|

市場調查報告書

商品編碼

1797854

乳癌治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Breast Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

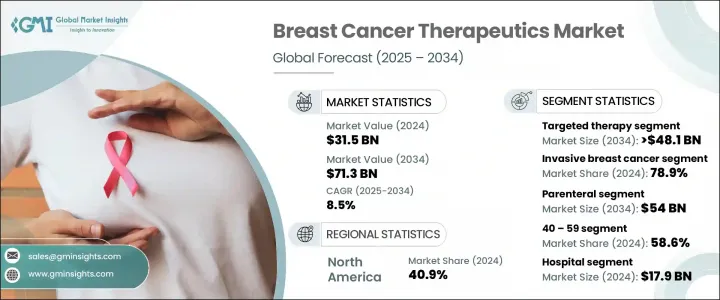

2024 年全球乳癌治療市場規模為 315 億美元,預計到 2034 年將以 8.5% 的複合年成長率成長至 713 億美元。市場成長歸因於多種因素:乳癌高發生率、早期發現和治療意識的提高、以及政府和非營利篩檢計畫的支持力度加大。隨著篩檢的增加和更多病例在早期階段被發現,對有效治療方案的需求上升,從而支持了市場的發展勢頭。此外,人口老化、肥胖、久坐生活方式和都市化進程的加速也導致乳癌盛行率上升。發展中市場醫療服務可近性的擴大進一步促進了治療的應用。標靶治療、荷爾蒙療法和免疫療法等個人化醫療的進展正在改善治療效果並推動市場擴張。

乳癌治療涵蓋一系列旨在控制病情進展、預防復發和提高存活率的療法。默克、阿斯特捷利康、諾華、輝瑞和羅氏等領先製藥公司正大力投資研發,尤其注重精準腫瘤學和生物標記驅動療法。政府篩選計畫和宣傳活動正在加速早期診斷,進而推動對先進療法的需求。新興經濟體醫療基礎設施的建設和報銷改革使得更廣泛的治療可近性成為可能。轉向更具針對性的干涉措施(包括單株抗體、小分子抑制劑和免疫腫瘤藥物)的轉變正在提高療效並減少副作用,從而進一步推動其應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 315億美元 |

| 預測值 | 713億美元 |

| 複合年成長率 | 8.5% |

2024年,標靶療法的市場規模達到214億美元,佔據主導地位,這得益於其能夠靶向癌症相關生物標記且不良反應較少。抗體-藥物偶聯物、HER2抑制劑和PARP抑制劑等劑型在早期和晚期治療方案中被廣泛採用。 HER2低亞型療法的創新以及AI引導的患者分層技術,鞏固了其在該領域的市場領先地位。

2024年,侵襲性乳癌佔78.9%的市場佔有率,是最常見的乳癌類型。光是浸潤性乳管癌就約佔所有侵襲性病例的80%,約佔乳癌診斷的55%。由於侵襲性乳癌具有侵襲性且可能轉移至導管外,因此需要多種治療方法,包括標靶藥物、荷爾蒙調節劑(例如選擇性雌激素受體調節劑SERM)、化療和免疫療法,從而推動了強勁的臨床需求。

2024年,北美乳癌治療市場佔40.9%的市場佔有率,其中美國和加拿大佔據主導地位。先進的醫療基礎設施、高度的早期檢測意識、強大的腫瘤學研究投入以及優惠的報銷制度推動了治療方案的採用。該地區受益於快速的法規核准、專利療法的高滲透率以及新興治療模式的廣泛應用,鞏固了其在全球乳癌治療領域的領先地位。

輝瑞、羅氏、默克、阿斯特捷利康、諾華和禮來等主要公司正在塑造這一行業,它們推動創新和全球影響力。領先的製藥公司正專注於按分子亞型對患者進行分層,從而透過伴隨診斷最佳化精準標靶治療。許多公司正在拓展抗體藥物偶聯物、雙特異性抗體、CDK4/6抑制劑和免疫療法組合等新型療法的研發管線,以增強產品組合深度。策略性收購、授權協議以及與生技公司的策略合作,加速了創新化合物和新興研發人才的取得。透過與區域分銷商和醫療保健系統的合作,公司正在向新興市場進行全球擴張。此外,公司還投資於真實世界研究和基於價值的成果,以支持報銷談判。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 全球乳癌發生率上升

- 標靶治療和免疫治療的進展

- 提高認知和早期檢測計劃

- 個人化醫療和生物標記檢測的需求不斷成長

- 產業陷阱與挑戰

- 治療費用高昂

- 治療的副作用和毒性

- 市場機會

- 新型療法的開發

- 合作與策略夥伴關係

- 成長動力

- 成長潛力分析

- 技術格局

- 當前的技術趨勢

- 新興技術

- 管道分析

- 監管格局

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

第5章:市場估計與預測:按療法,2021 - 2034 年

- 主要趨勢

- 標靶治療

- 荷爾蒙療法

- 化療

- 免疫療法

第6章:市場估計與預測:按癌症類型,2021 - 2034 年

- 主要趨勢

- 乳管原位癌(DCIS)

