|

市場調查報告書

商品編碼

1797744

尿液收集設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Urine Collection Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

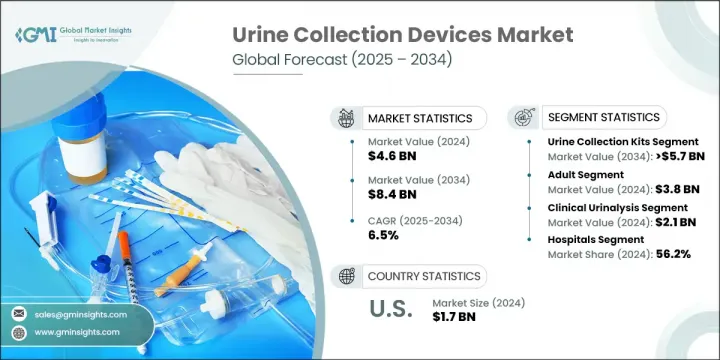

2024年,全球尿液採集設備市場規模達46億美元,預計2034年將以6.5%的複合年成長率成長至84億美元。慢性腎臟病、泌尿道感染以及老齡化人口失禁等日益加重的負擔,有力地推動了市場擴張。居家醫療保健的興起,加上即時診斷技術的蓬勃發展以及設備功能和設計的持續創新,共同塑造著市場趨勢。尿液採集設備在診斷中發揮至關重要的作用,能夠安全、無菌、準確地採集、運輸和儲存尿液樣本。這些工具——從尿杯、樣本袋到採集試劑盒和運輸容器——廣泛應用於醫院、診所、實驗室和家庭。疾病篩檢頻率的提高,尤其是在慢性病照護和代謝診斷領域,正在推動對這些服務的持續需求。隨著分散式醫療保健日益普及,以及以患者為中心的照護模式不斷發展,人們對使用者友善、衛生可靠的尿液採集系統的需求日益成長。這些市場動態正在幫助企業擴大生產規模,同時投資能夠提升樣本處理和診斷精確度的技術。

腎臟病學、腫瘤學和內分泌學等領域的臨床研究日益增多,推動了對兼容基因組學、蛋白質組學和生物標記檢測的先進尿液採集解決方案的需求。研究人員越來越需要無菌、化學穩定的容器,以便在運輸和分析過程中保持樣本的完整性。因此,供應商正在開發更專業的試劑盒,以滿足實驗室研究的需求,從而支持更廣泛的臨床研究生態系統。此外,針對行動不便或慢性病患者的居家照護的擴展,也促進了尿液採集產品在傳統臨床環境之外的更廣泛應用。這種轉變促進了產品設計格局的演變,更重視便攜性、安全性和易用性。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 46億美元 |

| 預測值 | 84億美元 |

| 複合年成長率 | 6.5% |

2024年,尿液採集試劑盒市場佔有69.4%的佔有率。這一強勁地位主要源於對家用診斷試劑盒的日益依賴、分散式臨床試驗的成長以及無菌安全標本處理日益重要。這些試劑盒為臨床機構以外的使用者提供了便利性和可近性,有助於提高診斷依從性和照護的連續性。尿液採集試劑盒在慢性疾病監測、生殖健康和藥物檢測等領域的應用非常廣泛。

臨床尿液分析應用領域在2024年創造了21億美元的市場規模,預計在2025-2034年期間的複合年成長率將達到6.1%。這個領域引領市場,因為尿液檢測仍然是識別各種疾病(從泌尿道感染、糖尿病到腎臟疾病和代謝疾病)的第一線診斷工具。醫院和診斷中心是主要的終端用戶,他們依靠化學穩定、耐污染的設備來確保實驗室結果的準確性。定期健康篩檢和慢性病診斷數量的不斷成長,鞏固了尿液分析作為預防和急性護理基石的地位。

2024年,歐洲尿液採集設備市場規模達13億美元。該地區擁有高度發展的醫療基礎設施,且廣泛採用非侵入性檢測方法。高昂的人均醫療支出和廣泛的公共篩檢項目,正在加速醫院和家庭尿液檢測的需求。西歐和斯堪的納維亞半島國家由於更加重視老年族群慢性泌尿系統疾病的管理,尿液採集設備使用率尤其高。

