|

市場調查報告書

商品編碼

1773433

戶外太陽能 LED 市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Outdoor Solar LED Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

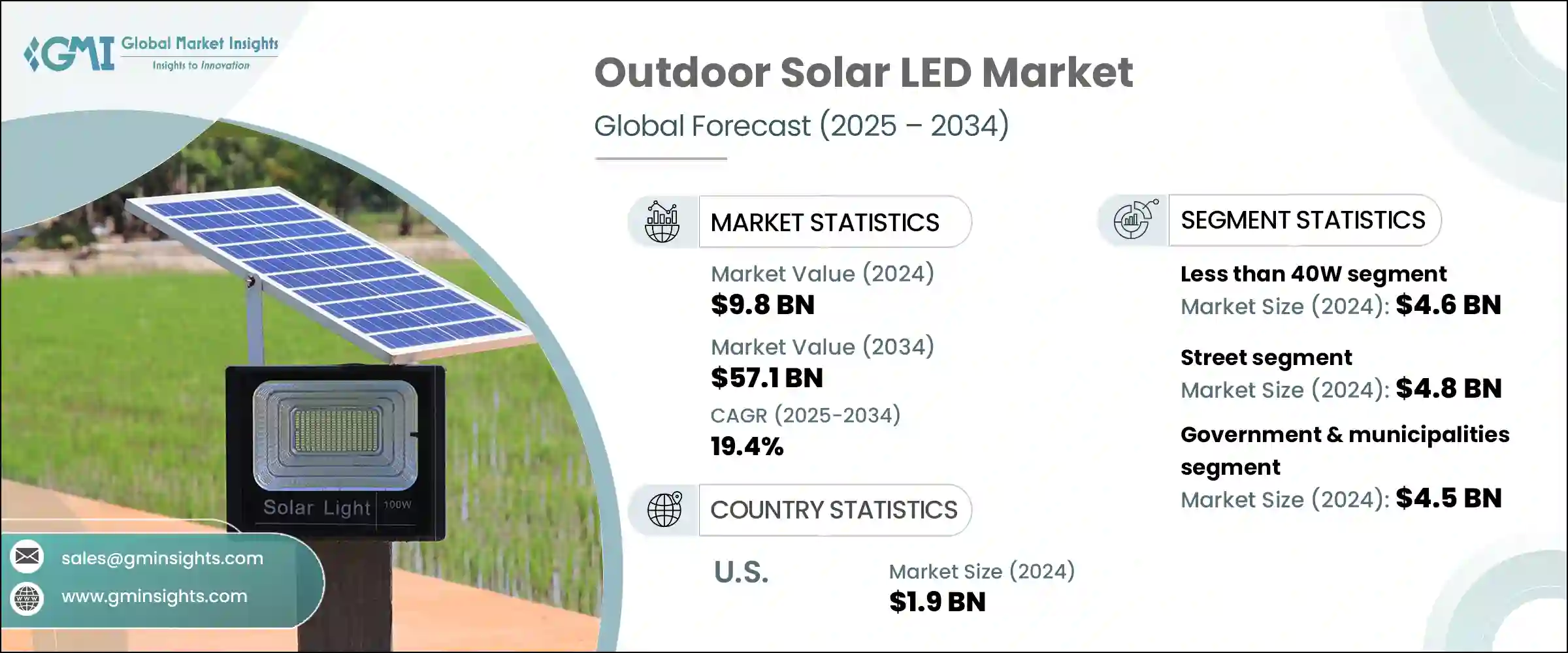

2024年,全球戶外太陽能LED市場規模達98億美元,預計2034年將以19.4%的複合年成長率成長,達到571億美元。強勁成長主要源自於全球對節能照明替代品日益成長的需求。隨著永續發展目標在全球日益受到重視,機構和終端消費者都越來越傾向於環保解決方案。與傳統照明技術相比,戶外太陽能LED燈憑藉其更長的使用壽命和更低的功耗,正逐漸成為人們青睞的選擇。

