|

市場調查報告書

商品編碼

1782096

麵糊預混料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Batter-Based Premixes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

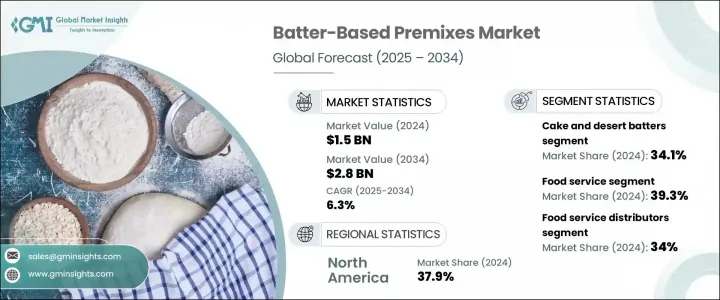

2024 年全球麵糊預混料市場價值為 15 億美元,預計到 2034 年將以 6.3% 的複合年成長率成長至 28 億美元。麵糊預混料是方便、即用的乾性或半乾性混合物,包含麵粉、澱粉、膨鬆劑、調味料和功能性添加劑等成分。這些混合物在油炸或烘烤前應用於肉類、海鮮、蔬菜和烘焙食品等各種食品,以確保所有批次的口味、質地和外觀一致。由於其節省時間的優勢和標準化的質量,它們廣泛應用於餐飲服務、冷凍食品生產和家庭烹飪。消費者對簡便食品的需求不斷成長,以及快餐店 (QSR) 在城市和半城市地區的擴張,推動了市場穩步成長。

隨著清潔標籤、無過敏原、植物性和功能性塗層越來越受到關注,以滿足注重健康的消費者的需求,巨大的成長機會隨之而來。無麩質和純素麵糊的創新,以及人們對韓式、地中海式和天婦羅式油炸食品等民族美食日益成長的興趣,正在擴大各地區的產品種類。冷凍塗層食品在零售業的日益流行,以及自有品牌和合約製造在發展中市場的興起,為行業帶來了進一步的成長途徑和合作夥伴關係。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15億美元 |

| 預測值 | 28億美元 |

| 複合年成長率 | 6.3% |

2024年,蛋糕和甜點麵糊市場佔據主導地位,市佔率達34.1%,價值達5.214億美元。此細分市場包括漏斗蛋糕、甜甜圈和特色甜點等產品的預拌粉,這得益於消費者對便利、即食甜點的強烈需求。由於其易用性、穩定的品質和創新的口味,該細分市場在餐飲服務、烘焙連鎖店和零售業廣受歡迎。此外,低糖和無過敏原等功能性甜點麵糊將繼續提升該細分市場在傳統市場和健康市場中的相關性。

餐飲服務領域在2024年佔據39.3%的市場佔有率,估值達6.014億美元。該領域佔據領先地位,因為麵糊預混料在快餐店、休閒餐廳和機構餐飲服務中廣泛使用,而穩定的品質、速度和口感對於油炸和裹粉類菜餚至關重要。消費者對油炸開胃菜、雞肉菜餚、海鮮和國際風味的日益成長的喜愛推動了這一需求。餐飲服務提供者依靠專用麵糊來實現酥脆口感、保留風味,並在大量生產中保持高效。

2024年,北美麵糊預混料市場佔據37.9%的市佔率。該地區的領先地位得益於密集的快餐店、消費者對即食食品和加工食品的強勁需求,以及發達的餐飲服務和零售分銷基礎設施。 House-Autry Mills、Bowman Ingredients、Newly Weds Foods、Kerry Group PLC 和 Blendex Company 等大型公司在該地區佔有重要地位,推動產品創新並擴大市場覆蓋範圍。持續的研發工作專注於清潔標籤、無過敏原和健康導向的麵糊配方,以滿足消費者日益成長的透明度和便利性需求。

為了鞏固市場地位,麵糊類預混料行業的公司高度重視產品創新,開發清潔標籤、無過敏原和植物性配方,以滿足不斷變化的消費者偏好。他們投資研發,客製化符合不同烹飪風格和地理口味的預混料。與餐飲連鎖店、快餐店和零售店建立策略合作夥伴關係,有助於擴大分銷管道並提升品牌知名度。此外,公司透過精簡供應鏈來提高營運效率,並投資於強調便利性、健康益處和品質的行銷活動,從而增強消費者忠誠度並加速市場滲透。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 煎餅和華夫餅預拌粉

