|

市場調查報告書

商品編碼

1773454

材料減縮劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Material Shrinkage-Reducing Agents Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

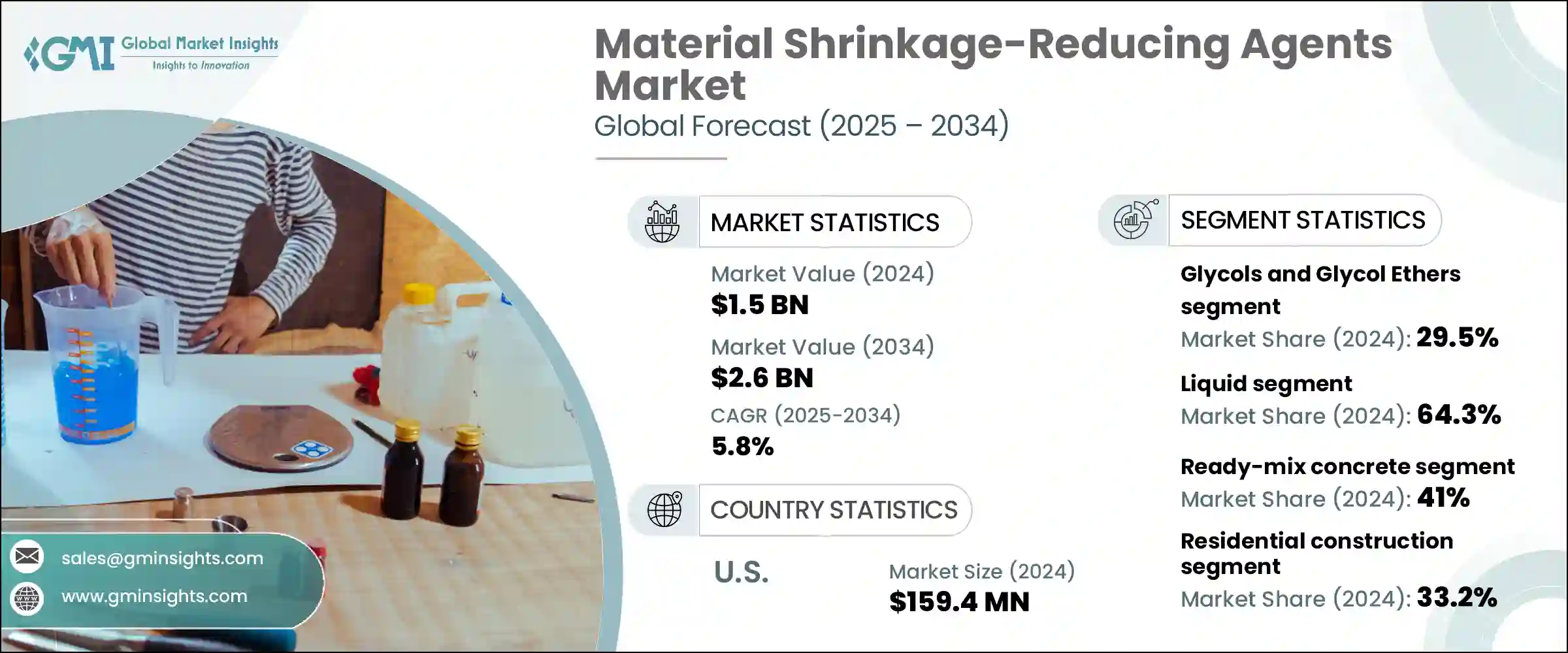

2024年,全球材料減縮劑市場規模達15億美元,預計2034年將以5.8%的複合年成長率成長,達到26億美元。隨著建築標準不斷發展,更加重視結構彈性和長期性能,減縮劑 (SRA) 已從簡單的添加劑轉變為高性能混凝土混合料中不可或缺的成分。這些化學溶液在減少收縮裂縫、維持混凝土強度和增強耐久性方面發揮關鍵作用。過去,人們透過調整混合比來應對收縮問題,但如今,基礎設施和住宅建築對先進材料的需求正推動全球市場對SRA的採用。

在快速工業化和城市發展的推動下,亞太地區的成長尤其顯著。人們對永續性的日益重視以及向下一代外加劑的轉變,正在加速SRA的應用,尤其是在大型專案中,防裂對於降低長期維護成本至關重要。隨著混凝土應用在隧道、高層建築和模組化設計等領域的不斷多樣化,SRA越來越被視為延長結構壽命並在環境應力和荷載下保持性能的關鍵。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 15億美元 |

| 預測值 | 26億美元 |

| 複合年成長率 | 5.8% |

2024年,液體SRAs市場佔64.3%,由於其易於與混凝土混合料融合,展現出強勁成長動能。其高效的分散性以及與預拌混凝土應用的兼容性,使其成為基礎設施和大量住宅建築的首選。這些助劑能夠持續減少收縮,廣泛應用於現場和工廠環境,包括商業房地產和公共部門工程。

