|

市場調查報告書

商品編碼

1797768

物聯網感測器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測IoT Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

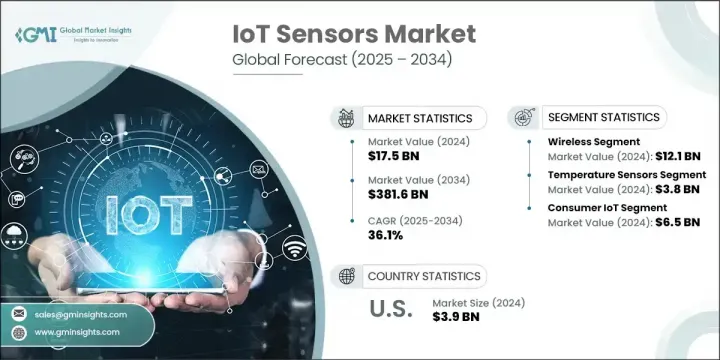

2024年,全球物聯網感測器市場規模達175億美元,預計到2034年將以36.1%的複合年成長率成長,達到3,816億美元。物聯網感測器市場的快速擴張得益於各行各業互聯技術的加速應用和數位轉型。隨著從工業機械到智慧消費設備的互聯設備數量不斷增加,對能夠提供即時洞察的感測器的需求也日益成長。此外,工業4.0的廣泛實施、汽車技術的不斷發展以及即時分析與營運框架的整合也推動了物聯網感測器市場的發展。物聯網感測器是實現自動化、預測性決策和持續系統最佳化的重要組成部分。

製造業、公用事業和醫療保健行業的企業正在從傳統的被動系統轉向預測模型,這種模型透過先進的感測解決方案持續捕獲資料來實現,這些解決方案可以檢測異常、觸發維護並提高營運可靠性。這些預測框架依賴即時分析,而即時分析則由感測器產生的連續資料流驅動,這些資料流可以即時洞察系統性能。透過利用這些智慧訊息,組織可以預測設備故障、安排及時干預措施並最大限度地減少代價高昂的停機時間。在製造業,物聯網感測器正在將生產線轉變為智慧環境,能夠即時適應不斷變化的變量,確保一致性和品質。在公用事業領域,即時監控可以及早發現電網波動或基礎設施壓力,從而降低停電風險。醫療保健機構也在部署基於感測器的系統,以遠端追蹤患者生命徵象、確保設備可用性並維護無菌環境。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 175億美元 |

| 預測值 | 3816億美元 |

| 複合年成長率 | 36.1% |

2024年,無線感測器市場規模達121億美元。其廣泛應用源自於對可擴展且易於部署的解決方案的需求,這些解決方案能夠在動態或遠端環境中有效運作。低功耗廣域網路 (LPWAN)、低功耗藍牙和5G連接技術的創新,使無線感測器成為現代工業監控系統的支柱。這些感測器與邊緣和雲端平台無縫連接,使組織能夠實現自主系統和數據驅動的決策。隨著越來越多的產業轉向分散式營運,無線感測器正逐漸成為在分散式環境中獲取即時洞察的關鍵推動因素。

受智慧家庭環境、醫療保健技術和工業系統日益成長的需求推動,溫度感測器市場在2024年創造了38億美元的市場規模。這些感測器在確保自動化工業流程的安全性、穩定性和合規性方面發揮著至關重要的作用。隨著遠端健康監測和穿戴式技術的快速普及,對緊湊型低功耗溫度感測器的需求日益成長。為了保持競爭力,感測器製造商正在開發高度微型化且節能的型號,以便能夠順利整合到穿戴式裝置和邊緣驅動的應用中。

2024年,美國物聯網感測器市場產值達39億美元。美國在該領域的強勢地位得益於其在智慧基礎設施、國防技術和公共部門現代化方面的大量投資。專注於即時基礎設施管理和預測分析的先進舉措持續支撐著對感測器技術日益成長的需求。此外,旨在提升網路安全和系統互通性的立法框架正在增強互聯感測器生態系統的擴展和信任。

