|

市場調查報告書

商品編碼

1773453

汽車壓電燃油噴射器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Piezoelectric Fuel Injectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024年,全球汽車壓電燃油噴射器市場規模達7.463億美元,預計年複合成長率將達5.3%,2034年將達12億美元。 CRDI和GDI等先進引擎技術的日益普及,以及全球汽車排放法規的日益嚴格,推動了該市場的成長。這些噴射器能夠快速且極為精確地輸送燃油,從而顯著提高燃燒效率並減少污染物排放。

在環境標準嚴格的地區,壓電式噴油嘴正穩定取代傳統的電磁閥噴油嘴。它們與智慧電子控制單元和先進的診斷系統整合,能夠即時調節燃油流量,從而最佳化引擎性能並減少顆粒物排放。向更清潔的出行解決方案的轉變也加速了對這些高精度組件的需求,因為它們能夠在所有類型車輛平台的內燃機應用中提供更強大的控制力和更高的效率。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.463億美元 |

| 預測值 | 12億美元 |

| 複合年成長率 | 5.3% |

壓電噴油嘴透過在單一燃燒循環內實現多次超快速燃油噴射,重新定義了引擎管理。這種控制水平有助於工程師以無與倫比的精度微調空燃比,從而提高燃油效率並顯著降低排放。隨著各國實施歐7、BS-VI Stage II和EPA Tier 3等更嚴格的排放法規,這些特性變得越來越重要。汽車產業正在快速發展,基於壓電的系統能夠突破電磁閥噴油嘴的局限性,尤其是在需要更快反應時間和更高噴射射精度的場景中。

2024年,乘用車市場佔據主導地位,貢獻了70%的市場佔有率,預計到2034年將以5.5%的複合年成長率成長。這種主導地位源自於全球轎車、輕型卡車和多用途車的高產銷量。亞洲、歐洲和北美等地區嚴格的排放控制措施正推動製造商在這些車型中採用先進的燃油噴射系統。壓電式燃油噴射器有助於滿足監管門檻,同時提升性能和燃油經濟性,滿足消費者對動力和環保意識的期望。其在混合動力和插電式混合動力平台上的應用正在不斷擴展,在這些平台上,快速的開關循環和啟動停止操作需要快速高效響應的噴射器——而壓電技術正是能夠始終如一地提供這些特性。

汽油車市場佔46%的佔有率,預計2025年至2034年間的複合年成長率為5.7%。隨著各大洲的監管機構紛紛限制輕型車輛的排放,汽油引擎因其顆粒物和氮氧化物排放量相對柴油引擎較低而更具吸引力。汽車製造商正傾向於採用配備壓電噴油嘴的汽油直噴系統,以滿足性能目標和排放基準。汽油引擎因其重量輕、運行更安靜、生產成本更低而備受青睞,壓電噴油器可幫助這些引擎改善燃燒並提升油門響應,從而鞏固其在汽油引擎市場的關鍵部件地位。

亞太地區汽車壓電燃油噴射器市場佔67%的市場佔有率,產值達1.995億美元。中國龐大的內燃機汽車產量和日益嚴格的環保法規正在推動高精度噴射技術的廣泛應用。中國採用先進的排放標準,進一步加強了對清潔燃燒的重視,從而對壓電噴射系統產生了強勁的需求。此外,英飛凌、京瓷、安波福和西門子等一級零件製造商正在加強在該地區的業務力度,與當地企業合作,根據區域市場需求客製化解決方案。這些合作致力於最佳化商用和乘用車應用的噴射器性能,確保在高壓閾值下的耐用性和效率,同時保持具有競爭力的成本。

積極影響全球汽車壓電燃油噴射器市場的知名公司包括京瓷、大陸集團、西門子、英飛凌、日立Astemo Indiana、安波福、羅伯特·博世、電裝、NGK火星塞公司和村田製作所。這些公司正在不斷創新和投資,以跟上行業不斷發展的燃油輸送要求和排放法規。

汽車壓電式燃油噴射器市場的主要製造商正專注於幾個戰略領域,以建立強大的競爭地位。首先,他們大力投資研發,以改善噴射器的速度、反應精度和燃油霧化效果,以實現更好的排放控制和燃燒效率。其次,他們正在與汽車原始設備製造商合作,開發針對汽油直噴和混合動力系統最佳化的專用噴射器。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- GDI 和 CRDI 引擎的採用率不斷上升