- 侵襲性乳癌

- 浸潤性乳管癌(IDC)

- 荷爾蒙受體

- HER2+

- 三陰性乳癌(TNBC)

- 其他浸潤性乳管癌 (IDC) 類型

- 浸潤性小葉癌(ILC)

- 浸潤性乳管癌(IDC)

第7章:市場估計與預測:按管理路線,2021 - 2034 年

- 主要趨勢

- 口服

- 腸外

第8章:市場估計與預測:按年齡層,2021 - 2034 年

- 主要趨勢

- 20 - 39

- 40 - 59

- 60歲以上

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 腫瘤診所

- 其他最終用途

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Amgen

- AstraZeneca

- Eisai

- Eli Lilly and Company

- F. Hoffmann La Roche

- GE HealthCare

- Gilead Sciences

- Macrogenics

- Merck

- Novartis

- Pfizer

- Sun Pharmaceutical

The Global Breast Cancer Therapeutics Market was valued at USD 31.5 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 71.3 billion by 2034. The market growth is attributed to a combination of factors: high incidence of breast cancer, expanded awareness of early detection and treatment, and rising support from government and nonprofit screening initiatives. As screening increases and more cases are identified at earlier stages, demand for effective treatment options rises, supporting the market's momentum. Also, rising rates of aging populations, obesity, sedentary lifestyles, and urbanization are contributing to higher breast cancer prevalence. Expanded health access in developing markets further boosts therapy uptake. Advances in personalized medicine-such as targeted treatments, hormone therapy, and immunotherapy-are enhancing outcomes and fueling market expansion.

Breast cancer therapeutics encompass a spectrum of treatments aimed at controlling disease progression, preventing recurrence, and improving survival. Leading pharmaceutical firms such as Merck, AstraZeneca, Novartis, Pfizer, and F. Hoffmann-La Roche are investing heavily in R&D, particularly focusing on precision oncology and biomarker-driven therapies. Government screening programs and awareness campaigns are accelerating early diagnosis, which in turn drives demand for advanced treatments. Growth in emerging economies' healthcare infrastructure and reimbursement reforms enabling broader access. The shift toward more targeted interventions-including monoclonal antibodies, small-molecule inhibitors, and immuno-oncology agents-is improving efficacy while reducing side effects, further boosting adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $31.5 Billion |

| Forecast Value | $71.3 Billion |

| CAGR | 8.5% |

The targeted therapies generated USD 21.4 billion in 2024, dominating due to their ability to target cancer-associated biomarkers with fewer adverse reactions. Formats such as antibody-drug conjugates, HER2 inhibitors, and PARP inhibitors are widely adopted across both early- and late-stage treatment protocols. Innovations in HER2 low subtype therapies and AI guided patient stratification support continued market leadership of this category.

The invasive breast cancer segment held 78.9% share in 2024 and is the most prevalent form of disease. Invasive ductal carcinoma alone accounts for about 80% of all invasive cases and roughly 55% of breast cancer diagnoses. Because of its aggressive nature and potential to metastasize beyond the ducts, invasive breast cancer demands broad treatment approaches, including targeted agents, hormone modulators such as SERMs, chemotherapy, and immunotherapies, driving strong clinical demand.

North America Breast Cancer Therapeutics Market held 40.9% share in 2024, with the United States and Canada leading. Advanced healthcare infrastructure, high early detection awareness, strong oncology research investment, and favorable reimbursement systems drove therapeutic adoption. This region benefits from rapid regulatory approvals, high proprietary therapy penetration, and widespread uptake of emerging treatment modalities, reinforcing its leadership in the global breast cancer therapeutics landscape.

Major companies shaping this industry include Pfizer, F. Hoffmann-La Roche, Merck, AstraZeneca, Novartis, and Eli Lilly, driving innovation and global reach. Leading pharmaceutical players are focusing heavily on patient stratification by molecular subtype, enabling precision-targeted therapies optimized with companion diagnostics. Many firms are expanding pipelines in novel modalities such as antibody-drug conjugates, bispecific antibodies, CDK4/6 inhibitors, and immunotherapy combinations to strengthen portfolio depth. Strategic acquisitions, licensing agreements, and strategic partnerships with biotech firms accelerate access to innovative compounds and emerging R&D talent. Global expansion into emerging markets is being achieved through collaborations with regional distributors and healthcare systems. Additionally, firms invest in real-world studies and value-based outcomes to support reimbursement negotiations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Therapy

