|

市場調查報告書

商品編碼

1797709

農業特種花卉種子市場機會、成長動力、產業趨勢分析及2025-2034年預測Agriculture Specialty Flower Seeds Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

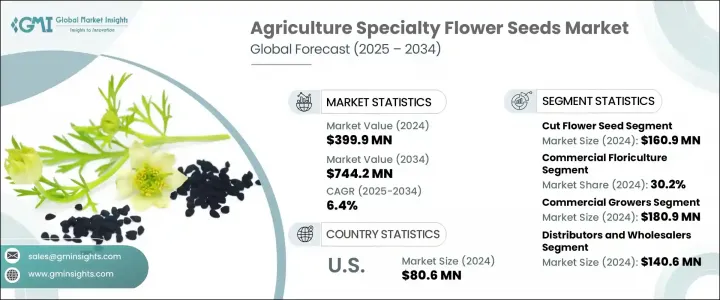

2024 年,全球農業特種花卉種子市場價值為 3.999 億美元,預計到 2034 年將以 6.4% 的複合年成長率成長,達到 7.442 億美元。受觀賞花卉和生態園林綠化需求日益成長的推動,該市場正在穩步發展。特種花卉種子通常稀有或外來,主要針對希望培育高價值花卉作物的商業種植者。這些種子是蓬勃發展的花卉產業的核心,該產業在全球僱用了 300 多萬名從業人員。除了美觀之外,該行業還透過促進生物多樣性和透過綠色城市空間增強永續性來支持生態目標。都市化進程的加速和消費者對環境效益的認知,正在推動這些種子成為主流的園林綠化和城市綠化應用。

此類植物對環境的貢獻包括淨化空氣、吸引傳粉昆蟲和改善土壤健康。抗病、快速發芽的雜交品種的開發以及其他種子品質的技術改進預計將推動未來的成長。人們對有機園藝和自然花卉美學的興趣日益濃厚,越來越多的消費者轉向無化學成分、環保的園藝方法,也推動了市場的上升趨勢。總體而言,持續的創新和環保意識的興起為持續擴張奠定了基調。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.999億美元 |

| 預測值 | 7.442億美元 |

| 複合年成長率 | 6.4% |

2024年,切花種子市場產值達1.609億美元,預計到2034年複合年成長率為6.6%。蓬勃發展的花卉市場對住宅和商業場所的新鮮花卉展示需求顯著成長,有力地支撐了這一成長。無論是用於活動裝飾或提升生活空間,消費者都更青睞鮮豔持久的花卉。種植者更青睞那些外觀出色、色彩豐富且瓶插壽命長的種子。這些偏好促使育種者不斷創新,推出極具特色的花卉品種,以滿足各通路的市場預期。

商業花卉種植領域在2024年佔據30.2%的市場佔有率,預計在2025-2034年期間的複合年成長率將達到6.7%。該領域受益於商業場所、零售企業和活動管理領域的花卉消費成長。注重抗逆性和低投入要求的雜交種子開發持續推動著花卉的商業化應用。此外,減少對化學農藥依賴的新品種正受到那些致力於獲得生態認證或有機認證的生產商的關注。同時,園林綠化領域對耐寒耐旱品種的興趣日益濃厚。那些維護成本低且能很好地適應當地土壤的花卉更受青睞,尤其是在公園和機構綠地等永續的戶外應用領域。

美國農業特種花卉種子市場佔81%的市場佔有率,2024年產值為8,060萬美元。美國的需求主要源自於城市景觀設計趨勢、消費者對本地本土花卉品種的關注以及對居住區生物多樣性的日益重視。隨著大眾對城市農業和保護性園藝的興趣日益濃厚,獨特且針對特定地點的花卉種子的需求也日益成長。這種區域性趨勢為專注於本地和氣候適應性植物品種的種子開發商帶來了廣泛的市場潛力。

