|

市場調查報告書

商品編碼

1797883

凍乾注射藥物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Lyophilized Injectable Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

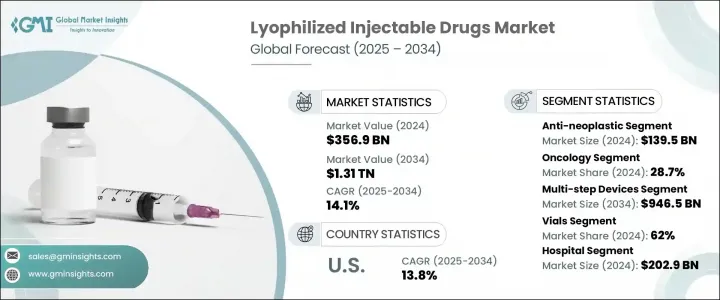

2024 年全球冷凍乾燥注射劑市場規模為 3,569 億美元,預計到 2034 年將以 14.1% 的複合年成長率成長,達到 1.31 兆美元。癌症和傳染病等慢性疾病發生率的上升,持續推高了對穩定長效治療藥物的需求。對延長保存期限和提高藥效的需求,使得冷凍乾燥注射劑成為醫藥產品線的重要組成部分。此外,全球監管部門批准的增加以及凍乾製程技術的進步,顯著提高了市場滲透率。隨著住院和門診治療逐漸轉向生物製劑和注射療法,冷凍乾燥注射劑產業的製造能力、物流基礎設施和臨床應用正在快速發展。

隨著對耐用且高度穩定的藥物製劑的需求日益成長,製藥公司正將冷凍乾燥技術應用於越來越多的注射藥物。諸如強化冷鏈配送、單劑量包裝以及復溶效率提升等創新技術,正在增強全球醫療體系的產品可靠性。冷凍乾燥製劑在穩定性和無菌性至關重要的疾病治療中正日益受到青睞。這些藥物通常與稀釋劑混合後給藥,這使得醫療保健提供者能夠控制劑量的準確性並延長產品的可用性。由於可靠的製劑具有更長的保存期限,冷凍乾燥藥物成為首選,尤其是在基礎設施有限且先進醫療服務日益普及的地區。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3569億美元 |

| 預測值 | 1.31兆美元 |

| 複合年成長率 | 14.1% |

2024年,抗腫瘤藥物市場規模達1,395億美元,反映出市場對腫瘤生物製劑和細胞毒性化合物的需求激增。冷凍乾燥注射劑尤其適合此類治療,它具有更高的穩定性和更長的保存期限,同時最大限度地降低了污染和操作相關的風險。這些特性在癌症治療中至關重要,因為精準劑量、無菌和長期儲存至關重要。隨著監管機構擴大批准冷凍乾燥製劑用於腫瘤治療,製藥公司正優先考慮抗腫瘤注射劑的研發,尤其是那些高價值製劑且效力或純度偏差空間有限的藥物。

2024年,腫瘤治療領域佔據領先地位,市佔率達28.7%。該領域佔據主導地位的原因是全球癌症發病率的不斷上升,以及對穩定注射療法的需求,這些療法需要透過長期儲存和運輸來維持療效。全球醫療保健系統正在投資更強大的藥物輸送解決方案,而冷凍乾燥注射劑則提供了一種經濟高效、長期有效的解決方案。為了滿足日益成長的癌症治療需求,藥物開發商正致力於改善輸送方法、減少藥物浪費並延長產品壽命。

2024年,北美冷凍乾燥注射劑市場佔據47%的市場佔有率,這得益於該地區先進的醫藥產業格局和高度集中的慢性病病例。該地區的主導地位也源於其強大的研發能力、FDA頻繁批准的冷凍乾燥注射劑,以及成熟的醫療保健體系,支持其在醫院和門診的廣泛應用。對腫瘤學、自體免疫疾病治療和生物製劑的持續投入,加上人們對保存期限較長的注射劑的日益接受,將繼續鞏固該地區在全球凍乾注射劑市場的地位。

