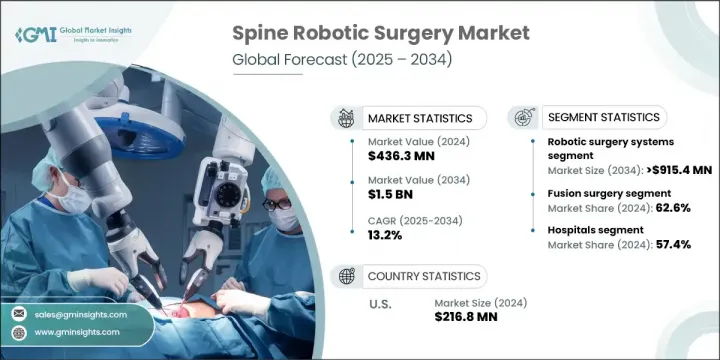

2024年,全球脊椎機器人手術市場規模達4.363億美元,預計2034年將以13.2%的複合年成長率成長,達到15億美元。這一大幅成長主要源於脊椎疾病發病率的上升、醫療保健投資的增加以及全球向微創手術的轉變。隨著患者和醫療機構都尋求更安全、更精準、更短恢復時間的手術方案,對先進手術方案的需求持續成長。隨著人口老化加劇和醫療保健體系的不斷發展,各地區對機器人輔助脊椎手術的需求正在不斷成長。

手術機器人技術的創新,加上人工智慧、導航和即時影像技術的發展,正在使這些系統更加可靠,並得到更廣泛的應用。這些技術正在提高複雜脊椎手術的精準度,並實現傳統手術方法難以達到的效果。在不斷發展的醫療格局中,機器人系統正成為脊椎手術的重要組成部分,提升手術安全性和效率。它們在醫院和外科中心的日益普及,預示著未來十年市場將呈現強勁成長動能。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 4.363億美元 |

| 預測值 | 15億美元 |

| 複合年成長率 | 13.2% |

脊椎機器人手術提供了高水準的控制力和精準度,顯著改善了脊椎手術的實施方式。其微創特性有助於加快癒合速度並降低併發症風險,這對外科醫生和患者都極具吸引力。透過使用機器人系統,臨床醫生可以進行更小、更精確的切口,從而最大限度地減少對周圍組織的損傷。這些系統能夠實現手動難以複製的精細操作,從而降低手術失誤的可能性並取得更好的效果。醫院受益於患者復原時間的縮短和住院時間的縮短,這進而降低了整體醫療成本並提高了手術流程的效率。

2024年,機器人手術系統細分市場佔據58.3%的市場。專家指出,技術進步和卓越的臨床療效是推動這項績效的關鍵因素。現代手術機器人配備了增強型成像、人工智慧驅動的手術計劃和即時導航功能,可幫助外科醫生輕鬆完成高度複雜的手術。這意味著手術更加精準,修復風險更低,使機器人平台成為許多醫療機構的首選。此外,機器人系統旨在支援微創技術,提供先進的工具來協助完成精細複雜的手術。這種精準度不僅提高了手術質量,也增強了外科醫生的信心。

2024年,融合手術市佔率達到62.6%,反映出其在脊椎治療領域持續受到歡迎。脊椎融合手術仍然是最常見的手術之一,尤其是在人口老化和生活方式因素導致脊椎相關問題日益普遍的背景下。機器人輔助融合手術具有更高的精準度、更少的併發症和更低的翻修率,所有這些都使其在該領域佔據主導地位。機器人技術的整合有助於改善這些手術,使其對於治療慢性脊椎疾病的患者更安全、更可預測。

2024年,美國脊椎機器人手術市場規模達2.168億美元。該地區的主導地位得益於先進的醫院系統、創新技術的快速應用以及不斷增加的研發投入。美國憑藉其完善的基礎設施和報銷體系,以及龐大的脊椎疾病患者群體,實現了強勁成長。這些因素使北美成為機器人脊椎手術的創新中心和商業領導者,吸引了許多致力於拓展全球業務的公司的注意。

