|

市場調查報告書

商品編碼

1773369

航太緊固件市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Aerospace Fasteners Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

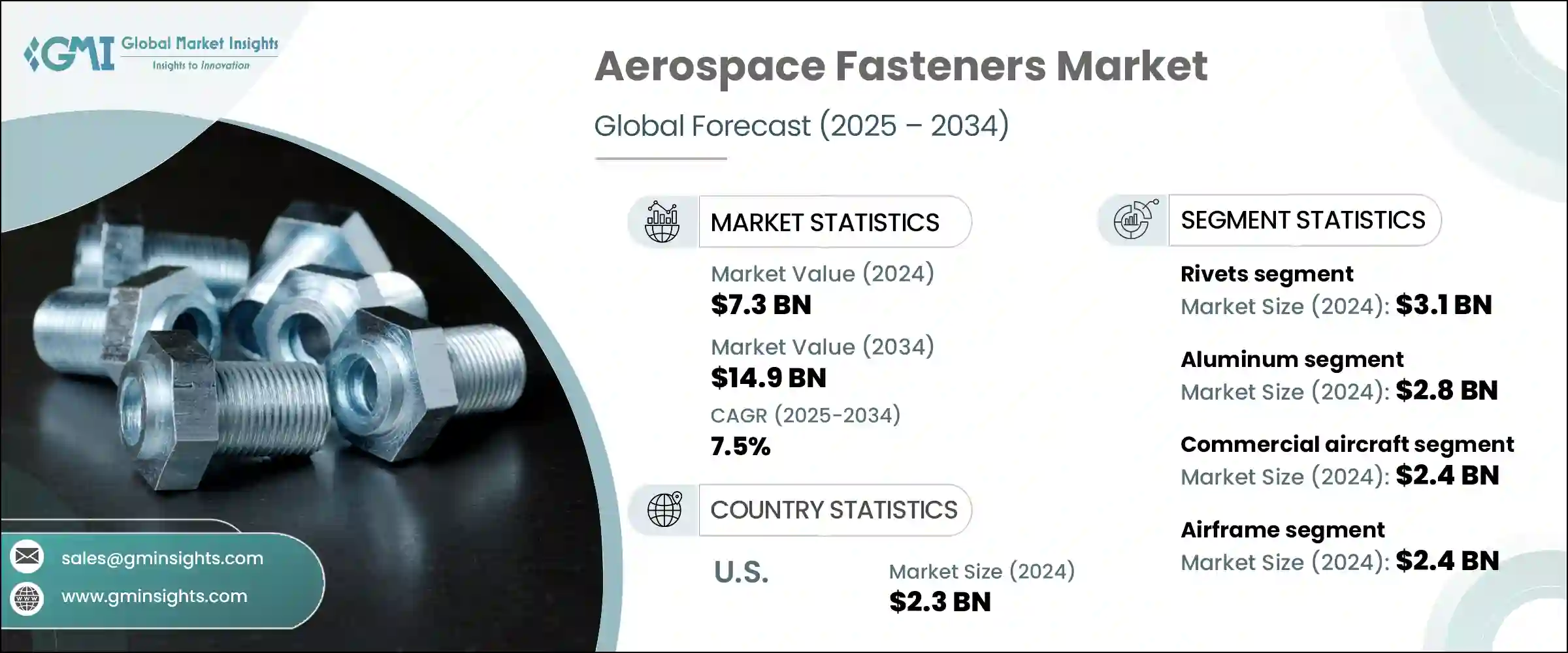

2024年,全球航太緊固件市場規模達73億美元,預計到2034年將以7.5%的複合年成長率成長,達到149億美元。這一強勁的成長軌跡與商用航空機隊的快速擴張以及軍用航空基礎設施的持續升級密切相關。新興經濟體日益成長的航空旅行需求,加上國防投資的不斷增加,正推動著過時的飛機零件被更新、更輕巧、更高性能的替代方案所取代。燃油效率和耐用性的重要性日益提升,使航太緊固件成為結構部件製造創新的核心,使其成為原始設備製造商(OEM)組裝和售後服務中不可或缺的一部分。

全球貿易格局對該市場產生了重大影響。先前針對進口航空級鋁和鋼(尤其是來自中國的鋁和鋼)徵收的關稅導致原料成本上升,並限制了關鍵零件的取得。這些干擾迫使美國製造商重新考慮採購策略,許多製造商轉向國內供應商或多元化供應商組合,以最大程度地降低風險。這些措施旨在抵消成本壓力,同時在緊湊的製造生態系統中保持交付時間。隨著輕量化設計和增強結構可靠性的持續發展,製造商正專注於能夠與複合材料無縫配合的緊固件。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 73億美元 |

| 預測值 | 149億美元 |

| 複合年成長率 | 7.5% |

2024年,鉚釘市場產值達31億美元。鉚釘因其在提供輕質耐用的接頭方面發揮重要作用,而這些接頭對於維護機身完整性至關重要,因此保持了市場主導地位。這些緊固件廣泛應用於商用飛機生產,特別適用於機翼和機身等高振動、高承重區域。鉚釘安裝技術的進步,尤其是盲鉚釘技術,進一步提高了效率和可靠性,使其成為原始設備製造OEM)製造和日常維護作業中不可或缺的一部分。

2024年,航太緊固件市場中的鋁材市場價值將達28億美元。鋁材因其優異的強度重量比、耐腐蝕性和成本效益而廣受歡迎,使其成為減輕飛機重量和提高燃油經濟性的首選材料。隨著飛機設計越來越注重減重,對鋁材緊固件的需求持續攀升,尤其是在非關鍵結構應用和內裝零件方面。增強的鋁合金配方也提高了材料與現代複合材料結構的兼容性,推動了製造和服務部門對鋁材的採用。

