|

市場調查報告書

商品編碼

1773452

運動感測器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Motion Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

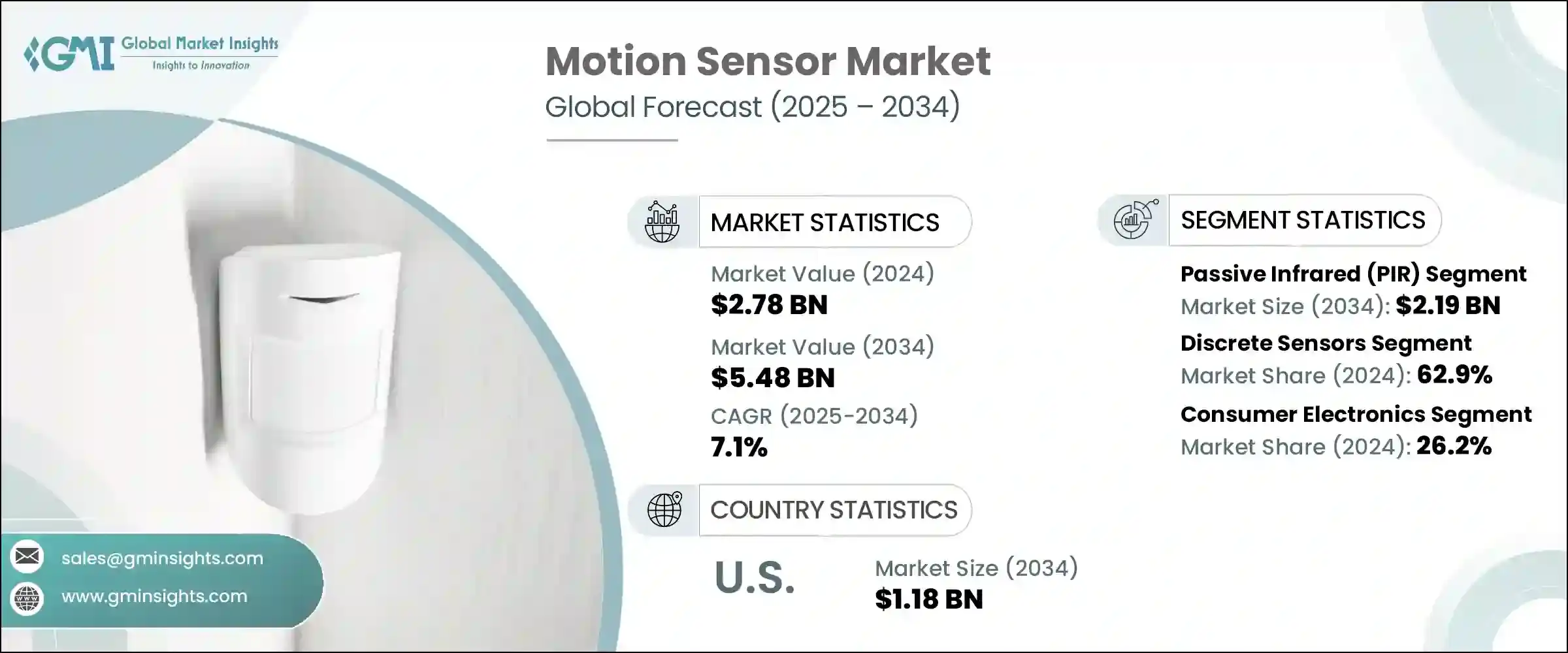

2024年,全球運動感測器市場規模達27.8億美元,預計到2034年將以7.1%的複合年成長率成長,達到54.8億美元。智慧電子產品和物聯網生活環境的需求日益成長,推動著各行各業的成長。運動感測器如今已成為各行各業創新的核心,尤其是在智慧家庭自動化領域,偵測未經授權的行動或環境風險至關重要。它們的用途遠不止照明或警報,它們在建立以安全性、效率和用戶響應能力為重點的互聯系統方面發揮著重要作用。隨著互聯生態系的蓬勃發展,消費者對更智慧、更快速、更安全的科技賦能空間的需求也日益成長。

