|

市場調查報告書

商品編碼

1797795

水陸兩棲飛機市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Amphibious Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

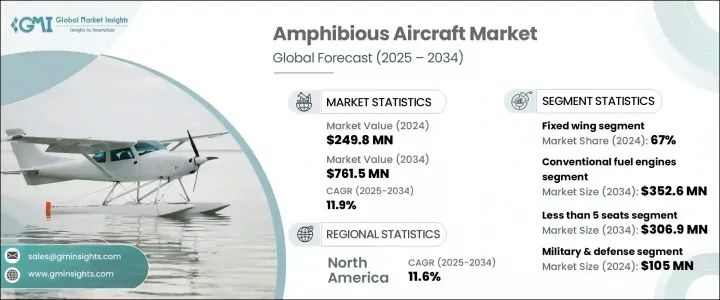

2024年,全球兩棲飛機市場規模達2.498億美元,預計2034年將以11.9%的複合年成長率成長,達到7.615億美元。強勁的成長勢頭主要源於人們對靈活的飛機租賃模式日益成長的興趣,以及偏遠沿海地區對多功能航空運輸日益成長的需求。由於機隊營運商致力於最佳化資本和營運效率,租賃兩棲飛機可以輕鬆調整機隊組成,從而能夠快速響應不斷變化的任務需求,從監視和物流到旅遊和緊急服務。

推動需求成長的關鍵因素是租賃帶來的更高靈活性。透過避免大量的前期投資,商業和專業營運商都可以使用更新、更先進的飛機,同時保留即時擴展機隊的選擇。這種方法對於需要適應不斷變化的環境的行動尤其有用,例如人道主義任務、離岸物流或偏遠地區的區域互聯互通。此外,海上旅遊和休閒航空旅行的日益普及,也促進了兩棲飛機在成熟市場和新興市場的部署。在水上降落往往是傳統飛機跑道唯一可行替代方案的地區,這些飛機越來越被視為一種經濟高效且省時的解決方案。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.498億美元 |

| 預測值 | 7.615億美元 |

| 複合年成長率 | 11.9% |

按飛機類型細分,固定翼飛機在2024年將以67%的市佔率領先市場。固定翼兩棲飛機憑藉其遠程能力、更大的有效載荷和燃油效率,持續受到青睞。這些飛機通常更適合執行需要遠距離覆蓋的任務。耐腐蝕材料、升級的航空電子設備和改進的短距起降能力等技術改進,使固定翼平台在各種應用中更加可靠。其操作靈活性,尤其是在惡劣環境條件下,確保了民用和政府部門的持續需求。

根據推進類型,市場分為混合電力推進系統、傳統燃料引擎和全電動推進系統。傳統燃料引擎在推進領域佔據主導地位,預計到2034年該細分市場的規模將達到3.526億美元。對於需要高續航能力、更大續航里程和在關鍵任務中保持穩定性能的營運商而言,這些引擎仍然是首選。即使混合動力和電動技術已開始在早期部署階段進入市場,其可靠性和強大的功率輸出也使其成為國防、消防和長途運輸的理想選擇。

根據應用,兩棲飛機市場可分為軍事和國防、商業以及政府和公共部門。 2024年,軍事和國防領域的市場規模為1.05億美元。國防機構對特定任務飛機平台的持續投資凸顯了兩棲飛機在戰略行動中的重要性。這些飛機在海上偵察、戰術運輸和沿海監視中發揮著至關重要的作用。隨著對監視、夜間作戰和雷達整合的日益重視,現代兩棲平台正在根據軍隊不斷變化的需求進行客製化,尤其是在海岸線和島嶼地區。

從地區來看,北美在兩棲飛機市場佔據主導地位,2024 年將佔據全球 35.1% 的佔有率,預計預測期內複合年成長率將達到 11.6%。該地區兩棲飛機的廣泛使用源自於戰略和商業需求。北美綿長的海岸線、島嶼群和偏遠社區對能夠在陸地和水上條件下作業的飛機產生了強勁的需求。資金和機構支持的充足性進一步加速了多個領域兩棲機隊的現代化。

在北美,美國引領市場,2024 年估值達 7,720 萬美元。水陸兩棲飛機在美國被廣泛用於遠端監視、快速部署和後勤支援。政府對海上航空資產的大力支持凸顯了這些平台的戰略重要性。該領域的投資反映出,各方對確保海上環境中空中戰備狀態的重視程度日益增強。

