|

市場調查報告書

商品編碼

1782109

輸尿管鏡市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Ureteroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

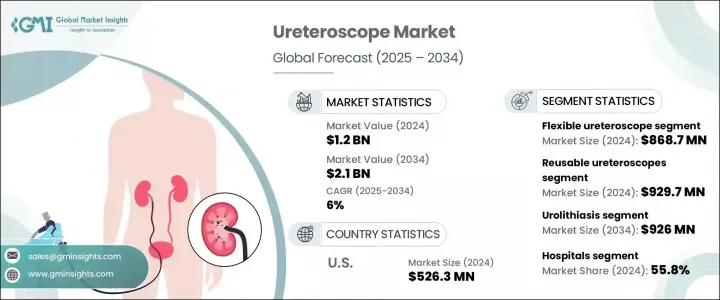

2024 年全球輸尿管鏡市場規模達 12 億美元,預計到 2034 年將以 6% 的複合年成長率成長至 21 億美元。這一成長軌跡主要受全球腎結石和其他泌尿道相關疾病發生率上升的驅動。此外,由於臨床療效改善、術後併發症減少以及住院時間縮短,採用微創技術的醫療保健趨勢持續增強。這些優點促使醫護人員和患者更傾向於選擇內視鏡介入而非傳統手術。輸尿管鏡——用於診斷和治療輸尿管及腎臟疾病的設備——隨著其設計不斷改進,靈活性和影像技術不斷提升,其重要性日益凸顯。這些創新技術能夠實現更精準的治療,提高患者的舒適度和安全性,從而支持其在全球醫療保健系統中的廣泛應用。

泌尿道感染和腎結石的增多,可歸因於現代生活習慣、肥胖率上升、遺傳因素以及某些人群的體液攝取不足等多種因素。隨著這些健康問題日益普遍,醫學界正將輸尿管鏡視為一種有效且微創的解決方案。輸尿管鏡旨在解決各種泌尿系統問題,例如狹窄、腫瘤和結石。它們配備先進的可視化和可操作性,可對整個泌尿道進行全面診斷和微創治療。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 12億美元 |

| 預測值 | 21億美元 |

| 複合年成長率 | 6% |

2024年,軟性輸尿管鏡市場價值達8.687億美元。其適應性強,易於在複雜的泌尿道中導航,使其成為診斷和處理複雜泌尿外科病例的理想選擇。材料和視覺化技術的進步進一步提升了這些設備的性能,使其在臨床上廣泛應用。隨著泌尿科醫師尋求能夠進行更安全、更有效率手術的精密器械,對軟性輸尿管鏡的需求日益成長。

在臨床應用方面,泌尿系統結石領域在2024年佔據了最高的市場佔有率,預計到2034年將達到9.26億美元。泌尿系統結石影響著廣泛的人群,如果不及時治療,可能會導致嚴重的併發症。輸尿管鏡的精準性和高效性使其成為治療此類疾病的重要工具,尤其是在需要透過微創手術取出或碎石的情況下。

由於強大的醫療基礎設施和對泌尿系統疾病的高度認知,美國輸尿管鏡市場在2024年的價值達到5.263億美元。先進的醫療技術,加上龐大的腎結石和泌尿道疾病患者群體,推動了持續的需求。此外,頂級醫療器材製造商的湧現以及新型成像工具的快速普及,鞏固了美國在該領域的領先地位。

輸尿管鏡市場競爭格局中的關鍵參與者包括波士頓科學 (Boston Scientific)、史托斯 (STORZ)、安布 (Ambu)、普森 (PUSEN)、康樂保 (Coloplast)、BD、史賽克 (Stryker)、多尼爾醫療科技 (Dornier MedTech)、Neoscope、奧運、歐普夫醫療 (Dornier MedTech) 和理查康歐普夫 (EULF)。為了鞏固市場地位,輸尿管鏡產業的公司正在大力投資創新,專注於提高設備的靈活性、小型化和光學清晰度。他們正積極透過策略合作夥伴關係和量身定做的產品發布來擴展產品組合,以滿足已開發和新興醫療市場的需求。一次性和電子輸尿管鏡技術的持續改進也是一個重點關注領域。此外,各公司正在加強其全球分銷網路,並參與培訓項目以支持臨床應用,從而確保長期競爭力和持續的市場成長。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 腎結石和泌尿道疾病的盛行率不斷上升