- 壓電材料的技術進步

- 高檔豪華汽車細分市場的成長

- 更嚴格的排放法規

- 原始設備製造商及一級供應商增加研發投資

- 產業陷阱與挑戰

- 壓電噴油嘴成本高

- 改良的電磁噴油嘴的競爭

- 市場機會

- 混合動力系統的採用日益增多

- 商用車柴油引擎最佳化

- 汽油直噴 (GDI) 引擎的廣泛轉變

- 數位引擎管理和人工智慧整合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

第6章:市場估計與預測:按燃料,2021 - 2034 年

- 主要趨勢

- 汽油

- 柴油引擎

- 其他

第7章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第8章:市場估計與預測:按推進方式,2021 - 2034 年

- 主要趨勢

- 冰

- 混合

第9章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 直接噴射(DI)

- 共軌直噴(CRDI)

- 汽油直噴(GDI)

- 進氣道燃油噴射 (PFI)

第10章:市場估計與預測:依工作壓力範圍,2021 - 2034 年

- 主要趨勢

- 低壓(<200 巴)

- 中壓(200–1000 bar)

- 高壓(>1000 bar)

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳新銀行

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第12章:公司簡介

- Aptiv

- Continental

- Delphi Technologies

- Denso Corporation

- Edelbrock LLC

- Fuzhou Ruida Machinery

- GB Remanufacturing

- Hitachi Astemo Indiana

- Infineon

- Keihin

- KYOCERA

- Magneti Marelli Parts and Services.

