|

市場調查報告書

商品編碼

1773421

獸醫除顫器市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Veterinary Defibrillators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

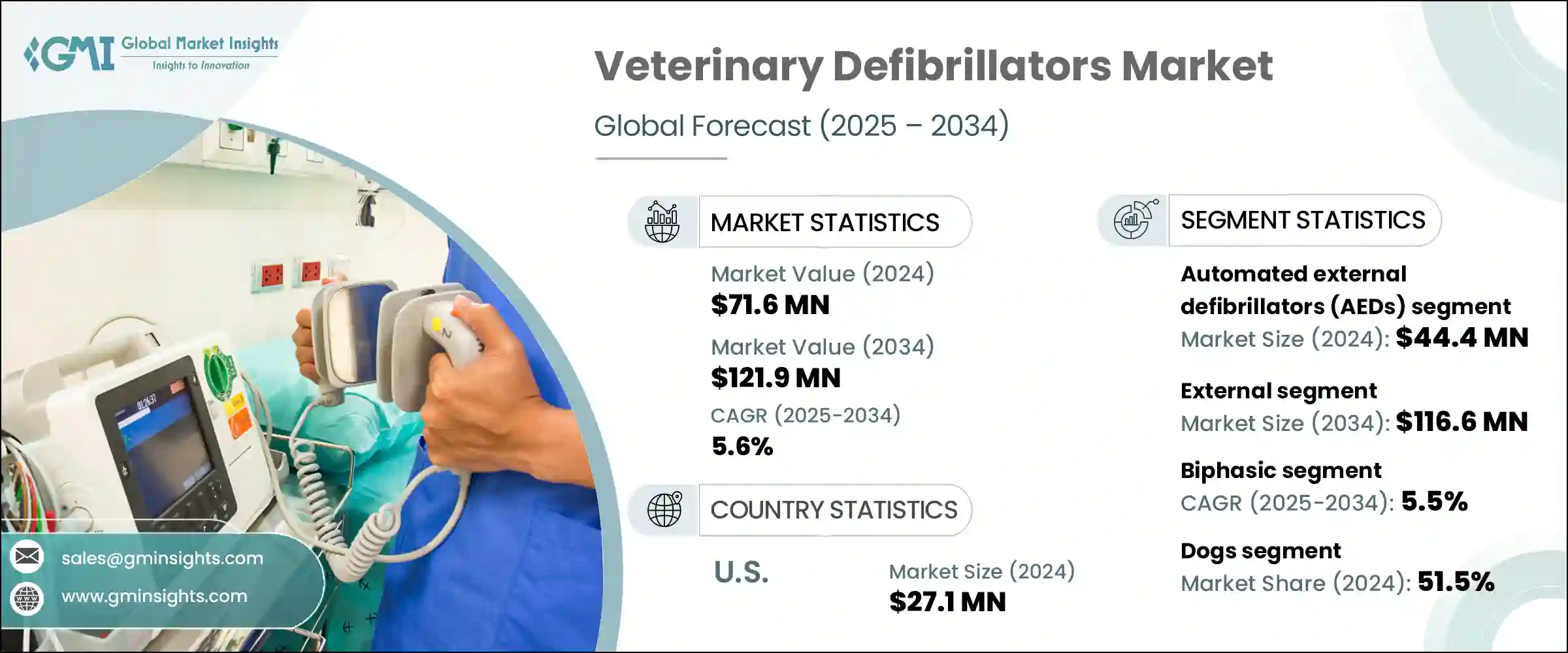

2024年,全球獸用去顫器市場規模達7,160萬美元,預計2034年將以5.6%的複合年成長率成長,達到1.219億美元。動物心血管疾病發生率的不斷上升是推動市場需求的主要驅動力。獸醫院、診所和急救機構數量的不斷增加也進一步推動了市場的成長。全天候動物急救服務和專業的心臟護理增加了對去顫器的需求,尤其是配備多參數功能的除顫器。緊湊、便攜且易於使用的自動體外除顫器 (AED) 的最新進展,使其覆蓋範圍擴展到小型診所和流動診所,使更多人能夠獲得救生技術。