這些系統正廣泛應用於基礎設施和智慧城市建設,而能源最佳化在這些領域至關重要。在美國等地區,節能照明(尤其是經過認證的家用LED產品)的功耗顯著降低,使用壽命也遠超白熾燈,因此在市政當局和私人用戶中得到廣泛採用。這些節能措施正在推動各行各業的強勁成長,並持續推動太陽能LED技術的發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 98億美元 |

| 預測值 | 571億美元 |

| 複合年成長率 | 19.4% |

全球各國政府正在推出激勵措施和監管措施,以促進太陽能的應用。戶外太陽能LED在為農村和服務欠缺地區提供可靠照明方面發揮關鍵作用,有助於改善公共安全和基本服務的可及性。它們也被納入國家農村電氣化、緊急準備和低碳基礎設施擴建項目。隨著公共機構在優惠政策和資金支持下擴大採用太陽能系統,無論是在發展中地區還是已開發地區,太陽能系統的部署都在迅速擴大。

2024年,40瓦以下市場產值達46億美元。這些低功率設備經濟高效、安裝簡便,且所需基礎設施極少,是電網存取受限的發展中國家和地區的理想選擇。它們在陽光直射較少的情況下也能保持良好性能,並且使用尺寸較小的面板,因此非常適合緊湊且陰涼的城市區域。在裝飾性景觀和周邊照明領域,這類產品的使用也日益增多,因為設計和價格都至關重要。隨著城市地區尋求經濟高效的永續照明覆蓋,郊區和鄉村照明計畫對40瓦以下產品的需求持續成長。

2024年,街道照明市場規模達48億美元。街道照明是城市發展的重要組成部分,因為它影響安全、交通和環境目標。不斷擴張的城市優先考慮太陽能街道照明,以降低能源成本並減少碳排放。這些系統提供可擴展的分散式部署,非常適合缺乏成熟電網基礎架構的地區。智慧調光、運動感測器和遠端監控等功能正日益整合,尤其是在全球智慧城市計畫的推動下。這種轉變進一步推動了用於道路和公共區域照明的戶外太陽能LED的成長。

2024年,美國戶外太陽能LED市場規模達19億美元,這得益於全國範圍內的節能減排任務和城市創新項目推動的太陽能照明解決方案的廣泛應用。各州和市政府正積極以太陽能照明方案取代傳統照明,以降低能源成本和碳排放。聯邦和州政府的財政支持持續為太陽能照明改造計畫提供資金。此外,對能源韌性的重視,尤其是在極端天氣事件頻繁的地區,正在刺激對獨立運作的太陽能LED系統的需求。這些因素正在鞏固美國作為太陽能LED部署領先和先進市場的地位。

戶外太陽能LED市場的知名公司包括BISOL集團、松下控股公司、Wipro照明、Signify控股和Sunna Design。為了在戶外太陽能LED領域獲得競爭優勢,各公司都優先考慮創新、垂直整合和全球擴張。主要參與者正在開發智慧太陽能LED解決方案,這些解決方案具有運動偵測、無線連接和自適應亮度等功能,以配合智慧城市基礎設施的目標。許多公司也致力於提高其照明系統中太陽能電池板和電池儲能系統的效率。與市政機構和基礎設施公司建立策略合作夥伴關係有助於確保大型專案的成功,尤其是在新興經濟體。各公司正在投資模組化和可擴展的產品線,以滿足不同的功率和設計需求,從而實現更高程度的客製化。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 川普政府關稅

- 對貿易的影響

- 貿易量中斷

- 報復措施

- 對產業的影響

- 供給側影響

- 關鍵零件價格波動

- 供應鏈重組

- 生產成本影響

- 需求面影響(售價)

- 價格傳導至終端市場

- 市佔率動態

- 消費者反應模式

- 供給側影響

- 受影響的主要公司

- 策略產業反應

- 供應鏈重組

- 定價和產品策略

- 政策參與

- 展望與未來考慮

- 對貿易的影響

- 產業衝擊力

- 成長動力

- 對節能照明解決方案的需求不斷成長

- 政府對太陽能利用的措施和補貼

- 農村及偏遠地區離網電氣化發展

- 太陽能板和LED技術成本下降

- 都市化和基礎建設不斷推進

- 產業陷阱與挑戰

- 依賴天氣條件和地理限制

- 初始安裝和基礎設施成本高

- 市場機會

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 物聯網與太陽能照明系統的整合

- 擴展智慧和自適應照明控制

- 使用高效能 LED 和儲能技術

- 新興技術

- 人工智慧驅動的太陽能燈預測性維護的開發

- 太陽能照明與城市智慧電網基礎設施的融合

- 薄膜和鈣鈦礦太陽能板技術的進步

- 當前的技術趨勢

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準化分析

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按瓦數,2021 年至 2034 年

- 主要趨勢

- 小於40W

- 40W至150W

- 超過150W

第6章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 街道

- 花園

- 途徑

- 其他

第7章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 政府和市政當局

- 商業企業

- 住宅消費者

- 工業和基礎設施

第8章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- BISOL Group

- Crompton Greaves Consumer Electricals Limited

- Greenshine New Energy

- Guangzhou Anern Energy Technology Co., Ltd.

