|

市場調查報告書

商品編碼

1782097

橡膠-金屬黏合製品市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Rubber-To-Metal Bonded Articles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

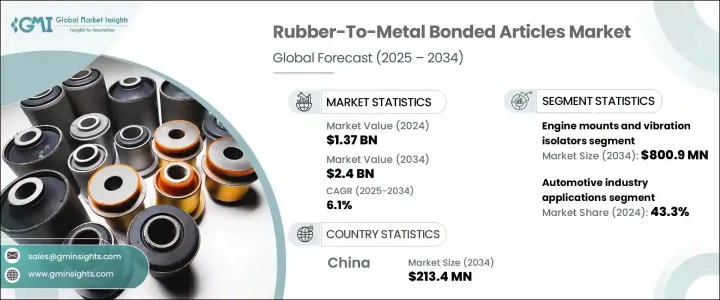

2024年,全球橡膠-金屬黏合製品市場規模達13.7億美元,預計到2034年將以6.1%的複合年成長率成長,達到24億美元。這一強勁勢頭得益於一系列終端行業日益成長的需求,包括工業機械、航太和汽車行業。在這些行業中,橡膠-金屬黏合製品對於降低噪音、吸收衝擊和抑制振動至關重要。由於汽車產業越來越青睞高性能、輕量化且符合燃油效率和排放標準的零件,汽車產業將繼續成為推動橡膠-金屬黏合製品需求的主導力量。

隨著法規日益嚴格,尤其是在排放和車輛安全方面,製造商正傾向於採用先進的黏合解決方案來滿足不斷變化的標準。航太業也在關鍵結構和功能領域擴大這些黏合部件的應用。此外,建築、醫療保健和電子等行業正在開闢新的應用途徑,預示著多元化的成長模式。黏合技術的創新,尤其是氰基丙烯酸酯黏合劑(其市場佔有率已超過40%),正在進一步推動產業發展。然而,原料和能源價格的上漲帶來了挑戰,尤其對規模較小的市場參與者而言。這可能會加速整合進程,因為大型企業正在尋求垂直整合和穩定其供應鏈。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13.7億美元 |

| 預測值 | 24億美元 |

| 複合年成長率 | 6.1% |

引擎支架和隔振器市場在2024年創收4.403億美元,預計到2034年將成長至8.009億美元,複合年成長率為6.2%。這些部件對於汽車和工業機械應用至關重要,在這些應用中,保持結構穩定性和最大限度地減少引擎相關的振動至關重要。在電動和混合動力車型中,它們的重要性更加突出,因為製造商優先考慮減輕重量和改善NVH(噪音、振動和聲振粗糙度)特性。

2024年,汽車領域佔據了最大的市場佔有率,達到43.3%,這得益於懸吊襯套、防振系統和排氣支架等黏合部件的廣泛使用。印度、德國、中國和美國等地區的市場擴張,帶動了對高性能耐用零件的需求成長。新興汽車技術正在重塑產品需求,促使製造商開發更整合、更有效率的零件,以符合最新的安全和排放標準。

中國橡膠-金屬黏合製品市場在2024年創收1.143億美元,預計年複合成長率為6.5%,到2034年將達到2.134億美元。儘管進口量下降,但該地區仍然是全球最大的橡膠-金屬黏合製品消費國,國內需求持續成長。有利的貿易政策和基礎設施投資正在推動中國向國內生產轉型,使中國在該行業更接近自給自足。與此同時,美國市場在同一時期經歷了顯著成長。

橡膠-金屬黏合製品市場的領導者包括大陸集團、哈金森公司、特瑞堡公司、住友理工株式會社和威巴克公司。為了鞏固其在橡膠-金屬黏合製品市場的地位,頂尖公司正專注於幾項核心策略。他們大力投資研發,以打造先進的輕量化黏合解決方案,滿足電動和混合動力汽車平台不斷變化的需求。他們正在進行策略性併購,以更好地控制供應鏈並擴大市場佔有率。主要參與者也在提升製造能力,並利用自動化來提高效率。此外,許多公司正在與原始設備製造商 (OEM) 簽訂長期契約,以確保穩定的需求並加強其全球影響力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計數據(註:僅提供重點國家的貿易統計數據

