|

市場調查報告書

商品編碼

1773389

汽車擋泥板輪圈面板零件市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive Fender Wheel House Panel Parts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

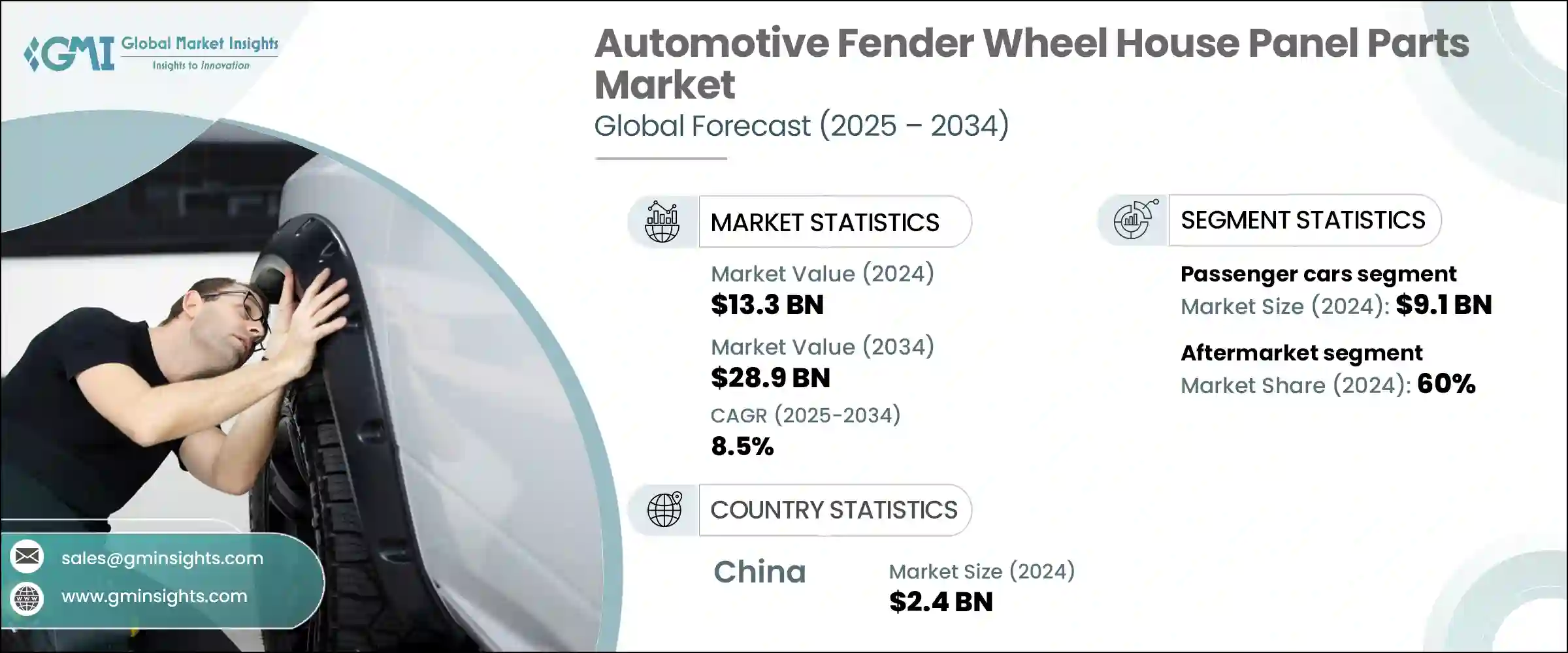

2024年,全球汽車翼子板和輪轂罩零件市場價值133億美元,預計到2034年將以8.5%的複合年成長率成長,達到289億美元。隨著汽車製造商越來越注重車輛效率、安全性能和設計創新,該市場正在穩步擴張。翼子板部件,包括襯裡、前後翼子板和輪圈罩面板,對於視覺吸引力和功能性能都至關重要。這些零件不僅有助於減少風阻、提高空氣動力學性能,還能保護車輛底部免受路面因素和碎屑的傷害。更嚴格的碰撞安全法規和設計要求使得它們在新車平台中變得更加重要,尤其是在汽車製造商追求更堅固、更符合空氣動力學的車輛結構的情況下。

汽車製造商正在從鋼材轉向複合材料、熱塑性塑膠和鋁等更輕的替代品,以減輕車輛總重。這種轉變對提高燃油效率至關重要,尤其是在電動車領域,更輕的結構可以延長續航里程。空氣動力學面板的趨勢也影響產品開發,因為光滑的擋泥板輪廓和一體式輪拱可以改善氣流並降低能耗。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 133億美元 |

| 預測值 | 289億美元 |

| 複合年成長率 | 8.5% |

這些改進對於電動和高性能車型尤其有益,因為降噪和效率是這些車型的賣點。隨著製造商不斷適應國際能源標準,模組化組裝技術也日益普及,允許將多個組件整合到單一單元中,從而加快製造速度並簡化安裝。