- 輸尿管鏡技術的進步

- 微創設備的採用日益增多

- 產業陷阱與挑戰

- 先進電子輸尿管鏡成本高昂

- 機會

- 向新興市場擴張

- 輸尿管鏡與機器人手術系統的整合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 按產品分類的價格趨勢

- 未來市場趨勢

- 報銷場景

- 消費者行為分析

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 軟性輸尿管鏡

- 硬性輸尿管鏡

第6章:市場估計與預測:按可用性,2021 - 2034 年

- 主要趨勢

- 可重複使用的輸尿管鏡

- 拋棄式輸尿管鏡

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 泌尿系統結石

- 尿道狹窄

- 泌尿道感染

- 其他應用

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Ambu

- BD

- Boston Scientific

- Coloplast

- Dornier MedTech

- neoscope

- OLYMPUS

- OPCOM Medical

- PUSEN

- RICHARD WOLF

- STORZ

- Stryker

The Global Ureteroscope Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 2.1 billion by 2034. This growth trajectory is primarily being driven by the rising global incidence of kidney stones and other urinary tract-related conditions. Alongside this, the broader healthcare trend of adopting minimally invasive technologies continues to gain pace, fueled by better clinical outcomes, reduced post-operative complications, and shorter hospital stays. These advantages are pushing both healthcare providers and patients to prefer endoscopic interventions over traditional surgery. Ureteroscopes-devices designed to diagnose and treat ureteral and renal conditions-have become increasingly important as their designs evolve to offer improved flexibility and advanced imaging. These innovations allow for more precise treatments with greater patient comfort and enhanced safety, supporting their growing adoption across healthcare systems worldwide.

The increase in urinary tract infections and renal calculi can be attributed to a mix of modern lifestyle habits, rising obesity rates, genetic influences, and poor hydration in certain populations. As these health issues become more common, the medical community is turning to ureteroscopy as an effective and less invasive solution. These scopes are engineered to address a wide range of urological concerns such as strictures, tumors, and calculi. Equipped with cutting-edge visualization and maneuverability, they enable thorough diagnosis and minimally invasive treatment across the urinary tract.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 6% |

The flexible ureteroscopes segment was valued at USD 868.7 million in 2024. Their adaptability and ease of navigation through the intricate urinary pathways make them ideal for diagnosing and managing complex urological cases. Technological advancements in materials and visualization further enhance the performance of these devices, leading to widespread clinical acceptance. The demand for flexible ureteroscopes is increasing as urologists seek precision instruments that allow for safer and more efficient procedures.

In terms of clinical application, the urolithiasis segment commanded the highest market share in 2024 and is expected to reach USD 926 million by 2034. Urolithiasis affects a broad demographic and can result in serious complications if untreated. The precision and efficiency of ureteroscopes make them essential tools in treating this condition, particularly when stone removal or fragmentation is required through less invasive surgical means.

U.S. Ureteroscope Market was valued at USD 526.3 million in 2024 due to its strong healthcare infrastructure and high awareness of urological disorders. Advanced medical technology, combined with a significant patient population dealing with kidney stones and urinary tract issues, drives consistent demand. Additionally, the presence of top-tier medical device manufacturers and the rapid adoption of newer imaging tools solidify the country's leadership in this space.

