|

市場調查報告書

商品編碼

1797687

地板化學品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Flooring Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

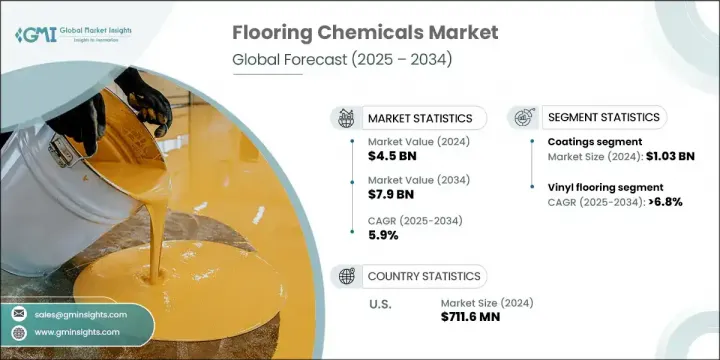

2024年,全球地板化學品市場規模達45億美元,預計2034年將以5.9%的複合年成長率成長,達到79億美元。由於市場轉向環保材料和低排放化學配方,該市場正在快速發展。隨著永續性成為核心關注點,製造商正在開發先進的地板解決方案,降低揮發性有機化合物(VOC)含量並增加生物基含量,以滿足環境法規和不斷變化的消費者期望。智慧製造技術和數位化工具正在整合到生產中,以確保更高的流程效率、品質控制和對需求的回應能力。

數位化的不斷發展使得即時監控、供應鏈協調和精準定位客戶需求成為可能。對高性能、耐用且永續的地板材料的追求,正推動住宅、商業和工業建築領域的廣泛需求。樹脂、塗料和黏合劑等地板化學物質對於提升地板的美觀度、耐磨性以及在不同環境負荷下的功能性至關重要。市場受益於強勁的創新和對兼具高彈性、易於維護和環境影響極小的地板系統的快速普及,進一步鞏固了其在已開發地區和新興地區的全球擴張。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 45億美元 |

| 預測值 | 79億美元 |

| 複合年成長率 | 5.9% |

塗料產業在2024年創造了10.3億美元的市場規模,預計到2034年將繼續以7.2%的複合年成長率成長。塗料、黏合劑和密封劑對於多種材料(包括木材、瓷磚、複合地板和乙烯基)的地板安裝和保護仍然至關重要。隨著人們對排放的認知不斷提高,企業正在創新低VOC和快速固化的黏合劑配方,從而推動住宅和商業建築的需求。水性和生物基黏合劑的產品進步因其對環境的影響最小以及對各種地板類型的適應性而備受青睞。

預計2025年至2034年期間,乙烯基地板市場的複合年成長率將達到6.8%。這種地板解決方案因其多功能性和高回彈性而發展勢頭強勁,而背襯、粘合劑和表面塗層方面的化學創新則提升了其在潮濕和人流量大區域的性能。其他熱門地板類型,例如地毯,在抗菌處理和低排放材料方面也取得了進展,以符合綠色建築標準和公共衛生期望。

美國地板化學品市場佔80%的市場佔有率,2024年市場規模達7.116億美元。由於強勁的房屋建設、翻新趨勢以及對高性能地板系統的需求,美國地板化學品產業蓬勃發展。由於氣候條件多樣,且各地區建築規範各不相同,塗料、底漆和黏合劑的創新著重於氣候適應型和結構專用型解決方案。這使得美國成為地板化學品技術創新的重要樞紐。

全球地板化學品市場的領導公司包括西卡股份公司、巴斯夫股份公司、陶氏化學公司、漢高股份公司和 3M 公司。地板化學品市場的主要參與者正在投資研發,以開發具有更低 VOC 排放和更高耐用性的先進配方。他們正在轉向更綠色的化學品,以遵守不斷變化的法規並滿足消費者對永續產品日益成長的需求。正在與地板材料製造商和建築公司建立策略合作夥伴關係,以創建針對不同安裝需求的整合解決方案。公司正在透過在高成長地區開設新的製造工廠和加強分銷網路來擴大其全球影響力。包括即時分析和智慧物流在內的數位轉型正在提高營運效率。現在的行銷策略主要集中在環保地板化學品的環境和健康效益,以吸引商業買家和有環保意識的消費者的注意。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 黏合劑

