|

市場調查報告書

商品編碼

1773414

胸腰椎融合植入物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Thoracolumbar Spinal Fusion Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

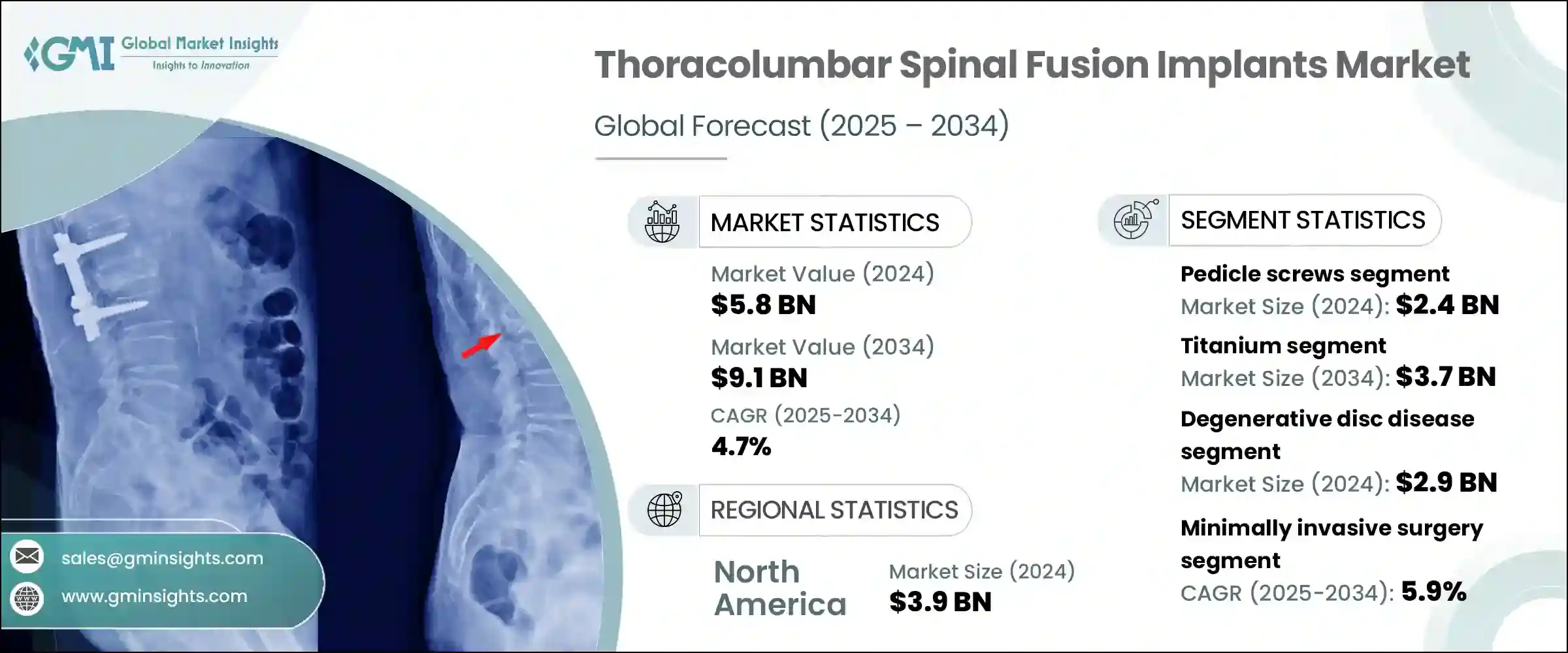

2024年,全球胸腰椎融合植入物市場規模達58億美元,預計2034年將以4.7%的複合年成長率成長,達到91億美元。市場擴張的動力源於脊椎疾病盛行率的上升、道路交通事故傷害的激增以及人們對微創手術解決方案日益成長的興趣。創傷、退化性疾病和先天性畸形患者對脊椎穩定的需求日益成長,顯著促進了醫院和外科中心對脊椎融合手術的採用。隨著全球老齡人口的成長,與年齡相關的脊椎併發症(尤其是在胸腰椎區域)的發生率持續上升,從而導致融合植入物的應用範圍不斷擴大。

此外,手術方法的改進以及患者對微創手術的偏好也推動了這一趨勢,尤其是在新興醫療保健系統中。隨著醫療專業人員尋求更快的康復時間和更少的併發症,他們開始轉向外科植入物的創新,以最大限度地減少組織損傷,同時提供長期的脊椎支撐。總體而言,臨床需求、人口老化、技術進步以及不斷成長的創傷發生率等因素共同推動全球市場持續成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 58億美元 |

| 預測值 | 91億美元 |

| 複合年成長率 | 4.7% |

2024年,椎弓根螺釘佔據胸腰椎融合植入物市場主導地位,總估值達24億美元。其結構強度高,能夠提供3D脊椎的剛性支撐,使其成為穩定椎體骨折、矯正排列問題或緩解椎間盤壓力的首選方案。在胸腰椎手術中,由於安全固定至關重要,其應用範圍更加廣泛。