2024年,乘用車市場產值達91億美元。該市場持續蓬勃發展,尤其是在拉丁美洲和亞太等個人出行日益普及的地區。轎車、SUV和掀背車等乘用車類型越來越依賴流線型設計、空氣動力學造型和更輕的材料,這推動了對增強型擋泥板系統的需求。電動和混合動力乘用車的興起也重塑了擋泥板的設計要求,因為新型車輛需要更輕、結構更獨特的面板配置。此外,為了滿足嚴格的噪音標準並提供更好的道路碎屑防護,製造商正在開發兼具功能性和安全性的多層擋泥板。

2024年,售後市場佔了60%的市佔率。由於輕微事故、車輛老化或磨損後對替換零件的需求持續成長,該領域持續成長。輪罩板和擋泥板等車身外部零件是更換頻率最高的零件之一,尤其是在容易出現惡劣天氣或交通擁擠的地區。消費者被線上通路、獨立門市和本地供應商提供的種類繁多、經濟實惠的售後配件所吸引。售後市場也能讓消費者以實惠的價格定製或維修車輛,尤其是在汽車保有量高但保固期有限的地區。

2024年,中國汽車翼子板輪轂罩零件市場規模達24億美元。受不斷成長的消費需求和持續的汽車生產投資推動,中國仍然是汽車製造業的強國,尤其是在乘用車和電動車領域。在政府的大力支持和國家能源目標的支持下,中國大力推動電動車發展,鼓勵在汽車零件中使用先進材料和空氣動力學設計。中國強大的供應鏈和經濟高效的生產能力是其關鍵優勢,使其成為金屬和複合材料翼板零件的主要出口國。

全球汽車翼板輪圈罩零件市場的知名市場參與者包括科世達集團、法雷奧公司、矢崎株式會社、Flex-N-Gate 公司、李爾公司、麥格納國際公司、愛信精機株式會社等。汽車翼子板輪轂罩零件市場的領先公司正專注於創新材料開發和先進製造技術,以保持競爭力。許多公司正在投資輕質複合材料技術和模組化面板系統,以縮短組裝時間並提高車輛空氣動力學性能。與電動車製造商的合作使供應商能夠根據電動傳動系統和結構佈局來客製化零件。企業也在擴大新興市場的生產,以滿足不斷成長的區域需求並降低成本。為了迎合售後市場的需求,企業正在透過推出可客製化、耐用且價格合理的零件來實現產品多樣化。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 對部隊的影響

- 成長動力

- 車輛複雜性和電子控制單元整合度不斷提高

- ADAS 和基於感測器的安全系統的進步

- 連網汽車技術的發展使遠端診斷成為可能

- 需要專業維護的電動和混合動力汽車日益普及

- 產業陷阱與挑戰

- 先進診斷工具和設備的高初始投資

- 缺乏接受過電動車和 ADAS 技術培訓的熟練技術人員

- 市場機會

- 基於人工智慧的預測性維護系統的開發

- 透過智慧診斷擴展行動平台

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 前擋泥板

- 擋泥板襯裡

- 後擋泥板

- 輪罩板

- 內擋泥板

第6章:市場估計與預測:依資料,2021 - 2034 年

- 主要趨勢

- 鋼

- 塑膠

- 鋁

- 合成的

- 碳纖維

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 掀背車

- 越野車

- 商用車

- 輕型商用車

- 中型商用車

- 重型商用車

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 汽車零件分銷商和批發商

- 車隊營運商

- 政府和市政機構

- 專用車輛製造商

- DIY 愛好者和業餘愛好者

- 其他

第9章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- 售後市場

- OEM

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Aisin Seiki

- Dongfeng Liuzhou

- Dongfeng Motor

- Ficosa International

- Flex-N-Gate

- Gestamp Automocion

- Hyundai Mobis

- Inteva Products

- Kostal

- Lear Corporation

- Magna International

- Martinrea International

- Plastic Omnium

- Sanden

- Siemens

- Schaeffler

- Toyoda Gosei

- Toyota Boshoku

- Valeo

- Yazaki

The Global Automotive Fender Wheel House Panel Parts Market was valued at USD 13.3 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 28.9 billion by 2034. The market is experiencing steady expansion as automakers increasingly focus on vehicle efficiency, safety features, and design innovation. Fender components, including liners, front and rear fenders, and wheel house panels, are essential for both visual appeal and functional performance. These parts not only help reduce wind resistance and increase aerodynamics but also protect vehicles' underbodies from road elements and debris. Stricter crash safety regulations and design demands have made them more critical in new vehicle platforms, especially as carmakers aim for stronger, more aerodynamic vehicle builds.