2024年,預拌混凝土佔整個市場的41%,成為SRA的主要消費領域。這些添加劑對於降低固化過程中出現表面裂縫和內部應力的風險至關重要,尤其是在城市住宅和商業開發項目中使用的預拌混凝土系統中。在預製混凝土領域,SRA對於維持尺寸精度和防止因材料收縮而導致的組裝錯位至關重要。

美國材料減縮劑市場佔85%的市場佔有率,價值1.594億美元。其領先地位源自於強勁的基礎設施建設活動以及對永續建築實踐的日益重視。政府主導的公共資產修復投資,例如橋樑、政府大樓和交通基礎設施,持續推動對耐用抗裂混凝土的需求。這促使承包商廣泛採用減縮劑,以延長混凝土結構的使用壽命,同時最大限度地降低維修和保養成本。美國致力於環保建築實踐,也加速了先進外加劑技術的轉變。

材料減縮劑市場的知名公司包括巴斯夫歐洲公司 (BASF SE)、馬貝集團 (Mapei SpA)、基仕伯應用技術公司(聖戈班)、富斯樂國際有限公司 (Fosroc International Ltd.) 和西卡股份公司 (Sika AG)。材料減縮劑市場的公司正在利用創新、區域擴張和永續性來鞏固其市場地位。領先的公司專注於開發符合綠色建築認證並能提高結構耐久性的環保減縮劑 (SRA)。與建築公司和基礎設施開發商的策略聯盟使這些公司能夠將其產品直接嵌入長期專案中。研發投資旨在提高配方效率和在不同環境條件下的性能。許多參與者也在亞太等高成長地區擴大產能,以滿足不斷成長的城市建設需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 高性能混凝土的需求不斷成長

- 增加基礎建設項目

- 越來越重視耐久性和防裂

- 外加劑配方的技術進步

- 產業陷阱與挑戰

- 原物料價格波動

- 嚴格的監管要求

- 技術專長要求

- 來自替代收縮控制方法的競爭

- 市場機會

- 環保減縮劑的開發

- 新興市場的擴張

- 與智慧混凝土技術的整合

- 應用於專業建築領域

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 液體減縮劑

- 粉末減縮劑

- 其他

第6章:市場估計與預測:按化學複合材料,2021 - 2034 年

- 主要趨勢

- 聚醚

- 多元醇

- 乙二醇和乙二醇醚

- 界面活性劑

- 其他

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 預拌混凝土

- 預製混凝土

- 自密實混凝土

- 高性能混凝土

- 噴射混凝土

- 砂漿和灌漿

- 其他

第8章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 住宅建築

- 商業建築

- 基礎建設發展

- 工業建築

- 水圍結構

- 其他

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- BASF SE

- Cementaid International Group

- Cemex SAB de CV

- Euclid Chemical Company

- Fosroc International Ltd.

- GCP Applied Technologies (now part of Saint-Gobain)

- Imerys SA

- Mapei SpA

- Nippon Shokubai Co., Ltd.

- RPM International Inc.

- Sika AG

- Sobute New Material Co., Ltd.

- WR Grace & Co. (now part of Standard Industries)

The Global Material Shrinkage-Reducing Agents Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 2.6 billion by 2034. As construction standards evolve to prioritize structural resilience and long-term performance, shrinkage-reducing agents (SRAs) have transitioned from simple additives to essential components in high-performance concrete mixes. These chemical solutions play a critical role in minimizing shrinkage-related cracks, preserving concrete strength, and enhancing durability. Previously, shrinkage concerns were managed by altering mix ratios, but today's demand for advanced materials in infrastructure and residential construction is fueling SRA adoption across global markets.

This growth is especially prominent in the Asia-Pacific region, driven by rapid industrialization and urban development. Rising emphasis on sustainability and the shift toward next-generation admixtures are accelerating the use of SRAs, particularly in large-scale projects where crack prevention is essential to lower long-term maintenance costs. As concrete applications continue to diversify across tunnels, high-rise structures, and modular designs, SRAs are increasingly seen as key to extending structural life while maintaining performance under environmental stress and load.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.6 Billion |

| CAGR | 5.8% |

The liquid SRAs segment made up 64.3% share in 2024, showing strong momentum due to their ease of integration with concrete mixtures. Their effective dispersion and compatibility with ready-mix applications make them a top choice in infrastructure and high-volume residential construction. These agents ensure consistent shrinkage mitigation and are widely adopted in both on-site and factory settings, including commercial real estate and public sector works.

Ready-mix concrete contributed 41% to the total market in 2024, standing out as a major consumer of SRAs. These agents are essential in reducing the risk of surface cracks and internal stress during the curing process, especially in ready-mix systems used in urban housing and commercial developments. In the precast concrete segment, SRAs have become crucial for maintaining dimensional accuracy and preventing assembly misalignments, which can arise due to material contraction.

U.S. Material Shrinkage-Reducing Agents Market held an 85% share, valued at USD 159.4 million. Its leadership position stems from robust infrastructure activity and increased focus on sustainable construction practices. Government-led investments in rehabilitating public assets such as bridges, government complexes, and transport infrastructure continue to drive demand for durable, crack-resistant concrete. This has led to the widespread adoption of SRAs among contractors seeking to extend the lifecycle of concrete structures while minimizing repair and upkeep costs. The country's commitment to eco-conscious building practices has also accelerated the shift toward advanced admixture technologies.