影響全球脊椎機器人手術市場的主要參與者包括強生、Zimmer Biomet、西門子醫療、美敦力、直覺外科、史賽克、Brainlab、CUREXO、Orthofix Medical、R2 Surgical、B Braun、Globus Medical 等。他們持續的研發投入和對產品創新的關注正在塑造脊椎外科技術的未來。為了建立強大的市場影響力,脊椎機器人手術領域的領先公司正專注於持續創新和策略合作夥伴關係。他們正在大力投資人工智慧整合、下一代導航工具和先進的成像功能,以提供精確增強的系統。許多公司正在擴大其臨床試驗管道,以在全球市場更快獲得監管部門的批准。與醫院和學術機構的合作透過提供培訓和演示設施,有助於加速機器人平台的採用。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 脊椎疾病盛行率不斷上升

- 技術進步

- 微創外科手術激增

- 醫療支出增加

- 產業陷阱與挑戰

- 機器人設備的複雜性

- 嚴格的監管要求

- 市場機會

- 發展中經濟體的成長潛力

- 持續投入研發,促進產品開發

- 成長動力

- 成長潛力

- 成長潛力分析

- 報銷場景

- 監管格局

- 美國

- 歐洲

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 未來市場趨勢

- 新產品開發格局

- 啟動場景

- 2024年定價分析

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 機器人手術系統

- 全機器人系統

- 機械手臂輔助系統

- 手術導航系統

- 電磁導航系統

- 光學導航系統

- 混合導航系統

- 軟體解決方案

- 配件和耗材

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 融合手術

- 非融合手術

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- B Braun

- Brainlab

- CUREXO

- Globus Medical

- Intuitive Surgical Operations

- Johnson & Johnson

- Medtronic

- Orthofix Medical

- R2 Surgical

- Siemens Healthineers

- Stryker

- Zimmer Biomet

The Global Spine Robotic Surgery Market was valued at USD 436.3 million in 2024 and is estimated to grow at a CAGR of 13.2% to reach USD 1.5 billion by 2034. This substantial growth is largely driven by the rising incidence of spinal disorders, increased healthcare investment, and a global shift toward minimally invasive surgical procedures. The need for advanced surgical options continues to grow as patients and providers alike seek safer, more accurate procedures that also reduce recovery time. As the aging population increases and healthcare systems evolve, the demand for robot-assisted spinal procedures is expanding across various regions.

Innovations in surgical robotics-combined with developments in artificial intelligence, navigation, and real-time imaging-are making these systems more reliable and widely adopted. These technologies are improving precision during complex spine procedures and enabling outcomes that traditional surgical methods struggle to achieve. In this evolving medical landscape, robotic systems are becoming an essential component of spinal surgery, enhancing both safety and efficiency. Their growing presence in hospitals and surgical centers signals a strong market trajectory through the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $436.3 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 13.2% |

Spine robotic surgery offers a level of control and accuracy that dramatically improves the way spinal procedures are performed. Its minimally invasive nature supports faster healing and lowers complication risks, which appeals to both surgeons and patients. By using robotic systems, clinicians can make smaller, more precise incisions, which helps minimize trauma to surrounding tissue. These systems enable fine-tuned maneuvers that are difficult to replicate manually, reducing the potential for surgical error and delivering better results. Hospitals benefit from reduced recovery times and shorter patient stays, which in turn lowers overall healthcare costs and increases efficiency in surgical workflows.

The robotic surgery systems segment held a 58.3% share in 2024. Experts pointed to technological advancement and strong clinical outcomes as key drivers for this performance. Modern surgical robotics are equipped with enhanced imaging, AI-driven planning, and real-time navigation, helping surgeons perform highly complex procedures with ease. This translates into more precise surgeries and less risk of revision, making robotic platforms a preferred choice in many facilities. Additionally, robotic systems are built to support minimally invasive techniques, offering advanced tools that assist with delicate and intricate tasks. This precision not only improves surgical quality but also boosts surgeon confidence.

The fusion surgery segment accounted for a 62.6% share in 2024, reflecting its continued popularity in spinal treatment. Spinal fusion remains one of the most frequently performed procedures, particularly as spine-related issues become more common with aging populations and lifestyle factors. Robotic-assisted fusion surgeries offer heightened precision, fewer complications, and lower revision rates, all of which contribute to their dominance in this space. The integration of robotics has helped refine these procedures, making them safer and more predictable for patients dealing with chronic spine conditions.