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 引擎支架和隔振器

- 汽車引擎支架

- 乘用車引擎支架

- 商用車引擎支架

- 電動車專用支架

- 工業隔振器

- 機械支架和隔離器

- 暖通空調系統隔離器

- 幫浦和壓縮機支架

- 航太引擎支架

- 飛機引擎支架

- 直升機振動系統

- 無人機和無人駕駛飛機應用

- 汽車引擎支架

- 襯套和懸吊部件

- 汽車襯套

- 控制臂襯套

- 穩定桿襯套

- 支柱安裝襯套

- 板簧襯套

- 工業套管

- 機械襯套

- 輸送系統組件

- 重型設備襯套

- 船舶和非公路用套管

- 船用引擎支架

- 建築設備襯套

- 農業機械零件

- 汽車襯套

- 密封件和墊圈

- 汽車密封件

- 引擎密封件和墊圈

- 變速箱密封件

- 差速器密封件

- 航太密封件

- 航空引擎密封件

- 液壓系統密封件

- 環境控制系統密封件

- 工業密封件

- 幫浦和閥門密封件

- 管道密封件

- 製程設備密封件

- 汽車密封件

- 聯軸器和軟性連接器

- 汽車驅動聯軸器

- CV 接頭防塵罩

- 傳動軸聯軸器

- 傳動聯軸器

- 工業用撓性聯軸器

- 馬達聯軸器

- 泵浦聯軸器

- 發電機聯軸器

- 船舶和航太聯軸器

- 螺旋槳軸聯軸器

- 飛機系統聯軸器

- 特殊黏合部件

- 汽車驅動聯軸器

- 防震墊和支架

- 減震器和阻尼器

- 軟性接頭和連接器

- 客製化工程解決方案

第6章:市場估計與預測:按鍵結技術,2021 - 2034 年

- 主要趨勢

- 化學鍵合技術

- 基於黏合劑的黏合系統

- 環氧基黏合劑

- 聚氨酯黏合劑

- 有機矽基體系

- 特種化學黏合劑

- 硫化黏合

- 硫磺硫化體系

- 過氧化物硫化

- 輻射硫化

- 金屬氧化物硫化

- 底漆和塗料系統

- 金屬表面底漆

- 橡膠相容塗料

- 多層黏合系統

- 基於黏合劑的黏合系統

- 機械鍵結技術

- 包覆成型工藝

- 嵌件成型應用

- 雙色射出成型系統

- 多材料成型

- 封裝技術

- 完整的封裝系統

- 部分封裝方法

- 選擇性黏合區域

- 機械聯鎖

- 紋理表面黏合

- 機械緊固系統

- 混合鍵合方法

- 包覆成型工藝

- 先進的鍵合技術

- 等離子處理黏合

- 大氣等離子系統

- 低壓等離子處理

- 電暈處理應用

- 雷射輔助鍵合

- 雷射表面活化

- 雷射焊接應用

- 選擇性雷射加工

- 奈米科技增強黏合

- 奈米粒子增強黏合劑

- 碳奈米管的應用

- 基於石墨烯的系統

- 等離子處理黏合

- 新興黏合技術

- 自修復黏合系統

- 智慧黏合技術

- 生物基黏合系統

- 可回收黏合解決方案

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 汽車產業應用

- 搭乘用車

- 引擎和動力總成部件

- 懸吊和底盤系統

- 車身和內裝應用

- 電動車專用零件

- 商用車

- 重型卡車應用

- 公車和長途汽車系統

- 專用車輛零件

- 摩托車和二輪車應用

- 引擎懸吊系統

- 懸吊部件

- 振動控制系統

- 汽車售後市場

- 替換零件市場

- 性能升級組件

- 維護和維修應用

- 搭乘用車

- 航太和國防工業

- 商業航空

- 引擎懸吊系統

- 起落架部件

- 客艙和內裝應用

- 環境控制系統

- 軍用和國防飛機

- 戰鬥機部件

- 運輸飛機系統

- 直升機應用

- 無人機和無人駕駛飛機系統

- 太空和衛星應用

- 運載火箭部件

- 衛星系統

- 太空站應用

- 航太售後市場

- 維修、維修和大修 (MRO)