- 水性黏合劑

- 溶劑型黏合劑

- 聚氨酯基/濕氣固化黏合劑

- 粉末黏合劑

- 熱熔膠

- 密封劑

- 矽酮密封膠

- 聚氨酯密封膠

- 丙烯酸密封膠

- 丁基密封膠

- 塗料

- 環氧塗料

- 聚氨酯塗料

- 聚天門冬胺酸塗料

- 丙烯酸塗料

- 抗菌塗層

- 底漆和表面處理

- 環氧底漆

- 丙烯酸底漆

- 聚氨酯底漆

- 表面處理化學品

- 底層和平滑化合物

- 自流平化合物

- 防潮層

- 隔音墊層

- 地板飾面和拋光劑

- 水性塗料

- 溶劑型塗飾劑

- 紫外線固化塗層

- 保養拋光劑

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 硬木地板

- 強化木地板

- 乙烯基地板

- 地毯地板

- 磁磚和石材地板

- 混凝土地板

- 其他地板類型

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 住宅

- 獨棟住宅

- 多戶住宅

- 翻新和改造

- 商業的

- 辦公大樓

- 零售空間

- 飯店業

- 醫療保健設施

- 教育機構

- 工業的

- 生產設施

- 倉庫和配送中心

- 食品加工廠

- 製藥設施

- 化學加工廠

第8章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 常規化學系統

- 傳統環氧體系

- 標準聚氨酯配方

- 常規丙烯酸體系

- 先進化學技術

- 奈米科技增強配方

- 智慧功能塗料

- 自修復材料

- 抗菌技術

- 永續和生物基系統

- 生物基聚氨酯

- 植物性黏合劑

- 再生材料配方

- 低VOC和零VOC系統

- 專業和高性能系統

- 耐化學腐蝕配方

- 耐高溫系統

- 防靜電和導電系統

- 裝飾和美學系統

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 菲律賓

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 埃及

第10章:公司簡介

- BASF SE

- Sika AG

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- 3M Company

- Sherwin-Williams Company

- Mapei SpA

- HB Fuller Company

- RPM International Inc.

- Arkema Group

The Global Flooring Chemicals Market was valued at USD 4.5 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 7.9 billion by 2034. The market is rapidly evolving due to a shift toward eco-friendly materials and low-emission chemical formulations. As sustainability becomes a core focus, manufacturers are developing advanced flooring solutions with reduced VOC levels and increased bio-based content to meet both environmental regulations and changing consumer expectations. Smart manufacturing techniques and digital tools are being integrated into production to ensure greater process efficiency, quality control, and responsiveness to demand.

Increasing digitalization is enabling real-time monitoring, improved supply chain coordination, and precise targeting of customer needs. The push for high-performance, durable, and sustainable flooring materials is fueling widespread demand across residential, commercial, and industrial construction. Flooring chemicals such as resins, coatings, and adhesives are central to improving floor aesthetics, wear resistance, and functionality under varying environmental loads. The market is benefiting from strong innovation and rapid adoption of flooring systems that combine resilience, easy maintenance, and minimal environmental impact, further reinforcing its global expansion across developed and emerging regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.5 Billion |

| Forecast Value | $7.9 Billion |

| CAGR | 5.9% |

The coatings segment generated USD 1.03 billion in 2024 and is expected to continue growing at 7.2% CAGR through 2034. Coatings, adhesives, and sealants remain critical to floor installation and protection across multiple materials including wood, tile, laminate, and vinyl. With rising awareness around emissions, companies are innovating low-VOC and fast-curing adhesive formulations, boosting demand across both residential and commercial construction. Product advancements in water-based and bio-based adhesives have gained traction for their minimal environmental footprint and adaptability across diverse flooring types.

