|

市場調查報告書

商品編碼

1797792

絕緣玻璃單元 (IGU) 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Insulating Glass Units (IGUs) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球中空玻璃市場規模達 665 億美元,預計到 2034 年將以 7.5% 的複合年成長率成長,達到 1,350 億美元。全球日益嚴格的能源效率要求在推動中空玻璃 (IGU) 需求方面發揮重要作用。各國政府正努力提高建築物的熱性能,從而更多地安裝採用先進塗層的多層玻璃單元。這些趨勢在新建住宅和商業建築項目中尤其明顯,因為在這些項目中,遵守修訂後的能源法規是不可或缺的。最新的建築規範對 U 係數和太陽得熱係數 (SHGC) 提出了更嚴格的限制,鼓勵建築商投資低輻射塗層和充氣中空玻璃單元 (IGU)。這種在不影響預算的情況下對效能的日益重視,鼓勵了人們使用成本最佳化的配置。

永續性基準和生態認證正將中空玻璃單元(IGU)推向綠建築合規的聚光燈下。注重能源性能的認證系統越來越依賴中空玻璃單元(IGU)來累積信用。不斷上漲的能源費用和大眾對環境問題的認知也促使消費者尋求更有效率的解決方案。中空玻璃單元(IGU)透過改善隔熱性能來幫助減少供暖和製冷負荷,從而為屋主和商業物業管理者帶來實際的長期節約。隨著中空玻璃單元(IGU)在環保建築中的應用日益廣泛,它已成為節能建築策略的核心要素。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 665億美元 |

| 預測值 | 1350億美元 |

| 複合年成長率 | 7.5% |

2024年,雙層中空玻璃單元(IGU)市值達349億美元,預計2025年至2034年的複合年成長率為5.8%。這類單元因其在成本效益和基準能源合規性之間的平衡而保持著廣泛的吸引力。它們在溫和氣候和預算有限的項目中尤其受歡迎。另一方面,對三層中空玻璃單元(IGU)的需求正在成長,尤其是在寒冷地區和尋求綠色建築認證的項目中。這些高性能產品具有更好的隔熱和隔音效果,對追求卓越熱性能的住宅和商業開發商都具有吸引力。隨著熱標準日益嚴格,人們擴大轉向更先進的多層配置。

2024年,新建築市場價值達325億美元,預計到2034年將以6.6%的複合年成長率成長。新建築從一開始就將中空玻璃單元(IGU)納入建築設計,以滿足最新的能源法規要求。開發商傾向於在規劃階段早期就將中空玻璃單元納入其中,以確保合規並提升能源資質。這些單元在規模化建設中也具有成本效益,非常適合住宅綜合體、辦公大樓和教育機構等大型專案。隨著能源法規日益嚴格,開發商正在將中空玻璃單元嵌入規範中,以避免追溯升級並簡化施工核准流程。

美國中空玻璃單元 (IGU) 市場在 2024 年的產值達到 165 億美元,預計到 2034 年將以 7.2% 的複合年成長率成長。該地區受益於成熟的建築規範、先進的能源政策以及對永續發展的大力推動。國家框架正在推動新建和翻新建築對高性能玻璃系統的需求。除了新建案外,由於業主希望降低營運成本並延長使用壽命,該地區各地的老舊建築也正成為 IGU 改造的沃土。隨著綠色建築繼續成為建築業的優先事項,各行各業的需求都很高,尤其是在住宅和商業基礎設施領域。

影響全球絕緣玻璃單元 (IGU) 市場的主要公司包括 NSG Group(皮爾金頓)、Guardian Glass、Cardinal Glass Industries、AGC Inc.(旭硝子)和聖戈班公司。這些公司透過創新、產能和全球影響力的結合在產業中佔據主導地位。其中許多公司正在建築活動不斷增加的地區擴大生產能力,以更有效地滿足不斷成長的需求。主要參與者正在投資研發具有先進熱學和聲學性能的下一代 IGU,通常採用智慧玻璃技術和新塗層配方。與房地產開發商、建築師和能源顧問的合作幫助他們在規劃階段的早期就與即將到來的項目保持一致。此外,公司正在優先考慮永續的生產技術和認證,以滿足環保的建築要求。這些策略幫助大公司鞏固其地位,同時為 IGU 技術開闢新的應用領域。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:2021-2034 年玻璃類型市場估計與預測