為產業成長做出貢獻的傑出市場參與者包括西普拉、諾和諾德、Akums Drugs and Pharmaceuticals、默克、Aurobindo Pharma、輝瑞、吉利德科學、賽諾菲、強生、武田製藥、Vetter Pharma、Zydus、明治集團、Gufic Group、Fareva、百時美林施貴寶、費森斯、施貴羅氏和 Boraticals Pharmauticals。為了鞏固市場領導地位,冷凍乾燥注射藥物行業的公司正在增加對高容量凍乾設備和符合嚴格的全球監管標準的最先進生產線的投資。許多公司正在擴大其合約製造服務,改善冷鏈物流,並整合自動化以減少停機時間和生產成本。策略合作和授權協議通常用於獲取創新生物化合物和擴大產品組合。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性病和傳染病的盛行率不斷上升

- 藥物輸送系統的技術進步

- 對生物製劑和複雜分子的需求不斷成長

- 產業陷阱與挑戰

- 生產和設備成本高

- 監管和品質合規挑戰

- 市場機會

- 個人化精準醫療

- 擴大合約研究與製造服務(CRAMS)

- 成長動力

- 成長潛力分析

- 技術格局

- 當前的技術趨勢

- 新興技術

- 定價分析

- 研發管線及研發投資分析

- 專利態勢分析

- 母市場分析

- 監管格局

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

第5章:市場估計與預測:按藥物類型,2021 - 2034 年

- 主要趨勢

- 抗感染

- 抗腫瘤

- 抗凝血劑

- 荷爾蒙

- 抗心律不整藥

- 質子幫浦抑制劑

- 麻醉藥

- 其他藥物類型

第6章:市場估計與預測:按適應症,2021 - 2034 年

- 主要趨勢

- 自體免疫疾病

- 呼吸系統疾病

- 胃腸道疾病

- 腫瘤學

- 心血管疾病

- 傳染病

- 荷爾蒙失調

- 代謝紊亂

- 生殖健康

- 其他適應症

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 預充式稀釋劑注射器

- 多步驟設備

第8章:市場估計與預測:按包裝,2021 - 2034 年

- 主要趨勢

- 小瓶

- 墨水匣

- 預充式裝置

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 專科診所

- 其他最終用途

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Akums Drugs and Pharmaceuticals

- Aurobindo Pharma

- Bora Pharmaceuticals

- Bristol Myers Squibb

- Cipla

- F. Hoffmann-La Roche

- Fareva

- Fresenius

- Gilead Sciences

- Gufic Group

- Johnson & Johnson

- Meiji Group

- Merck

- Novo Nordisk

- Pfizer

- Sanofi

- Takeda Pharmaceuticals

- Vetter Pharma

- Zydus

The Global Lyophilized Injectable Drugs Market was valued at USD 356.9 billion in 2024 and is estimated to grow at a CAGR of 14.1% to reach USD 1.31 trillion by 2034. Rising incidences of chronic health conditions, including cancer and infectious diseases, continue to escalate demand for stable and long-acting therapeutics. The need for extended shelf life and improved drug efficacy has made freeze-dried injectable formulations an essential part of the pharmaceutical pipeline. Additionally, the increase in global regulatory approvals and technological advancements in lyophilization processes is significantly enhancing market penetration. With a shift toward biologics and injectable therapies in both inpatient and outpatient care, the lyophilized injectables sector is seeing rapid development in manufacturing capabilities, logistics infrastructure, and clinical applications.

The rising need for durable and highly stable drug formulations is pushing pharmaceutical companies to adopt lyophilization for an expanding range of injectable drugs. Innovations such as enhanced cold-chain distribution, single-dose packaging, and improvements in reconstitution efficiency are strengthening product reliability across global healthcare systems. Lyophilized formulations are gaining momentum in the treatment of diseases where stability and sterility are critical. These drugs are typically administered after mixing with a diluent, allowing healthcare providers to manage dosing accuracy and extend product usability. The availability of reliable formulations with longer shelf lives makes lyophilized drugs a preferred choice, particularly in regions with limited infrastructure and growing access to advanced medical care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $356.9 Billion |

| Forecast Value | $1.31 Trillion |

| CAGR | 14.1% |

In 2024, the anti-neoplastic agents segment captured a USD 139.5 billion share, reflecting the surging demand for oncology-focused biologics and cytotoxic compounds. Lyophilized injectable drugs are particularly well-suited for these treatments, offering improved stability and longer shelf life while minimizing the risks associated with contamination and handling. These properties are critical in cancer care, where precise dosage, sterility, and long-term storage are vital. With regulatory bodies increasingly approving freeze-dried formulations in oncology, pharmaceutical firms are prioritizing development pipelines around anti-neoplastic injectables, particularly those with high-value formulations and limited room for deviation in potency or purity.