影響全球農業特種花卉種子市場的關鍵參與者包括先正達股份公司、拜耳股份公司(作物科學部)、科迪華公司、巴斯夫股份公司(農業解決方案)、Dummen Orange、Kieft Seed BV 和 KWS SAAT SE & Co.。為了鞏固其在農業特種花卉種子市場的立足點,各大公司都在投資研發,以生產適應氣候、抗蟲害和高產量的雜交種子。他們透過開發需要更少化學投入和更少水消耗的品種來實現永續發展。與園藝機構和商業苗圃的合作有助於測試和微調新品種。各公司也正在擴大種子組合,以滿足特定區域的需求,並利用有機園藝和本地植物栽培等趨勢。他們正在利用策略聯盟、全球分銷網路和針對有環保意識的消費者的定向行銷活動來擴大影響力。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)

(註:僅提供重點國家的貿易統計數據

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021-2034

- 主要趨勢

- 切花種子

- 玫瑰種子

- 菊花種子

- 康乃馨種子

- 非洲菊種子

- 百合種子

- 鬱金香種子

- 葵花籽

- 其他切花種子

- 觀賞花卉種子

- 一年生花卉種子

- 萬壽菊種子

- 矮牽牛種子

- 百日菊種子

- 藿香薊種子

- 其他一年生種子

- 多年生花卉種子

- 飛燕草種子

- 羽扇豆種子

- 蜀葵種子

- 其他多年生種子

- 球根花卉種子

- 一年生花卉種子

- 食用花種子

- 旱金蓮種子

- 紫羅蘭種子

- 金盞花種子

- 薰衣草種子

- 其他食用花卉種子

- 特產和稀有品種

- 傳家寶品種

- 本地物種種子

- 野花混合物

- 對傳粉媒介友善的品種

第6章:市場估計與預測:按應用,2021-2034

- 主要趨勢

- 商業花卉栽培

- 切花生產

- 盆栽生產

- 溫室作業

- 現場生產

- 庭園綠化

- 商業景觀美化

- 公共花園和公園

- 住宅景觀美化

- 都市美化項目

- 家庭園藝

- 業餘園藝

- 容器園藝

- 室內園藝

- 社區花園

- 食品工業應用

- 餐廳和烹飪用途

- 食品加工業

- 飲料業

- 營養保健品應用

- 研究與教育

- 學術研究機構

- 植物園

- 農業推廣項目

- 育種計劃

第7章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 商業種植者

- 大型商業營運

- 中型種植戶

- 特色作物生產商

- 溫室操作員

- 零售苗圃和花園中心

- 獨立花園中心

- 連鎖苗圃

- 家居裝飾店

- 線上零售商

- 個人消費者

- 家庭園丁

- 業餘種植者

- 城市農民

- 教育機構

- 專業服務

- 景觀承包商

- 花店和花店

- 活動策劃者

- 農業顧問

第8章:市場估計與預測:按配銷通路,2021-2034 年

- 主要趨勢

- 直銷

- 製造商到種植者

- 合約銷售

- 從農場到消費者的銷售

- 分銷商和批發商

- 區域經銷商

- 專業種子經銷商

- 農業投入品經銷商

- 零售通路

- 花園中心和苗圃

- 農場用品商店

- 百貨公司

- 專業花店

- 線上平台

- 電子商務網站

- 網路市集

- 直接面對消費者的平台

- 訂閱服務

第9章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- Ball Horticultural Company

- BASF SE (Agricultural Solutions)

- Bayer AG (Crop Science Division)

- Botanical Interests, Inc.

- Corteva, Inc.

- Dummen Orange

- Eden Brothers

- Ferry-Morse Seed Company

- Floranova Ltd.

- Hem Genetics

- Kieft Seed BV

- KWS SAAT SE & Co. KGaA

- PanAmerican Seed

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Syngenta AG

- Vilmorin & Cie

The Global Agriculture Specialty Flower Seeds Market was valued at USD 399.9 million in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 744.2 million by 2034. This market is steadily evolving, driven by the increasing demand for ornamental blooms and eco-conscious landscaping practices. Specialty flower seeds, often rare or exotic, are primarily targeted at commercial growers looking to cultivate high-value floral crops. These seeds are central to a thriving flower industry that employs more than 3 million individuals worldwide. Beyond aesthetics, this sector supports ecological goals by fostering biodiversity and enhancing sustainability through green urban spaces. Increasing urbanization and consumer awareness of environmental benefits are pushing these seeds into mainstream landscaping and urban greening applications.