更便捷的可及性、更便捷的操作以及與現代監測工具的整合,正推動其在更廣泛的獸醫應用中得到應用。隨著越來越多的寵物主人重視心臟健康,以及人們越來越意識到緊急情況下及時除顫的益處,獸醫診所也逐漸認知到這些救生設備的重要性。寵物收養率的提高和動物照護標準的不斷提升,正在推動對手動和自動化解決方案的長期需求,尤其是在基礎設施完善且不斷擴展的已開發市場。獸醫除顫器可在動物出現心律不整或心臟驟停時,對其施加治療性電擊。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7160萬美元 |

| 預測值 | 1.219億美元 |

| 複合年成長率 | 5.6% |

2024年,自動體外心臟去顫器 (AED) 細分市場收入達4,440萬美元。 AED的高普及率主要歸功於其直覺的設計和使用者引導功能。內建演算法可協助獸醫完成除顫過程,這促使其在中小型診所以及行動醫療單位中得到廣泛應用。 AED能夠即時評估心律並給予必要的電擊,使其成為快速反應場景中不可或缺的一部分。緊湊的外形、可充電電源和整合監控功能使其用途廣泛。 AED的應用範圍已逐漸超越傳統診所,擴展到行動獸醫服務、救援行動以及偏遠地區的動物衛生機構,這極大地促進了該細分市場的持續成長。

預計到2034年,雙相除顫器市場將以5.5%的複合年成長率成長。這些設備採用雙相電擊輸送,使電流更有效率、更可控地流經心臟,對心血管系統敏感的動物尤其有益。較低的能量需求降低了組織損傷風險,這在治療小型寵物時至關重要。雙相技術增強的安全性和有效性使其成為獸醫的首選。該市場的成長還得益於其與現代多參數監視器的高度相容性,以及與ICU和外科病房等重症監護環境的整合。由於其先進的電擊演算法和在高強度醫療環境中的適應性,獸醫專家和教學醫院越來越青睞這些系統。

2024年,美國獸醫除顫器市場規模達2,710萬美元。這一持續成長反映了寵物飼養量的不斷成長、獸醫基礎設施的改善以及對動物緊急護理的日益重視。寵物保險的普及也促進了高階技術的普及,使更多寵物主人能夠負擔得起雙相除顫器和自動體外心臟去顫器(AED)等設備。對寵物心臟護理的追求,正在推動獸醫診所建立更強大、技術更精良的緊急應變系統。

影響全球獸用除顫器市場的關鍵參與者包括邁瑞醫療國際有限公司、Avante Animal Health、武漢協和醫療技術公司、新一代醫療系統、Shinova Medical、ARI Medical Technology、Infinium Medical、深圳科曼醫療器材公司、Promed Technology、重慶遠星光學、Kalstein、Digicare Biomedical、Meditech Equiicalt、Meditech Epment、科學技術。為了鞏固和加強其市場地位,領先的獸用去顫器製造商正在積極投資開發緊湊、便攜的設備,將易用性與先進的臨床功能相結合。將智慧電擊演算法和多參數監控整合到手動和 AED 系統中有助於提升產品價值。與獸醫院和急救護理提供者建立策略合作夥伴關係使品牌能夠了解現實世界的需求並相應地客製化解決方案。此外,該公司正在擴大其全球分銷網路,並進入獸醫護理基礎設施仍在發展的服務不足地區。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 寵物擁有量增加以及寵物人性化

- 寵物心臟病發生率不斷上升

- 獸醫醫療技術的進步

- 產業陷阱與挑戰

- 除顫器成本高昂

- 缺乏意識和培訓

- 機會

- 緊急和重症護理服務需求不斷成長

- 發展中地區獸醫基礎設施投資不斷增加

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 新興技術

- 未來市場趨勢

- 消費者行為分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 自動體外去顫器(AED)