外科醫生更傾向於在需要高精度和持久支撐的手術中使用這類系統,尤其是在創傷和畸形矯正病例中。隨著微創技術的日益普及,新一代椎弓根螺釘現已包含多軸頭、空心軸和可擴展型等先進配置。這些改進正在提高術中效率、外科醫生的控制力以及對不同脊椎解剖結構的適應性,所有這些都有助於改善臨床療效並提高手術成功率。

2034年,鈦合金市場規模將達到37億美元。鈦及其合金,尤其是Ti-6Al-4V,因其兼具高強度、生物相容性和耐腐蝕性,已成為脊椎融合植入物的首選材料。鈦與人體組織的相容性使其能夠更快地促進骨整合,這對於實現長期融合至關重要。其彈性模量與人體骨骼非常接近,從而減少了應力遮擋,並最大限度地減少了植入物鬆動或鄰近節段疾病等併發症。此外,鈦與MRI和CT掃描等診斷影像技術的兼容性進一步增強了其臨床應用的潛力。

2024年,美國胸腰椎融合植入物市場規模達36億美元。這一成長得益於高手術量、尖端手術技術的普及以及優惠的保險報銷政策。患有椎管狹窄、脊椎滑脫和退化性椎間盤疾病的老年人口不斷成長,持續刺激相關手術需求。此外,機器人和導航系統融入脊椎外科手術工作流程,提高了融合手術的精準度,從而增加了對植入物的需求。可擴展椎間融合器和經皮螺釘系統在微創技術中的廣泛應用,進一步提升了市場規模。 Globus Medical和美敦力等領先公司透過持續的產品創新、外科醫生教育計畫以及廣泛的分銷合作夥伴關係,在美國保持著強大的市場佔有率。

引領全球胸腰椎融合植入物市場的知名企業包括 Highridge Medical (ZimVie)、B. Braun、Spineart、Orthofix Medical、DePuy Synthes (JnJ)、Ulrich、JAYON、Alphatec Spine、Medtronic、Stryker (VB Spine)、RTI Surgical、Globus Medical、WASTON 和GSSTON。這些公司在拓展外科產品組合、改進植入物技術以及滿足多樣化患者需求方面發揮關鍵作用。

胸腰椎融合植入物市場的公司正在積極創新、產品開發和全球擴張,以鞏固其市場地位。主要參與者正在投資設計先進的植入系統,以支持微創手術並適應不同的患者解剖結構。客製化、模組化和適應性是優先考慮的核心產品特性。該公司還與外科醫生合作進行臨床試驗和真實世界證據生成,以改善產品並確保臨床療效。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 脊椎疾病盛行率上升

- 微創手術的需求不斷增加

- 技術進步

- 優惠的報銷政策

- 產業陷阱與挑戰

- 脊椎植入物和手術費用高昂

- 嚴格的監管情景

- 機會

- 人工智慧和機器人技術在脊椎手術中的整合

- 日益關注門診與流動醫療環境

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 按產品分類的價格趨勢

- 未來市場趨勢

- 報銷場景

- 報銷政策對市場成長的影響

- 消費者行為分析

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 全球的

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 椎弓根螺釘

- 椎間融合裝置(IBFD)

- 桿

- 盤子

- 其他產品類型

第6章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 鈦

- 聚醚醚酮(PEEK)

- 鈷鉻合金

- 不銹鋼

- 其他材料

第7章:市場估計與預測:依手術類型,2021 年至 2034 年

- 主要趨勢

- 開放性手術

- 微創手術

第 8 章:市場估計與預測:按適應症,2021 年至 2034 年

- 主要趨勢

- 椎間盤退化性疾病

- 脊椎創傷

- 脊椎畸形

- 脊椎腫瘤

- 其他適應症

第9章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 骨科診所

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Alphatec Spine

- B. Braun

- DePuy Synthes (JnJ)

- Globus Medical

- GS Medical

- Highridge Medical (ZimVie)

- JAYON

- Medtronic

- Orthofix Medical

- RTI Surgical

- Spineart

- Stryker (VB Spine)

- Ulrich

- WASTON MEDICAL

The Global Thoracolumbar Spinal Fusion Implants Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 9.1 billion by 2034. Market expansion is being driven by the increasing prevalence of spinal conditions, a surge in road-related injuries, and rising interest in minimally invasive surgical solutions. Growing demand for spinal stabilization in trauma cases, degenerative disorders, and congenital deformities has significantly boosted the uptake of spinal fusion procedures across hospitals and surgical centers. As the global elderly population rises, the frequency of age-associated spine complications-particularly in the thoracolumbar region-continues to grow, leading to greater adoption of fusion implants.

