|

市場調查報告書

商品編碼

1797832

心臟映射市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Cardiac Mapping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

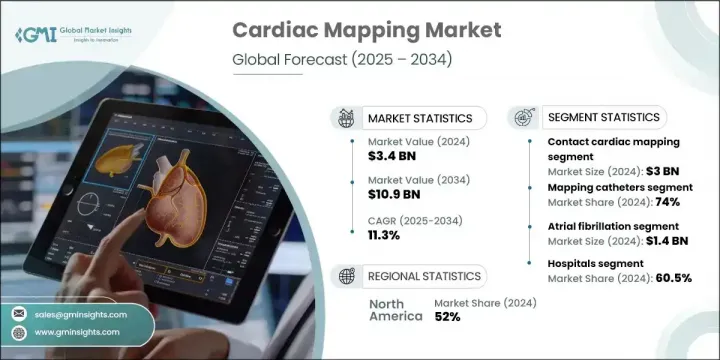

2024年,全球心臟測繪市場規模達34億美元,預計到2034年將以11.3%的複合年成長率成長,達到109億美元。推動這一強勁成長的因素包括:心律不整患者數量的不斷成長、測繪技術的快速創新以及人們對微創診斷程序日益成長的偏好。此外,電生理學領域投資的不斷成長以及心血管醫療服務覆蓋範圍的不斷擴大(尤其是在發展中醫療保健體系中),也正在加速市場的發展。隨著世界各地的心臟科室紛紛採用即時視覺化和精確測繪的新技術,對心臟測繪工具的需求也迅速成長。醫院和專科中心正大力推行精準引導治療,以減少手術併發症並改善病患預後。

醫療現代化的推進,加上支持性報銷框架和全球研究資金的增加,正在為成熟經濟體和新興經濟體的心臟測繪技術塑造一個充滿希望的未來。隨著醫院越來越重視精準醫療和個人化治療方案,對即時心臟診斷的需求也日益成長。醫療保健系統正在投資尖端電生理實驗室,各國政府也提供財政誘因,鼓勵採用微創手術。同時,公共和私人資助機構正在將資源投入到旨在提高測繪準確性、降低手術風險以及開發人工智慧測繪平台的研究中。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 34億美元 |

| 預測值 | 109億美元 |

| 複合年成長率 | 11.3% |

2024年,標測導管市場佔據74%的市佔率。由於複雜心律不整病例的增多,以及微創電生理手術中對高清電解剖資料的需求,該市場保持強勁成長。高密度多電極導管系統正迅速成為業界黃金標準,因為它們使醫生能夠在短時間內收集數萬個資料點,提供無與倫比的細節和準確性。這些標測解決方案有助於更有針對性、更有效率的消融,從而支持心房顫動和室性心動過速的識別和治療。

接觸式心臟標測領域在2024年創造了30億美元的市場規模,預計到2034年將以11.6%的複合年成長率成長。這些系統透過與心臟組織保持持續接觸,提供精確的電生理和解剖學讀數,從而產生極其清晰的活化圖和電壓圖。這種細節程度對於診斷和治療通常需要精確定位的複雜心律不整尤其重要。由於其卓越的訊號質量,接觸式標測工具在臨床電生理學中廣受歡迎。此外,能夠即時追蹤電訊號的自動化心臟標測系統使臨床醫生能夠縮短手術時間,並透過更準確地檢測問題組織來提高消融治療的成功率。

2024年,美國心臟電生理市場規模達17億美元。預計2025年至2034年,該市場的複合年成長率將達到10.6%。美國擁有高度發展的醫療基礎設施,包括配備先進電生理系統的專科電生理實驗室和心臟中心。領先的醫院和學術研究中心定期採用先進的技術執行複雜的消融手術,以提高手術的準確性和安全性。良好的報銷環境和廣泛的電生理治療保險覆蓋範圍,支持了高手術量,並促進了技術的更快普及。