- 零件更換市場

- 升級和現代化計劃

- 商業航空

- 工業機械設備

- 生產設備

- 工具機應用

- 自動化系統組件

- 機器人應用

- 流程工業

- 化學加工設備

- 石油和天然氣工業應用

- 發電系統

- 建築和採礦設備

- 重型機械部件

- 土方設備

- 礦山機械應用

- 海洋和近海

- 船舶引擎支架

- 海上平台部件

- 船舶推進系統

- 生產設備

- 基礎設施和建築

- 建築和施工

- 暖通空調系統組件

- 電梯和電扶梯系統

- 結構振動控制

- 交通基礎設施

- 鐵路系統部件

- 橋樑和隧道應用

- 機場基礎設施

- 公用事業和能源

- 發電廠部件

- 再生能源系統

- 輸配電

- 建築和施工

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- 3M Company

- BASF SE

- Bridgestone Corporation

- Continental AG

- Cooper Standard

- ElringKlinger AG

- Freudenberg Group

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hutchinson SA

- Parker Hannifin Corporation

- Sumitomo Riko Company Limited

- Trelleborg AB

- Vibracoustic

- ZF Friedrichshafen AG

The Global Rubber-To-Metal Bonded Articles Market was valued at USD 1.37 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 2.4 billion by 2034. This strong momentum is attributed to the growing demand across a range of end-use industries, including industrial machinery, aerospace, and automotive, where these components are essential in minimizing noise, absorbing shocks, and dampening vibrations. The automotive sector continues to be a dominant force in driving demand, owing to the increasing preference for high-performance, weight-saving components that support fuel efficiency and emissions compliance.

As regulations tighten, especially around emissions and vehicle safety, manufacturers are leaning into advanced bonding solutions to meet evolving standards. The aerospace industry is also expanding its use of these bonded parts in critical structural and functional areas. Additionally, sectors such as construction, healthcare, and electronics are creating new pathways for application, signaling a diversified growth pattern. Innovations in bonding technologies, especially with cyanoacrylate adhesives-which already command over 40% of the market-are providing a further lift. However, rising raw material and energy prices pose challenges, particularly for smaller market players. This may accelerate consolidation efforts, as larger firms look to integrate and stabilize their supply chains vertically.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.37 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 6.1% |

The engine mounts and vibration isolators segment generated USD 440.3 million in 2024 and is projected to grow to USD 800.9 million by 2034, growing at a CAGR of 6.2%. These components are critical across automotive and industrial machinery applications, where maintaining structural stability and minimizing engine-related vibrations are essential. Their relevance is heightened in both electric and hybrid models, where manufacturers prioritize reduced weight and improved NVH (Noise, Vibration, and Harshness) characteristics.

In 2024, the automotive segment held the largest market share at 43.3%, owing to the extensive usage of bonded components like suspension bushings, anti-vibration systems, and exhaust brackets. Market expansion in regions such as India, Germany, China, and the United States has led to increased demand for high-performance, durable components. Emerging vehicle technologies are reshaping product requirements, pushing manufacturers to develop more integrated, efficient parts that align with updated safety and emissions standards.

China Rubber-To-Metal Bonded Articles Market generated USD 114.3 million in 2024 and is forecasted to grow at a CAGR of 6.5%, to reach USD 213.4 million by 2034. Despite a dip in imports, the region remains the largest global consumer, with local demand continuing to rise. Favorable trade policies and infrastructure investment are driving a shift toward domestic production, allowing China to move closer to self-reliance in this industry. Meanwhile, the United States experienced significant market growth during the same period.

Leading players in the Rubber-To-Metal Bonded Articles Market include Continental AG, Hutchinson SA, Trelleborg AB, Sumitomo Riko Co., Ltd., and Vibracoustic GmbH. To strengthen their position in the rubber-to-metal bonded articles market, top companies are focusing on several core strategies. They are heavily investing in research and development to create advanced, lightweight bonding solutions that cater to the evolving needs of electric and hybrid vehicle platforms. Strategic mergers and acquisitions are being pursued to gain better control of supply chains and expand market share. Key players are also enhancing their manufacturing capabilities and leveraging automation to improve efficiency. Furthermore, many are entering long-term contracts with OEMs to ensure consistent demand and strengthen their global presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.7 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Engine mounts and vibration isolators

