|

市場調查報告書

商品編碼

1782156

腸道疾病檢測市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Enteric Disease Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

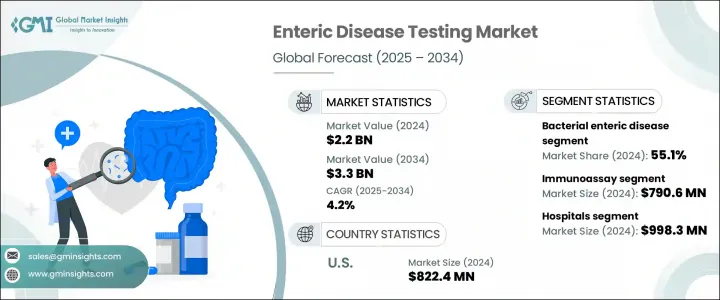

2024年,全球腸道疾病檢測市場規模達22億美元,預計2034年將以4.2%的複合年成長率成長,達到33億美元。這一成長主要源於腸道感染盛行率的上升、公眾意識的提升、監測措施的推進以及診斷檢測技術的進步。腸道疾病多發於中低收入國家,通常與衛生條件不佳和水污染有關。這些感染具有復發性和地方性持續性,因此及時、準確的診斷至關重要。早期發現對於促進有效干預、改善患者預後和支持更有效的疾病控制至關重要。

此外,膠囊內視鏡、可攝取感測器和藥物傳輸系統需求的成長,也刺激了對腸道器械進行精準檢測的需求。這包括評估溶解度、轉運時間和胃腸道結構內的局部釋放等因素,進一步推動了市場擴張。腸道疾病檢測是指用於識別影響消化道的細菌、病毒或寄生蟲引起的感染的診斷方法。這些檢測可用於檢測腹瀉、霍亂、傷寒和痢疾等疾病。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 22億美元 |

| 預測值 | 33億美元 |

| 複合年成長率 | 4.2% |

免疫測定領域佔據市場主導地位,2024年市場規模達7.906億美元,預計2034年複合年成長率將達4.3%。免疫測定廣泛用於檢測腸道病原體,尤其在資源匱乏的環境中(包括即時診斷環境)普遍使用。免疫測定是監測和應對疫情的主要方法,特別適用於細菌毒素和輪狀病毒、諾羅病毒等病毒感染。

2024年,醫院領域以9.983億美元的收入引領市場,預計2025-2034年期間的複合年成長率將達到4.4%。作為急診和緊急干預的主要中心,醫院處理著許多嚴重的胃腸道病例,尤其是與食源性疾病相關的病例。大多數緊急病例在醫院實驗室處理,這反映了這些機構在腸道疾病檢測中的關鍵作用。

2024年,美國腸道疾病檢測市場規模達8.224億美元。美國每年發生數百萬例食源性疾病病例,主要由沙門氏菌、大腸桿菌和諾羅病毒等病原體引起。應對這項公共衛生挑戰需要定期進行準確的腸道疾病檢測。美國疾病管制與預防中心(CDC)和美國食品藥物管理局(FDA)等機構的項目,例如FoodNet和PulseNet,在疫情檢測和先進診斷檢測方法的開發中發揮著至關重要的作用。這些機構推動著提高診斷速度和準確性所需的創新。

腸道疾病檢測市場的主要參與者包括雅培實驗室、碧迪公司、Biomerica、bioMerieux、Bio-Rad Laboratories、Coris BioConcept、丹納赫、DiaSorin、默克公司、Meridian Bioscience、Techlab 和賽默飛世爾科技。為了鞏固其在腸道疾病檢測市場的地位,各公司正專注於持續創新和開發先進的診斷技術。這包括大力投資研發 (R&D),以提高檢測試劑盒的準確性、速度和易用性,特別是對於即時診斷環境。與政府機構、研究機構和醫療保健提供者的策略合作也是擴大其市場影響力的關鍵。各公司也透過提供價格合理、易於使用的診斷解決方案,擴大其在腸道疾病高發新興市場的影響力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 腸道疾病盛行率不斷上升

- 診斷技術的進步

- 預防性醫療保健服務需求不斷成長

- 醫療支出和投資不斷增加

- 產業陷阱與挑戰

- 腸道疾病檢測成本高昂

- 測試程序的複雜性

- 成長動力

- 成長潛力分析

- 監管格局

- 美國

- 歐洲

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按疾病,2021 - 2034 年

- 主要趨勢

- 細菌性腸道疾病

- 沙門氏菌

- 大腸桿菌

- 彎曲桿菌

- 艱難梭菌

- 志賀氏菌症

- 李斯特菌

- 病毒性腸疾病

- 輪狀病毒感染

- 諾羅病毒感染

- 腸道寄生蟲病

- 賈第鞭毛蟲病

- 阿米巴病

- 隱孢子蟲病

第6章:市場估計與預測:按測試類型,2021 - 2034 年

- 主要趨勢

- 免疫測定

- 分子

- 傳統的

- 色譜法和光譜法

- 其他測試類型

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 診斷實驗室

- 研究與學術機構

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Abbott Laboratories

- Becton, Dickinson and Company

- Biomerica

- bioMerieux

- Bio-Rad Laboratories

- Coris BioConcept

- Danaher

- DiaSorin

- Merck KGaA

- Meridian Bioscience

- Techlab

- Thermo Fisher Scientific

The Global Enteric Disease Testing Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 3.3 billion by 2034. This growth is driven by the increasing prevalence of enteric infections, greater awareness, surveillance initiatives, and technological advancements in diagnostic testing. Enteric diseases, often occurring in low- and middle-income countries, are commonly linked to inadequate sanitation and contaminated water. These infections are recurrent, with endemic persistence, highlighting the need for timely, accurate diagnostics. Early detection is crucial in facilitating effective interventions that improve patient outcomes and support better disease control efforts.

