|

市場調查報告書

商品編碼

1797805

礦物土壤改良劑碳封存市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Mineral Soil Amendments for Carbon Sequestration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

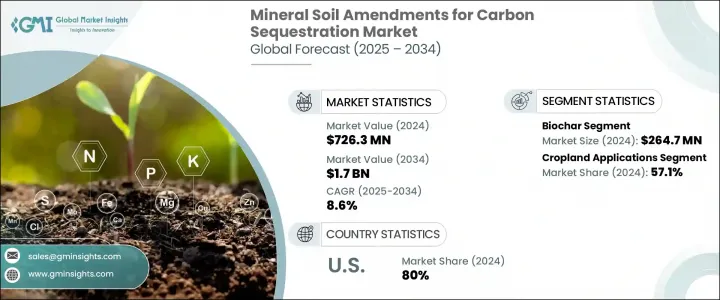

2024 年全球碳封存礦物土壤改良劑市值為 7.263 億美元,預計到 2034 年將以 8.6% 的複合年成長率成長至 17 億美元。人們對減緩氣候變遷的日益關注極大地推動了對基於自然的解決方案的需求,而礦物土壤改良劑正成為這一轉變的有力工具。這些材料——從生物炭到增強風化的礦物和石灰——不僅有助於鎖住土壤中的碳,還能改善土壤結構和肥力。世界各國政府都在透過提供政策誘因、研究支持和碳權機制來支持這項運動。同時,工業界和農業社區也正在採用這些做法,以符合永續發展目標並提高土地生產力。隨著人們對再生農業和減排興趣的日益濃厚,礦物改良劑在各種景觀中都越來越受到關注。對土地退化日益成長的擔憂以及對長期環境復原力的需求繼續推動著這個市場的發展。

隨著人們對環境和經濟效益的認知不斷加深,礦物土壤改良劑不僅被視為氣候解決方案,也被視為提升農業系統生產力的利器。農民和土地所有者開始意識到,這些改良劑帶來的長期價值遠遠超過碳封存。生物炭、玄武岩、石灰和橄欖石等礦物質投入能夠改善土壤結構、增強養分保留和促進有益微生物活性,直接有助於提高作物產量和土壤恢復力。這不僅能提高用水效率,減少對化學肥料的依賴,也能增強土壤對侵蝕和極端天氣條件的抵抗力。因此,將其納入土壤管理計畫正成為永續農業的策略性舉措。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.263億美元 |

| 預測值 | 17億美元 |

| 複合年成長率 | 8.6% |

到2024年,生物炭市場產值將達到2.647億美元,2034年全年複合年成長率將達到8.7%。生物炭憑藉其在碳封存和土壤改善方面的可靠性,成為該市場的主要貢獻者。這種多孔材料透過熱解生成,可以提高保水性,增加微生物壽命,並促進土壤生態系統的養分循環。諸如更移動的熱解裝置和原料最佳化技術等技術創新,使得生物炭的生產更加便利、成本更低。這正在擴大其在大型農場和永續發展驅動型企業的應用。然而,為了確保更廣泛的市場可靠性和信任度,仍需應對諸如原料投入品質不穩定以及缺乏標準化認證架構等挑戰。

2024年,農地應用領域佔57.1%的佔有率,預計2025年至2034年的複合年成長率為8.5%。農田仍是礦物土壤改良劑的主要應用領域,石灰、玄武岩和生物炭等材料的使用量不斷增加,以提高生產力和碳封存。農民正在利用這些投入來保持水分、穩定養分並提高產量,同時實現氣候目標。這些土壤處理方法不僅改善了土地的性能,還透過將碳封存在地下來幫助抵消排放。隨著對永續農業的需求不斷成長,農地應用在向再生和低碳農業體系轉變的過程中發揮著至關重要的作用。

2024年,北美碳封存礦物土壤改良劑市場產值達2.209億美元。美國以80%的佔有率(相當於1.492億美元)保持主導地位。美國憑藉其先進的耕作方式和對永續農業計畫的大力資金支持,已成為領跑者。研究機構、私人企業和政府機構正在合作,加強土壤改良劑的使用,以捕獲碳並提高土壤活力。這項方法得到了一系列政策、補貼和州級計畫的支持,這些計畫旨在支持相關實施,使美國成為推動該地區創新和應用的關鍵力量。