- 5.2.1 Automotive engine mounts

- 5.2.1.1 Passenger vehicle engine mounts

- 5.2.1.2 Commercial vehicle engine mounts

- 5.2.1.3 Electric vehicle specialized mounts

- 5.2.2 Industrial vibration isolators

- 5.2.2.1 Machinery mounts and isolators

- 5.2.2.2 Hvac system isolators

- 5.2.2.3 Pump and compressor mounts

- 5.2.3 Aerospace engine mounts

- 5.2.3.1 Aircraft engine mounts

- 5.2.3.2 Helicopter vibration systems

- 5.2.3.3 Uav and drone applications

- 5.2.1 Automotive engine mounts

- 5.3 Bushings and suspension components

- 5.3.1 Automotive bushings

- 5.3.1.1 Control arm bushings

- 5.3.1.2 Sway bar bushings

- 5.3.1.3 Strut mount bushings

- 5.3.1.4 Leaf spring bushings

- 5.3.2 Industrial bushings

- 5.3.2.1 Machinery bushings

- 5.3.2.2 Conveyor system components

- 5.3.2.3 Heavy equipment bushings

- 5.3.3 Marine and off-highway bushings

- 5.3.3.1 Marine engine mounts

- 5.3.3.2 Construction equipment bushings

- 5.3.3.3 Agricultural machinery components

- 5.3.1 Automotive bushings

- 5.4 Seals and gaskets

- 5.4.1 Automotive seals

- 5.4.1.1 Engine seals and gaskets

- 5.4.1.2 Transmission seals

- 5.4.1.3 Differential seals

- 5.4.2 Aerospace seals

- 5.4.2.1 Aircraft engine seals

- 5.4.2.2 Hydraulic system seals

- 5.4.2.3 Environmental control system seals

- 5.4.3 Industrial seals

- 5.4.3.1 Pump and valve seals

- 5.4.3.2 Pipeline seals

- 5.4.3.3 Process equipment seals

- 5.4.1 Automotive seals

- 5.5 Couplings and flexible connectors

- 5.5.1 Automotive drive couplings

- 5.5.1.1 Cv joint boots

- 5.5.1.2 Driveshaft couplings

- 5.5.1.3 Transmission couplings

- 5.5.2 Industrial flexible couplings

- 5.5.2.1 Motor couplings

- 5.5.2.2 Pump couplings

- 5.5.2.3 Generator couplings

- 5.5.3 Marine and aerospace couplings

- 5.5.3.1 Propeller shaft couplings

- 5.5.3.2 Aircraft system couplings

- 5.5.3.3 Specialty bonded components

- 5.5.1 Automotive drive couplings

- 5.6 Anti-vibration pads and mounts

- 5.6.1 Shock absorbers and dampers

- 5.6.2 Flexible joints and connectors

- 5.6.3 Custom engineered solutions

Chapter 6 Market Estimates and Forecast, By Bonding Technology, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Chemical bonding technologies

- 6.2.1 Adhesive-based bonding systems

- 6.2.1.1 Epoxy-based adhesives

- 6.2.1.2 Polyurethane adhesives

- 6.2.1.3 Silicone-based systems

- 6.2.1.4 Specialty chemical adhesives

- 6.2.2 Vulcanization bonding

- 6.2.2.1 Sulfur vulcanization systems

- 6.2.2.2 Peroxide vulcanization

- 6.2.2.3 Radiation vulcanization

- 6.2.2.4 Metal oxide vulcanization

- 6.2.3 Primer and coating systems

- 6.2.3.1 Metal surface primers

- 6.2.3.2 Rubber-compatible coatings

- 6.2.3.3 Multi-layer bonding systems

- 6.2.1 Adhesive-based bonding systems

- 6.3 Mechanical bonding technologies

- 6.3.1 Overmolding processes

- 6.3.1.1 Insert molding applications

- 6.3.1.2 Two-shot molding systems

- 6.3.1.3 Multi-material molding

- 6.3.2 Encapsulation technologies

- 6.3.2.1 Complete encapsulation systems

- 6.3.2.2 Partial encapsulation methods

- 6.3.2.3 Selective bonding areas

- 6.3.3 Mechanical interlocking

- 6.3.3.1 Textured surface bonding

- 6.3.3.2 Mechanical fastening systems

- 6.3.3.3 Hybrid bonding approaches

- 6.3.1 Overmolding processes

- 6.4 Advanced bonding technologies

- 6.4.1 Plasma treatment bonding

- 6.4.1.1 Atmospheric plasma systems

- 6.4.1.2 Low-pressure plasma treatment

- 6.4.1.3 Corona treatment applications

- 6.4.2 Laser-assisted bonding

- 6.4.2.1 Laser surface activation

- 6.4.2.2 Laser welding applications

- 6.4.2.3 Selective laser processing

- 6.4.3 Nanotechnology-enhanced bonding

- 6.4.3.1 Nanoparticle-enhanced adhesives

- 6.4.3.2 Carbon nanotube applications

- 6.4.3.3 Graphene-based systems

- 6.4.1 Plasma treatment bonding

- 6.5 Emerging bonding technologies

- 6.5.1 Self-healing bonding systems

- 6.5.2 Smart adhesive technologies

- 6.5.3 Bio-based bonding systems

- 6.5.4 Recyclable bonding solutions

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Automotive industry applications