在物聯網感測器市場產生重大影響的公司包括西門子股份公司、森薩塔科技公司、博通公司、歐姆龍公司、霍尼韋爾國際公司、SmartThings 公司、恩智浦半導體公司、意法半導體公司、村田製作所、費加羅工程公司、艾默生電氣公司、Sierra 北電氣公司、Impin 公司、費加羅工程公司、艾默生電氣公司、Sierra 北電氣公司、Impin 公司、Dexjin 公司感測器公司和德州儀器公司。為了擴大影響力和增強市場競爭力,物聯網感測器領域的領先公司正專注於將人工智慧驅動的分析和邊緣運算功能直接整合到他們的感測器中。他們正在積極投資研發,以創建適用於下一代應用的超低功耗和微型設計。與雲端服務供應商和軟體平台的策略合作正在實現跨行業的無縫整合。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 連網設備的激增

- 無線通訊技術的進步

- 工業自動化與工業4.0

- 汽車產業發展(ADAS 和電動車)

- 即時數據監控需求不斷成長

- 陷阱與挑戰

- 初始成本高且投資報酬率不確定

- 資料安全和隱私問題

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按感測器類型,2021 - 2034 年

- 主要趨勢

- 溫度感測器

- 壓力感測器

- 濕度感測器

- 流量感測器

- 加速度計

- 磁力儀

- 陀螺儀

- 慣性感測器

- 影像感測器

- 觸摸感應器

- 接近感測器

- 聲學感測器

- 運動感應器

- 佔用感應器

- 影像處理佔用感應器

- 智慧佔用感應器

- 二氧化碳感測器

- 其他

第6章:市場估計與預測:按網路類型,2021 - 2034 年

- 主要趨勢

- 有線

- KNX

- Lonworks

- 乙太網路

- Modbus

- 其他

- 無線的

- 無線上網

- 藍牙

- Zigbee

- Z-Wave

- 近場通訊

- 射頻識別

- 埃諾西恩

- 無線哈特

- 其他

第7章:市場估計與預測:依最終用途應用,2021 - 2034 年

- 主要趨勢

- 消費者物聯網

- 商業物聯網

- 智慧城市

- 零售

- 航太與國防

- 物流和供應鏈

- 娛樂

- 其他

- 工業物聯網

- 能源

- 工業自動化

- 智慧農業

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Global Key Players

- Regional Key Players

- 顛覆者/利基市場參與者

- Impinj 公司

The Global IoT Sensors Market was valued at USD 17.5 billion in 2024 and is estimated to grow at a CAGR of 36.1% to reach USD 381.6 billion by 2034. The rapid expansion is driven by the accelerating adoption of connected technologies and digital transformation across multiple industries. As the number of connected devices continues to rise, from industrial machinery to smart consumer devices, the demand for sensors capable of delivering real-time insights is intensifying. The market is also benefiting from widespread implementation of Industry 4.0, the evolution of automotive technologies, and the integration of real-time analytics into operational frameworks. IoT sensors serve as essential components enabling automation, predictive decision-making, and continuous system optimization.

Businesses across manufacturing, utilities, and healthcare are moving away from traditional reactive systems toward predictive models, enabled by constant data capture through advanced sensing solutions that detect anomalies, trigger maintenance, and enhance operational reliability. These predictive frameworks rely on real-time analytics, which are fueled by continuous sensor-generated data streams that provide immediate insight into system performance. By leveraging this intelligence, organizations can anticipate equipment failures, schedule timely interventions, and minimize costly downtimes. In manufacturing, IoT sensors are transforming production lines into smart environments that adapt instantly to shifting variables, ensuring consistency and quality. In the utilities sector, real-time monitoring enables early identification of grid fluctuations or infrastructure stress, reducing the risk of outages. Healthcare facilities are also deploying sensor-based systems to track patient vitals remotely, ensure equipment availability, and maintain sterile environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.5 Billion |

| Forecast Value | $381.6 Billion |

| CAGR | 36.1% |

The wireless sensors segment generated USD 12.1 billion in 2024. Their widespread adoption is attributed to the need for scalable and easily deployable solutions that function effectively across dynamic or remote settings. Innovations in low-power wide-area networks (LPWAN), Bluetooth Low Energy, and 5G connectivity have allowed wireless sensors to become the backbone of monitoring systems used in modern industries. These sensors seamlessly link with edge and cloud platforms, allowing organizations to enable autonomous systems and data-driven decision-making. As more industries shift to decentralized operations, wireless sensors are emerging as a key enabler of real-time insights across distributed environments.