- 手動去顫器

第6章:市場估計與預測:依模式,2021 年至 2034 年

- 主要趨勢

- 外部的

- 內部的

第7章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 雙相

- 單相

第8章:市場估計與預測:依動物類型,2021 年至 2034 年

- 主要趨勢

- 狗

- 貓

- 馬匹

- 其他動物類型

第9章:市場估計與預測:按功能,2021 年至 2034 年

- 主要趨勢

- 標準

- 多參數能力

第 10 章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 獸醫醫院和診所

- 獸醫研究機構

- 其他最終用途

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- ARI Medical Technology

- Avante Animal Health

- Chongqing Vision Star Optical

- Digicare Biomedical

- Hefei Eur Vet Technology

- Infinium Medical

- Kalstein

- Meditech Equipment

- Mindray Medical International Limited

- New Gen Medical Systems

- Promed Technology

- Shenzhen Comen Medical Instruments

- Shinova Medical

- Wuhan Union Medical Technology

The Global Veterinary Defibrillators Market was valued at USD 71.6 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 121.9 million by 2034. Increasing occurrences of cardiovascular issues in animals are a major driver fueling market demand. The growth is further supported by the rising number of veterinary hospitals, clinics, and emergency care facilities. Around-the-clock animal emergency services and specialized cardiac care are increasing the need for defibrillators, particularly those equipped with multiparameter functionalities. Recent advancements in compact, portable, and easy-to-use automated external defibrillators (AEDs) are extending their reach to smaller clinics and mobile practices, enabling broader access to life-saving technologies.

Enhanced accessibility, combined with improvements in ease of operation and integration with modern monitoring tools, is helping drive adoption across a wider range of veterinary applications. As more pet owners prioritize cardiac health, and as awareness spreads regarding the benefits of timely defibrillation during emergencies, veterinary practices are recognizing the importance of these life-saving devices. Increased pet adoption rates and the rising standards of animal care are contributing to long-term demand for both manual and automated solutions, particularly in developed markets where infrastructure is well-established and continually expanding. Veterinary defibrillators deliver therapeutic electrical shocks to animals in cases of cardiac arrhythmia or sudden cardiac arrest.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $71.6 Million |

| Forecast Value | $121.9 Million |

| CAGR | 5.6% |

In 2024, the automated external defibrillators (AEDs) segment generated USD 44.4 million. The high adoption rate of AEDs is largely due to their intuitive design and user-guided functionality. Built-in algorithms that assist veterinarians through the defibrillation process are encouraging their use in small and mid-size practices, as well as in mobile units. Their ability to instantly assess heart rhythms and deliver the necessary shock makes them essential for rapid-response scenarios. Compact form, rechargeable power, and integrated monitoring capabilities support their versatility. AEDs are being increasingly used beyond traditional clinics, in mobile veterinary services, rescue operations, and animal health facilities in remote areas, which contributes significantly to the segment's ongoing expansion.

The biphasic defibrillators segment is projected to grow at a CAGR of 5.5% through 2034. These devices utilize dual-phase shock delivery, allowing more efficient and controlled current flow through the heart, which is particularly beneficial for animals with sensitive cardiovascular systems. Lower energy requirements reduce tissue damage risks, which is crucial when treating small pets. The enhanced safety and effectiveness of biphasic technology are positioning it as a preferred option among veterinarians. The segment's growth is also driven by its high compatibility with contemporary multiparameter monitors and integration into critical care environments like ICUs and surgical units. Veterinary specialists and teaching hospitals increasingly favor these systems due to their advanced shock algorithms and adaptability in high-intensity medical settings.

United States Veterinary Defibrillators Market reached USD 27.1 million in 2024. This consistent increase reflects growing pet ownership, improvements in veterinary infrastructure, and a heightened focus on emergency animal care. Pet insurance adoption is also supporting access to high-end technologies, enabling more pet owners to afford devices like biphasic defibrillators and AEDs. The push for better cardiac care in pets is fostering a more robust and technologically equipped emergency response system in veterinary practices.