- 主要趨勢

- 雙層玻璃中空玻璃單元

- 三層玻璃中空玻璃單元

- 電致變色中空玻璃單元

- 智慧型動態玻璃中空玻璃單元

- 特種玻璃中空玻璃

- 防火 IGU

第6章:市場估計與預測:依技術,2021-2034 年

- 主要趨勢

- Low-e鍍膜技術

- 氣體填充技術

- 氬氣填充系統

- 氪氣和氙氣填充

- 空氣填充標準系統

- 間隔系統技術

- 鋁製間隔條系統

- 暖邊間隔條技術

- 先進的間隔系統

- 密封劑和黏合劑技術

第7章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 住宅建築

- 新建築

- 獨棟住宅

- 多戶住宅

- 客製化和豪華住宅

- 翻新和改造

- 更換窗戶

- 能源效率升級

- 歷史建築翻修

- 新建築

- 商業建築

- 辦公大樓

- 高層建築

- 公司總部

- 混合用途開發項目

- 零售和酒店

- 購物中心

- 飯店和餐廳

- 娛樂設施

- 機構建築

- 教育設施

- 醫療保健建築

- 政府大樓

- 辦公大樓

- 工業應用

- 生產設施

- 倉庫和配送中心

- 資料中心和技術設施

- 專業工業建築

- 帷幕牆系統

- 店面和窗牆應用

第8章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 新建築

- 更換和改造

- 翻新和改造

- 綠建築與永續發展項目

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Saint-Gobain SA

- Guardian Glass

- NSG Group (Pilkington)

- AGC Inc. (Asahi Glass)

- Cardinal Glass Industries

- Viracon

- Xinyi Glass Holdings Limited

- Vitro Architectural Glass

- PPG Industries

- Glas Trosch Holding AG

- ClearVue Technologies Limited

- Thermoseal Group

- Quanex Building Products (Edgetech)

- SAGE Electrochromics (SageGlass)

- View Inc.

- Gentex Corporation

- Pleotint LLC

- National Glass (Australia)

- ToughGlaze

- Glassfab USA

- V-Glass

- Glaston Corporation

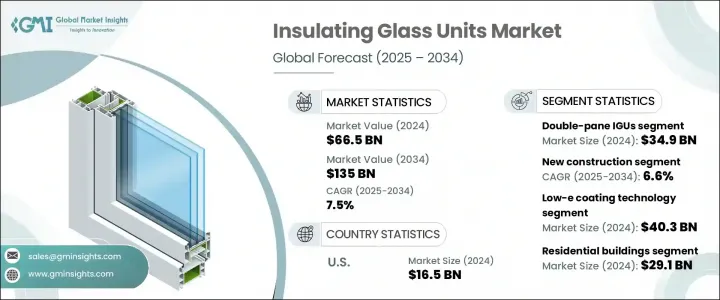

The Global Insulating Glass Units Market was valued at USD 66.5 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 135 billion by 2034. Stricter global energy efficiency mandates are playing a major role in boosting the demand for IGUs. Governments are pushing for better thermal performance in buildings, leading to greater installation of multi-pane units with advanced coatings. These trends are especially notable in new residential and commercial construction projects, where compliance with revised energy codes is non-negotiable. The newest building codes are placing tighter restrictions on U-factor and solar heat gain coefficient (SHGC), encouraging builders to invest in Low-E coatings and gas-filled IGUs. This growing emphasis on performance without compromising on budget is encouraging the use of cost-optimized configurations.

