|

市場調查報告書

商品編碼

1797859

柴油發電機組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Diesel Gensets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

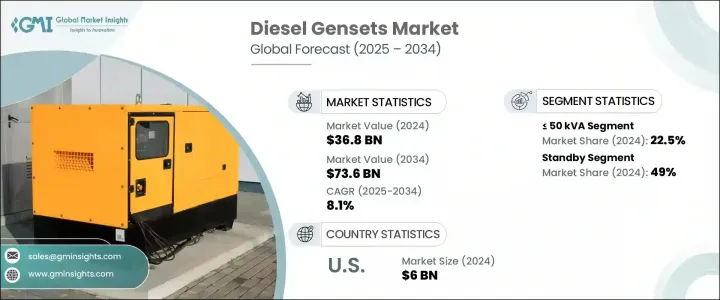

2024年,全球柴油發電機組市場規模達368億美元,預計2034年將以8.1%的複合年成長率成長,達到736億美元。該市場的擴張源於住宅、商業和工業領域對可靠備用電源日益成長的需求,尤其是在電網不穩定或頻繁中斷的地區。柴油發電機組在這些領域至關重要,能夠立即恢復電力供應,並確保電信、醫療保健和基礎設施等行業的服務連續性。隨著環境法規的日益嚴格,製造商正在融入自動化、遠端監控和旨在減少排放的功能。為了應對永續性問題,將柴油與太陽能或電池儲能等再生能源相結合的混合動力系統正日益受到關注。這種轉變使柴油發電機組在環境敏感地區更具可行性,既可靠又能降低環境影響。在亞太地區,柴油發電機組市場正在成長,尤其是在頻繁停電的城鄉地區。

對道路、醫院和資料中心等關鍵基礎設施的投資極大地推動了對可靠備用電源解決方案的需求。隨著政府和私營部門持續致力於基礎設施的擴建和現代化,對持續供電以支持這些重要營運的需求日益成長。道路和交通網路需要不間斷電源來支援交通管理系統、號誌傳輸和緊急服務。醫院依靠備用電源來確保救生設備在停電期間繼續運行,尤其是在重症監護病房或急診室。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 368億美元 |

| 預測值 | 736億美元 |

| 複合年成長率 | 8.1% |

預計到2034年,50 kVA以上至125 kVA的柴油發電機組市場將以7.5%的複合年成長率成長。這類系統在中小企業、醫療機構和建築工地中越來越受歡迎。它們尤其因其在電網中斷期間提供不間斷電力的能力而備受青睞,確保關鍵服務和營運不間斷地持續運作。

備用柴油發電機組市場在2024年佔據49%的市場佔有率,預計到2034年將以7.5%的複合年成長率成長。該市場的崛起歸因於醫療保健、商業基礎設施和資料中心等關鍵產業對可靠備用電源的需求日益成長。隨著人們對電網可靠性的擔憂加劇(尤其是在極端天氣事件和自然災害的影響下),企業優先考慮備用系統,以減少停機時間並確保營運連續性。備用柴油發電機組是這些產業的首選,可在需要時快速恢復電力。

2024年,美國柴油發電機組市場佔85.9%的市場佔有率,產值達60億美元。人們對電網可靠性、頻繁的天氣干擾以及基礎設施老化的擔憂日益加劇,推動了對備用電源解決方案的需求。工業和商業設施正在投資柴油發電機組,以確保停電期間的業務連續性。此外,再生能源的日益普及也激發了人們對混合動力系統的興趣,而柴油發電機組正是可靠的補充電源。

全球柴油發電機組市場的頂級公司包括康明斯、Caterpillar、亞力克、勞斯萊斯和 Generac 電力系統。為了鞏固其市場地位,柴油發電機組產業的公司正專注於幾項關鍵策略。許多公司正在大力投資技術進步,例如自動化和遠端監控,這使用戶能夠更有效地監控和控制發電機組,從而提高營運效率。該公司也將永續性放在首位,加入減排功能並開發將柴油與太陽能和電池儲存等再生能源相結合的混合動力系統。這項創新不僅減少了碳足跡,而且還增強了產品在注重環保的市場的吸引力。此外,該行業的參與者正在擴大其產品組合,以滿足從小型企業到大型工業營運的更廣泛客戶的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 按地區分析公司市場佔有率