The oncology segment held the leading share of 28.7% in 2024. Its dominance is driven by the growing global incidence of cancer and the necessity for stable injectable therapies that maintain therapeutic effectiveness through extended storage and transport. Healthcare systems worldwide are investing in more robust drug delivery solutions, and lyophilized injectables provide a cost-effective, long-term answer. Pharmaceutical developers are focusing heavily on refining delivery methods, reducing drug wastage, and enhancing product lifespan through lyophilization to meet the growing demand for cancer treatments.

North America Lyophilized Injectable Drugs Market held 47% in 2024, underpinned by the region's advanced pharmaceutical landscape and high concentration of chronic disease cases. The region's dominance also stems from strong R&D capabilities, frequent FDA approvals for freeze-dried injectables, and a mature healthcare delivery system that supports wide adoption across hospital and ambulatory settings. Continued investment in oncology, autoimmune disease therapies, and biologics, combined with growing acceptance of injectable drugs with extended shelf lives, continues to support the region's stronghold in the global lyophilized injectable drugs market.

Prominent market participants contributing to industry growth include Cipla, Novo Nordisk, Akums Drugs and Pharmaceuticals, Merck, Aurobindo Pharma, Pfizer, Gilead Sciences, Sanofi, Johnson & Johnson, Takeda Pharmaceuticals, Vetter Pharma, Zydus, Meiji Group, Gufic Group, Fareva, Bristol Myers Squibb, Fresenius, F. Hoffmann-La Roche, and Bora Pharmaceuticals. To secure their market leadership, companies in the lyophilized injectable drugs industry are increasingly investing in high-capacity freeze-drying equipment and state-of-the-art manufacturing lines that meet stringent global regulatory standards. Many firms are expanding their contract manufacturing services, improving cold chain logistics, and integrating automation to reduce downtime and production costs. Strategic collaborations and licensing agreements are commonly used to gain access to innovative biologic compounds and expand product portfolios.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Indication

- 2.2.4 Application

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic and infectious diseases

- 3.2.1.2 Technological advancements in drug delivery systems

- 3.2.1.3 Rising demand for biologics and complex molecules

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production and equipment costs

- 3.2.2.2 Regulatory and quality compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Personalized and precision medicine

- 3.2.3.2 Expansion of contract research and manufacturing services (CRAMS)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pricing analysis

- 3.6 Pipeline and R&D investment analysis

- 3.7 Patent landscape analysis

- 3.8 Parent market analysis

- 3.9 Regulatory landscape

- 3.9.1 North America

- 3.9.2 Europe

- 3.9.3 Asia Pacific

- 3.9.4 Latin America

- 3.9.5 Middle East and Africa

- 3.10 Future market trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Anti-infective

- 5.3 Anti-neoplastic

- 5.4 Anticoagulant

- 5.5 Hormones

- 5.6 Antiarrhythmic

- 5.7 Proton pump inhibitors

- 5.8 Anesthetics

- 5.9 Other drug types

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Autoimmune diseases

- 6.3 Respiratory diseases

- 6.4 Gastrointestinal disorders

- 6.5 Oncology

- 6.6 Cardiovascular diseases

- 6.7 Infectious diseases

- 6.8 Hormonal disorders

- 6.9 Metabolic disorders

- 6.10 Reproductive health

- 6.11 Other indications

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prefilled diluent syringes

- 7.3 Multi-step devices

Chapter 8 Market Estimates and Forecast, By Packaging, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Vials

- 8.3 Cartridges

- 8.4 Prefilled devices

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Specialty clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Akums Drugs and Pharmaceuticals

- 11.2 Aurobindo Pharma

- 11.3 Bora Pharmaceuticals

- 11.4 Bristol Myers Squibb

- 11.5 Cipla

- 11.6 F. Hoffmann-La Roche

- 11.7 Fareva

- 11.8 Fresenius

- 11.9 Gilead Sciences

- 11.10 Gufic Group

- 11.11 Johnson & Johnson

- 11.12 Meiji Group

- 11.13 Merck

- 11.14 Novo Nordisk

- 11.15 Pfizer

- 11.16 Sanofi

- 11.17 Takeda Pharmaceuticals

- 11.18 Vetter Pharma

- 11.19 Zydus