該市場的一個重要成長動力是現代車輛中運動感測器的日益普及。汽車安全正在經歷快速變革,越來越多的汽車配備了旨在預防事故的先進系統。這些安全應用,包括車道導引、碰撞警報和盲點監控,都嚴重依賴高精度感測器才能有效運作。運動感測單元提供的即時資料使這些智慧車輛系統能夠以更高的控制力和精度自主運行,尤其是在半自動駕駛功能不斷發展的背景下。此類運動技術與車輛框架的整合反映了自動化和駕駛輔助的更深層趨勢。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 27.8億美元 |

| 預測值 | 54.8億美元 |

| 複合年成長率 | 7.1% |

預計到2034年,微波感測器市場將以8.8%的複合年成長率成長,這得益於其在嚴苛多變環境中的高效性。這些感測器在能見度低和可穿透物理障礙的情況下也能提供穩定的運動偵測,性能優於傳統技術。由於微波運動感測器無論在何種光照或天氣條件下都能提供準確可靠的性能,因此在安防、工業和交通基礎設施領域正日益普及。其遠距離檢測能力以及與複雜系統的兼容性使其成為下一代安全應用和智慧感測裝置的理想選擇。

離散運動感測器市場在2024年佔據了62.9%的市場佔有率,這得益於其在照明、安防和工業控制等日常自動化系統中的廣泛應用。其簡潔的架構和靈活的設計使其成為成本敏感型專案和舊基礎設施改造的理想選擇。這些感測器也因其易於維護和與現有硬體平台的交叉相容性而備受青睞。儘管整合系統正在快速發展,但在注重簡潔性和成本效益的領域,尤其是在發展中或轉型期市場,離散感測器仍將佔據主導地位。

預計到2034年,美國運動感測器市場規模將達到11.8億美元。在美國,人們對家庭自動化、基礎設施升級和連網汽車日益成長的興趣正在推動巨大的需求。運動感測技術不僅應用於消費性電子產品,還應用於可靠性和性能至關重要的關鍵基礎設施網路。隨著數位化現代化的加速,這些設備在公用事業、交通系統和智慧能源管理中實現自動化回應方面發揮著至關重要的作用。政府正在努力升級老舊基礎設施,這進一步凸顯了運動感測器在監控、追蹤和保護實體資產方面的重要性。

全球運動感測器市場的領導公司包括德州儀器公司、霍尼韋爾國際公司、博世感測器技術有限公司和意法半導體。為了提升市場地位,運動感測器製造商正在實施各種策略措施。主要參與者正在投資開發微型化、節能型感測器,這些感測器針對穿戴式技術、汽車應用和物聯網系統進行了最佳化。加強全球分銷網路和進入新興市場也是利用日益成長的城市化進程的重點。與系統整合商和原始設備製造商 (OEM) 建立策略聯盟有助於加速感測器技術在智慧型裝置中的應用。此外,各公司正在優先研究混合感測器設計,將微波、紅外線和振動等多種檢測方法結合到緊湊的多功能單元中。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 智慧消費性電子產品需求不斷成長

- 工業應用自動化的成長

- 物聯網智慧家庭的擴展

- 汽車安全系統的採用率不斷提高

- 穿戴式裝置和健身追蹤器的普及

- 產業陷阱與挑戰

- 先進運動感測器技術成本高昂

- 智慧型應用中的隱私和資料安全問題

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理分佈比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:依技術,2021-2034 年

- 主要趨勢

- 被動紅外線(PIR)

- 超音波

- 微波

- 基於攝影機

- 振動感測器

- 其他

第6章:市場估計與預測:按整合度,2021-2034 年

- 主要趨勢

- 離散感測器

- 整合感測器

第7章:市場估計與預測:依最終用途,2021-2034

- 主要趨勢

- 消費性電子產品

- 汽車

- 安防與監控

- 智慧家庭和建築

- 工業的

- 衛生保健

- 零售

- 其他

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Allegro MicroSystems, Inc.

- Analog Devices, Inc.