- Havells India Limited

- LEADSUN

- Panasonic Holdings Corporation

- Polybrite Solar Co., Ltd.

- Sensol Technologies

- Signify Holding

- SOKOYO Solar Lighting Co., Ltd.

- Solar Lighting International, Inc.

- Sunna Design

- Suntech-Solar-Enterprises

- URJA SAUR ELECTRONICS

- Wipro Lighting

The Global Outdoor Solar LED Market was valued at USD 9.8 billion in 2024 and is estimated to grow at a CAGR of 19.4% to reach USD 57.1 billion by 2034. This robust growth is primarily driven by rising demand for energy-efficient lighting alternatives worldwide. As sustainability goals gain traction globally, both institutions and end consumers are gravitating toward eco-conscious solutions. Outdoor solar LED lights are becoming a favored option due to their extended service life and reduced power consumption when compared to conventional lighting technologies.

These systems are being widely adopted across infrastructure and smart city developments where energy optimization is critical. In regions like the United States, energy-efficient lighting-particularly certified residential LED products-consumes significantly less power and offers drastically longer lifespan than incandescent bulbs, leading to widespread adoption among municipalities and private users. These savings are contributing to strong uptake across diverse sectors, fueling continued momentum for solar LED technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.8 billion |

| Forecast Value | $57.1 billion |

| CAGR | 19.4% |

Globally, governments are introducing incentives and regulatory measures to promote solar adoption. Outdoor solar LEDs are playing a key role in bringing dependable lighting to rural and underserved areas, helping improve public safety and access to basic services. They are also being integrated into national programs focused on rural electrification, emergency preparedness, and low-carbon infrastructure expansion. With public institutions increasingly adopting solar-based systems under favorable policies and financial backing, deployment is scaling quickly across both developing and developed regions.

The less than 40W segment generated USD 4.6 billion in 2024. These lower-wattage units are cost-effective, simple to install, and require minimal infrastructure, making them ideal for developing countries and regions with limited grid access. Their ability to perform well under less direct sunlight and operate with smaller panels makes them suitable for compact and shaded urban zones. They are also seeing increased usage in decorative landscaping and perimeter lighting where both design and affordability are important. As urban areas seek sustainable lighting coverage that's cost-efficient, demand for under-40W products continues to rise across suburban and rural lighting initiatives.

Street lighting segment generated USD 4.8 billion in 2024. Street illumination is a vital part of urban development as it impacts security, transportation, and environmental goals. Expanding cities are prioritizing solar-powered street lighting as a solution to reduce energy bills and carbon emissions. These systems offer scalable and decentralized deployment, ideal for areas lacking established grid infrastructure. Features like smart dimming, motion sensors, and remote monitoring are being increasingly integrated, especially under global smart city programs. This shift is further boosting the growth of outdoor solar LEDs for roadway and public area lighting.

U.S. Outdoor Solar LED Market was valued at USD 1.9 billion in 2024, driven by broad adoption of solar lighting solutions under nationwide energy efficiency mandates and urban innovation projects. State and municipal governments are actively replacing conventional lights with solar options to lower energy expenses and carbon output. Financial support from both federal and state programs continues to fund solar lighting conversions. Additionally, heightened focus on energy resilience, particularly in areas prone to extreme weather events, is spurring demand for standalone solar LED systems that operate independently of the grid. These factors are strengthening the U.S. position as a leading and advanced market for solar LED deployment.