全球碳封存礦物土壤改良劑市場的主要實體包括 Indigo Agriculture、Mati Carbon、Lithos Carbon、Biochar Supreme、Nori、Pacific Biochar、Regen Network、Cool Planet、Soil Capital、UNDO Carbon Ltd.、InPlanet、Dagan、Carbonfuture、Silicate 和 Carbofex。這些公司在擴大氣候智慧型土壤解決方案和提高產品可用性方面發揮著至關重要的作用。許多公司正在投資研發,以開發適合各種土壤類型和氣候的高性能礦物混合物和生物炭產品。與農業合作社和碳補償平台的策略合作夥伴關係有助於建立強大的供應鏈並接觸新的客戶群。一些公司正專注於建造行動處理單元和在地化生產中心,以降低物流成本並提高採用率。此外,一些參與者正在努力建立認證和驗證框架,以增強市場信任並將其產品整合到碳權系統中。這種多管齊下的方法使他們能夠在快速發展的市場中保持競爭力並擴大影響力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 衝擊力

- 成長動力

- 氣候政策與淨零承諾

- 碳權市場發展與定價

- 農業永續性和土壤健康舉措

- 技術進步和成本降低

- 產業陷阱與挑戰

- 實施成本高,經濟障礙多

- 測量、報告和驗證的複雜性

- 市場機會

- 成長動力

- 成長潛力分析

- 監管格局

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 科技與創新格局

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東非洲

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依修訂類型,2021-2034 年

- 主要趨勢

- 生物炭

- 增強耐候材料

- 玄武岩和橄欖石

- 其他矽酸鹽礦物(如矽灰石、蛇紋石)

- 石灰和石灰石的應用

- 沸石和粘土礦物

- 有機礦物混合改良劑

- 新興的改良技術

- 奈米強化礦物改良劑

- 功能化碳材料

- 微生物-礦物質組合

第6章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 農地應用

- 一年生作物系統

- 多年生作物系統

- 土壤健康和生產力提高

- 草原和牧場管理

- 牲畜放牧系統

- 提高牧草產量

- 草原碳封存

- 林業和農林業

- 森林土壤管理

- 農林業系統

- 植樹造林管理

- 土地恢復與復墾

- 退化土地恢復

- 礦場修復

- 濕地和河岸修復

第7章:市場估計與預測:依最終用途領域,2021-2034

- 主要趨勢

- 商業性農業

- 大規模農業經營

- 精準農業整合

- 永續農業認證

- 小農和家庭農業

- 小規模生產者應用

- 擴展服務整合

- 金融包容性和支持

- 碳農業和補償項目

- 專用碳封存項目

- 自願性碳市場整合

- 合規碳市場應用

- 研究與開發

- 學術研究機構

- 私部門研發

- 試點示範項目

- 政府和公共部門

- 國家氣候計劃

- 農業政策實施

- 土地管理機構

第8章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- MEA

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- UNDO Carbon Ltd.

- InPlanet

- Silicate

- Lithos Carbon

- Mati Carbon

- Carbonfuture

- Pacific Biochar

- Biochar Supreme

- Carbofex

- Cool Planet

- Nori

- Indigo Agriculture

- Regen Network

- Soil Capital

- Dagan

The Global Mineral Soil Amendments for Carbon Sequestration Market was valued at USD 726.3 million in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 1.7 billion by 2034. Growing attention toward climate change mitigation is significantly driving demand for nature-based solutions, with mineral soil amendments emerging as a powerful tool in this transformation. These materials-ranging from biochar to enhanced weathering minerals and lime-not only help lock carbon in the soil but also improve soil structure and fertility. Governments across the globe are backing this movement by offering policy incentives, research support, and carbon credit mechanisms. In parallel, industries and farming communities are adopting these practices to align with sustainability goals and improve land productivity. With heightened interest in regenerative agriculture and emissions reduction, mineral amendments are gaining traction across varied landscapes. Rising concerns about land degradation and the need for long-term environmental resilience continue to push this market forward.