- 傳統煎餅粉

- 比利時華夫餅預拌粉

- 特色和風味變體

- 天婦羅和亞洲麵糊

- 傳統天婦羅麵糊

- 酥脆的麵糊

- 亞洲特色應用

- 魚和海鮮麵糊

- 炸魚薯條麵糊

- 海鮮塗料混合物

- 預浸麵糊系統

- 蛋糕和甜點麵糊

- 漏斗蛋糕混合物

- 甜甜圈麵糊

- 特色甜點應用

- 特種功能性麵糊

- 無麩質配方

- 有機和清潔標籤產品

- 植物性和替代蛋白麵糊

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 餐飲服務

- 速食店

- 休閒餐廳

- 機構餐飲服務

- 商業食品製造

- 冷凍食品生產商

- 休閒食品製造商

- 海鮮加工商

- 零售和消費者

- 雜貨店和超市連鎖店

- 特色食品店

- 線上零售平台

- 工業和合約製造

- 自有品牌製造商

- 聯合包裝商和合約生產商

- 出口型製造商

第7章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 直銷

- 製造商到食品服務

- 合約製造協議

- 食品服務分銷商

- 廣泛經銷商

- 特色食品服務供應商

- 零售通路

- 超市和大賣場

- 特色食品店

- 線上零售平台

- 產業分佈

- 原料分銷商

- 設備及解決方案提供商

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- Kerry Group PLC

- Newly Weds

- Bowman Ingredients

- Breading & Coating Ltd.

- House-Autry mills Inc.

- BRATA Produktions

- Shimakyu

- Thai Nisshin Technomic Co., Ltd

- Arcadia Foods

- Blendex Company

The Global Batter-Based Premixes Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 2.8 billion by 2034. Batter-based premixes are convenient, ready-to-use dry or semi-dry blends that include ingredients such as flour, starches, leavening agents, seasonings, and functional additives. These mixes are applied to various food items like meat, seafood, vegetables, and baked goods before frying or baking to ensure consistent taste, texture, and appearance across all batches. Their widespread use spans foodservice, frozen food production, and home cooking due to the time-saving benefits and standardized quality they provide. The market's steady growth is fueled by rising consumer demand for convenience foods and the expansion of quick-service restaurants (QSRs) in urban and semi-urban regions.

Significant growth opportunities exist with increased focus on clean-label, allergen-free, plant-based, and functional coatings catering to health-conscious consumers. Innovations in gluten-free and vegan batters, along with growing interest in ethnic cuisines such as Korean, Mediterranean, and tempura-style fried foods, are broadening product variety across regions. The rising popularity of frozen coated foods in retail and the emergence of private label and contract manufacturing in developing markets present further growth avenues and partnerships.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 6.3% |

The cake and dessert batters segment led the market in 2024, holding 34.1% share with a value of USD 521.4 million. This segment includes mixes for products such as funnel cakes, donuts, and specialty desserts, driven by strong consumer demand for convenient, ready-to-cook sweet treats. Its popularity spans foodservice, bakery chains, and retail sectors, supported by ease of use, consistent quality, and innovative flavors. Additionally, functional dessert batters like low-sugar and allergen-free varieties continue to enhance the segment's relevance in both traditional and health-focused markets.

The foodservice segment has a 39.3% share in 2024, with a valuation of USD 601.4 million. This sector leads due to extensive use of batter premixes in QSRs, casual dining, and institutional foodservice, where consistent quality, speed, and texture are essential for fried and coated menu items. Growing consumer preference for fried appetizers, chicken dishes, seafood, and international flavors drives this demand. Foodservice providers rely on specialized batters to achieve crispiness, preserve flavor, and maintain efficiency in high-volume production.