Notable companies in the Outdoor Solar LED Market include BISOL Group, Panasonic Holdings Corporation, Wipro Lighting, Signify Holding, and Sunna Design. To gain a competitive edge in the outdoor solar LED space, companies are prioritizing innovation, vertical integration, and global expansion. Major players are developing smart-enabled solar LED solutions featuring motion detection, wireless connectivity, and adaptive brightness to align with smart city infrastructure goals. Many firms are also focusing on enhancing the efficiency of solar panels and battery storage within their lighting systems. Strategic partnerships with municipal bodies and infrastructure firms help secure large-scale projects, particularly in emerging economies. Companies are investing in modular and scalable product lines to meet varying wattage and design needs, allowing greater customization.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising demand for energy-efficient lighting solutions

- 3.3.1.2 Government initiatives and subsidies for solar energy adoption

- 3.3.1.3 Growing off-grid electrification in rural and remote areas

- 3.3.1.4 Declining costs of solar panels and LED technology

- 3.3.1.5 Increasing urbanization and infrastructure development

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Dependence on weather conditions and geographic limitations

- 3.3.2.2 High initial installation and infrastructure costs

- 3.3.3 Market opportunities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 Integration of IoT with solar lighting systems

- 3.8.1.2 Expansion of smart and adaptive lighting controls

- 3.8.1.3 Use of high-efficiency LED and energy storage technologies

- 3.8.2 Emerging technologies

- 3.8.2.1 Development of AI-driven predictive maintenance for solar lights

- 3.8.2.2 Integration of solar lighting with urban smart grid infrastructure

- 3.8.2.3 Advancements in thin-film and perovskite solar panel technologies

- 3.8.1 Current technological trends

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Sustainability measures

- 3.12 Consumer sentiment analysis

- 3.13 Patent and IP analysis

- 3.14 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Wattage, 2021 – 2034 (USD Billion & Units)

- 5.1 Key trends

- 5.2 Less than 40W

- 5.3 40W to 150W

- 5.4 More than 150W

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion & Units)

- 6.1 Key trends

- 6.2 Street

- 6.3 Garden

- 6.4 Pathway

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Billion & Units)

- 7.1 Key trends

- 7.2 Government & municipalities

- 7.3 Commercial enterprises

- 7.4 Residential consumers

- 7.5 Industrial & infrastructure

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BISOL Group

- 9.2 Crompton Greaves Consumer Electricals Limited

- 9.3 Greenshine New Energy

- 9.4 Guangzhou Anern Energy Technology Co., Ltd.

- 9.5 Havells India Limited

- 9.6 LEADSUN

- 9.7 Panasonic Holdings Corporation

- 9.8 Polybrite Solar Co., Ltd.

- 9.9 Sensol Technologies

- 9.10 Signify Holding

- 9.11 SOKOYO Solar Lighting Co., Ltd.

- 9.12 Solar Lighting International, Inc.

- 9.13 Sunna Design

- 9.14 Suntech-Solar-Enterprises

- 9.15 URJA SAUR ELECTRONICS

- 9.16 Wipro Lighting

戶外太陽能LED市場規模、佔有率和成長分析:按產品類型、電池類型、應用、分銷管道和地區分類-2026-2033年產業預測

戶外太陽能LED市場規模、佔有率和成長分析:按產品類型、電池類型、應用、分銷管道和地區分類-2026-2033年產業預測 戶外太陽能吊掛市場按產品類型、材質、功率輸出、工作模式、應用和最終用戶分類,全球預測(2026-2032年)

戶外太陽能吊掛市場按產品類型、材質、功率輸出、工作模式、應用和最終用戶分類,全球預測(2026-2032年) 戶外太陽能LED市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、電壓、最終用途、地區及競爭格局分類,2021-2031年)

戶外太陽能LED市場-全球產業規模、佔有率、趨勢、機會及預測(依產品類型、電壓、最終用途、地區及競爭格局分類,2021-2031年) 全球戶外太陽能LED市場

全球戶外太陽能LED市場 全球戶外太陽能 LED 市場:成長、展望與競爭分析(2025-2033年)

全球戶外太陽能 LED 市場:成長、展望與競爭分析(2025-2033年) 全球戶外太陽能 LED 市場規模研究,按應用、功率(低於 39W、40W 至 149W、高於 150W)、按最終用途(住宅、商業、工業)和區域預測 2022-2032 年

全球戶外太陽能 LED 市場規模研究,按應用、功率(低於 39W、40W 至 149W、高於 150W)、按最終用途(住宅、商業、工業)和區域預測 2022-2032 年 戶外太陽能 LED 市場規模、佔有率、趨勢分析報告:按應用、瓦數、最終用途、地區、細分預測,2025-2030 年

戶外太陽能 LED 市場規模、佔有率、趨勢分析報告:按應用、瓦數、最終用途、地區、細分預測,2025-2030 年