全球尿液採集設備市場的主要參與者包括 BioTouch、QIAGEN、Ardo Medical、賽默飛世爾科技、羅氏、雅培、POLYMED、Aspen Surgical、Cardinal Health、HENSO、Convatec、Becton、Dickinson and Company、Labcorp (Litholink)、MEDLINE 和 ANGIPLAST。參與尿液採集設備市場競爭的公司正在利用產品創新、策略合作夥伴關係和全球擴張來鞏固其立足點。核心重點在於開發以使用者為中心、無菌和一次性的套件,以符合現代臨床和家庭護理工作流程。許多公司正在投資具有防篡改和樣品保存功能的智慧包裝解決方案,以滿足不斷發展的診斷標準。與醫療保健提供者和實驗室的合作使得能夠共同開發針對特定測試應用的專用產品。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 慢性腎臟病(CKD)盛行率不斷上升

- 老年人口不斷增加

- 非侵入性診斷工具的需求不斷成長

- 尿液收集裝置的技術進步

- 產業陷阱與挑戰

- 污染和樣品處理錯誤的風險

- 市場機會

- 尿液液體活體組織切片和基因組檢測的使用日益增多

- 兒科友善智慧尿液採集裝置的開發

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 新興技術

- 2024年定價分析

- 差距分析

- 波特的分析

- PESTEL分析

- 未來市場趨勢

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 競爭定位矩陣

- 主要市場參與者的競爭分析

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品類型發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 尿液收集套件

- 尿液檢體袋

- 尿杯和容器

第6章:市場估計與預測:按患者,2021 - 2034 年

- 主要趨勢

- 成人

- 兒科

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 臨床尿液分析

- 泌尿道感染(UTI)

- 腎臟疾病

- 其他臨床尿液分析

- 藥物篩選

- 妊娠測試

- 臨床研究和調查

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 診斷實驗室

- 居家照護環境

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Abbott

- ANGIPLAST

- Ardo Medical

- Aspen Surgical

- Becton, Dickinson and Company

- BioTouch

- Cardinal Health

- convatec

- HENSO

- Labcorp (Litholink)

- MEDLINE

- POLYMED

- QIAGEN

- Roche

- Thermo Fisher Scientific

The Global Urine Collection Devices Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 8.4 billion by 2034. Market expansion is strongly supported by the rising burden of chronic kidney diseases, urinary tract infections, and an aging population dealing with incontinence. The shift toward home-based healthcare, together with the growth in point-of-care diagnostics and ongoing innovation in device functionality and design, continues to shape market trends. Urine collection devices play a crucial role in diagnostics by enabling safe, sterile, and accurate sample gathering, transportation, and storage. These tools-ranging from cups and specimen bags to collection kits and transport containers-are extensively used across hospitals, clinics, laboratories, and at-home settings. The increased frequency of disease screening, particularly in chronic care and metabolic diagnostics, is driving sustained demand for these services. As decentralized healthcare becomes more prominent and patient-centric care models evolve, there is significant interest in user-friendly, hygienic, and reliable urine collection systems. These market dynamics are helping companies scale production while investing in technology that enhances sample handling and diagnostic precision.

The rising number of clinical investigations in fields such as nephrology, oncology, and endocrinology is pushing demand for advanced urine collection solutions that are compatible with genomic, proteomic, and biomarker testing. Researchers increasingly require sterile, chemically stable containers that preserve sample integrity during transport and analysis. As a result, suppliers are developing more specialized kits tailored to lab research, supporting the wider clinical research ecosystem. Additionally, the expansion of home-based care for patients with limited mobility or chronic illness is promoting broader use of urine collection products outside traditional clinical settings. This transition is contributing to an evolving product design landscape focused on portability, safety, and ease of use.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $8.4 Billion |

| CAGR | 6.5% |

The urine collection kits segment held a 69.4% share in 2024. This strong position is primarily due to the increasing reliance on at-home diagnostic kits, growth in decentralized clinical trials, and the rising importance of sterile and secure specimen handling. These kits offer convenience and accessibility to users outside of clinical facilities, helping improve diagnostic compliance and continuity of care. High adoption of urine collection kits is seen in applications like chronic disease monitoring, reproductive health, and drug testing.

The clinical urinalysis application segment generated USD 2.1 billion in 2024 and is projected to grow at a CAGR of 6.1% during 2025-2034. This segment leads the market because urine testing remains a frontline diagnostic tool in identifying a wide range of disorders, from UTIs and diabetes to kidney and metabolic conditions. Hospitals and diagnostic centers are the main end users, relying on chemically stable, contamination-resistant devices to maintain accurate laboratory results. The growing volume of regular health screenings and chronic condition diagnostics has solidified urinalysis as a cornerstone in preventative and acute care.