The temperature sensors segment generated USD 3.8 billion in 2024, driven by the growing demand from smart home environments, healthcare technologies, and industrial systems. These sensors play a crucial role in ensuring safety, stability, and compliance in automated industrial processes. With the rapid adoption of remote health monitoring and wearable technology, there's a growing requirement for compact, low-power temperature sensors. To stay competitive, sensor manufacturers are developing highly miniaturized and energy-efficient models that integrate smoothly into wearable devices and edge-powered applications.

United States IoT Sensors Market generated USD 3.9 billion in 2024. The nation's stronghold in the sector is powered by significant investments in smart infrastructure, defense technologies, and public sector modernization. Advanced initiatives focused on real-time infrastructure management and predictive analytics continue to support the rising demand for sensor technologies. Additionally, legislative frameworks designed to improve cybersecurity and system interoperability are reinforcing the expansion and trust in connected sensor ecosystems.

Companies making a significant impact in the IoT Sensors Market include Siemens AG, Sensata Technologies, Inc., Broadcom Inc., Omron Corporation, Honeywell International Inc., SmartThings Inc., NXP Semiconductors N.V., STMicroelectronics N.V., Murata Manufacturing Co., Ltd., Figaro Engineering Inc., Emerson Electric Co., Sierra Wireless, Inc., Impinj, Inc., and Kita Sensor Tech. Co., Ltd., Bosch Sensortec GmbH, General Electric Company, TE Connectivity Ltd., DexCom, Inc., and Texas Instruments Incorporated. To expand their presence and enhance market competitiveness, leading companies in the IoT sensors sector are focusing on integrating AI-driven analytics and edge computing capabilities directly into their sensors. They are actively investing in R&D to create ultra-low-power and miniaturized designs suitable for next-gen applications. Strategic collaborations with cloud service providers and software platforms are enabling seamless integration across industries.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Sensor type trend

- 2.2.2 Network type trends

- 2.2.3 End use application trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry ecosystem analysis

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Proliferation of Connected Devices

- 3.3.1.2 Advancements in Wireless Communication Technologies

- 3.3.1.3 Industrial Automation & Industry 4.0

- 3.3.1.4 Automotive Sector Evolution (ADAS & EVs)

- 3.3.1.5 Growing demand for Real-Time Data Monitoring

- 3.3.2 Pitfalls and challenges

- 3.3.2.1 High Initial Costs & ROI Uncertainty

- 3.3.2.2 Data Security & Privacy Concerns

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing Strategies

- 3.11 Emerging Business Models

- 3.12 Compliance Requirements

- 3.13 Sustainability Measures

- 3.14 Consumer Sentiment Analysis

- 3.15 Patent and IP analysis

- 3.16 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Sensors Type, 2021 - 2034 (USD Billion & Million Units)

- 5.1 Key trends

- 5.2 Temperature sensors

- 5.3 Pressure sensors

- 5.4 Humidity sensors

- 5.5 Flow sensors

- 5.6 Accelerometer

- 5.7 Magnetometers

- 5.8 Gyroscopes

- 5.9 Inertial sensors

- 5.10 Image sensors

- 5.11 Touch sensors

- 5.12 Proximity sensors

- 5.13 Acoustic sensors

- 5.14 Motion sensors

- 5.15 Occupancy sensors

- 5.15.1 Image processing occupancy sensors

- 5.15.2 Intelligent occupancy sensors

- 5.16 CO2 sensors

- 5.17 Others

Chapter 6 Market estimates and forecast, by Network Type, 2021 - 2034 (USD Billion & Million Units)