The environmental contributions of such plantings include air purification, pollinator attraction, and soil health improvements. The development of disease-resistant, fast-germinating hybrid varieties and other technological improvements in seed quality are expected to drive future growth. The market's upward trajectory is also propelled by a rising interest in organic gardening and natural floral aesthetics, with more consumers shifting toward chemical-free, eco-friendly gardening methods. Overall, continued innovation and a surge in environmentally aware practices are setting the tone for sustained expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $399.9 Million |

| Forecast Value | $744.2 Million |

| CAGR | 6.4% |

The cut flower seeds segment generated USD 160.9 million in 2024 at a CAGR of 6.6% through 2034. This increase is strongly supported by the flourishing floral market, with a clear rise in demand for fresh floral displays in both residential and commercial settings. Whether for decorative arrangements at events or for enhancing living spaces, consumers are opting for vibrant, long-lasting blooms. Growers are prioritizing seeds that deliver superior visual appeal, color richness, and extended vase life. These preferences are driving breeders to innovate and deliver highly distinctive flower types that meet market expectations across distribution channels.

The commercial floriculture segment held a 30.2% share in 2024 and is set to grow at a CAGR of 6.7% during 2025-2034. The segment is benefiting from increased flower consumption in commercial venues, retail businesses, and event management sectors. Hybrid seed development focusing on resilience and low input requirements continues to drive commercial adoption. Additionally, new varieties that reduce dependency on chemical pesticides are gaining attention among producers aiming for eco-certified or organic labels. Simultaneously, the landscaping and garden segment is seeing rising interest in hardy, drought-tolerant varieties. Flowers that require minimal maintenance and adapt well to native soil are preferred, especially for sustainable outdoor applications such as parks and institutional green spaces.

U.S. Agriculture Specialty Flower Seeds Market held 81% share generating USD 80.6 million in 2024. Demand in the U.S. is largely powered by urban landscaping trends, consumer focus on regionally native flower types, and a greater emphasis on biodiversity in residential areas. With increasing public interest in urban farming and conservation gardening, unique and location-specific flower seeds are seeing growing demand. This regional trend opens expansive market potential for seed developers focused on native and climate-resilient plant species.

Key players shaping the Global Agriculture Specialty Flower Seeds Market include Syngenta AG, Bayer AG (Crop Science Division), Corteva, Inc., BASF SE (Agricultural Solutions), Dummen Orange, Kieft Seed B.V., and KWS SAAT SE & Co. To solidify their foothold in the agriculture specialty flower seeds market, major companies are investing in R&D to produce climate-adaptive, pest-resistant, and higher-yielding hybrid seeds. They are targeting sustainability by developing varieties that thrive with fewer chemical inputs and lower water consumption. Collaborations with horticultural institutions and commercial nurseries help in testing and fine-tuning new breeds. Firms are also expanding seed portfolios to cater to region-specific demands and tapping into trends such as organic gardening and native plant cultivation. Strategic alliances, global distribution networks, and targeted marketing campaigns focused on eco-conscious consumers are being used to expand reach.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 End use