Prominent companies operating in the Material Shrinkage-Reducing Agents Market include BASF SE, Mapei S.p.A., GCP Applied Technologies (Saint-Gobain), Fosroc International Ltd., and Sika AG. Companies in the material shrinkage-reducing agents market are leveraging innovation, regional expansion, and sustainability to secure their market positions. Leading firms are focusing on developing eco-friendly SRAs that comply with green building certifications and enhance structural durability. Strategic alliances with construction firms and infrastructure developers allow these companies to embed their products directly into long-term projects. R&D investments are targeted toward improving formulation efficiency and performance under varied environmental conditions. Many players are also expanding production capacities in high-growth regions like Asia-Pacific to meet rising urban construction demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Chemical Composites

- 2.2.4 Application

- 2.2.5 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for high-performance concrete

- 3.2.1.2 Increasing infrastructure development projects

- 3.2.1.3 Rising focus on durability and crack prevention

- 3.2.1.4 Technological advancements in admixture formulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price fluctuations

- 3.2.2.2 Stringent regulatory requirements

- 3.2.2.3 Technical expertise requirements

- 3.2.2.4 Competition from alternative shrinkage control methods

- 3.2.3 Market opportunities

- 3.2.3.1 Development of eco-friendly shrinkage-reducing agents

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Integration with smart concrete technologies

- 3.2.3.4 Application in specialized construction segments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Liquid shrinkage-reducing agents

- 5.3 Powder shrinkage-reducing agents

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Chemical Composites, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyethers

- 6.3 Polyalcohols

- 6.4 Glycols and glycol ethers

- 6.5 Surfactants

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Ready-mix concrete

- 7.3 Precast concrete

- 7.4 Self-consolidating concrete

- 7.5 High-performance concrete

- 7.6 Shotcrete

- 7.7 Mortars and grouts

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.3 Commercial construction

- 8.4 Infrastructure development

- 8.5 Industrial construction

- 8.6 Water containment structures

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 BASF SE

- 10.2 Cementaid International Group

- 10.3 Cemex S.A.B. de C.V.

- 10.4 Euclid Chemical Company

- 10.5 Fosroc International Ltd.

- 10.6 GCP Applied Technologies (now part of Saint-Gobain)

- 10.7 Imerys S.A.

- 10.8 Mapei S.p.A.

- 10.9 Nippon Shokubai Co., Ltd.

- 10.10 RPM International Inc.

- 10.11 Sika AG

- 10.12 Sobute New Material Co., Ltd.

- 10.13 W. R. Grace & Co. (now part of Standard Industries)

建築潤滑劑市場:按產品類型、設備類型、應用和銷售管道分類的全球市場預測,2026-2032年

建築潤滑劑市場:按產品類型、設備類型、應用和銷售管道分類的全球市場預測,2026-2032年 先進工業潤滑油市場預測至2034年:按產品類型、基礎油、形態、通路、應用、最終用戶和地區分類的全球分析按基油類型、最終用途、應用和銷售管道分類的柱塞潤滑劑顆粒市場,全球預測,2026-2032年

先進工業潤滑油市場預測至2034年:按產品類型、基礎油、形態、通路、應用、最終用戶和地區分類的全球分析按基油類型、最終用途、應用和銷售管道分類的柱塞潤滑劑顆粒市場,全球預測,2026-2032年 無氧潤滑劑市場規模、佔有率和成長分析:按產品類型、配方類型、應用、終端用戶產業和地區分類-2026-2033年產業預測

無氧潤滑劑市場規模、佔有率和成長分析:按產品類型、配方類型、應用、終端用戶產業和地區分類-2026-2033年產業預測 2026年全球建築潤滑劑市場報告按類型、形式、通路、應用和最終用途產業分類的建築矽烷改質聚合物市場-全球預測(2026-2032年)摩托車乾式鏈條潤滑油市場:按配方、應用、通路和最終用戶分類-2026-2032年全球預測潤滑油增黏劑市場:依樹脂類型、形態、應用、終端用戶產業及通路分類,全球預測(2026-2032年)紡織機械潤滑劑市場:依產品類型、添加劑類型、黏度等級、應用和終端用戶產業分類,全球預測,2026-2032年自行車濕式鏈條潤滑劑市場:依產品類型、應用、通路和最終用戶分類-2026-2032年全球預測

2026年全球建築潤滑劑市場報告按類型、形式、通路、應用和最終用途產業分類的建築矽烷改質聚合物市場-全球預測(2026-2032年)摩托車乾式鏈條潤滑油市場:按配方、應用、通路和最終用戶分類-2026-2032年全球預測潤滑油增黏劑市場:依樹脂類型、形態、應用、終端用戶產業及通路分類,全球預測(2026-2032年)紡織機械潤滑劑市場:依產品類型、添加劑類型、黏度等級、應用和終端用戶產業分類,全球預測,2026-2032年自行車濕式鏈條潤滑劑市場:依產品類型、應用、通路和最終用戶分類-2026-2032年全球預測