Sustainability benchmarks and eco-certifications are pushing IGUs into the spotlight for green building compliance. Certification systems that focus on energy performance increasingly rely on IGUs for credit accumulation. Rising energy bills and public awareness of environmental issues are also pushing consumers toward more efficient solutions. IGUs help to reduce heating and cooling loads by improving insulation, translating into tangible long-term savings for homeowners and commercial property managers. With their growing relevance in environmentally conscious architecture, IGUs have become a core element of energy-efficient construction strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $66.5 Billion |

| Forecast Value | $135 Billion |

| CAGR | 7.5% |

The double-pane IGUs segment was valued at USD 34.9 billion in 2024 and is projected to grow at a CAGR of 5.8% from 2025 to 2034. These units maintain broad appeal due to their balance between cost-efficiency and baseline energy compliance. Their popularity is especially strong in moderate climates and projects operating within budget constraints. On the other hand, demand for triple-pane IGUs is gaining momentum, particularly in colder regions and projects pursuing green building certifications. These high-performance variants offer better insulation and soundproofing, appealing to both residential and commercial developers aiming for superior thermal performance. As thermal standards become more demanding, there is an increasing shift toward more advanced multi-layer configurations.

The new construction segment was valued at USD 32.5 billion in 2024 and is expected to grow at a CAGR of 6.6% through 2034. New builds integrate IGUs from the outset as part of architectural designs that are required to meet updated energy regulations. Developers prefer to incorporate IGUs early in the planning stages to ensure compliance and boost energy credentials. These units are also cost-effective at scale, making them well-suited for larger projects such as residential complexes, office buildings, and educational institutions. With energy codes becoming increasingly strict, developers are embedding IGUs into specifications to avoid retroactive upgrades and to streamline construction approvals.

United States Insulating Glass Units (IGUs) Market generated USD 16.5 billion in 2024 and is projected to grow at a 7.2% CAGR through 2034. The region benefits from mature building codes, progressive energy policies, and a strong push for sustainability. National frameworks are driving demand for high-performance glazing systems in both new and renovated structures. In addition to new developments, aging buildings across the region are becoming a fertile market for IGU retrofits as owners look to reduce operational costs and extend lifecycle performance. Demand is high across sectors-particularly in residential housing and commercial infrastructure-as green construction continues to shape building priorities.

Major companies shaping the Global Insulating Glass Units (IGUs) Market include NSG Group (Pilkington), Guardian Glass, Cardinal Glass Industries, AGC Inc. (Asahi Glass), and Saint-Gobain S.A. These players dominate the industry through a combination of innovation, volume capacity, and global reach. Many of them are expanding production capabilities in regions with increasing construction activity to meet rising demand more efficiently. Key players are investing in R&D to develop next-generation IGUs with advanced thermal and acoustic properties, often incorporating smart-glass technology and new coating formulations. Partnerships with real estate developers, architects, and energy consultants are helping them align with upcoming projects early in the planning phase. In addition, companies are prioritizing sustainable production techniques and certifications to appeal to environmentally driven construction mandates. These strategies help major firms solidify their presence while opening new application areas for IGU technology.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Glass type

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2021-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Glass Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Double-Pane IGUs