North America Batter-Based Premixes Market held a 37.9% share in 2024. The region's leadership is supported by a dense presence of QSRs, strong consumer demand for ready-to-cook and processed foods, and well-developed foodservice and retail distribution infrastructures. Major companies such as House-Autry Mills, Bowman Ingredients, Newly Weds Foods, Kerry Group PLC, and Blendex Company have a significant presence here, driving product innovation and expanding market reach. Continuous R&D efforts focusing on clean-label, allergen-free, and health-oriented batter formulations align with growing consumer demand for transparency and convenience.

To strengthen their market position, companies in the batter-based premixes sector focus heavily on product innovation, developing clean-label, allergen-free, and plant-based formulations that resonate with evolving consumer preferences. They invest in research and development to customize premixes that cater to diverse culinary styles and regional tastes. Strategic partnerships with foodservice chains, quick-service restaurants, and retail outlets help expand distribution and boost brand visibility. Additionally, companies enhance operational efficiency through streamlined supply chains and invest in marketing campaigns that emphasize convenience, health benefits, and quality, building stronger consumer loyalty and accelerating market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pancake and waffle mixes

- 5.2.1 Traditional pancake mixes

- 5.2.2 Belgian waffle mixes

- 5.2.3 Specialty and flavoured variants

- 5.3 Tempura and asian batters

- 5.3.1 Traditional tempura batters

- 5.3.2 Crispy coating batters

- 5.3.3 Specialty asian applications

- 5.4 Fish and seafood batters

- 5.4.1 Fish and chips batters

- 5.4.2 Seafood coating mixes

- 5.4.3 Pre-dip batter systems

- 5.5 Cake and dessert batters

- 5.5.1 Funnel cake mixes

- 5.5.2 Donut batters

- 5.5.3 Specialty dessert applications

- 5.6 Specialty and functional batters

- 5.6.1 Gluten-free formulations

- 5.6.2 Organic and clean label products

- 5.6.3 Plant-based and alternative protein batters

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food service

- 6.2.1 Quick service restaurants

- 6.2.2 Casual dining restaurants

- 6.2.3 Institutional food service

- 6.3 Commercial food manufacturing

- 6.3.1 Frozen food producers

- 6.3.2 Snack food manufacturers

- 6.3.3 Seafood processors

- 6.4 Retail and consumer

- 6.4.1 Grocery and supermarket chains

- 6.4.2 Specialty food stores

- 6.4.3 Online retail platforms

- 6.5 Industrial and contract manufacturing

- 6.5.1 Private label manufacturers

- 6.5.2 Co-packers and contract producers

- 6.5.3 Export-oriented manufacturers

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.2.1 Manufacturer to food service

- 7.2.2 Contract manufacturing agreements

- 7.3 Food service distributors

- 7.3.1 Broad-line distributors

- 7.3.2 Specialty food service suppliers

- 7.4 Retail channels

- 7.4.1 Supermarkets and hypermarkets

- 7.4.2 Specialty food stores

- 7.4.3 Online retail platforms

- 7.5 Industrial distribution

- 7.5.1 Ingredient distributors

- 7.5.2 Equipment and solution providers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 1.1 Key trends

- 1.2 North America

- 1.2.1 U.S.

- 1.2.2 Canada

- 1.3 Europe

- 1.3.1 Germany

- 1.3.2 UK

- 1.3.3 France

- 1.3.4 Spain

- 1.3.5 Italy

- 1.3.6 Netherlands

- 1.3.7 Rest of Europe

- 1.4 Asia Pacific

- 1.4.1 China

- 1.4.2 India

- 1.4.3 Japan

- 1.4.4 Australia

- 1.4.5 South Korea

- 1.4.6 Rest of Asia Pacific

- 1.5 Latin America

- 1.5.1 Brazil

- 1.5.2 Mexico

- 1.5.3 Argentina

- 1.5.4 Rest of Latin America

- 1.6 Middle East and Africa

- 1.6.1 Saudi Arabia

- 1.6.2 South Africa

- 1.6.3 UAE

- 1.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Kerry Group PLC

- 9.2 Newly Weds

- 9.3 Bowman Ingredients

- 9.4 Breading & Coating Ltd.

- 9.5 House-Autry mills Inc.

- 9.6 BRATA Produktions

- 9.7 Shimakyu

- 9.8 Thai Nisshin Technomic Co., Ltd

- 9.9 Arcadia Foods

- 9.10 Blendex Company