United States Spine Robotic Surgery Market generated USD 216.8 million in 2024. The region's dominance is fueled by advanced hospital systems, quick adoption of innovative technologies, and increasing investments in research and development. The US shows strong growth due to its established infrastructure and reimbursement landscape, alongside a large patient population affected by spine disorders. These factors make North America an innovation hub and commercial leader in robotic spine surgery, drawing interest from companies aiming to expand their global footprint.

Major players influencing the Global Spine Robotic Surgery Market include Johnson & Johnson, Zimmer Biomet, Siemens Healthineers, Medtronic, Intuitive Surgical Operations, Stryker, Brainlab, CUREXO, Orthofix Medical, R2 Surgical, B Braun, Globus Medical, and others. Their continued R&D investments and focus on product innovation are shaping the future of spinal surgery technologies. To build a strong market presence, leading companies in the spine robotic surgery space are focusing on continual innovation and strategic partnerships. They're investing heavily in AI integration, next-gen navigation tools, and advanced imaging capabilities to offer precision-enhanced systems. Many are expanding their clinical trial pipelines to gain regulatory approvals faster across global markets. Collaborations with hospitals and academic institutions are helping accelerate the adoption of robotic platforms by providing training and demonstration facilities.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of spinal disorders

- 3.2.1.2 Technological advancements

- 3.2.1.3 Surge in minimally invasive surgical procedures

- 3.2.1.4 Increased healthcare spending

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity of robotic devices

- 3.2.2.2 Stringent regulatory requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Growth potential in developing economies

- 3.2.3.2 Continued investment in research and development for product development

- 3.2.1 Growth drivers

- 3.3 Growth potential

- 3.4 Growth potential analysis

- 3.5 Reimbursement scenario

- 3.6 Regulatory landscape

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Future market trends

- 3.9 New product development landscape

- 3.10 Start-up scenario

- 3.11 Pricing analysis, 2024

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Robotic surgery systems

- 5.2.1 Fully robotic systems

- 5.2.2 Robotic arm-assisted systems

- 5.3 Surgical navigation systems

- 5.3.1 Electromagnetic navigation systems

- 5.3.2 Optical navigation systems

- 5.3.3 Hybrid navigation systems

- 5.4 Software solutions

- 5.5 Accessories and consumables

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Fusion surgery

- 6.3 Non-fusion surgery

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 B Braun

- 9.2 Brainlab

- 9.3 CUREXO

- 9.4 Globus Medical

- 9.5 Intuitive Surgical Operations

- 9.6 Johnson & Johnson

- 9.7 Medtronic

- 9.8 Orthofix Medical

- 9.9 R2 Surgical

- 9.10 Siemens Healthineers

- 9.11 Stryker

- 9.12 Zimmer Biomet

脊椎外科產品市場:2026-2032年全球市場預測(依手術入路、產品類型、材料、最終用戶和分銷管道分類)

脊椎外科產品市場:2026-2032年全球市場預測(依手術入路、產品類型、材料、最終用戶和分銷管道分類) 2026年全球脊椎外科器械及設備市場報告2026年全球脊椎外科手術器械市場報告

2026年全球脊椎外科器械及設備市場報告2026年全球脊椎外科手術器械市場報告 日本脊椎外科器械市場報告(按類型(脊椎減壓、脊椎融合、骨折修復及其他)和地區分類,2026-2034年)

日本脊椎外科器械市場報告(按類型(脊椎減壓、脊椎融合、骨折修復及其他)和地區分類,2026-2034年) 脊椎外科器械:市場洞察、競爭格局及預測(至2032年)2025年脊椎治療全球市場報告

脊椎外科器械:市場洞察、競爭格局及預測(至2032年)2025年脊椎治療全球市場報告 全球脊椎手術機器人市場

全球脊椎手術機器人市場 全球脊椎外科產品市場規模依技術、程序、最終用戶、地區和預測分類:

全球脊椎外科產品市場規模依技術、程序、最終用戶、地區和預測分類: 微創脊椎手術的全球市場:市場規模,趨勢分析(2025年~2031年):MedSuite - 微創椎間設備,微創椎弓骨釘,其他全球脊椎手術器材市場:規模、佔有率和趨勢分析(2025-2031):MedCore

微創脊椎手術的全球市場:市場規模,趨勢分析(2025年~2031年):MedSuite - 微創椎間設備,微創椎弓骨釘,其他全球脊椎手術器材市場:規模、佔有率和趨勢分析(2025-2031):MedCore