- Mikuni American

- Murata Manufacturing

- Robert Bosch

- Siemens

- Stanadyne

- Valley Fuel Injection & Turbo

- Woodward

- WUZETEM

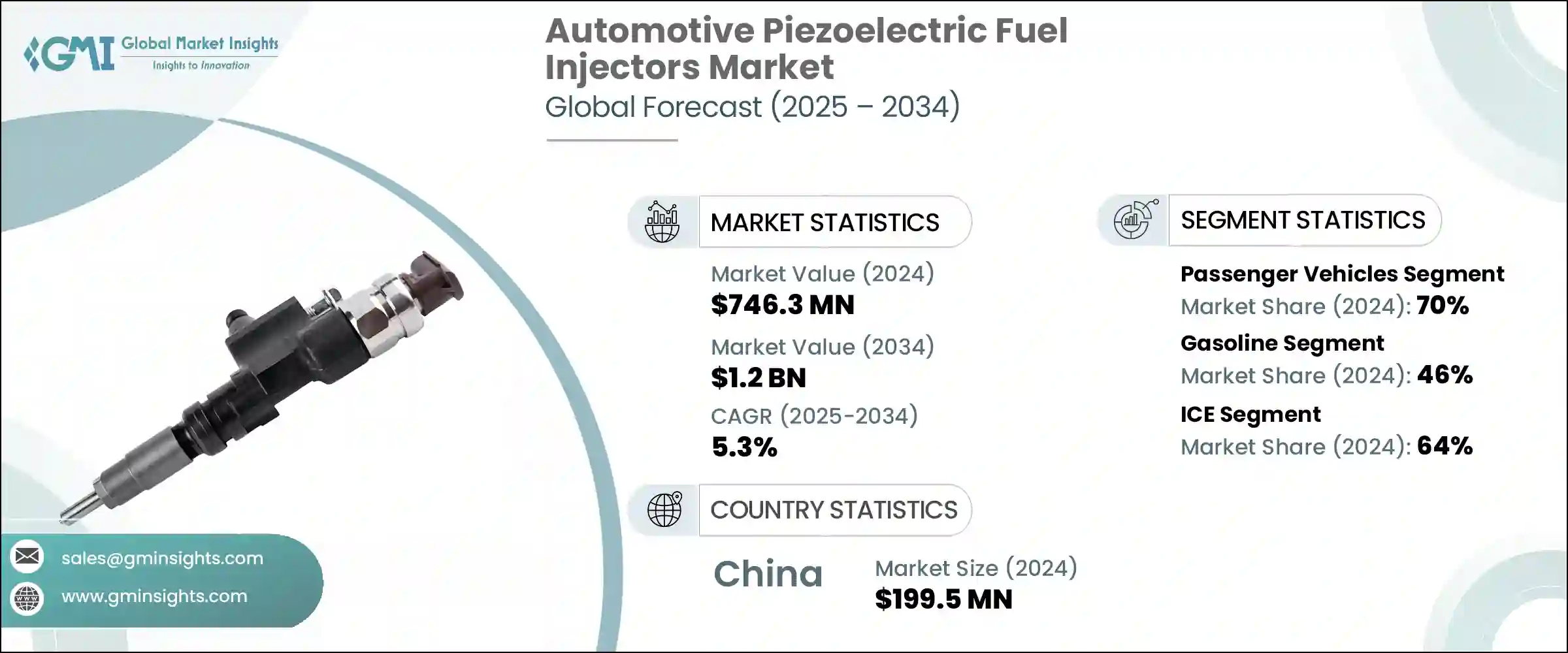

The Global Automotive Piezoelectric Fuel Injectors Market was valued at USD 746.3 million in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 1.2 billion by 2034. Growth in this market is being fueled by the increasing implementation of advanced engine technologies such as CRDI and GDI, alongside stricter global regulations around vehicle emissions. These injectors allow for rapid and extremely precise fuel delivery, which contributes significantly to enhanced combustion efficiency and reduced pollutants.

Piezoelectric injectors are steadily replacing traditional solenoid types in regions with aggressive environmental standards. Their integration with smart electronic control units and advanced diagnostics enables real-time adjustment of fuel flow, allowing for optimized engine performance and fewer particulate emissions. The shift toward cleaner mobility solutions is also accelerating the need for these high-precision components, as they offer greater control and efficiency in internal combustion applications across all types of vehicle platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $746.3 Million |

| Forecast Value | $1.2 Billion |

| CAGR | 5.3% |

Piezoelectric injectors are redefining engine management by enabling multiple ultra-fast fuel injections within a single combustion cycle. This level of control helps engineers fine-tune the air-fuel mixture with unmatched accuracy, boosting fuel efficiency and significantly lowering emissions. These attributes are becoming increasingly important as countries implement tighter regulations like Euro 7, BS-VI Stage II, and EPA Tier 3. The automotive sector is evolving rapidly, with piezo-based systems positioned to address the limitations of solenoid injectors, especially in scenarios demanding faster response times and higher injection precision.

The passenger vehicles segment led the market in 2024, contributing 70% share, and is projected to grow at a CAGR of 5.5% through 2034. This dominance stems from the high global production and sales volumes of cars, light trucks, and utility vehicles. Stringent emission controls in regions like Asia, Europe, and North America are pushing manufacturers toward incorporating advanced fuel injection systems in these vehicle classes. Piezoelectric fuel injectors help meet regulatory thresholds while improving performance and economy, aligning with consumer expectations for both power and environmental consciousness. Their application is expanding in hybrid and plug-in hybrid platforms, where rapid on-off cycles and start-stop operation demand injectors that respond quickly and efficiently-qualities that piezo technology delivers consistently.

The gasoline vehicle segment held a 46% share, and it is projected to grow at a CAGR of 5.7% between 2025 and 2034. As regulatory bodies across multiple continents move to restrict emissions from light-duty vehicles, gasoline engines are becoming more attractive due to their relatively lower particulate and nitrogen oxide output compared to diesel. Automotive manufacturers are leaning into gasoline direct injection systems, enhanced with piezoelectric injectors, to meet both performance goals and emission benchmarks. With gasoline engines favored for their lighter weight, quieter operation, and lower cost of production, piezo injectors help these engines deliver improved combustion and better throttle response, securing their position as a key component in the gasoline segment.

Asia Pacific Automotive Piezoelectric Fuel Injectors Market held a 67% share, generating USD 199.5 million. The country's massive internal combustion vehicle output and increasingly rigorous environmental mandates are driving the widespread integration of high-precision injection technology. China's adoption of advanced emission standards has intensified the focus on cleaner combustion, creating a strong demand for piezoelectric injector systems. Additionally, Tier-1 component manufacturers such as Infineon, KYOCERA, Aptiv, and Siemens are intensifying their efforts in the region by collaborating with domestic firms to tailor solutions for regional market needs. These partnerships focus on optimizing injector performance for both commercial and passenger applications, ensuring durability and efficiency at elevated pressure thresholds while maintaining competitive costs.

Notable companies actively shaping the Global Automotive Piezoelectric Fuel Injectors Market include KYOCERA, Continental, Siemens, Infineon, Hitachi Astemo Indiana, Aptiv, Robert Bosch, Denso, NGK Spark Plug Co, and Murata Manufacturing. These players are innovating and investing to keep pace with the industry's evolving fuel delivery requirements and emissions legislation.