- 北美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

- 拉丁美洲

- 戰略儀表板

- 策略舉措

- 競爭基準測試

- 創新與永續發展格局

第5章:市場規模及預測:依功率等級,2021 - 2034 年

- 主要趨勢

- ≤50千伏安

- > 50千伏安 - 125千伏安

- > 125 千伏安 - 200 千伏安

- > 200 千伏安 - 330 千伏安

- > 330 千伏安 - 750 千伏安

- > 750千伏安

第6章:市場規模及預測:依最終用途,2021 - 2034

- 主要趨勢

- 住宅

- 商業的

- 工業的

第7章:市場規模及預測:依應用,2021 - 2034

- 主要趨勢

- 支援

- 削峰

- 主/連續

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 俄羅斯

- 英國

- 德國

- 法國

- 西班牙

- 奧地利

- 義大利

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 印尼

- 馬來西亞

- 泰國

- 越南

- 菲律賓

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 土耳其

- 伊朗

- 阿曼

- 非洲

- 埃及

- 奈及利亞

- 阿爾及利亞

- 南非

- 安哥拉

- 肯亞

- 莫三比克

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

第9章:公司簡介

- Aggreko

- Ashok Leyland

- Atlas Copco

- Captiva Energy Solutions Private Limited

- Caterpillar

- Cooper Corp.

- Cummins, Inc.

- Deere & Company

- FG Wilson

- Generac Power Systems, Inc.

- Greaves Cotton Limited

- HIMOINSA

- JC Bamford Excavators Ltd.

- Kirloskar

- Rehlko

- Mahindra POWEROL

- Mitsubishi Heavy Industries, Ltd.

- Powerica Limited

- Rapid Power Generation Ltd.

- Rolls-Royce plc

- Siemens

- Sterling and Wilson Pvt. Ltd.

- Sudhir Power Ltd.

- Supernova Genset

- Wartsila

- Yamaha Motor Co., Ltd.

The Global Diesel Gensets Market was valued at USD 36.8 billion in 2024 and is anticipated to grow at a CAGR of 8.1% to reach USD 73.6 billion by 2034. The expansion of this market is driven by an increasing demand for reliable backup power across residential, commercial, and industrial sectors, particularly in regions with unstable or frequently interrupted power grids. Diesel gensets are crucial in these areas, providing immediate power restoration and ensuring the continuity of services in sectors like telecom, healthcare, and infrastructure. As stricter environmental regulations come into play, manufacturers are incorporating automation, remote monitoring, and features aimed at reducing emissions. In response to sustainability concerns, hybrid systems that combine diesel with renewable energy sources, such as solar or battery storage, are gaining traction. This shift is making diesel gensets more viable in environmentally sensitive regions, offering both reliability and lower environmental impact. In the Asia-Pacific region, the diesel genset market is experiencing growth, particularly in urban and rural areas suffering from frequent power outages.

Investments in critical infrastructure like roads, hospitals, and data centers are significantly driving the demand for reliable backup power solutions. As governments and private sectors continue to focus on expanding and modernizing infrastructure, there is an increasing need for a continuous power supply to support these vital operations. Roads and transportation networks require uninterrupted power for traffic management systems, signaling, and emergency services. Hospitals depend on backup power to ensure life-saving equipment remains operational during power outages, especially in critical care units or emergency rooms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $36.8 Billion |

| Forecast Value | $73.6 Billion |

| CAGR | 8.1% |

The diesel genset market for units between >50 kVA and 125 kVA is expected to grow at a CAGR of 7.5% through 2034. These systems are becoming increasingly popular among small to medium-sized businesses, healthcare institutions, and construction sites. They are particularly valued for their ability to provide uninterrupted power during grid disruptions, ensuring that critical services and operations continue without delay.

The standby diesel genset segment held a 49% share in 2024 and is expected to grow at a 7.5% CAGR until 2034. This segment's rise is attributed to the growing need for reliable backup power in essential sectors such as healthcare, commercial infrastructure, and data centers. As concerns over grid reliability intensify-especially due to extreme weather events and natural disasters-businesses are prioritizing backup systems to mitigate downtime and ensure operational continuity. Standby diesel gensets are the preferred choice in these sectors, providing quick power restoration in times of need.