- Bosch Sensortec GmbH

- Elmos Semiconductor SE

- Honeywell International Inc.

- InvenSense

- KEMET Corporation

- Littelfuse, Inc.

- NXP Semiconductors

- Panasonic Holdings Corporation

- Schneider Electric

- Siemens AG

- STMicroelectronics

- TE Connectivity

- Texas Instruments Incorporated

- Vishay Intertechnology, Inc.

The Global Motion Sensor Market was valued at USD 2.78 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 5.48 billion by 2034. Growth across industry is being propelled by increasing demand for smart electronics and IoT-powered living environments. Motion sensors are now central to innovations across a wide spectrum of industries, especially in smart home automation where detecting unauthorized movement or environmental risks is essential. Their use extends far beyond just lighting or alarms-they're instrumental in building interconnected systems that prioritize security, efficiency, and user responsiveness. With connected ecosystems gaining traction, the need for motion-based sensing solutions in homes, offices, and commercial buildings is only expanding, driven by consumers who demand smarter, faster, and safer tech-enabled spaces.

An important growth driver within this market is the increasing deployment of motion sensors in modern vehicles. Automotive safety is undergoing a rapid transformation with more cars incorporating advanced systems designed to prevent accidents. These safety applications, including lane guidance, collision alerts, and blind-spot monitoring, rely heavily on high-precision sensors to operate effectively. Real-time data provided by motion sensing units allows these intelligent vehicle systems to function autonomously with greater control and accuracy, especially as semi-autonomous features continue to evolve. The integration of such motion technology into vehicle frameworks reflects a deeper trend toward automation and driver assistance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.78 Billion |

| Forecast Value | $5.48 billion |

| CAGR | 7.1% |

The microwave sensor segment is expected to grow at a CAGR of 8.8% through 2034, driven by its effectiveness in demanding and variable environments. These sensors outperform conventional technologies by offering stable motion detection in poor visibility conditions and through physical barriers. Because they can deliver accurate and reliable performance regardless of lighting or weather, microwave motion sensors are gaining ground in security, industrial, and transport infrastructure. Their capacity for long-range detection and compatibility with complex systems has made them highly sought-after for next-generation safety applications and intelligent sensing installations.

Discrete motion sensors segment accounted for a 62.9% share in 2024, supported by widespread use in everyday automation systems such as lighting, security, and industrial controls. Their straightforward architecture and flexible design make them ideal for cost-sensitive projects and retrofitting older infrastructure. These sensors are also preferred for their ease of maintenance and cross-compatibility with existing hardware platforms. While integrated systems are advancing rapidly, discrete sensors continue to dominate where simplicity and cost-effectiveness are paramount, especially in developing or transitional markets.

United States Motion Sensor Market is expected to generate USD 1.18 billion by 2034. In the U.S., expanding interest in home automation, infrastructure upgrades, and connected vehicles is driving significant demand. Motion sensing technology is being deployed not just in consumer gadgets, but also across critical infrastructure networks where reliability and performance are essential. As digital modernization accelerates, these devices are proving vital in enabling automated responses across utilities, transportation systems, and smart energy management. Government efforts to upgrade outdated infrastructure further underscore the importance of motion sensors in monitoring, tracking, and securing physical assets.

Leading companies in the Global Motion Sensor Market include Texas Instruments Incorporated, Honeywell International Inc., Bosch Sensortec GmbH, and STMicroelectronics. To enhance their market position, motion sensor manufacturers are implementing a variety of strategic initiatives. Key players are investing in the development of miniaturized, power-efficient sensors optimized for wearable tech, automotive applications, and IoT-enabled systems. Strengthening global distribution networks and entering emerging markets are also high on the agenda to capitalize on growing urbanization. Strategic alliances with system integrators and OEMs help foster faster adoption of sensor technology into smart devices. Additionally, companies are prioritizing research on hybrid sensor designs that combine multiple detection methods-such as microwave, infrared, and vibration-into compact, multifunctional units.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.3 Technology type

- 2.4 Integration level type

- 2.5 End use type

- 2.6 Regional

- 2.7 TAM Analysis, 2025-2034 (USD Billion)