Automotive manufacturers are transitioning from steel to lighter alternatives like composites, thermoplastics, and aluminum to reduce overall vehicle weight. This shift plays a critical role in supporting fuel efficiency, which is especially vital in the electric vehicle space, where lighter structures can boost driving range. The trend toward aerodynamic paneling is also shaping product development, as smooth fender contours and integrated wheel arches improve airflow and reduce energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.3 Billion |

| Forecast Value | $28.9 Billion |

| CAGR | 8.5% |

These enhancements are particularly beneficial for electric and high-performance models, where noise reduction and efficiency are selling points. As manufacturers continue adapting to international energy standards, modular assembly techniques are also gaining ground, allowing multiple components to be integrated into single units for quicker manufacturing and easier installation.

The passenger vehicles segment generated USD 9.1 billion in 2024. This segment continues to thrive, particularly in regions like Latin America and the Asia Pacific, where personal mobility is on the rise. Passenger vehicle types such as sedans, SUVs, and hatchbacks increasingly rely on sleek designs, aerodynamic styling, and lighter materials, driving up demand for enhanced fender systems. The rise of electric and hybrid passenger models is also reshaping Fender design requirements, as newer vehicles require lighter and structurally unique panel configurations. Additionally, the need to meet strict noise standards and provide better protection from road debris is encouraging manufacturers to develop multilayered fender panels that serve both functional and safety roles.

In 2024, the aftermarket segment held a 60% share. This sector continues to grow due to the consistent demand for replacement parts following minor accidents, aging vehicles, or wear and tear. Exterior body parts like wheel house panels and fenders are among the most replaced, especially in areas prone to harsh weather or heavy traffic. Consumers are drawn to the wide selection of cost-effective aftermarket options offered through online channels, independent shops, and local suppliers. The aftermarket also enables consumers to customize or repair their vehicles affordably, particularly in areas with high car ownership but limited warranties.

China Automotive Fender Wheel House Panel Parts Market generated USD 2.4 billion in 2024. The country remains a powerhouse in vehicle manufacturing, particularly in the passenger and EV categories, fueled by growing consumer demand and continued investment in automotive production. China's push toward electric mobility, backed by strong government support and national energy goals, is encouraging the use of advanced materials and aerodynamic designs in vehicle parts. The country's robust supply chain and cost-effective production capabilities are key advantages, making it a leading exporter of both metal and composite fender parts.

Notable market participants in the Global Automotive Fender Wheel House Panel Parts Market include Kostal Group, Valeo S.A., Yazaki Corporation, Flex-N-Gate Corporation, Lear Corporation, Magna International Inc., Aisin Seiki Co., Ltd., among others. Leading companies in the automotive fender wheel house panel parts market are focusing on innovative material development and advanced manufacturing techniques to stay competitive. Many are investing in lightweight composite technologies and modular panel systems that improve assembly time and vehicle aerodynamics. Partnerships with EV manufacturers allow suppliers to tailor parts to electric drivetrains and structural layouts. Firms are also expanding production in emerging markets to meet growing regional demand and reduce costs. To cater to the aftermarket, businesses are diversifying their offerings by introducing customizable, durable, and affordable components.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing vehicle complexity and integration of electronic control units

- 3.2.1.2 Advancements in ADAS and sensor-based safety systems

- 3.2.1.3 Growth in connected car technologies enabling remote diagnostics

- 3.2.1.4 Rising adoption of electric and hybrid vehicles requiring specialized maintenance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment in advanced diagnostic tools and equipment

- 3.2.2.2 Shortage of skilled technicians trained in EVs and ADAS technologies

- 3.2.3 Market Opportunities

- 3.2.3.1 Development of AI-based predictive maintenance systems

- 3.2.3.2 Expansion of mobile platforms with smart diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front fender panels

- 5.3 Fender liners

- 5.4 Rear fender panels

- 5.5 Wheel house panels

- 5.6 Inner fender panels

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Plastic

- 6.4 Aluminum

- 6.5 Composite

- 6.6 Carbon Fiber

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUV

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles

- 7.3.2 Medium Commercial Vehicles

- 7.3.3 Heavy Commercial Vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Automotive part distributor and wholesaler

- 8.3 Fleet operators

- 8.4 Government and municipal bodies

- 8.5 Specialty vehicle manufacturers

- 8.6 DIY enthusiasts and hobbyists

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Aftermarket

- 9.3 OEM

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Dongfeng Liuzhou

- 11.3 Dongfeng Motor

- 11.4 Ficosa International

- 11.5 Flex-N-Gate

- 11.6 Gestamp Automocion

- 11.7 Hyundai Mobis

- 11.8 Inteva Products

- 11.9 Kostal

- 11.10 Lear Corporation

- 11.11 Magna International

- 11.12 Martinrea International

- 11.13 Plastic Omnium

- 11.14 Sanden

- 11.15 Siemens

- 11.16 Schaeffler

- 11.17 Toyoda Gosei

- 11.18 Toyota Boshoku

- 11.19 Valeo

- 11.20 Yazaki