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trend

- 5.2 Cut flower seeds

- 5.2.1 Rose seeds

- 5.2.2 Chrysanthemum seeds

- 5.2.3 Carnation seeds

- 5.2.4 Gerbera seeds

- 5.2.5 Lily seeds

- 5.2.6 Tulip seeds

- 5.2.7 Sunflower seeds

- 5.2.8 Other cut flower seeds

- 5.3 Ornamental flower seeds

- 5.3.1 Annual flower seeds

- 5.3.1.1 Marigold seeds

- 5.3.1.2 Petunia seeds

- 5.3.1.3 Zinnia seeds

- 5.3.1.4 Ageratum seeds

- 5.3.1.5 Other annual seeds

- 5.3.2 Perennial flower seeds

- 5.3.2.1 Delphinium seeds

- 5.3.2.2 Lupine seeds

- 5.3.2.3 Hollyhock seeds

- 5.3.2.4 Other perennial seeds

- 5.3.3 Bulb flower seeds

- 5.3.1 Annual flower seeds

- 5.4 Edible flower seeds

- 5.4.1 Nasturtium seeds

- 5.4.2 Viola seeds

- 5.4.3 Calendula seeds

- 5.4.4 Lavender seeds

- 5.4.5 Other edible flower seeds

- 5.5 Specialty and rare varieties

- 5.5.1 Heirloom varieties

- 5.5.2 Native species seeds

- 5.5.3 Wildflower mixes

- 5.5.4 Pollinator-friendly varieties

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Commercial floriculture

- 6.2.1 Cut flower production

- 6.2.2 Potted plant production

- 6.2.3 Greenhouse operations

- 6.2.4 Field production

- 6.3 Landscaping and gardening

- 6.3.1 Commercial landscaping

- 6.3.2 Public gardens and parks

- 6.3.3 Residential landscaping

- 6.3.4 Urban beautification projects

- 6.4 Home gardening

- 6.4.1 Hobby gardening

- 6.4.2 Container gardening

- 6.4.3 Indoor gardening

- 6.4.4 Community gardens

- 6.5 Food industry applications

- 6.5.1 Restaurant and culinary use

- 6.5.2 Food processing industry

- 6.5.3 Beverage industry

- 6.5.4 Nutraceutical applications

- 6.6 Research and education

- 6.6.1 Academic research institutions

- 6.6.2 Botanical gardens

- 6.6.3 Agricultural extension programs

- 6.6.4 Breeding programs

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Tons)

- 7.1 Key trend

- 7.2 Commercial growers

- 7.2.1 Large-scale commercial operations

- 7.2.2 Medium-scale growers

- 7.2.3 Specialty crop producers

- 7.2.4 Greenhouse operators

- 7.3 Retail nurseries and garden centers

- 7.3.1 Independent garden centers

- 7.3.2 Chain nurseries

- 7.3.3 Home improvement stores

- 7.3.4 Online retailers

- 7.4 Individual consumers

- 7.4.1 Home gardeners

- 7.4.2 Hobby growers

- 7.4.3 Urban farmers

- 7.4.4 Educational institutions

- 7.5 Professional services

- 7.5.1 Landscape contractors

- 7.5.2 Florists and flower shops

- 7.5.3 Event planners

- 7.5.4 Agricultural consultants

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 Direct sales

- 8.2.1 Manufacturer to grower

- 8.2.2 Contract sales

- 8.2.3 Farm-to-consumer sales

- 8.3 Distributors and wholesalers

- 8.3.1 Regional distributors

- 8.3.2 Specialty seed distributors

- 8.3.3 Agricultural input dealers

- 8.4 Retail channels

- 8.4.1 Garden centers and nurseries

- 8.4.2 Farm supply stores

- 8.4.3 Department stores

- 8.4.4 Specialty flower shops

- 8.5 Online platforms

- 8.5.1 E-commerce websites

- 8.5.2 Online marketplaces

- 8.5.3 Direct-to-consumer platforms

- 8.5.4 Subscription services

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Ball Horticultural Company

- 10.2 BASF SE (Agricultural Solutions)

- 10.3 Bayer AG (Crop Science Division)

- 10.4 Botanical Interests, Inc.

- 10.5 Corteva, Inc.

- 10.6 Dummen Orange

- 10.7 Eden Brothers

- 10.8 Ferry-Morse Seed Company

- 10.9 Floranova Ltd.

- 10.10 Hem Genetics

- 10.11 Kieft Seed B.V.

- 10.12 KWS SAAT SE & Co. KGaA

- 10.13 PanAmerican Seed

- 10.14 Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- 10.15 Syngenta AG

- 10.16 Vilmorin & Cie