|

市場調查報告書

商品編碼

1773456

輻照設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Irradiation Apparatus Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

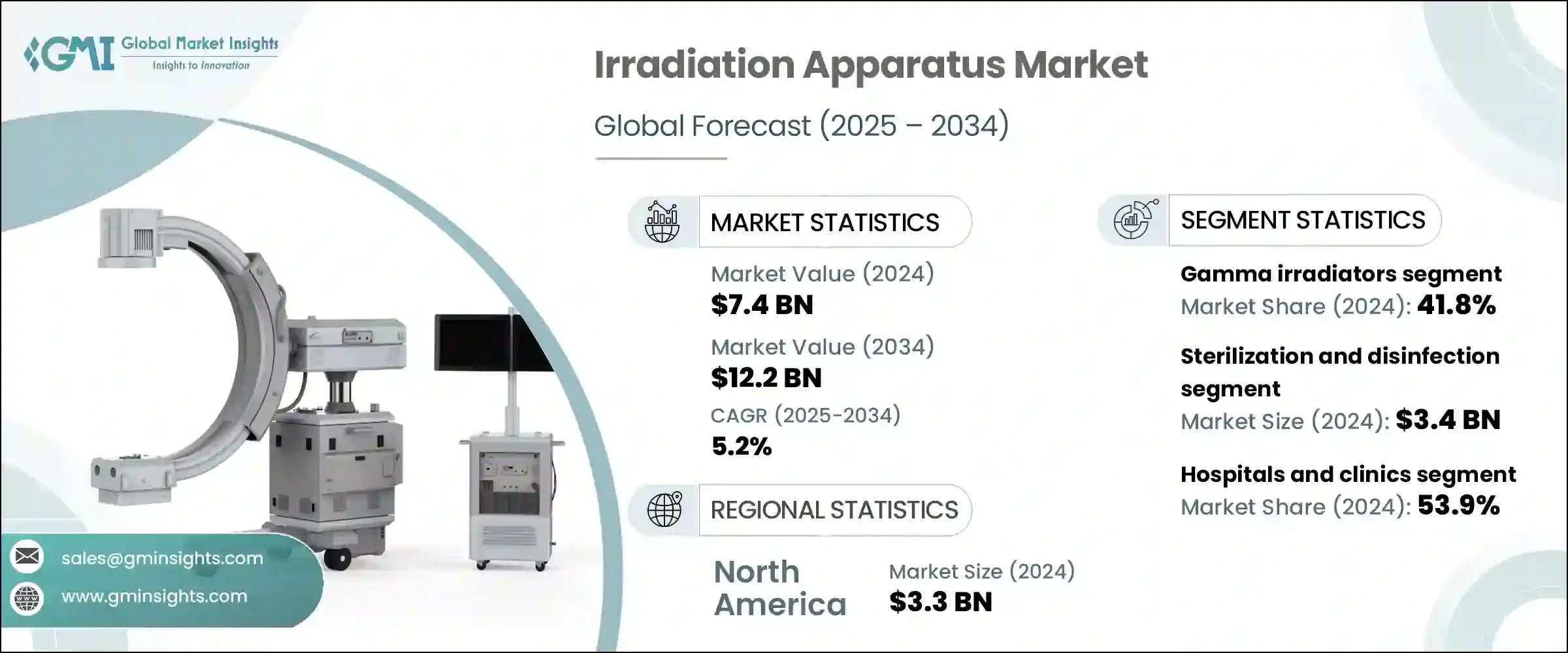

2024年,全球輻照設備市場規模達74億美元,預計到2034年將以5.2%的複合年成長率成長,達到122億美元。這一成長主要得益於醫療和工業領域對電離輻射和非電離輻射的日益成長的需求。這些系統主要用於診斷、治療、滅菌和研究。