U.S. Diesel Gensets Market held 85.9% share in 2024, generating USD 6 billion. The demand for backup power solutions is driven by increasing concerns about grid reliability, frequent weather-related disruptions, and aging infrastructure. Industrial and commercial facilities are investing in diesel gensets to ensure business continuity during outages. Moreover, the growing integration of renewable energy sources has spurred interest in hybrid power systems, with diesel gensets serving as reliable supplemental power sources.

Top companies in the Global Diesel Gensets Market include Cummins, Caterpillar, Aggreko, Rolls-Royce, and Generac Power Systems. To solidify their market presence, companies in the diesel genset industry are focusing on several key strategies. Many are investing heavily in technological advancements, such as automation and remote monitoring, which allow users to monitor and control gensets more efficiently, improving operational efficiency. Companies are also prioritizing sustainability by incorporating emissions-reduction features and developing hybrid systems that combine diesel with renewable energy sources like solar and battery storage. This innovation not only reduces carbon footprints but also enhances product appeal in environmentally conscious markets. Additionally, players in the industry are expanding their product portfolios to cater to a broader range of customers, from small businesses to large-scale industrial operations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East

- 4.2.5 Africa

- 4.2.6 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 Standby

- 7.3 Peak shaving

- 7.4 Prime/continuous

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Russia

- 8.3.2 UK

- 8.3.3 Germany

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Indonesia

- 8.4.7 Malaysia

- 8.4.8 Thailand

- 8.4.9 Vietnam

- 8.4.10 Philippines

- 8.5 Middle East

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Turkey

- 8.5.5 Iran

- 8.5.6 Oman

- 8.6 Africa

- 8.6.1 Egypt

- 8.6.2 Nigeria

- 8.6.3 Algeria

- 8.6.4 South Africa

- 8.6.5 Angola

- 8.6.6 Kenya

- 8.6.7 Mozambique

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Mexico

- 8.7.3 Argentina

- 8.7.4 Chile

Chapter 9 Company Profiles

- 9.1 Aggreko

- 9.2 Ashok Leyland

- 9.3 Atlas Copco

- 9.4 Captiva Energy Solutions Private Limited

- 9.5 Caterpillar

- 9.6 Cooper Corp.

- 9.7 Cummins, Inc.

- 9.8 Deere & Company

- 9.9 FG Wilson

- 9.10 Generac Power Systems, Inc.

- 9.11 Greaves Cotton Limited

- 9.12 HIMOINSA

- 9.13 J C Bamford Excavators Ltd.

- 9.14 Kirloskar

- 9.15 Rehlko

- 9.16 Mahindra POWEROL

- 9.17 Mitsubishi Heavy Industries, Ltd.

- 9.18 Powerica Limited

- 9.19 Rapid Power Generation Ltd.

- 9.20 Rolls-Royce plc

- 9.21 Siemens

- 9.22 Sterling and Wilson Pvt. Ltd.

- 9.23 Sudhir Power Ltd.

- 9.24 Supernova Genset

- 9.25 Wartsila

- 9.26 Yamaha Motor Co., Ltd.

全球柴油發電機組市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球柴油發電機組市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 柴油發電機組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按功率容量、便攜性、應用、最終用戶、地區和競爭格局分類,2021-2031年)

柴油發電機組市場 - 全球產業規模、佔有率、趨勢、機會及預測(按功率容量、便攜性、應用、最終用戶、地區和競爭格局分類,2021-2031年) 商用柴油發電機市場按產品類型、額定功率、冷卻系統、安裝方式、相數類型、最終用戶和銷售管道分類,全球預測(2026-2032年)

商用柴油發電機市場按產品類型、額定功率、冷卻系統、安裝方式、相數類型、最終用戶和銷售管道分類,全球預測(2026-2032年) 備用商用柴油發電機組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測柴油發電機市場:2025-2030 年全球預測(按額定功率、銷售管道、應用和最終用戶)商用柴油發電機組市場機會、成長動力、產業趨勢分析及 2025-2034 年預測

備用商用柴油發電機組市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測柴油發電機市場:2025-2030 年全球預測(按額定功率、銷售管道、應用和最終用戶)商用柴油發電機組市場機會、成長動力、產業趨勢分析及 2025-2034 年預測