Major manufacturers in the automotive piezoelectric fuel injectors market are focusing on several strategic areas to build a strong competitive position. First, they are investing heavily in research and development to refine injector speed, response precision, and fuel atomization, enabling better emissions control and combustion efficiency. Second, collaborations with vehicle OEMs are being formed to develop application-specific injectors optimized for gasoline direct injection and hybrid systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Fuel type

- 2.2.4 Sales channel

- 2.2.5 Propulsions

- 2.2.6 Technology

- 2.2.7 Operating pressure range

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of GDI and CRDI engines

- 3.2.1.2 Technological advancements in Piezo materials

- 3.2.1.3 Growth of premium and luxury vehicle segments

- 3.2.1.4 Stricter emission regulations

- 3.2.1.5 Increased R&D investments by OEMs and Tier-1 suppliers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of piezoelectric injectors

- 3.2.2.2 Competition from improved solenoid injectors

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of hybrid powertrains

- 3.2.3.2 Diesel engine optimization in commercial vehicles

- 3.2.3.3 The widespread shift to gasoline direct injection (GDI) engines

- 3.2.3.4 Digital engine management and AI integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($ Mn, units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCV)

- 5.3.2 Medium commercial vehicles (MCV)

- 5.3.3 Heavy commercial vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.1.1 Gasoline

- 6.1.2 Diesel

- 6.1.3 Others

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 Hybrid

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Direct injection (DI)

- 9.3 Common rail direct injection (CRDI)

- 9.4 Gasoline direct injection (GDI)

- 9.5 Port fuel injection (PFI)

Chapter 10 Market Estimates & Forecast, By Operating Pressure Range, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 Low pressure (<200 bar)

- 10.3 Medium pressure (200–1000 bar)

- 10.4 High pressure (>1000 bar)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Aptiv

- 12.2 Continental

- 12.3 Delphi Technologies

- 12.4 Denso Corporation

- 12.5 Edelbrock LLC

- 12.6 Fuzhou Ruida Machinery

- 12.7 GB Remanufacturing

- 12.8 Hitachi Astemo Indiana

- 12.9 Infineon

- 12.10 Keihin

- 12.11 KYOCERA

- 12.12 Magneti Marelli Parts and Services.

- 12.13 Mikuni American

- 12.14 Murata Manufacturing

- 12.15 Robert Bosch

- 12.16 Siemens

- 12.17 Stanadyne

- 12.18 Valley Fuel Injection & Turbo

- 12.19 Woodward

- 12.20 WUZETEM

汽車噴油嘴市場 - 全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、技術、車輛類型、地區和競爭格局分類,2021-2031年汽車氫氣噴射器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、需求類別、流量、地區和競爭格局分類,2021-2031年)

汽車噴油嘴市場 - 全球產業規模、佔有率、趨勢、機會、預測:按燃料類型、技術、車輛類型、地區和競爭格局分類,2021-2031年汽車氫氣噴射器市場 - 全球產業規模、佔有率、趨勢、機會及預測(按車輛類型、需求類別、流量、地區和競爭格局分類,2021-2031年) 汽車燃油噴射市場規模、佔有率和成長分析(按燃油類型、車輛類型、噴油嘴類型、組件、分銷管道和地區分類)-2026-2033年產業預測

汽車燃油噴射市場規模、佔有率和成長分析(按燃油類型、車輛類型、噴油嘴類型、組件、分銷管道和地區分類)-2026-2033年產業預測 汽車噴油嘴市場規模、佔有率和成長分析(按燃料類型、銷售管道、噴嘴孔數、噴嘴類型和地區分類)-2026-2033年產業預測

汽車噴油嘴市場規模、佔有率和成長分析(按燃料類型、銷售管道、噴嘴孔數、噴嘴類型和地區分類)-2026-2033年產業預測 燃油噴射設備市場-2025-2030年預測

燃油噴射設備市場-2025-2030年預測 氫氣噴射器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

氫氣噴射器:全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 2025年全球汽車燃油噴射系統市場報告汽車燃油噴射器市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、燃料、車輛類型、銷售管道、地區和競爭細分,2020-2030 年

2025年全球汽車燃油噴射系統市場報告汽車燃油噴射器市場-全球產業規模、佔有率、趨勢、機會和預測,按類型、燃料、車輛類型、銷售管道、地區和競爭細分,2020-2030 年 汽車噴嘴的全球市場:各車輛類型,各燃料類型,各技術類型,各地區,機會,預測,2018年~2032年

汽車噴嘴的全球市場:各車輛類型,各燃料類型,各技術類型,各地區,機會,預測,2018年~2032年 汽車燃油噴射器市場機會、成長動力、產業趨勢分析及 2025 年至 2034 年預測

汽車燃油噴射器市場機會、成長動力、產業趨勢分析及 2025 年至 2034 年預測