放射治療在癌症治療中的日益普及是推動市場成長的重要因素,因為精準靶向照射系統能夠改善治療結果和患者體驗。對早期發現和即時干預的強烈追求正在推動近距離放射治療設備和直線加速器等設備的投資不斷增加。隨著腫瘤診所和專科醫療中心在全球範圍內的擴張,先進照射系統的採用率持續上升,凸顯了對高效、便捷的癌症治療技術的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 74億美元 |

| 預測值 | 122億美元 |

| 複合年成長率 | 5.2% |

影像導引放射治療和人工智慧系統的現代創新正在重塑放射治療設備的格局。這些平台整合了機器人控制和即時成像技術,能夠在保護周圍組織的同時,為腫瘤提供精準的劑量。直線加速器和影像導引放射治療等技術如今正提供更高的精準度和更低的併發症風險,並且正在被醫療機構廣泛採用。

更佳的治療效果、更短的恢復時間和更低的副作用,正激勵醫院和診所轉型為新一代系統。在新興地區,公共和私營部門的持續投資正在支持醫療基礎設施的升級,從而縮小治療的可及性差距。隨著對基於輻射的治療和滅菌解決方案的需求不斷成長,醫療改革和技術驅動的改進正在推動全球市場的發展。

2024年,伽瑪輻照器市場佔最大佔有率,達41.8%。一次性醫療產品消費的不斷成長是伽馬射線滅菌系統發展的主要驅動力。由於伽馬射線能夠有效滅菌熱敏性和化學易損物品,製造商越來越依賴這種方法來滅菌注射器、導管和手術手套。

使用伽馬射線的滅菌過程不會留下有害殘留物,在受監管的醫療環境中提供可靠的解決方案。這些系統在處理血液成分以防止輸血後不良反應方面也至關重要。隨著感染控制和無菌保證日益受到全球監管機構的重視,伽馬輻照器將繼續成為關鍵醫療設備和用品製造和加工的首選解決方案。

2024年,醫院和診所市場佔據主導地位,佔有率達53.9%。這些機構是輻照設備的主要用戶,廣泛用於診斷影像和治療干預。 X光機、CT系統和透視機等設備在非侵入性評估患者病情方面發揮關鍵作用。

此外,為了因應醫療相關感染,醫院正轉向採用基於輻照的滅菌技術對侵入性醫療器材進行滅菌,以確保病患安全並符合衛生法規。與熱處理或化學滅菌相比,輻照滅菌為手術器械和其他可重複使用零件的滅菌提供了更快速、更可靠的方法。診斷準確性與感染預防相結合,使得輻照設備在現代醫療機構中不可或缺。

2024年,美國輻照設備市場規模達30億美元,預計2034年將達49億美元。慢性疾病(尤其是癌症)的發生率不斷上升,推動了美國各地對先進放射治療解決方案的需求。同時,美國醫療保健產業對門診手術中心和門診診所等分散式治療場所的重視,也加速了對緊湊高效滅菌系統的需求。

隨著這些小型醫療機構尋求高通量且節省空間的解決方案,模組化輻照系統因其速度快、可靠性高且能夠保持設備完整性而變得極具吸引力。這種向經濟高效且分散式醫療保健模式的轉變預計將使輻照技術在城市和農村地區保持強勁成長。

塑造輻照設備市場競爭格局的關鍵產業參與者包括通用電氣醫療集團 (GE HealthCare)、醫科達 (Elekta)、西門子醫療集團 (Siemens Healthineers)、邁瑞 (Mindray)、佳能醫療系統 (Canon Medical Systems)、NPB 離子束技術 (NPB Ion Beam Technology)、東大醫科醫療系統 (Canon Medical Systems)、NPB 離子束技術 (NPB Ion Beam Technology)、東業軟工醫療系統 (Neusoft Medical)、重做家庭工友Heavy Industries)、新華醫療 (Shinva Medical)、荷蘭皇家飛利浦 (Koninklijke Philips)、Mevion 醫療系統 (Mevion Medical Systems) 和 Panacea 醫療技術 (Panacea Medical Technologies)。這些公司透過產品創新和策略擴張持續樹立產業標竿。

輻照設備領域的領先企業正致力於透過先進的影像引導和人工智慧整合放射系統來擴展產品組合。許多公司正在大力投資研發,以提高治療準確性、實現工作流程自動化並增強安全性。與癌症治療中心和醫療機構的合作有助於客製化符合不斷變化的臨床需求的解決方案。為了滿足全球需求,尤其是在醫療資源匱乏的地區,各公司正在開發模組化且經濟高效的系統,以降低安裝複雜性。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 癌症和慢性病發生率上升

