|

市場調查報告書

商品編碼

1773428

霍爾效應電流感測器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Hall-Effect Current Sensor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

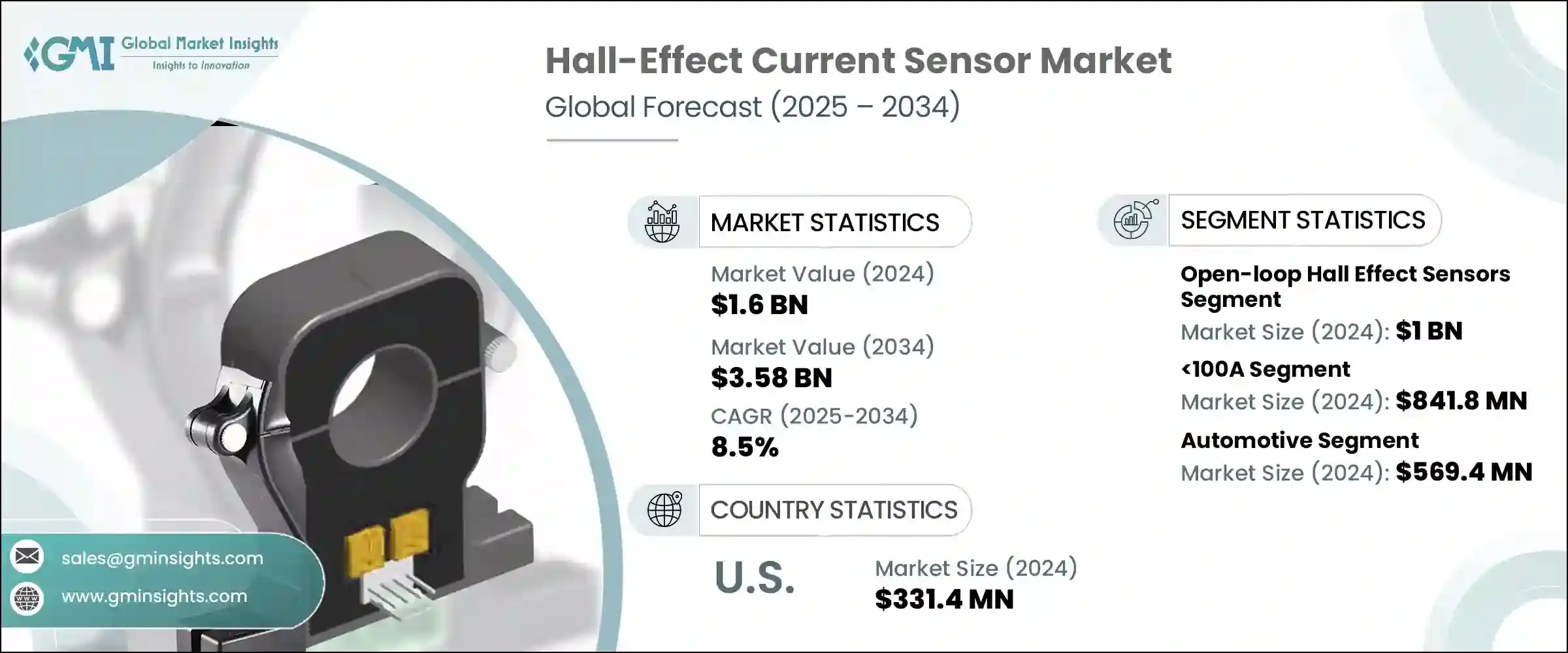

2024 年全球霍爾效應電流感測器市場價值為 16 億美元,預計到 2034 年將以 8.5% 的複合年成長率成長,達到 35.8 億美元。這一成長主要得益於電動車的普及以及向智慧電網技術的轉變。隨著能源產業的發展,對精確和即時電流感測的需求也在增加,尤其是隨著電源分散和再生能源的整合。霍爾效應電流感測器提供非侵入式、精確的測量,這對於能量流管理、故障檢測和整體電網性能監控至關重要。它們能夠在交流和直流環境中工作,同時保持電氣隔離,這使得它們在太陽能逆變器、電池儲存系統、電動車充電站和綜合智慧電網應用中不可或缺。