As awareness of the environmental and economic benefits grows, mineral soil amendments are increasingly seen not just as a climate solution but also as a productivity enhancer for agricultural systems. Farmers and landowners are beginning to recognize that these amendments provide long-term value far beyond carbon sequestration. By improving soil structure, enhancing nutrient retention, and promoting beneficial microbial activity, mineral inputs such as biochar, basalt, lime, and olivine contribute directly to increased crop yields and soil resilience. This leads to better water efficiency, reduced reliance on chemical fertilizers, and greater resistance to erosion and extreme weather conditions. As a result, their integration into soil management plans is becoming a strategic move for sustainable agriculture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $726.3 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 8.6% |

The biochar segment generated USD 264.7 million by 2024, with a consistent CAGR of 8.7% throughout 2034. Biochar is a leading contributor within this market, thanks to its reliability in both carbon sequestration and enhancing soil quality. Created through pyrolysis, this porous material improves water retention, increases microbial life, and supports nutrient cycling in soil ecosystems. Innovations in technology, such as more mobile pyrolysis units and feedstock optimization techniques, are making biochar easier and more affordable to produce. This is expanding its adoption among large-scale farms and sustainability-driven enterprises. However, challenges such as inconsistent quality of feedstock inputs and the lack of standardized certification frameworks still need to be addressed to ensure broader market reliability and trust.

In 2024, the cropland applications segment held 57.1% share and is expected to grow at a CAGR of 8.5% from 2025 through 2034. Cropland remains the dominant application area for mineral soil amendments, with increased use of materials like lime, basalt, and biochar to boost productivity and carbon sequestration. Farmers are turning to these inputs to retain moisture, stabilize nutrients, and boost yields, all while meeting climate goals. These soil treatments are not just improving the land's performance-they're also helping to offset emissions by storing carbon underground. As demand for sustainable agriculture increases, cropland applications are proving critical in the shift toward regenerative and carbon-conscious farming systems.

North America Mineral Soil Amendments for Carbon Sequestration Market generated USD 220.9 million in 2024. United States maintained its dominant position with an 80% share, translating to USD 149.2 million. The U.S. has emerged as a frontrunner due to its progressive farming practices and significant financial support for sustainable agriculture initiatives. Research institutions, private companies, and government agencies are collaborating to enhance the use of soil amendments that trap carbon and improve soil vitality. This approach is backed by a framework of policies, subsidies, and state-level programs that support implementation, making the U.S. a key force in driving innovation and adoption across the region.

Leading entities operating in the Global Mineral Soil Amendments for Carbon Sequestration Market include Indigo Agriculture, Mati Carbon, Lithos Carbon, Biochar Supreme, Nori, Pacific Biochar, Regen Network, Cool Planet, Soil Capital, UNDO Carbon Ltd., InPlanet, Dagan, Carbonfuture, Silicate, and Carbofex. These companies play a crucial role in scaling up climate-smart soil solutions and advancing product availability. Many are investing in R&D to develop high-performance mineral blends and biochar products tailored for various soil types and climates. Strategic partnerships with agricultural cooperatives and carbon offset platforms are helping to build robust supply chains and access new customer segments. Some firms are focusing on building mobile processing units and localized production hubs to reduce logistics costs and increase adoption rates. Additionally, several players are working toward certification and verification frameworks to enhance market trust and integrate their products into carbon credit systems. This multifaceted approach enables them to remain competitive and expand their reach in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Climate policy and net-zero commitments

- 3.2.1.2 Carbon credit market development and pricing

- 3.2.1.3 Agricultural sustainability and soil health initiatives

- 3.2.1.4 Technology advancement and cost reduction

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation costs and economic barriers

- 3.2.2.2 Measurement, reporting, and verification complexity

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Amendment Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Biochar

- 5.3 Enhanced weathering materials

- 5.3.1 Basalt and olivine

- 5.3.2 Other silicate minerals (e.g., wollastonite, serpentine)