Furthermore, improvements in surgical methods and patient preference for less invasive approaches are supporting this trend, especially in emerging healthcare systems. As medical professionals seek faster recovery times and fewer complications, they're turning to innovations in surgical implants that minimize tissue damage while providing long-term spinal support. Overall, the combination of clinical necessity, aging demographics, technological advancement, and growing trauma incidence is pushing the market toward consistent growth globally.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $9.1 Billion |

| CAGR | 4.7% |

In 2024, pedicle screws dominated the thoracolumbar spinal fusion implants market with a total valuation of USD 2.4 billion. Their structural strength and ability to provide rigid three-dimensional spinal support make them the go-to option for stabilizing vertebral fractures, correcting alignment issues, or relieving disc pressure. Their utility is amplified in thoracolumbar surgeries, where secure fixation is critical.

Surgeons prefer these systems for procedures that demand high precision and long-lasting support, especially in trauma and deformity correction cases. With more minimally invasive techniques being adopted, newer generations of pedicle screws now include advanced configurations such as polyaxial heads, cannulated shafts, and expandable versions. These enhancements are improving intraoperative efficiency, surgeon control, and adaptability to varying spinal anatomies-all of which are enhancing clinical outcomes and boosting procedural success.

The titanium segment will reach USD 3.7 billion by 2034. Titanium and its alloys, especially Ti-6Al-4V, have become the preferred material choice for spinal fusion implants due to their ideal combination of high strength, biocompatibility, and corrosion resistance. Titanium's compatibility with human tissue enables quicker bone integration, which is vital for achieving long-term fusion. Its elastic modulus closely resembles that of human bone, reducing stress shielding and minimizing complications like implant loosening or adjacent segment disease. Moreover, its compatibility with diagnostic imaging technologies, including MRI and CT scans, further enhances its clinical desirability.

United States Thoracolumbar Spinal Fusion Implants Market was valued at USD 3.6 billion in 2024. This growth can be attributed to high surgical volumes, cutting-edge surgical technology availability, and favorable insurance reimbursement policies. A growing elderly population experiencing spinal stenosis, spondylolisthesis, and degenerative disc issues continues to fuel procedural demand. In addition, the integration of robotics and navigation systems into spinal surgery workflows has improved the precision of fusion procedures, thereby increasing the demand for implants. The broader use of expandable cages and percutaneous screw systems in minimally invasive techniques further boost market volume. Leading companies like Globus Medical and Medtronic maintain a strong market presence in the U.S. through continued product innovation, surgeon education programs, and wide-reaching distribution partnerships.

Prominent players shaping the Global Thoracolumbar Spinal Fusion Implants Market include Highridge Medical (ZimVie), B. Braun, Spineart, Orthofix Medical, DePuy Synthes (JnJ), Ulrich, JAYON, Alphatec Spine, Medtronic, Stryker (VB Spine), RTI Surgical, Globus Medical, WASTON MEDICAL, and GS Medical. These companies play pivotal roles in expanding surgical portfolios, improving implant technologies, and addressing diverse patient needs.

Companies in the thoracolumbar spinal fusion implants market are pursuing aggressive innovation, product development, and global expansion to strengthen their market positioning. Major players are investing in the design of advanced implant systems that support minimally invasive procedures and accommodate varying patient anatomies. Customization, modularity, and adaptability are core product features being prioritized. Firms are also collaborating with surgeons for clinical trials and real-world evidence generation to refine products and ensure clinical efficacy.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates & calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Material

- 2.2.4 Surgery type

- 2.2.5 Indication

- 2.2.6 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spinal diseases

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favorable reimbursement policies

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of spinal implants and surgeries

- 3.2.2.2 Stringent regulatory scenario

- 3.2.3 Opportunities

- 3.2.3.1 Integration of AI and robotics in spine surgery

- 3.2.3.2 Growing focus on outpatient and ambulatory settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pedicle screws

- 5.3 Intervertebral body fusion device (IBFD)

- 5.4 Rods

- 5.5 Plates

- 5.6 Other product types

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Polyether ether ketone (PEEK)

- 6.4 Cobalt chrome

- 6.5 Stainless steel

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open surgery

- 7.3 Minimally invasive surgery

Chapter 8 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Degenerative disc disease

- 8.3 Spinal trauma

- 8.4 Spinal deformities

- 8.5 Spinal tumors

- 8.6 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Orthopedic clinics

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alphatec Spine

- 11.2 B. Braun

- 11.3 DePuy Synthes (JnJ)

- 11.4 Globus Medical

- 11.5 GS Medical

- 11.6 Highridge Medical (ZimVie)

- 11.7 JAYON

- 11.8 Medtronic

- 11.9 Orthofix Medical

- 11.10 RTI Surgical

- 11.11 Spineart

- 11.12 Stryker (VB Spine)

- 11.13 Ulrich

- 11.14 WASTON MEDICAL