小型多功能消費電子產品的興起也推動了市場擴張。智慧型手機、穿戴式裝置和智慧家庭系統等設備需要微型電流感測器,這些感測器既要提供高精度,又要節省空間。霍爾效應感測器憑藉其固態設計、低功耗和高靈敏度,完美契合了這項需求。透過將這些感測器整合到電源管理電路中,製造商可以透過即時電流監控、過載保護和能量最佳化來提高設備的安全性和效率——這些功能對於當今的智慧電子產品至關重要。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 16億美元 |

| 預測值 | 35.8億美元 |

| 複合年成長率 | 8.5% |

預計到2034年,閉迴路(或補償式)霍爾效應電流感測器市場將以9.6%的複合年成長率成長。此類感測器在要求卓越精度、快速響應和穩定性的應用中備受青睞,例如工業馬達驅動、機器人自動化、軌道運輸系統和再生能源設施。這些感測器通常設計用於測量40A至150A之間的電流,即使在溫度波動的情況下也能保持出色的線性度,使其成為高性能環境的理想選擇。它們在高功率系統(例如不間斷電源、電動車充電基礎設施和儲能逆變器)中至關重要,因為可靠性和精確控制至關重要。

市場按電流範圍細分為 100A、100-500A 和 500A 以上類別。 2024 年,100A 細分市場佔據市場主導地位,價值 8.418 億美元。此範圍涵蓋中低功率需求的應用,例如電源、照明系統、小型電動車和智慧家電。涉及街道照明和分散式太陽能發電系統的智慧城市計畫高度依賴 100A 感測器進行即時電流監控和功率最佳化。此類感測器提供關鍵的回饋迴路,可實現調光、運動啟動和診斷報告等智慧照明功能,這些功能在城市地區推進基礎設施建設時至關重要。

2024年,美國霍爾效應電流感測器市場規模達3.314億美元。受聯邦智慧城市計畫和綠色能源計劃的推動,節能基礎設施的日益普及推動了該地區的成長。城市地區太陽能照明改造的不斷擴展,對用於電力監控、故障檢測和能源最佳化的霍爾效應電流感測器的需求也顯著增加。美國能源部的激勵措施和州級撥款持續推動太陽能路燈計畫的發展,並促進了這些感測器在性能管理中的應用。

霍爾效應電流感測器產業的主要參與者包括邁來芯 (Melexis)、德州儀器公司 (Texas Instruments Incorporated)、Allegro MicroSystems, Inc.、LEM International SA 和英飛凌科技股份公司 (Infineon Technologies AG)。這些公司在創新、產品可靠性以及拓展新興市場和成熟市場的方面積極競爭。為了鞏固市場地位並擴大市場佔有率,霍爾效應電流感測器市場的領先公司高度重視持續創新,推出靈敏度更高、微型化程度更高、能效更高的先進感測器。

與原始設備製造商和公用事業供應商建立戰略合作夥伴關係,使其能夠進入電動車、再生能源和智慧基礎設施等新興領域。透過投資智慧電網部署和電動車普及正在加速發展的新興市場,擴大全球影響力是另一個重要策略。企業也專注於開發針對特定應用需求的客製化解決方案,以提高客戶留存率。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 電動和混合動力汽車需求不斷成長

- 工業自動化和機器人技術的成長

- 再生能源系統的擴展

- 智慧電網和能源監控的普及率不斷提高

- 消費性電子產品的小型化和整合化

- 產業陷阱與挑戰

- 易受外部磁干擾

- 電流水平非常低時精度有限

- 市場機會

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 物聯網與太陽能照明系統的整合

- 智慧和自適應照明控制的擴展

- 使用高效LED和儲能技術

- 新興技術

- 人工智慧驅動的太陽能燈預測性維護的開發

- 太陽能照明與城市智慧電網基礎設施的融合

- 薄膜和鈣鈦礦太陽能板技術的進步

- 當前的技術趨勢

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準化分析

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理分佈比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 合併與收購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 開迴路霍爾效應感測器

- 閉迴路(補償)霍爾效應感測器

第6章:市場估計與預測:依目前範圍,2021 年至 2034 年

- 主要趨勢

- <100 安

- 100–500 安

- >500 安

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 電力設施

- 製造業

- 消費性電子產品

- 再生能源

- 電信

- 鐵路

- 航太

- 汽車

- 其他

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第9章:公司簡介

- Allegro MicroSystems, Inc.

- Asahi Kasei Microdevices Corporation

- Infineon Technologies AG

- LEM International SA

- Littelfuse, Inc.