The vinyl flooring segment is expected to grow at a CAGR of 6.8% from 2025 to 2034. This flooring solution is gaining momentum due to its versatility and resilience, enhanced by chemical innovations in backings, adhesives, and surface coatings that boost performance in moisture-prone and high-traffic areas. Other popular flooring types, like carpet, are seeing advancements in antimicrobial treatments and low-emission materials to align with green building standards and public health expectations.

United States Flooring Chemicals Market held 80% share and generated USD 711.6 million in 2024. The U.S. flooring chemicals sector is thriving on the back of strong housing construction, renovation trends, and demand for performance-based flooring systems. With its diverse climate and varying construction codes across regions, innovation in coatings, primers, and adhesives is focused on climate-resilient and structure-specific solutions. This has positioned the U.S. as a key hub for innovation in flooring chemical technologies.

Leading companies in the Global Flooring Chemicals Market include Sika AG, BASF SE, The Dow Chemical Company, Henkel AG & Co. KGaA, and 3M Company. Major players in the flooring chemicals market are investing in R&D to develop advanced formulations with lower VOC emissions and improved durability. They are shifting toward greener chemistries to comply with evolving regulations and to meet rising consumer demand for sustainable products. Strategic partnerships with flooring material manufacturers and construction firms are being formed to create integrated solutions tailored to diverse installation needs. Companies are expanding their global footprints by opening new manufacturing facilities in high-growth regions and strengthening distribution networks. Digital transformation, including real-time analytics and smart logistics, is enhancing operational efficiency. Marketing strategies now focus heavily on the environmental and health benefits of eco-conscious flooring chemicals to capture the attention of both commercial buyers and environmentally aware consumers.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Applications

- 2.2.4 End use

- 2.2.5 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 ($Bn, Kilo tons)

- 5.1 Key trends

- 5.2 Adhesives

- 5.2.1 Water-based adhesives

- 5.2.2 Solvent-based adhesives

- 5.2.3 Urethane-based/moisture-cure adhesives

- 5.2.4 Powder adhesives

- 5.2.5 Hot-melt adhesives

- 5.3 Sealants

- 5.3.1 Silicone sealants

- 5.3.2 Polyurethane sealants

- 5.3.3 Acrylic sealants

- 5.3.4 Butyl sealants

- 5.4 Coatings

- 5.4.1 Epoxy coatings

- 5.4.2 Polyurethane coatings

- 5.4.3 Polyaspartic coatings

- 5.4.4 Acrylic coatings

- 5.4.5 Antimicrobial coatings

- 5.5 Primers and surface preparation

- 5.5.1 Epoxy primers

- 5.5.2 Acrylic primers

- 5.5.3 Polyurethane primers

- 5.5.4 Surface preparation chemicals

- 5.6 Underlayments and smoothing compounds

- 5.6.1 Self-leveling compounds

- 5.6.2 Moisture barriers

- 5.6.3 Sound dampening underlayments

- 5.7 Floor finishes and polishes

- 5.7.1 Water-based finishes

- 5.7.2 Solvent-based finishes

- 5.7.3 UV-cured finishes

- 5.7.4 Maintenance polishes

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Kilo tons)

- 6.1 Key trends

- 6.2 Hardwood flooring

- 6.3 Laminate flooring

- 6.4 Vinyl flooring

- 6.5 Carpet flooring

- 6.6 Tile and stone flooring

- 6.7 Concrete flooring

- 6.8 Other flooring types

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Kilo tons)