Key players contributing to the competitive landscape of the Ureteroscope Market include Boston Scientific, STORZ, Ambu, PUSEN, Coloplast, BD, Stryker, Dornier MedTech, Neoscope, OLYMPUS, OPCOM Medical, and RICHARD WOLF. To strengthen their market position, companies in the ureteroscope industry are investing heavily in innovation, focusing on enhancing device flexibility, miniaturization, and optical clarity. They are actively expanding their product portfolios through strategic partnerships and product launches tailored to meet the demands of both developed and emerging healthcare markets. Continuous improvement in disposable and digital ureteroscope technology is also a key focus area. Additionally, players are ramping up their global distribution networks and engaging in training programs to support clinical adoption, thereby ensuring long-term competitiveness and sustained market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Usability

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of kidney stones and urinary tract diseases

- 3.2.1.2 Technological advancements in ureteroscopy

- 3.2.1.3 Growing adoption of minimally invasive devices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced and digital ureteroscopes

- 3.2.3 Opportunities

- 3.2.3.1 Expansion into emerging markets

- 3.2.3.2 Integration of ureteroscopes with robotic surgical systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Flexible ureteroscope

- 5.3 Rigid ureteroscope

Chapter 6 Market Estimates and Forecast, By Usability, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Reusable ureteroscopes

- 6.3 Disposable ureteroscopes

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Urolithiasis

- 7.3 Urethral stricture

- 7.4 Urinary tract infections

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Ambu

- 10.2 BD

- 10.3 Boston Scientific

- 10.4 Coloplast

- 10.5 Dornier MedTech

- 10.6 neoscope

- 10.7 OLYMPUS

- 10.8 OPCOM Medical

- 10.9 PUSEN

- 10.10 RICHARD WOLF

- 10.11 STORZ

- 10.12 Stryker

輸尿管鏡市場:2026-2032年全球市場預測(依產品類型、應用、技術、應用領域及最終用戶分類)輸尿管鏡設備市場:全球市場預測(按設備類型、技術、配件、應用和最終用戶分類)—2026-2032年機器人輔助輸尿管鏡市場:2026-2032年全球市場預測(按產品類型、可重複使用與一次性使用、技術、最終用戶和應用分類)

輸尿管鏡市場:2026-2032年全球市場預測(依產品類型、應用、技術、應用領域及最終用戶分類)輸尿管鏡設備市場:全球市場預測(按設備類型、技術、配件、應用和最終用戶分類)—2026-2032年機器人輔助輸尿管鏡市場:2026-2032年全球市場預測(按產品類型、可重複使用與一次性使用、技術、最終用戶和應用分類) 全球柔軟性和半硬式輸尿管鏡市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球柔軟性和半硬式輸尿管鏡市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026-2030年全球輸尿管鏡設備市場泌尿系統耗材市場按產品類型、材料、最終用戶、應用和分銷管道分類-2026年至2032年全球預測輸尿管鏡市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,2026-2034 年

2026-2030年全球輸尿管鏡設備市場泌尿系統耗材市場按產品類型、材料、最終用戶、應用和分銷管道分類-2026年至2032年全球預測輸尿管鏡市場規模、佔有率、成長及全球產業分析:按類型、應用和地區劃分的洞察,2026-2034 年 輸尿管鏡市場規模、佔有率及成長分析(按產品類型、應用、最終用戶和地區分類)-2026-2033年產業預測

輸尿管鏡市場規模、佔有率及成長分析(按產品類型、應用、最終用戶和地區分類)-2026-2033年產業預測 軟式和半硬式輸尿管鏡市場規模、佔有率和成長分析(按產品類型、應用、最終用戶和地區分類)—產業預測(2026-2033 年)

軟式和半硬式輸尿管鏡市場規模、佔有率和成長分析(按產品類型、應用、最終用戶和地區分類)—產業預測(2026-2033 年) 輸尿管鏡檢查:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)

輸尿管鏡檢查:全球市場佔有率和排名、總銷售額和需求預測(2025-2031 年)