- Magnesensor Technology

- Melexis

- Mornsun Guangzhou Science & Technology Co., Ltd.

- ROHM Co., Ltd.

- Socan Technologies

- TAMURA Corporation

- TDK-Micronas GmbH

- Texas Instruments Incorporated

- Vishay Intertechnology, Inc.

The Global Hall-Effect Current Sensor Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 3.58 billion by 2034. This growth is largely driven by the rising adoption of electric vehicles, as well as the shift towards smart grid technologies. As the energy sector evolves, the demand for precise and real-time current sensing increases, especially with the decentralization of power sources and integration of renewable energy. Hall-effect current sensors provide non-intrusive, accurate measurements critical for energy flow management, fault detection, and overall grid performance monitoring. Their ability to operate in both AC and DC environments while maintaining electrical isolation makes them indispensable in solar inverters, battery storage systems, electric vehicle charging stations, and comprehensive smart grid applications.

The rise of compact, multifunctional consumer electronics also fuels market expansion. Devices such as smartphones, wearables, and smart home systems require miniaturized current sensors that deliver high accuracy without sacrificing space. Hall-effect sensors fit this need perfectly due to their solid-state design, low power usage, and high sensitivity. By integrating these sensors into power management circuits, manufacturers enhance device safety and efficiency through real-time current monitoring, overload protection, and energy optimization-features essential for today's smarter electronic products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 billion |

| Forecast Value | $3.58 billion |

| CAGR | 8.5% |

The closed-loop, or compensated, hall-effect current sensor segment is expected to grow at a CAGR of 9.6% through 2034. This category is preferred in applications demanding exceptional accuracy, rapid response, and stability, including industrial motor drives, robotic automation, rail systems, and renewable energy setups. Typically designed to measure currents between 40A and 150A, these sensors maintain excellent linearity even under temperature fluctuations, making them ideal for high-performance environments. They are crucial in high-power systems like uninterruptible power supplies, EV charging infrastructure, and energy storage inverters, where reliability and precise control are vital.

The market is segmented by current range into 100A, 100-500A, and above 500A categories. The 100A segment led the market in 2024, valued at USD 841.8 million. This range covers applications with low to medium power demands, such as power supplies, lighting systems, smaller electric vehicles, and smart appliances. Smart city initiatives involving street lighting and distributed solar power systems heavily rely on 100A sensors for real-time current monitoring and power optimization. Such sensors provide critical feedback loops that enable smart lighting functionalities like dimming, motion activation, and diagnostic reporting, which are essential as urban areas advance their infrastructure.

U.S. Hall-Effect Current Sensor Market was valued at USD 331.4 million in 2024. Growth in this region is supported by the increasing adoption of energy-efficient infrastructure fueled by federal smart city programs and green energy initiatives. The expansion of solar lighting retrofits across urban areas is creating significant demand for hall-effect current sensors used in power monitoring, fault detection, and optimizing energy use. Incentives from the U.S. Department of Energy and state-level grants continue to promote solar street lighting projects, bolstering the adoption of these sensors for performance management.

Key players in the Hall-Effect Current Sensor Industry include Melexis, Texas Instruments Incorporated, Allegro MicroSystems, Inc., LEM International SA, and Infineon Technologies AG. These companies actively compete on innovation, product reliability, and expanding their reach across emerging and established markets. To solidify their position and expand market share, leading companies in the Hall-Effect Current Sensor Market focus heavily on continuous innovation, introducing advanced sensors with improved sensitivity, miniaturization, and energy efficiency.

Strategic partnerships and collaborations with original equipment manufacturers and utility providers allow them to penetrate new sectors such as electric vehicles, renewable energy, and smart infrastructure. Expanding global footprints by investing in emerging markets where smart grid deployment and EV adoption are accelerating is another vital strategy. Companies also emphasize developing customizable solutions tailored to specific application requirements, improving customer retention.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.3 Type trends

- 2.4 Current range trends

- 2.5 End use trends

- 2.6 Regional

- 2.7 TAM Analysis, 2025-2034 (USD Million)

- 2.8 CXO Perspectives: Strategic imperatives

- 2.8.1 Executive decision points

- 2.8.2 Critical Success Factors

- 2.9 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for electric and hybrid vehicles

- 3.2.1.2 Growth in industrial automation and robotics

- 3.2.1.3 Expansion of renewable energy systems

- 3.2.1.4 Increasing adoption of smart grids and energy monitoring

- 3.2.1.5 Miniaturization and integration in consumer electronics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Susceptibility to external magnetic interference