塑造兩棲飛機市場競爭格局的關鍵參與者包括ICON Aircraft、德哈維蘭加拿大公司、赤道飛機公司、中航工業、AeroVolga、海納航空、Glasair Aviation、Atol Aviation和Dornier Seawings。這些公司積極致力於下一代飛機模型的開發,提升性能、安全性和適應性,以滿足軍事、商業和公共服務領域多樣化的客戶群的需求。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 擴大採用飛機租賃來支援機隊擴張和營運靈活性

- 擴大海洋旅遊和休閒活動

- 在救災和人道任務中的應用增加

- 海軍和海岸警衛隊艦隊的現代化

- 新興經濟體國防採購投資增加

- 產業陷阱與挑戰

- 購置和營運成本高

- 複雜的認證和法規核准

- 市場機會

- 混合動力和電動兩棲飛機的開發

- 島國和偏遠沿海地區尚未開發的需求

- 水陸兩棲飛機融入緊急醫療服務(EMS)

- 私人包機和旅遊業者的參與度不斷提高

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 永續發展舉措

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按飛機類型,2021 - 2034 年

- 主要趨勢

- 固定翼

- 旋翼機

第6章:市場估計與預測:按推進類型,2021 - 2034 年

- 主要趨勢

- 傳統燃料引擎

- 渦輪螺旋槳

- 活塞

- 混合電力推進

- 全電力推進

第7章:市場估計與預測:按座位容量,2021 - 2034 年

- 主要趨勢

- 少於5個席位

- 5-10個座位

- 超過10個席位

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 軍事與國防

- 監視和巡邏

- 搜救

- 兩棲攻擊與運輸

- 商業的

- 客運

- 貨運與物流

- 旅遊

- 政府和公共部門

- 救災

- 消防

- 海事執法

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- AeroVolga

- Atol Aviation

- AVIC

- De Havilland Canada

- Dornier Seawings

- Equator Aircraft

- Glasair Aviation

- Hynaero

- Icon Aircraft

- Jekta Switzerland

- Legend Aircraft

- Lisa Airplanes

- Maule Air

- Osprey Aircraft

- ShinMaywa Industries

- Textron

- TL Ultralight

- Vickers Aircraft

The Global Amphibious Aircraft Market was valued at USD 249.8 million in 2024 and is estimated to grow at a CAGR of 11.9% to reach USD 761.5 million by 2034. This strong growth trajectory is largely driven by increasing interest in flexible aircraft leasing models and the rising demand for versatile air transportation in remote coastal areas. As fleet operators aim to optimize both capital and operational efficiency, leasing amphibious aircraft allows for easy adjustments in fleet composition, enabling a rapid response to shifting mission profiles, from surveillance and logistics to tourism and emergency services.

A key factor fueling demand is the enhanced flexibility that leasing provides. By avoiding large upfront investments, both commercial and specialized operators can access newer, more advanced aircraft while retaining the option to scale their fleet in real time. This approach is especially useful for operations that require adaptability in changing conditions, such as humanitarian missions, offshore logistics, or regional connectivity in isolated areas. Additionally, the growing popularity of marine tourism and recreational air travel has contributed to greater deployment of amphibious aircraft in both established and emerging markets. These aircraft are increasingly seen as a cost-effective and time-saving solution in regions where water landings are often the only viable alternative to conventional airstrips.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $249.8 Million |

| Forecast Value | $761.5 Million |

| CAGR | 11.9% |

When segmented by aircraft type, the fixed-wing category leads the market with a 67% share in 2024. Fixed-wing amphibious aircraft continue to gain traction due to their long-range capabilities, larger payload capacity, and fuel efficiency. These aircraft are typically preferred for missions requiring extended coverage over large distances. Technological enhancements such as corrosion-resistant materials, updated avionics, and improved STOL capabilities have made fixed-wing platforms more reliable for diverse applications. Their operational versatility, especially in adverse environmental conditions, ensures continued demand across both civilian and government sectors.

Based on propulsion type, the market is categorized into hybrid-electric propulsion, conventional fuel engines, and fully electric propulsion systems. Conventional fuel engines dominate the propulsion landscape, with the segment projected to reach USD 352.6 million by 2034. These engines remain the preferred choice for operators requiring high endurance, extended operational range, and consistent performance in critical missions. Their reliability and strong power output make them ideal for defense, firefighting, and long-distance transport roles, even as hybrid and electric technologies begin to enter the market in early-stage deployments.

By application, the amphibious aircraft market is divided into military & defense, commercial, and government & public sector. The military & defense segment accounted for USD 105 million in 2024. Continued investments in mission-specific aircraft platforms by defense organizations underscore the relevance of amphibious aircraft in strategic operations. These aircraft play a crucial role in maritime reconnaissance, tactical transport, and coastal monitoring. With increasing emphasis on surveillance, night-time operations, and radar integration, modern amphibious platforms are being tailored to meet the evolving needs of military forces, particularly in regions with extended coastlines and island territories.