- 5.3 Triple-Pane IGUs

- 5.4 Electrochromic IGUs

- 5.5 Smart And Dynamic Glass IGUs

- 5.6 Specialty Glass IGUs

- 5.7 Fire-Rated IGUs

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low-e coating technology

- 6.3 Gas fill technologies

- 6.3.1 Argon gas fill systems

- 6.3.2 Krypton and xenon fill

- 6.3.3 Air fill standard systems

- 6.4 Spacer system technologies

- 6.4.1 Aluminum spacer systems

- 6.4.2 Warm edge spacer technologies

- 6.4.3 Advanced spacer systems

- 6.5 Sealant and adhesive technologies

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.2.1 New construction

- 7.2.1.1 Single-family homes

- 7.2.1.2 Multi-family housing

- 7.2.1.3 Custom and luxury homes

- 7.2.2 Renovation and retrofit

- 7.2.2.1 Window replacement

- 7.2.2.2 Energy efficiency upgrades

- 7.2.2.3 Historic building renovations

- 7.2.1 New construction

- 7.3 Commercial buildings

- 7.3.1 Office buildings

- 7.3.1.1 High-rise construction

- 7.3.1.2 Corporate headquarters

- 7.3.1.3 Mixed-use developments

- 7.3.2 Retail and hospitality

- 7.3.2.1 Shopping centers

- 7.3.2.2 Hotels and restaurants

- 7.3.2.3 Entertainment facilities

- 7.3.3 Institutional buildings

- 7.3.3.1 Educational facilities

- 7.3.3.2 Healthcare buildings

- 7.3.3.3 Government buildings

- 7.3.1 Office buildings

- 7.4 Industrial applications

- 7.4.1 Manufacturing facilities

- 7.4.2 Warehouses and distribution centers

- 7.4.3 Data centers and technical facilities

- 7.4.4 Specialized industrial buildings

- 7.5 Curtain wall systems

- 7.6 Storefront and window wall applications

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Replacement and retrofit

- 8.4 Renovation and remodeling

- 8.5 Green building and sustainability projects

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Saint-Gobain S.A.

- 10.2 Guardian Glass

- 10.3 NSG Group (Pilkington)

- 10.4 AGC Inc. (Asahi Glass)

- 10.5 Cardinal Glass Industries

- 10.6 Viracon

- 10.7 Xinyi Glass Holdings Limited

- 10.8 Vitro Architectural Glass

- 10.9 PPG Industries

- 10.10 Glas Trosch Holding AG

- 10.11 ClearVue Technologies Limited

- 10.12 Thermoseal Group

- 10.13 Quanex Building Products (Edgetech)

- 10.14 SAGE Electrochromics (SageGlass)

- 10.15 View Inc.

- 10.16 Gentex Corporation

- 10.17 Pleotint LLC

- 10.18 National Glass (Australia)

- 10.19 ToughGlaze

- 10.20 Glassfab USA

- 10.21 V-Glass

- 10.22 Glaston Corporation

2026年全球雙層玻璃窗市場報告

2026年全球雙層玻璃窗市場報告 雙層玻璃窗市場:依產品類型、玻璃類型、間隔條材料、安裝類型、應用和最終用戶分類-2026-2032年全球市場預測玻璃絕緣子市場:2026-2032年全球市場預測(依產品類型、電壓等級、應用、終端用戶產業及通路分類)中空玻璃市場:依產品類型、玻璃類型、技術、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測按電壓等級、每串絕緣子數量、配銷通路和最終用途分類的盤式懸式玻璃絕緣子市場-全球預測,2026-2032年

雙層玻璃窗市場:依產品類型、玻璃類型、間隔條材料、安裝類型、應用和最終用戶分類-2026-2032年全球市場預測玻璃絕緣子市場:2026-2032年全球市場預測(依產品類型、電壓等級、應用、終端用戶產業及通路分類)中空玻璃市場:依產品類型、玻璃類型、技術、應用、最終用戶和分銷管道分類-2026-2032年全球市場預測按電壓等級、每串絕緣子數量、配銷通路和最終用途分類的盤式懸式玻璃絕緣子市場-全球預測,2026-2032年 全球真空絕熱玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球真空絕熱玻璃市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026-2030年全球隔熱玻璃窗市場全球中空玻璃市場:市場規模、份額、成長率、產業分析、按類型、應用和地區劃分的分析以及未來預測(2026-2034)

2026-2030年全球隔熱玻璃窗市場全球中空玻璃市場:市場規模、份額、成長率、產業分析、按類型、應用和地區劃分的分析以及未來預測(2026-2034) 隔熱玻璃窗市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測(2025-2033 年)絕緣膠帶市場(按材料、黏合劑、應用和最終用戶產業分類)—2025-2030 年全球預測

隔熱玻璃窗市場規模、佔有率和趨勢分析報告:按產品類型、最終用途、地區和細分市場預測(2025-2033 年)絕緣膠帶市場(按材料、黏合劑、應用和最終用戶產業分類)—2025-2030 年全球預測