Europe Urine Collection Devices Market reached USD 1.3 billion in 2024. The region benefits from a highly developed healthcare infrastructure and widespread adoption of non-invasive testing methods. High per capita health expenditure and broad public screening programs are helping accelerate demand for urine testing in both hospitals and home-based settings. Countries in Western Europe and Scandinavia show particularly high usage due to increased focus on managing chronic urological conditions in elderly populations.

Major players operating in the Global Urine Collection Devices Market include BioTouch, QIAGEN, Ardo Medical, Thermo Fisher Scientific, Roche, Abbott, POLYMED, Aspen Surgical, Cardinal Health, HENSO, Convatec, Becton, Dickinson and Company, Labcorp (Litholink), MEDLINE, and ANGIPLAST. Companies competing in the urine collection devices market are leveraging product innovation, strategic partnerships, and global expansion to strengthen their foothold. A core focus lies in developing user-centric, sterile, and disposable kits that align with modern clinical and home care workflows. Many firms are investing in smart packaging solutions with tamper-evidence and sample-preservation features to meet evolving diagnostic standards. Collaborations with healthcare providers and laboratories are enabling co-development of purpose-driven products tailored to specific testing applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Patient trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic kidney diseases (CKD)

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Rising demand for non-invasive diagnostic tools

- 3.2.1.4 Technological advancements in urine collection devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of contamination and sample handling errors

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing use of urine-based liquid biopsy and genomic testing

- 3.2.3.2 Development of pediatric-friendly and smart urine collection devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Future market trends

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product type launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Urine collection kits

- 5.3 Urine specimen bags

- 5.4 Urine cups and containers

Chapter 6 Market Estimates and Forecast, By Patient, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Clinical urinalysis

- 7.2.1 Urinary tract infections (UTI)

- 7.2.2 Kidney disorders

- 7.2.3 Other clinical urinalysis

- 7.3 Drug screening

- 7.4 Pregnancy testing

- 7.5 Clinical research and studies

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Diagnostic laboratories

- 8.4 Home care settings

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott

- 10.2 ANGIPLAST

- 10.3 Ardo Medical

- 10.4 Aspen Surgical

- 10.5 Becton, Dickinson and Company

- 10.6 BioTouch

- 10.7 Cardinal Health

- 10.8 convatec

- 10.9 HENSO

- 10.10 Labcorp (Litholink)

- 10.11 MEDLINE

- 10.12 POLYMED

- 10.13 QIAGEN

- 10.14 Roche

- 10.15 Thermo Fisher Scientific

低成本尿袋市場報告:趨勢、預測和競爭分析(至2035年)

低成本尿袋市場報告:趨勢、預測和競爭分析(至2035年) 2026年全球尿液收集裝置市場報告2026年全球尿液檢查試紙市場報告

2026年全球尿液收集裝置市場報告2026年全球尿液檢查試紙市場報告 全球尿液檢查試紙市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球尿液檢查試紙市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 女性用泌尿輔助器具市場(依產品類型、材料、用途、可重複使用性、性別、通路和最終用戶分類),全球預測,2026-2032年床邊尿袋市場按產品類型、材質類型、最終用戶和分銷管道分類-2026-2032年全球預測尿液收集設備市場按產品類型、設計類型、材料、患者類型、最終用戶和分銷管道分類 - 2025-2030 年全球預測

女性用泌尿輔助器具市場(依產品類型、材料、用途、可重複使用性、性別、通路和最終用戶分類),全球預測,2026-2032年床邊尿袋市場按產品類型、材質類型、最終用戶和分銷管道分類-2026-2032年全球預測尿液收集設備市場按產品類型、設計類型、材料、患者類型、最終用戶和分銷管道分類 - 2025-2030 年全球預測 全球尿液收集裝置市場

全球尿液收集裝置市場 尿液檢查杯市場規模、佔有率、趨勢分析(按滅菌等級、產品、應用、最終用途、地區、細分市場預測),2025 年至 2030 年美國尿液檢查杯市場規模、佔有率、趨勢分析報告:按滅菌、產品、應用、最終用途、細分市場預測,2025-2030 年

尿液檢查杯市場規模、佔有率、趨勢分析(按滅菌等級、產品、應用、最終用途、地區、細分市場預測),2025 年至 2030 年美國尿液檢查杯市場規模、佔有率、趨勢分析報告:按滅菌、產品、應用、最終用途、細分市場預測,2025-2030 年