- 6.1 Key trends

- 6.2 Wired

- 6.2.1 KNX

- 6.2.2 Lonworks

- 6.2.3 Ethernet

- 6.2.4 Modbus

- 6.2.5 Others

- 6.3 Wireless

- 6.3.1 WiFi

- 6.3.2 Bluetooth

- 6.3.3 Zigbee

- 6.3.4 Z-Wave

- 6.3.5 Near field communication

- 6.3.6 RFID

- 6.3.7 Enocean

- 6.3.8 Wireless hart

- 6.3.9 Others

Chapter 7 Market estimates and forecast, by End Use Application, 2021 - 2034 (USD Billion & Million Units)

- 7.1 Key trends

- 7.2 Consumer IoT

- 7.3 Commercial IoT

- 7.3.1 Smart cities

- 7.3.2 Retail

- 7.3.3 Aerospace & defense

- 7.3.4 Logistics and supply chain

- 7.3.5 Entertainment

- 7.3.6 Others

- 7.4 Industrial IoT

- 7.4.1 Energy

- 7.4.2 Industrial automation

- 7.4.3 Smart agriculture

- 7.5 Others

Chapter 8 Market estimates and forecast, by Region, 2021 - 2034 (USD Billion & Million Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company profiles

- 9.1 Global Key Players

- 9.1.1 Texas Instruments Incorporated

- 9.1.2 Broadcom Inc.

- 9.1.3 NXP Semiconductors N.V.

- 9.1.4 STMicroelectronics N.V.

- 9.1.5 Honeywell International Inc.

- 9.1.6 Sensata Technologies, Inc.

- 9.1.7 Omron Corporation

- 9.1.8 Siemens AG

- 9.1.9 Emerson Electric Co.

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 TE Connectivity Ltd.

- 9.2.1.2 General Electric Company

- 9.2.1.3 SmartThings Inc.

- 9.2.1.4 DexCom, Inc.

- 9.2.2 Europe

- 9.2.2.1 Bosch Sensortec GmbH

- 9.2.2.2 NXP semiconductor

- 9.2.3 Asia-Pacific

- 9.2.3.1 Murata Manufacturing Co., Ltd.

- 9.2.3.2 Figaro Engineering Inc.

- 9.2.3.3 Kita Sensor Tech. Co., Ltd.

- 9.2.1 North America

- 9.3 Disruptors / Niche Players

- 9.3.1 Impinj, Inc.

全球物聯網感測器市場(至2035年):產業趨勢與預測

全球物聯網感測器市場(至2035年):產業趨勢與預測 物聯網感測器市場:2026-2032年全球市場預測(按感測器類型、連接方式、最終用戶和部署模式分類)

物聯網感測器市場:2026-2032年全球市場預測(按感測器類型、連接方式、最終用戶和部署模式分類) 物聯網感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝模式、解決方案

物聯網感測器市場分析與預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝模式、解決方案 日本物聯網感測器市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年

日本物聯網感測器市場規模、佔有率、趨勢和預測:按類型、應用和地區分類,2026-2034年 2026年全球物聯網感測器市場報告

2026年全球物聯網感測器市場報告 無線物聯網感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、類型、技術、垂直產業、地區和競爭格局分類,2021-2031年)物聯網感測器市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(依感測器類型、應用、網路類型、地區和競爭格局分類),2021-2031年物聯網家庭自動化軟體市場:按組件、部署、連接、應用和最終用戶分類,全球預測(2026-2032)

無線物聯網感測器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、類型、技術、垂直產業、地區和競爭格局分類,2021-2031年)物聯網感測器市場-全球產業規模、佔有率、趨勢、競爭格局、機會及預測(依感測器類型、應用、網路類型、地區和競爭格局分類),2021-2031年物聯網家庭自動化軟體市場:按組件、部署、連接、應用和最終用戶分類,全球預測(2026-2032) 物聯網感測器市場規模、佔有率和成長分析(按感測器類型、組件、技術、最終用戶產業和地區分類)-2026-2033年產業預測

物聯網感測器市場規模、佔有率和成長分析(按感測器類型、組件、技術、最終用戶產業和地區分類)-2026-2033年產業預測 物聯網 (IoT) 感測器市場:全球 2025-2029

物聯網 (IoT) 感測器市場:全球 2025-2029