Regionally, North America commands a dominant position in the amphibious aircraft market, accounting for 35.1% of the global share in 2024 and anticipated to grow at a CAGR of 11.6% through the forecast period. The widespread use of amphibious aircraft in this region stems from both strategic and commercial requirements. North America's extensive coastline, island clusters, and remote communities have created strong demand for aircraft capable of operating in both land and water conditions. The availability of funding and institutional support has further accelerated the modernization of amphibious fleets across multiple sectors.

Within North America, the United States leads the market, recording a valuation of USD 77.2 million in 2024. Amphibious aircraft are widely used in the country for long-range surveillance, rapid deployment, and logistics support. Strong government backing for sea-capable aviation assets highlights the strategic importance of these platforms. Investments in this sector reflect a growing commitment to ensuring aerial readiness in maritime environments.

Key players shaping the competitive landscape of the amphibious aircraft market include ICON Aircraft, De Havilland Canada, Equator Aircraft, AVIC, AeroVolga, Hynaero, Glasair Aviation, Atol Aviation, and Dornier Seawings. These companies are actively engaged in the development of next-generation aircraft models, enhancing performance, safety, and adaptability to cater to a diverse customer base across military, commercial, and public service applications.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Aircraft type trends

- 2.2.2 Propulsion type trends

- 2.2.3 Seating capacity trends

- 2.2.4 Application trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of aircraft leasing to support fleet expansion and operational flexibility

- 3.2.1.2 Expansion of marine tourism and recreational activities

- 3.2.1.3 Increased use in disaster relief and humanitarian missions

- 3.2.1.4 Modernization of naval and coast guard fleets

- 3.2.1.5 Rising investments in defense procurement by emerging economies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High acquisition and operational costs

- 3.2.2.2 Complex certification and regulatory approvals

- 3.2.3 Market opportunities

- 3.2.3.1 Development of hybrid and electric amphibious aircraft

- 3.2.3.2 Untapped demand in island nations and remote coastal regions

- 3.2.3.3 Integration of amphibious aircraft in emergency medical services (EMS)

- 3.2.3.4 Growing participation of private charter and tourism operators

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Defense budget analysis

- 3.13 Global defense spending trends

- 3.14 Regional defense budget allocation

- 3.14.1 North America

- 3.14.2 Europe

- 3.14.3 Asia Pacific

- 3.14.4 Middle East and Africa

- 3.14.5 Latin America

- 3.15 Key defense modernization programs

- 3.16 Budget forecast (2025-2034)

- 3.16.1 Impact on industry growth

- 3.16.2 Defense budgets by country

- 3.17 Sustainability initiatives

- 3.18 Supply chain resilience

- 3.19 Geopolitical analysis

- 3.20 Workforce analysis

- 3.21 Digital transformation

- 3.22 Mergers, acquisitions, and strategic partnerships landscape

- 3.23 Risk assessment and management

- 3.24 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Fixed wing

- 5.3 Rotary wing

Chapter 6 Market Estimates and Forecast, By Propulsion Type, 2021 - 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Conventional fuel engines

- 6.3 Turboprop

- 6.4 Piston

- 6.5 Hybrid-electric propulsion

- 6.6 Fully electric propulsion

Chapter 7 Market Estimates and Forecast, By Seating Capacity, 2021 - 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Less than 5 seats

- 7.3 5-10 seats

- 7.4 More than 10 seats

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Military & defense

- 8.2.1 Surveillance & patrol

- 8.2.2 Search & rescue

- 8.2.3 Amphibious assault & transport

- 8.3 Commercial

- 8.3.1 Passenger transport

- 8.3.2 Cargo & logistics

- 8.3.3 Tourism

- 8.4 Government & public sector

- 8.4.1 Disaster relief

- 8.4.2 Firefighting

- 8.4.3 Maritime law enforcement

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AeroVolga

- 10.2 Atol Aviation

- 10.3 AVIC

- 10.4 De Havilland Canada

- 10.5 Dornier Seawings

- 10.6 Equator Aircraft

- 10.7 Glasair Aviation

- 10.8 Hynaero

- 10.9 Icon Aircraft

- 10.10 Jekta Switzerland

- 10.11 Legend Aircraft

- 10.12 Lisa Airplanes

- 10.13 Maule Air

- 10.14 Osprey Aircraft

- 10.15 ShinMaywa Industries

- 10.16 Textron

- 10.17 TL Ultralight

- 10.18 Vickers Aircraft