- 7.1 Key trends

- 7.2 Residential

- 7.2.1 Single-family homes

- 7.2.2 Multi-family residential

- 7.2.3 Renovation and remodeling

- 7.3 Commercial

- 7.3.1 Office buildings

- 7.3.2 Retail spaces

- 7.3.3 Hospitality

- 7.3.4 Healthcare facilities

- 7.3.5 Educational institutions

- 7.4 Industrial

- 7.4.1 Manufacturing facilities

- 7.4.2 Warehouses and distribution centers

- 7.4.3 Food processing plants

- 7.4.4 Pharmaceutical facilities

- 7.4.5 Chemical processing plants

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Kilo tons)

- 8.1 Key trends

- 8.2 Conventional chemical systems

- 8.2.1 Traditional epoxy systems

- 8.2.2 Standard polyurethane formulations

- 8.2.3 Conventional acrylic systems

- 8.3 Advanced chemical technologies

- 8.3.1 Nanotechnology-enhanced formulations

- 8.3.2 Smart and functional coatings

- 8.3.3 Self-healing materials

- 8.3.4 Antimicrobial technologies

- 8.4 Sustainable and bio-based systems

- 8.4.1 Bio-based polyurethanes

- 8.4.2 Plant-based adhesives

- 8.4.3 Recycled content formulations

- 8.4.4 Low-voc and zero-voc systems

- 8.5 Specialty and high-performance systems

- 8.5.1 Chemical-resistant formulations

- 8.5.2 High-temperature resistant systems

- 8.5.3 Anti-static and conductive systems

- 8.5.4 Decorative and aesthetic systems

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Kilo tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Italy

- 9.3.4 Spain

- 9.3.5 Russia

- 9.3.6 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Philippines

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Egypt

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Sika AG

- 10.3 Henkel AG & Co. KGaA

- 10.4 The Dow Chemical Company

- 10.5 3M Company

- 10.6 Sherwin-Williams Company

- 10.7 Mapei S.p.A.

- 10.8 H.B. Fuller Company

- 10.9 RPM International Inc.

- 10.10 Arkema Group

工業地坪塗料市場:依樹脂類型、應用類型、基材類型及最終用戶分類-2026-2032年全球市場預測地板塗料市場:2026-2032年全球市場預測(依樹脂類型、類別、應用方法及用途分類)

工業地坪塗料市場:依樹脂類型、應用類型、基材類型及最終用戶分類-2026-2032年全球市場預測地板塗料市場:2026-2032年全球市場預測(依樹脂類型、類別、應用方法及用途分類) 地板塗料市場規模、佔有率和趨勢分析報告:按產品、成分、應用、最終用途、地區和細分市場預測(2026-2033 年)

地板塗料市場規模、佔有率和趨勢分析報告:按產品、成分、應用、最終用途、地區和細分市場預測(2026-2033 年) 全球工業地坪塗料市場規模、佔有率、趨勢及成長分析報告:2026-2034年

全球工業地坪塗料市場規模、佔有率、趨勢及成長分析報告:2026-2034年 2026年全球工業地板塗料市場報告

2026年全球工業地板塗料市場報告 工業地坪塗料市場規模、佔有率及成長分析(按類型、成分、地板材料、應用及地區分類)-2026-2033年產業預測

工業地坪塗料市場規模、佔有率及成長分析(按類型、成分、地板材料、應用及地區分類)-2026-2033年產業預測 地板塗料市場規模、佔有率和成長分析(按黏合劑類型、塗料成分、地板結構、配方、最終用戶和地區分類)—2026-2033年產業預測

地板塗料市場規模、佔有率和成長分析(按黏合劑類型、塗料成分、地板結構、配方、最終用戶和地區分類)—2026-2033年產業預測 工業地坪塗料市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

工業地坪塗料市場機會、成長要素、產業趨勢分析及預測(2026年至2035年) 地板配件:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

地板配件:全球市場佔有率和排名、總收入和需求預測(2025-2031年) 地板配件市場按產品類型、材料、最終用戶、分銷管道和地區分類

地板配件市場按產品類型、材料、最終用戶、分銷管道和地區分類