- 3.2.2.2 Limited accuracy at very low current levels

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Integration of IoT with Solar Lighting Systems

- 3.7.1.2 Expansion of Smart and Adaptive Lighting Controls

- 3.7.1.3 Use of High-Efficiency LED and Energy Storage Technologies

- 3.7.2 Emerging technologies

- 3.7.2.1 Development of AI-Driven Predictive Maintenance for Solar Lights

- 3.7.2.2 Integration of Solar Lighting with Urban Smart Grid Infrastructure

- 3.7.2.3 Advancements in Thin-Film and Perovskite Solar Panel Technologies

- 3.7.1 Current technological trends

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Measures

- 3.11 Consumer Sentiment Analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market Concentration Analysis

- 4.2.1 By region

- 4.3 Competitive Benchmarking of key Players

- 4.3.1 Financial Performance Comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit Margin

- 4.3.1.3 R&D

- 4.3.2 Product Portfolio Comparison

- 4.3.2.1 Product Range Breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic Presence Comparison

- 4.3.3.1 Global Footprint Analysis

- 4.3.3.2 Service Network Coverage

- 4.3.3.3 Market Penetration by Region

- 4.3.4 Competitive Positioning Matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche Players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial Performance Comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and Acquisitions

- 4.4.2 Partnerships and Collaborations

- 4.4.3 Technological Advancements

- 4.4.4 Expansion and Investment Strategies

- 4.4.5 Sustainability Initiatives

- 4.4.6 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Open-loop hall-effect sensors

- 5.3 Closed-loop (Compensated) hall-effect sensors

Chapter 6 Market Estimates and Forecast, By Current Range, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 <100 A

- 6.3 100–500 A

- 6.4 >500 A

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Power utility

- 7.3 Manufacturing

- 7.4 Consumer electronics

- 7.5 Renewable energy

- 7.6 Telecommunication

- 7.7 Railway

- 7.8 Aerospace

- 7.9 Automotive

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Allegro MicroSystems, Inc.

- 9.2 Asahi Kasei Microdevices Corporation

- 9.3 Infineon Technologies AG

- 9.4 LEM International SA

- 9.5 Littelfuse, Inc.

- 9.6 Magnesensor Technology

- 9.7 Melexis

- 9.8 Mornsun Guangzhou Science & Technology Co., Ltd.

- 9.9 ROHM Co., Ltd.

- 9.10 Socan Technologies

- 9.11 TAMURA Corporation

- 9.12 TDK-Micronas GmbH

- 9.13 Texas Instruments Incorporated

- 9.14 Vishay Intertechnology, Inc.

霍爾效應數位零速感測器市場報告:趨勢、預測和競爭分析(至2035年)

霍爾效應數位零速感測器市場報告:趨勢、預測和競爭分析(至2035年) 霍爾效應電流感測器市場:依產品類型、輸出類型、最終用戶和電流範圍分類-2026-2032年全球市場預測

霍爾效應電流感測器市場:依產品類型、輸出類型、最終用戶和電流範圍分類-2026-2032年全球市場預測 霍爾效應感測器市場:2025-2030 年預測

霍爾效應感測器市場:2025-2030 年預測 霍爾效應特斯拉計市場規模及預測 2021 - 2031 年,全球及地區佔有率、趨勢及成長機會分析報告範圍:按類型、最終用戶及地理分類霍爾效應電流感測器市場(按技術、類型、應用和地區劃分),2024 年至 2031 年

霍爾效應特斯拉計市場規模及預測 2021 - 2031 年,全球及地區佔有率、趨勢及成長機會分析報告範圍:按類型、最終用戶及地理分類霍爾效應電流感測器市場(按技術、類型、應用和地區劃分),2024 年至 2031 年 2024-2028 年全球霍爾效應電流感測器市場

2024-2028 年全球霍爾效應電流感測器市場 霍爾效應感測器市場 - 按技術(線性、閾值和雙極)、按材料(銻化銦、砷化鎵、砷化銦)、應用、最終用戶和預測,2024 - 2032 年

霍爾效應感測器市場 - 按技術(線性、閾值和雙極)、按材料(銻化銦、砷化鎵、砷化銦)、應用、最終用戶和預測,2024 - 2032 年