Key players shaping the Global Veterinary Defibrillators Market include Mindray Medical International Limited, Avante Animal Health, Wuhan Union Medical Technology, New Gen Medical Systems, Shinova Medical, ARI Medical Technology, Infinium Medical, Shenzhen Comen Medical Instruments, Promed Technology, Chongqing Vision Star Optical, Kalstein, Digicare Biomedical, Meditech Equipment, Hefei Eur Vet Technology, and Zucami Medical. To secure and strengthen their market position, leading veterinary defibrillator manufacturers are actively investing in the development of compact, portable devices that combine ease of use with sophisticated clinical features. Integration of intelligent shock algorithms and multiparameter monitoring into both manual and AED systems is helping enhance product value. Strategic partnerships with veterinary hospitals and emergency care providers allow brands to understand real-world needs and tailor solutions accordingly. Additionally, companies are broadening their global distribution networks and entering underserved regions where veterinary care infrastructure is still evolving.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Modality

- 2.2.4 Technology

- 2.2.5 Animal type

- 2.2.6 Functionality

- 2.2.7 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership and humanization of pets

- 3.2.1.2 Increasing incidence of cardiac disorders in pets

- 3.2.1.3 Advancements in veterinary medical technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of defibrillators

- 3.2.2.2 Lack of awareness and training

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for emergency and critical care services

- 3.2.3.2 Growing investments in veterinary infrastructure in developing regions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Consumer behaviour analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Automated external defibrillators (AEDs)

- 5.3 Manual defibrillators

Chapter 6 Market Estimates and Forecast, By Modality, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 External

- 6.3 Internal

Chapter 7 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Biphasic

- 7.3 Monophasic

Chapter 8 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Dogs

- 8.3 Cats

- 8.4 Horses

- 8.5 Other animal types

Chapter 9 Market Estimates and Forecast, By Functionality, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Standard

- 9.3 Multiparameter-capability

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Veterinary research institutes

- 10.4 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 ARI Medical Technology

- 12.2 Avante Animal Health

- 12.3 Chongqing Vision Star Optical

- 12.4 Digicare Biomedical

- 12.5 Hefei Eur Vet Technology

- 12.6 Infinium Medical

- 12.7 Kalstein

- 12.8 Meditech Equipment

- 12.9 Mindray Medical International Limited

- 12.10 New Gen Medical Systems

- 12.11 Promed Technology

- 12.12 Shenzhen Comen Medical Instruments

- 12.13 Shinova Medical

- 12.14 Wuhan Union Medical Technology

去心房顫動市場商業機會、成長要素、產業趨勢分析及2026-2035年預測

去心房顫動市場商業機會、成長要素、產業趨勢分析及2026-2035年預測 心臟去心房顫動市場:按產品類型、模式、最終用戶和應用分類 - 全球預測(2026-2032 年)

心臟去心房顫動市場:按產品類型、模式、最終用戶和應用分類 - 全球預測(2026-2032 年) 2026年全球去心房顫動器設備市場報告2026年全球潛在客戶開發工具市場報告

2026年全球去心房顫動器設備市場報告2026年全球潛在客戶開發工具市場報告 去心房顫動分析儀市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能、安裝類型分類

去心房顫動分析儀市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、設備、最終用戶、功能、安裝類型分類 去心房顫動市場報告:按產品類型、最終用戶和地區分類 2026-2034 年

去心房顫動市場報告:按產品類型、最終用戶和地區分類 2026-2034 年 心臟去心房顫動市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品、最終用戶、地區和競爭對手分類,2021-2031年日本除顫器市場報告(按產品類型(植入式除顫器、體外除顫器)、最終用戶(醫院和診所、院前急診機構、心臟中心、家庭護理機構及其他)和地區分類,2026-2034 年)

心臟去心房顫動市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品、最終用戶、地區和競爭對手分類,2021-2031年日本除顫器市場報告(按產品類型(植入式除顫器、體外除顫器)、最終用戶(醫院和診所、院前急診機構、心臟中心、家庭護理機構及其他)和地區分類,2026-2034 年) 去心房顫動市場規模、佔有率、成長分析(按類型、患者類型、最終用戶和地區分類)-2026-2033年產業預測

去心房顫動市場規模、佔有率、成長分析(按類型、患者類型、最終用戶和地區分類)-2026-2033年產業預測 心臟節律器和去心房顫動導線移除套件:全球市場佔有率和排名、總收入和需求預測(2025-2031年)

心臟節律器和去心房顫動導線移除套件:全球市場佔有率和排名、總收入和需求預測(2025-2031年)