- 影像和放射治療設備的技術進步

- 醫療基礎建設投資不斷增加

- 提高血液安全意識

- 產業陷阱與挑戰

- 資本投資和維護成本高

- 嚴格的法規核准和合規要求

- 市場機會

- 成像系統中人工智慧和自動化的應用

- 非化學滅菌需求加速成長

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 定價分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利分析

- 波特的分析

- PESTEL分析

- 消費者行為分析

第4章:競爭格局

- 介紹

- 競爭市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 伽瑪輻照器

- X光照射器

- 紫外線 (UV) 和中子輻照器

- 電子束輻照器

- 其他類型

第6章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 診斷影像

- 治療/放射治療

- 滅菌消毒

- 其他應用

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院和診所

- 研究實驗室和研究所

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Accuray

- Canon Medical Systems

- Elekta

- GE HealthCare

- Hitachi

- Koninklijke Philips

- Mevion Medical Systems

- Mindray

- Neusoft Medical Systems

- Panacea Medical Technologies

- Shinva Medical

- Siemens Healthineers

- Sumitomo Heavy Industries

- ViewRay

The Global Irradiation Apparatus Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 12.2 billion by 2034. This growth is driven by the increasing utilization of ionizing and non-ionizing radiation across both medical and industrial applications. These systems are primarily deployed for diagnostics, therapeutic use, sterilization, and research purposes.

The rising adoption of radiotherapy in cancer care is a significant factor propelling the market growth, as precision-targeted irradiation systems improve both outcomes and patient experiences. A strong push toward early detection and immediate intervention is increasing investments in devices such as brachytherapy equipment and linear accelerators. With oncology clinics and specialized medical centers expanding globally, the adoption of advanced irradiation systems continues to rise, underscoring the demand for efficient and accessible cancer treatment technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.2% |

Modern innovations in image-guided radiation therapy and AI-enabled systems are reshaping the landscape of irradiation apparatus. Integrated with robotic control and real-time imaging, these platforms provide accurate dose delivery to tumors while safeguarding surrounding tissues. Technologies such as linear accelerators and image-guided radiotherapy are now delivering higher levels of precision and lower complication risks, leading to widespread adoption across healthcare facilities.

Enhanced therapeutic outcomes, reduced recovery times, and minimized side effects are encouraging hospitals and clinics to transition to next-generation systems. In emerging regions, increased investments from both public and private sectors are supporting healthcare infrastructure upgrades, helping close treatment accessibility gaps. As demand grows for radiation-based solutions in both treatment and sterilization, the global market is being fueled by healthcare reforms and technology-driven improvements.

In 2024, the gamma irradiator segment accounted for the largest market share at 41.8%. The growing consumption of disposable medical products has been a major driver for gamma-based sterilization systems. As gamma radiation enables effective sterilization of heat-sensitive and chemically delicate items, manufacturers are increasingly relying on this method for syringes, catheters, and surgical gloves.

Sterilization processes using gamma rays leave no harmful residue, offering a reliable solution in regulated medical environments. These systems are also essential in treating blood components to prevent adverse post-transfusion reactions. With infection control and sterility assurance gaining focus across global regulatory bodies, gamma irradiators continue to be a preferred solution in the manufacture and processing of critical healthcare equipment and supplies.

The hospitals and clinics segment led the market in 2024 with a share of 53.9%. These facilities are primary users of irradiation apparatus, utilizing them extensively for diagnostic imaging and therapeutic interventions. Equipment like X-ray units, CT systems, and fluoroscopy machines play a pivotal role in evaluating patient conditions non-invasively.

Moreover, to combat healthcare-associated infections, hospitals are turning to irradiation-based sterilization for invasive medical tools, ensuring both patient safety and compliance with hygiene regulations. Compared to heat or chemical alternatives, irradiation offers a faster and more dependable method for sterilizing surgical instruments and other reusable components. The combination of diagnostic accuracy and infection prevention is making irradiation apparatus indispensable across modern healthcare facilities.