- 2.2.3 Cancer type

- 2.2.4 Route of administration

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global incidence of breast cancer

- 3.2.1.2 Advancements in targeted and immunotherapies

- 3.2.1.3 Growing awareness and early detection programs

- 3.2.1.4 Increasing demand for personalized medicine and biomarker testing

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects and toxicity of treatments

- 3.2.3 Market opportunities

- 3.2.3.1 Development of novel therapeutics

- 3.2.3.2 Collaborations and strategic partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Pipeline analysis

- 3.6 Regulatory landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Merger and acquisition

- 4.5.2 Partnership and collaboration

- 4.5.3 New product launches

Chapter 5 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Targeted therapy

- 5.3 Hormonal therapy

- 5.4 Chemotherapy

- 5.5 Immunotherapy

Chapter 6 Market Estimates and Forecast, By Cancer Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Ductal carcinoma in situ (DCIS)

- 6.3 Invasive breast cancer

- 6.3.1 Invasive ductal carcinoma (IDC)

- 6.3.1.1 Hormone receptor

- 6.3.1.2 HER2+

- 6.3.1.3 Triple-negative breast cancer (TNBC)

- 6.3.1.4 Other invasive ductal carcinoma (IDC) types

- 6.3.2 Invasive lobular carcinoma (ILC)

- 6.3.1 Invasive ductal carcinoma (IDC)

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 20 - 39

- 8.3 40 - 59

- 8.4 Above 60

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Oncology clinics

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amgen

- 11.2 AstraZeneca

- 11.3 Eisai

- 11.4 Eli Lilly and Company

- 11.5 F. Hoffmann La Roche

- 11.6 GE HealthCare

- 11.7 Gilead Sciences

- 11.8 Macrogenics

- 11.9 Merck

- 11.10 Novartis

- 11.11 Pfizer

- 11.12 Sun Pharmaceutical

乳癌治療市場:按藥物類別、給藥途徑、分銷管道和最終用戶分類的全球市場預測 – 2026-2032 年乳癌治療市場:2026-2032年全球市場預測(依治療方法、作用機制、受體狀態、治療階段、劑型、患者年齡層及最終用戶分類)

乳癌治療市場:按藥物類別、給藥途徑、分銷管道和最終用戶分類的全球市場預測 – 2026-2032 年乳癌治療市場:2026-2032年全球市場預測(依治療方法、作用機制、受體狀態、治療階段、劑型、患者年齡層及最終用戶分類) HER2陽性乳癌市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、模式、分期分類

HER2陽性乳癌市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、最終用戶、模式、分期分類 乳癌治療市場 - 全球產業規模、佔有率、趨勢、機會及預測(按治療方法類型、荷爾蒙療法、標靶治療、最終用戶、地區和競爭格局分類,2021-2031年)

乳癌治療市場 - 全球產業規模、佔有率、趨勢、機會及預測(按治療方法類型、荷爾蒙療法、標靶治療、最終用戶、地區和競爭格局分類,2021-2031年) 男性乳癌治療市場規模、佔有率及成長分析(按類型、產品類型、治療方法、診斷、最終用戶和地區分類)-2026-2033年產業預測

男性乳癌治療市場規模、佔有率及成長分析(按類型、產品類型、治療方法、診斷、最終用戶和地區分類)-2026-2033年產業預測 乳癌藥物市場規模、佔有率和成長分析(治療方法、癌症類型、通路和地區分類)—2026-2033年產業預測

乳癌藥物市場規模、佔有率和成長分析(治療方法、癌症類型、通路和地區分類)—2026-2033年產業預測 乳癌藥物市場規模、佔有率和趨勢分析報告:按治療方法、癌症類型、分銷管道、地區和細分市場預測(2025-2033 年)

乳癌藥物市場規模、佔有率和趨勢分析報告:按治療方法、癌症類型、分銷管道、地區和細分市場預測(2025-2033 年) 乳癌抗體藥物複合體的全球市場:市場機會,專利,價格,認證核可藥的銷售額和臨床試驗趨勢(2030年)Pertuzumab單抗生物相似藥市場(按配方、用途、分銷管道和最終用戶分類)—2025-2030 年全球預測

乳癌抗體藥物複合體的全球市場:市場機會,專利,價格,認證核可藥的銷售額和臨床試驗趨勢(2030年)Pertuzumab單抗生物相似藥市場(按配方、用途、分銷管道和最終用戶分類)—2025-2030 年全球預測 良性乳房病變和早期乳癌市場-全球及區域分析:2025-2035 年分析與預測

良性乳房病變和早期乳癌市場-全球及區域分析:2025-2035 年分析與預測