塑造全球心臟測繪市場競爭格局的關鍵參與者包括美敦力、雅培實驗室、強生、波士頓科學、樂普醫療、Kardium、微創醫療科學、APN Health 和 EnChannel Medical。這些公司正透過創新和策略措施積極促進市場發展。主要的心臟測繪公司正透過創新、臨床合作和地理擴張等方式鞏固其市場地位。這些公司正大力投資研發,以推出具有增強電極設計和更快訊號擷取能力的下一代導管。與頂級醫院和學術機構的合作使先進的電解剖測繪平台能夠進行真實世界的測試。許多參與者專注於自動化和 AI 整合軟體,以改善消融過程中的資料分析。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 心血管疾病發生率高

- 提高對心血管疾病治療方案的認知

- 政府對研究和資助的優惠政策

- 產品技術進步

- 產業陷阱與挑戰

- 心臟測繪系統成本高昂

- 缺乏熟練且經驗豐富的電生理學家

- 市場機會

- 映射系統在兒科心臟病學中的應用日益廣泛

- 3D電解剖映射的應用日益廣泛

- 成長動力

- 成長潛力分析

- 監管格局

- 美國

- 歐洲

- 技術格局

- 報銷場景

- 差距分析

- 2024 年全球各產品定價分析

- 地圖系統

- 測繪導管

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 按地區

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 測繪導管

- 地圖系統

第6章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 接觸式心臟測繪

- 非接觸式心臟測繪

第7章:市場估計與預測:按適應症,2021 - 2034 年

- 主要趨勢

- 心房震顫

- 心房撲動

- 室性心搏過速

- 其他適應症

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- EP實驗室

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abbott Laboratories

- APN Health

- Boston Scientific

- EnChannel Medical

- Johnson & Johnson

- Kardium

- Lepu Medical

- Medtronic

- MicroPort Scientific

The Global Cardiac Mapping Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 10.9 billion by 2034. This robust growth is being driven by a rising number of patients diagnosed with cardiac arrhythmias, rapid innovation in mapping technologies, and increased preference for minimally invasive diagnostic procedures. Alongside these factors, growing investments in electrophysiology and expanded access to cardiovascular care-particularly in developing healthcare systems-are accelerating market development. As cardiology departments worldwide adopt new techniques for real-time visualization and accurate mapping, the demand for cardiac mapping tools is rapidly increasing. Hospitals and specialty centers are emphasizing precision-guided treatments to reduce procedural complications and improve patient outcomes.

The push toward healthcare modernization, coupled with supportive reimbursement frameworks and an uptick in global research funding, is shaping a promising future for cardiac mapping technologies across both established and emerging economies. As hospitals increasingly prioritize precision medicine and personalized treatment plans, the demand for real-time cardiac diagnostics is accelerating. Healthcare systems are investing in cutting-edge electrophysiology labs, and governments are offering financial incentives to adopt minimally invasive procedures. At the same time, public and private funding bodies are channeling resources into research aimed at improving mapping accuracy, reducing procedural risks, and developing AI-powered mapping platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 11.3% |

In 2024, the mapping catheters segment held 74% share. This segment remains strong due to growing cases of complex heart rhythm disorders and the need for high-definition electroanatomical data during minimally invasive electrophysiological procedures. High-density and multi-electrode catheter systems are rapidly becoming the gold standard as they allow physicians to collect tens of thousands of data points within moments, offering unmatched detail and accuracy. These mapping solutions support the identification and treatment of atrial fibrillation and ventricular tachycardia by facilitating more targeted and efficient ablation.

The contact cardiac mapping segment generated USD 3 billion in 2024 and is forecasted to grow at a CAGR of 11.6% through 2034. These systems provide precise electrical and anatomical readings by maintaining continuous contact with cardiac tissue, producing exceptionally clear activation and voltage maps. This level of detail is particularly crucial in diagnosing and treating complex arrhythmias that often require pinpoint accuracy. Due to their superior signal quality, contact mapping tools are widely preferred in clinical electrophysiology. Furthermore, automated cardiac mapping systems capable of tracking electrical signals in real time are enabling clinicians to shorten procedures while improving success rates in ablation therapies by detecting problematic tissue with greater accuracy.

United States Cardiac Mapping Market generated USD 1.7 billion in 2024. The market is projected to grow at a CAGR of 10.6% from 2025 to 2034. The country benefits from a highly developed healthcare infrastructure, including specialized electrophysiology labs and cardiac centers outfitted with advanced mapping systems. Leading hospitals and academic research centers routinely perform complex ablation procedures with sophisticated technologies that enhance procedural accuracy and safety. A favorable reimbursement environment and wide insurance coverage for EP treatments support high procedure volumes and facilitate quicker technology adoption.