- 2.8 CXO Perspectives: Strategic imperatives

- 2.8.1 Executive decision points

- 2.8.2 Critical Success Factors

- 2.9 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for smart consumer electronics

- 3.2.1.2 Growth in automation across industrial applications

- 3.2.1.3 Expansion of IoT-enabled smart homes

- 3.2.1.4 Increased adoption in automotive safety systems

- 3.2.1.5 Proliferation of wearable devices and fitness trackers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced motion sensor technologies

- 3.2.2.2 Privacy and data security concerns in smart applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.11 Consumer Sentiment Analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Passive infrared (PIR)

- 5.3 Ultrasonic

- 5.4 Microwave

- 5.5 Camera-based

- 5.6 Vibration sensors

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Integration Level, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Discrete sensors

- 6.3 Integrated sensors

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Consumer electronics

- 7.3 Automotive

- 7.4 Security & surveillance

- 7.5 Smart homes & buildings

- 7.6 Industrial

- 7.7 Healthcare

- 7.8 Retail

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allegro MicroSystems, Inc.

- 9.2 Analog Devices, Inc.

- 9.3 Bosch Sensortec GmbH

- 9.4 Elmos Semiconductor SE

- 9.5 Honeywell International Inc.

- 9.6 InvenSense

- 9.7 KEMET Corporation

- 9.8 Littelfuse, Inc.

- 9.9 NXP Semiconductors

- 9.10 Panasonic Holdings Corporation

- 9.11 Schneider Electric

- 9.12 Siemens AG

- 9.13 STMicroelectronics

- 9.14 TE Connectivity

- 9.15 Texas Instruments Incorporated

- 9.16 Vishay Intertechnology, Inc.

消費性動作感測器市場:按技術、產品、安裝類型、應用、最終用戶和分銷管道分類-2026年至2032年全球預測

消費性動作感測器市場:按技術、產品、安裝類型、應用、最終用戶和分銷管道分類-2026年至2032年全球預測 2026年全球動作感測器市場報告2026年全球穿戴式裝置人機介面(HMI)感測器市場報告住宅PIR人體感應器市場按產品類型、電源、安裝類型、安裝方式、應用、最終用戶和分銷管道分類-2026年至2032年全球預測商用PIR動作感測器市場按連接方式、類型、安裝方式、輸出、應用和最終用戶分類-全球預測(2026-2032年)家用PIR運動感測器市場按技術、設備類型、安裝類型、應用和分銷管道分類-全球預測(2026-2032年)戶外動作感測器燈市場:按光源類型、應用、技術、安裝類型、連接方式和感測器範圍分類-2026-2032年全球預測智慧動作感測器照明市場:按技術、安裝方式、光源類型、電源、最終用戶和分銷管道分類-2026-2032年全球預測目標偵測感測器市場按組件、安裝類型、感測器類型和應用分類-全球預測,2026-2032年

2026年全球動作感測器市場報告2026年全球穿戴式裝置人機介面(HMI)感測器市場報告住宅PIR人體感應器市場按產品類型、電源、安裝類型、安裝方式、應用、最終用戶和分銷管道分類-2026年至2032年全球預測商用PIR動作感測器市場按連接方式、類型、安裝方式、輸出、應用和最終用戶分類-全球預測(2026-2032年)家用PIR運動感測器市場按技術、設備類型、安裝類型、應用和分銷管道分類-全球預測(2026-2032年)戶外動作感測器燈市場:按光源類型、應用、技術、安裝類型、連接方式和感測器範圍分類-2026-2032年全球預測智慧動作感測器照明市場:按技術、安裝方式、光源類型、電源、最終用戶和分銷管道分類-2026-2032年全球預測目標偵測感測器市場按組件、安裝類型、感測器類型和應用分類-全球預測,2026-2032年 動作感測器市場規模、佔有率和成長分析(按技術、嵌入式感測器、功能、應用和地區分類)-2026-2033年產業預測

動作感測器市場規模、佔有率和成長分析(按技術、嵌入式感測器、功能、應用和地區分類)-2026-2033年產業預測