U.S. Irradiation Apparatus Market was valued at USD 3 billion in 2024 and is estimated to reach USD 4.9 billion by 2034. A growing prevalence of chronic illnesses-particularly cancer-is pushing demand for advanced radiation therapy solutions across the country. In tandem, the U.S. healthcare industry's emphasis on decentralized treatment settings like ambulatory surgical centers and outpatient clinics is accelerating the need for compact, efficient sterilization systems.

As these smaller facilities look for high-throughput and space-saving solutions, modular irradiation systems have become highly attractive due to their speed, reliability, and ability to preserve equipment integrity. This shift toward cost-effective and distributed healthcare models is expected to sustain robust growth for irradiation technologies across both urban and rural settings.

Key industry participants shaping the competitive landscape of the Irradiation Apparatus Market include GE HealthCare, Elekta, Siemens Healthineers, Mindray, Canon Medical Systems, NPB Ion Beam Technology, Neusoft Medical Systems, Accuray, ViewRay, Hitachi, Sumitomo Heavy Industries, Shinva Medical, Koninklijke Philips, Mevion Medical Systems, and Panacea Medical Technologies. These companies continue to set benchmarks through product innovation and strategic expansion.

Leading players in the irradiation apparatus space are focusing on product portfolio expansion through advanced imaging-guided and AI-integrated radiation systems. Many companies are heavily investing in R&D to boost treatment accuracy, automate workflows, and enhance safety. Collaborations with cancer treatment centers and healthcare institutions are helping tailor solutions that match evolving clinical needs. To address global demand, especially in underserved regions, firms are developing modular and cost-effective systems that reduce installation complexity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cancer and chronic diseases

- 3.2.1.2 Technological advancements in imaging and radiotherapy equipment

- 3.2.1.3 Growing investments in healthcare infrastructure

- 3.2.1.4 Increased awareness of blood safety

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital investment and maintenance costs

- 3.2.2.2 Strict regulatory approvals and compliance requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AI and automation in imaging systems

- 3.2.3.2 Accelerated demand for non-chemical sterilization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

- 3.12 Consumer behaviour analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Gamma irradiators

- 5.3 X-ray irradiators

- 5.4 Ultraviolet (UV) and neutron irradiators

- 5.5 Electron-beam irradiators

- 5.6 Other types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Diagnostic imaging

- 6.3 Therapy/radiotherapy

- 6.4 Sterilization and disinfection

- 6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Research laboratories and institutes

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accuray

- 9.2 Canon Medical Systems

- 9.3 Elekta

- 9.4 GE HealthCare

- 9.5 Hitachi

- 9.6 Koninklijke Philips

- 9.7 Mevion Medical Systems

- 9.8 Mindray

- 9.9 Neusoft Medical Systems

- 9.10 Panacea Medical Technologies

- 9.11 Shinva Medical

- 9.12 Siemens Healthineers

- 9.13 Sumitomo Heavy Industries

- 9.14 ViewRay

2026年全球綠色電子加速器市場報告

2026年全球綠色電子加速器市場報告 電子束輻照系統市場按應用、終端用戶產業、能量水平和設備類型分類,全球預測(2026-2032年)2026年全球輻射設備市場報告2025年全球醫療輻照市場報告

電子束輻照系統市場按應用、終端用戶產業、能量水平和設備類型分類,全球預測(2026-2032年)2026年全球輻射設備市場報告2025年全球醫療輻照市場報告 全球電子束線性加速器市場全球輻照設備市場

全球電子束線性加速器市場全球輻照設備市場 輻照設備市場,按類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

輻照設備市場,按類型、按應用、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測 美國輻照設備市場規模、佔有率、趨勢分析報告:按類型、應用、最終用途和細分市場預測,2025 年至 2030 年輻照設備市場規模、佔有率、趨勢分析報告:2025-2030 年按類型、應用、最終用途、地區和細分市場進行的預測

美國輻照設備市場規模、佔有率、趨勢分析報告:按類型、應用、最終用途和細分市場預測,2025 年至 2030 年輻照設備市場規模、佔有率、趨勢分析報告:2025-2030 年按類型、應用、最終用途、地區和細分市場進行的預測 輻照設備市場:現況分析與預測(2024-2032)

輻照設備市場:現況分析與預測(2024-2032)