Additionally, the rise in demand for capsule endoscopy, ingestible sensors, and drug delivery systems has spurred the need for accurate testing of enteric devices. This includes evaluating factors like dissolution, transit time, and localized release within gastrointestinal structures, further driving market expansion. Enteric disease testing refers to diagnostic methods used to identify infections caused by bacteria, viruses, or parasites that affect the digestive tract. Tests are used to detect conditions like diarrhea, cholera, typhoid, and dysentery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 4.2% |

The immunoassay segment dominated the market, generating USD 790.6 million in 2024, and is projected to grow at a CAGR of 4.3% through 2034. Immunoassays are widely used for detecting enteric pathogens and are particularly prevalent in low-resource settings, including point-of-care environments. They are the primary method for surveillance and outbreak response, especially for bacterial toxins and viral infections like rotavirus and norovirus.

The hospitals segment led the market in 2024 with a revenue of USD 998.3 million and is expected to grow at a CAGR of 4.4% during 2025-2034. As major centers for acute care and emergency interventions, hospitals handle many severe gastrointestinal cases, especially those related to foodborne diseases. Most urgent cases are processed in hospital-based labs, reflecting the crucial role of these institutions in enteric disease testing.

U.S. Enteric Disease Testing Market was valued at USD 822.4 million in 2024. The country sees millions of foodborne illness cases annually, driven by pathogens like Salmonella, E. coli, and Norovirus. Addressing this public health challenge requires regular, accurate enteric disease testing. Programs from organizations like the CDC and FDA, such as FoodNet and PulseNet, play a vital role in outbreak detection and the development of advanced diagnostic tests. These agencies drive the innovation necessary to improve diagnostic speed and accuracy.

Key players in the Enteric Disease Testing Market include Abbott Laboratories, Becton, Dickinson and Company, Biomerica, bioMerieux, Bio-Rad Laboratories, Coris BioConcept, Danaher, DiaSorin, Merck KGaA, Meridian Bioscience, Techlab, and Thermo Fisher Scientific. To strengthen their position in the enteric disease testing market, companies are focusing on continuous innovation and the development of advanced diagnostic technologies. This includes investing heavily in research and development (R&D) to improve the accuracy, speed, and ease of use of testing kits, particularly for point-of-care settings. Strategic collaborations with government agencies, research institutions, and healthcare providers are also key to expanding their market footprint. Companies are also increasing their presence in emerging markets where the incidence of enteric diseases is high by providing affordable, easy-to-use diagnostic solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Disease trends

- 2.2.3 Test type trends

- 2.2.4 End use trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of enteric diseases

- 3.2.1.2 Technological advancements in diagnostic technologies

- 3.2.1.3 Growing demand for preventive healthcare services

- 3.2.1.4 Rising healthcare expenditure and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with enteric disease testing

- 3.2.2.2 Complexity of testing procedures

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Bacterial enteric disease

- 5.2.1 Salmonella

- 5.2.2 E. coli

- 5.2.3 Campylobacter

- 5.2.4 C. difficile

- 5.2.5 Shigellosis

- 5.2.6 Listeria

- 5.3 Viral enteric disease

- 5.3.1 Rotavirus infection

- 5.3.2 Norovirus infection

- 5.4 Parasitic enteric disease

- 5.4.1 Giardiasis

- 5.4.2 Amebiasis

- 5.4.3 Cryptosporidiosis

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Immunoassay

- 6.3 Molecular

- 6.4 Conventional

- 6.5 Chromatography & spectrometry

- 6.6 Other test types

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Diagnostic laboratories

- 7.4 Research & academic institutes

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Becton, Dickinson and Company

- 9.3 Biomerica

- 9.4 bioMerieux

- 9.5 Bio-Rad Laboratories

- 9.6 Coris BioConcept

- 9.7 Danaher

- 9.8 DiaSorin

- 9.9 Merck KGaA

- 9.10 Meridian Bioscience

- 9.11 Techlab

- 9.12 Thermo Fisher Scientific

腸道疾病檢測市場:2026-2032年全球市場預測(依檢測方法、產品類型、病原體、檢體類型、最終用戶和通路分類)

腸道疾病檢測市場:2026-2032年全球市場預測(依檢測方法、產品類型、病原體、檢體類型、最終用戶和通路分類) 腸道疾病檢測市場分析及預測(至2035年):依類型、產品、服務、技術、應用、最終使用者、流程、功能及安裝類型分類

腸道疾病檢測市場分析及預測(至2035年):依類型、產品、服務、技術、應用、最終使用者、流程、功能及安裝類型分類 腸道疾病檢測市場-全球產業規模、佔有率、趨勢、機會和預測,依疾病類型、最終用戶、地區和競爭格局分類,2020-2030年預測

腸道疾病檢測市場-全球產業規模、佔有率、趨勢、機會和預測,依疾病類型、最終用戶、地區和競爭格局分類,2020-2030年預測 2025年全球腸道疾病檢測市場報告

2025年全球腸道疾病檢測市場報告 腸道疾病檢測市場規模、佔有率、趨勢及預測(按產品類型、技術、疾病類型、最終用戶和地區),2025 年至 2033 年

腸道疾病檢測市場規模、佔有率、趨勢及預測(按產品類型、技術、疾病類型、最終用戶和地區),2025 年至 2033 年 全球腸道疾病檢測市場:市場規模、佔有率、趨勢分析(按疾病和地區)、細分市場預測(2025-2030 年)

全球腸道疾病檢測市場:市場規模、佔有率、趨勢分析(按疾病和地區)、細分市場預測(2025-2030 年)