- 7.2.1 Passenger vehicles

- 7.2.1.1 Engine and powertrain components

- 7.2.1.2 Suspension and chassis systems

- 7.2.1.3 Body and interior applications

- 7.2.1.4 Electric vehicle specific components

- 7.2.2 Commercial vehicles

- 7.2.2.1 Heavy-duty truck applications

- 7.2.2.2 Bus and coach systems

- 7.2.2.3 Specialty vehicle components

- 7.2.3 Motorcycle and two-wheeler applications

- 7.2.3.1 Engine mount systems

- 7.2.3.2 Suspension components

- 7.2.3.3 Vibration control systems

- 7.2.4 Automotive aftermarket

- 7.2.4.1 Replacement parts market

- 7.2.4.2 Performance upgrade components

- 7.2.4.3 Maintenance and repair applications

- 7.2.1 Passenger vehicles

- 7.3 Aerospace and defense industry

- 7.3.1 Commercial aviation

- 7.3.1.1 Engine mount systems

- 7.3.1.2 Landing gear components

- 7.3.1.3 Cabin and interior applications

- 7.3.1.4 Environmental control systems

- 7.3.2 Military and defense aircraft

- 7.3.2.1 Fighter aircraft components

- 7.3.2.2 Transport aircraft systems

- 7.3.2.3 Helicopter applications

- 7.3.2.4 Uav and drone systems

- 7.3.3 Space and satellite applications

- 7.3.3.1 Launch vehicle components

- 7.3.3.2 Satellite systems

- 7.3.3.3 Space station applications

- 7.3.4 Aerospace aftermarket

- 7.3.4.1 Maintenance, repair, and overhaul (MRO)

- 7.3.4.2 Component replacement market

- 7.3.4.3 Upgrade and modernization programs

- 7.3.1 Commercial aviation

- 7.4 Industrial machinery and equipment

- 7.4.1 Manufacturing equipment

- 7.4.1.1 Machine tool applications

- 7.4.1.2 Automation system components

- 7.4.1.3 Robotics applications

- 7.4.2 Process industries

- 7.4.2.1 Chemical processing equipment

- 7.4.2.2 Oil and gas industry applications

- 7.4.2.3 Power generation systems

- 7.4.3 Construction and mining equipment

- 7.4.3.1 Heavy machinery components

- 7.4.3.2 Earth moving equipment

- 7.4.3.3 Mining machinery applications

- 7.4.4 Marine and offshore

- 7.4.4.1 Ship engine mounts

- 7.4.4.2 Offshore platform components

- 7.4.4.3 Marine propulsion systems

- 7.4.1 Manufacturing equipment

- 7.5 Infrastructure and construction

- 7.5.1 Building and construction

- 7.5.1.1 Hvac system components

- 7.5.1.2 Elevator and escalator systems

- 7.5.1.3 Structural vibration control

- 7.5.2 Transportation infrastructure

- 7.5.2.1 Railway system components

- 7.5.2.2 Bridge and tunnel applications

- 7.5.2.3 Airport infrastructure

- 7.5.3 Utilities and energy

- 7.5.3.1 Power plant components

- 7.5.3.2 Renewable energy systems

- 7.5.3.3 Transmission and distribution

- 7.5.1 Building and construction

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 3M Company

- 9.2 BASF SE

- 9.3 Bridgestone Corporation

- 9.4 Continental AG

- 9.5 Cooper Standard

- 9.6 ElringKlinger AG

- 9.7 Freudenberg Group

- 9.8 H.B. Fuller Company

- 9.9 Henkel AG & Co. KGaA

- 9.10 Hutchinson SA

- 9.11 Parker Hannifin Corporation

- 9.12 Sumitomo Riko Company Limited

- 9.13 Trelleborg AB

- 9.14 Vibracoustic

- 9.15 ZF Friedrichshafen AG