Key players shaping the competitive landscape in the Global Cardiac Mapping Market include Medtronic, Abbott Laboratories, Johnson & Johnson, Boston Scientific, Lepu Medical, Kardium, MicroPort Scientific, APN Health, and EnChannel Medical. These companies are actively contributing to market evolution through innovation and strategic initiatives. Major cardiac mapping firms are reinforcing their market standing through a combination of innovation, clinical partnerships, and geographic expansion. These companies are investing heavily in R&D to introduce next-generation catheters with enhanced electrode designs and faster signal acquisition capabilities. Collaborations with top-tier hospitals and academic institutions are enabling real-world testing of advanced electroanatomical mapping platforms. Many players are focusing on automation and AI-integrated software to improve data analysis during ablation procedures.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Type trends

- 2.2.4 Indication trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High incidence of cardiovascular diseases

- 3.2.1.2 Rising awareness about the treatment options for cardiovascular diseases

- 3.2.1.3 Favourable government policies for research and funding

- 3.2.1.4 Technological advancements in the products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the cardiac mapping systems

- 3.2.2.2 Lack of skilled and experienced electrophysiologists

- 3.2.3 Market opportunities

- 3.2.3.1 Growing use of mapping systems in pediatric cardiology

- 3.2.3.2 Increasing adoption of 3D electroanatomical mapping

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Gap analysis

- 3.8 Pricing analysis, by product, at global level, 2024

- 3.8.1 Mapping systems

- 3.8.2 Mapping catheters

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

- 3.12 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Latin America

- 4.3.1.5 MEA

- 4.3.1 By Region

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Mapping catheters

- 5.3 Mapping systems

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Contact cardiac mapping

- 6.3 Non-contact cardiac mapping

Chapter 7 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Atrial fibrillation

- 7.3 Atrial flutter

- 7.4 Ventricular tachycardia

- 7.5 Other indications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 EP labs

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 APN Health

- 10.3 Boston Scientific

- 10.4 EnChannel Medical

- 10.5 Johnson & Johnson

- 10.6 Kardium

- 10.7 Lepu Medical

- 10.8 Medtronic

- 10.9 MicroPort Scientific

心臟定位市場:按產品類型、技術、應用和最終用戶分類的全球市場預測 – 2026-2032 年

心臟定位市場:按產品類型、技術、應用和最終用戶分類的全球市場預測 – 2026-2032 年 全球心臟定位市場:按類型、適應症、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年)

全球心臟定位市場:按類型、適應症、最終用戶、國家和地區分類-產業分析、市場規模、佔有率和預測(2025-2032年) 全球心臟定位市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球心臟定位市場規模、佔有率、趨勢和成長分析報告(2026-2034) 心臟定位設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、適應症、最終用途、地區和競爭格局分類,2021-2031年

心臟定位設備市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、適應症、最終用途、地區和競爭格局分類,2021-2031年 心臟定位市場按類型、技術、應用、產品、系統、最終用戶和地區分類

心臟定位市場按類型、技術、應用、產品、系統、最終用戶和地區分類 心臟定位市場規模、佔有率及成長分析(按類型、適應症、最終用戶和地區分類)-2026-2033年產業預測

心臟定位市場規模、佔有率及成長分析(按類型、適應症、最終用戶和地區分類)-2026-2033年產業預測 全球3D心臟定位系統市場:洞察、競爭格局及至2032年預測

全球3D心臟定位系統市場:洞察、競爭格局及至2032年預測 2025年心臟定位全球市場報告全球3D心臟定位系統市場報告(2025年)

2025年心臟定位全球市場報告全球3D心臟定位系統市場報告(2025年) 全球測繪導管市場:市場規模、佔有率、趨勢分析(按技術、適應症、最終用途和地區)、細分市場預測(2025-2030 年)

全球測繪導管市場:市場規模、佔有率、趨勢分析(按技術、適應症、最終用途和地區)、細分市場預測(2025-2030 年)