- 5.4 Lime and limestone applications

- 5.5 Zeolites and clay minerals

- 5.6 Organic-mineral hybrid amendments

- 5.7 Emerging amendment technologies

- 5.8 Nano-enhanced mineral amendments

- 5.9 Functionalized carbon materials

- 5.10 Microbial-mineral combinations

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cropland applications

- 6.2.1 Annual crop systems

- 6.2.2 Perennial crop systems

- 6.2.3 Soil health and productivity enhancement

- 6.3 Grassland and pasture management

- 6.3.1 Livestock grazing systems

- 6.3.2 Forage production enhancement

- 6.3.3 Carbon sequestration in grasslands

- 6.4 Forestry and agroforestry

- 6.4.1 Forest soil management

- 6.4.2 Agroforestry systems

- 6.4.3 Tree plantation management

- 6.5 Land restoration and rehabilitation

- 6.5.1 Degraded land recovery

- 6.5.2 Mine site rehabilitation

- 6.5.3 Wetland and riparian restoration

Chapter 7 Market Estimates & Forecast, By End Use Sector, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial agriculture

- 7.2.1 Large-scale farming operations

- 7.2.2 Precision agriculture integration

- 7.2.3 Sustainable agriculture certification

- 7.3 Smallholder and family farming

- 7.3.1 Small-scale producer applications

- 7.3.2 Extension service integration

- 7.3.3 Financial inclusion and support

- 7.4 Carbon farming and offset projects

- 7.4.1 Dedicated carbon sequestration projects

- 7.4.2 Voluntary carbon market integration

- 7.4.3 Compliance carbon market applications

- 7.5 Research and development

- 7.5.1 Academic research institutions

- 7.5.2 Private sector R&D

- 7.5.3 Pilot and demonstration projects

- 7.6 Government and public sector

- 7.6.1 National climate programs

- 7.6.2 Agricultural policy implementation

- 7.6.3 Land management agencies

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 UNDO Carbon Ltd.

- 9.2 InPlanet

- 9.3 Silicate

- 9.4 Lithos Carbon

- 9.5 Mati Carbon

- 9.6 Carbonfuture

- 9.7 Pacific Biochar

- 9.8 Biochar Supreme

- 9.9 Carbofex

- 9.10 Cool Planet

- 9.11 Nori

- 9.12 Indigo Agriculture

- 9.13 Regen Network

- 9.14 Soil Capital

- 9.15 Dagan

土壤改良劑市場:按類型、土壤類型、劑型、作物類型、通路和最終用途分類-2026-2032年全球市場預測土壤改良劑市場:按類型、配方、土壤類型、作物類型、應用和分銷管道分類-2026-2032年全球市場預測

土壤改良劑市場:按類型、土壤類型、劑型、作物類型、通路和最終用途分類-2026-2032年全球市場預測土壤改良劑市場:按類型、配方、土壤類型、作物類型、應用和分銷管道分類-2026-2032年全球市場預測 2026年全球土壤肥力檢測市場報告土壤燻蒸劑市場:依化學類型、作物類型、應用方法和劑型分類-2026年至2032年全球市場預測土壤潤濕劑市場:按類型、形態、作物類型、應用方法和分銷管道分類-2026-2032年全球市場預測

2026年全球土壤肥力檢測市場報告土壤燻蒸劑市場:依化學類型、作物類型、應用方法和劑型分類-2026年至2032年全球市場預測土壤潤濕劑市場:按類型、形態、作物類型、應用方法和分銷管道分類-2026-2032年全球市場預測 土壤改良劑市場分析及預測(至2035年):類型、應用、形式、材質類型、技術、最終用戶、組件、製程和解決方案2026年全球土壤改良劑市場報告2026年全球土壤改良材料市場報告

土壤改良劑市場分析及預測(至2035年):類型、應用、形式、材質類型、技術、最終用戶、組件、製程和解決方案2026年全球土壤改良劑市場報告2026年全球土壤改良材料市場報告 土壤改良劑市場規模、佔有率和趨勢分析報告:按產品、溶解度、土壤類型、作物類型、地區和細分市場預測(2026-2033 年)

土壤改良劑市場規模、佔有率和趨勢分析報告:按產品、溶解度、土壤類型、作物類型、地區和細分市場預測(2026-2033 年) 土壤處理和肥力市場預測至2032年:按類型、技術、配方、作物類型、應用、最終用戶和地區分類的全球分析

土壤處理和肥力市場預測至2032年:按類型、技術、配方、作物類型、應用、最終用戶和地區分類的全球分析