2024年,美國航太緊固件市場產值達23億美元。美國佔據主導地位,得益於其全球航太樞紐的地位,匯集了許多領先的商用和國防航空製造商。該領域的主要參與者持續透過持續的機隊維護和下一代系統的整合來刺激國內需求。美國還擁有全球最全面的MRO網路之一,為大型民用和軍用機隊的定期維護週期和系統升級提供支援。國防開支的不斷成長,主要集中在下一代轟炸機和高超音速飛機等戰略空中能力,加劇了對鈦合金、高溫因科鎳合金和碳基複合材料製成的專用緊固件的需求。

積極影響航太航太緊固件市場的關鍵參與者包括 TriMas Corporation、波音、LISI 航太 、Wurth Group、B& 航太 Specialties Inc.、Cherry 航太、Precision Castparts Corp.、National 航太 Fasteners Corporation、Preci-Manufacturing、Stanley Black & Decker Inc.、MS 航太 Inc.為了增強競爭優勢,航太緊固件產業的公司正在採取幾項關鍵策略。他們正在大力投資研發更輕、耐腐蝕且在極端條件下也能可靠運作的緊固件。與飛機原始設備製造商的策略合作有助於確保儘早整合到新的平台設計中。此外,該公司還專注於透過在地化製造和數位採購系統最佳化供應鏈,以最大限度地減少中斷。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 全球空中交通量增加和機隊擴張

- 軍用飛機現代化浪潮

- MRO(維修、維修和大修)服務的成長

- 採用先進的製造技術

- 太空探索和衛星發射的興起

- 產業陷阱與挑戰

- 先進緊固件材料成本高

- 嚴格的監管和認證要求

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 未來市場趨勢

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 國防預算分析

- 全球國防開支趨勢

- 區域國防預算分配

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 重點國防現代化項目

- 預算預測(2025-2034)

- 對產業成長的影響

- 各國國防預算

- 供應鏈彈性

- 地緣政治分析

- 勞動力分析

- 數位轉型

- 合併、收購和策略夥伴關係格局

- 風險評估與管理

- 主要合約授予(2021-2024)

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各地區市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:依產品類型,2021 年至 2034 年

- 主要趨勢

- 鉚釘

- 螺絲

- 螺帽和螺栓

- 其他

第6章:市場估計與預測:按材料,2021 年至 2034 年

- 主要趨勢

- 鋁

- 鋼

- 高溫合金

- 鈦

第7章:市場估計與預測:按平台,2021 年至 2034 年

- 主要趨勢

- 商用飛機

- 窄體飛機

- 寬體飛機

- 支線噴射機

- 軍用機

- 公務機

- 直升機

- 無人駕駛飛行器(UAV)

第 8 章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 機體

- 內飾

- 引擎

- 控制面

- 起落架

- 其他

第9章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- OEM (原始設備製造商)

- MRO(維修、修理和大修)

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- B&B Specialties Inc.

- Boeing

- Bollhoff Group

- Cherry Aerospace

- Howmet Aerospace Inc.

- LISI Aerospace

- MS Aerospace

- National Aerospace Fasteners Corporation

- Preci-Manufacturing

- Precision Castparts Corp.

- Stanley Black & Decker, Inc.

- TriMas Corporation

- Wurth Group

The Global Aerospace Fasteners Market was valued at USD 7.3 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 14.9 billion by 2034. This robust growth trajectory is closely tied to the rapid expansion of commercial airline fleets and the continuous upgrades in military aviation infrastructure. Rising air travel demand across emerging economies, coupled with increasing investments in national defense, is fueling the replacement of outdated aircraft components with newer, lightweight, and high-performance alternatives. The growing importance of fuel efficiency and durability has placed aerospace fasteners at the center of innovation in structural component manufacturing, making them essential in both OEM assembly and aftermarket servicing.

The global trade landscape has had a significant influence on this market. Previous tariffs targeting imported aerospace-grade aluminum and steel-especially those from China-led to elevated raw material costs and constrained access to essential components. These disruptions forced US-based manufacturers to rethink sourcing strategies, with many turning to domestic suppliers or diversifying vendor portfolios to minimize risk. These actions aimed to offset cost pressures while maintaining delivery timelines in a tightly scheduled manufacturing ecosystem. With an ongoing shift toward lightweight design and enhanced structural reliability, manufacturers are focusing on fasteners that can work seamlessly with composite materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.3 Billion |

| Forecast Value | $14.9 Billion |

| CAGR | 7.5% |

The rivets segment generated USD 3.1 billion in 2024. Rivets maintain dominance due to their essential role in delivering lightweight yet durable joints that are critical in maintaining airframe integrity. These fasteners are widely used in commercial aircraft production, particularly for high-vibration, load-bearing areas such as wings and fuselages. Advances in rivet installation-particularly blind rivet technology-have further increased efficiency and reliability, making them indispensable across both OEM manufacturing and ongoing maintenance operations.

Aluminum segment in the aerospace fasteners segment in 2024, valued at USD 2.8 billion. Its popularity stems from a superior strength-to-weight ratio, corrosion resistance, and cost-effectiveness, making it the material of choice for reducing aircraft mass and improving fuel economy. As aircraft designs increasingly focus on weight reduction, demand for aluminum fasteners continues to climb, particularly in non-critical structural applications and interior components. Enhanced aluminum alloy formulations are also boosting material compatibility with modern composite structures, driving adoption across both manufacturing and servicing divisions.

United States Aerospace Fasteners Market generated USD 2.3 billion in 2024. The country's dominance can be traced to its position as a global aerospace hub, home to leading manufacturers across commercial and defense aviation. Major players in this space continue to fuel domestic demand with both ongoing fleet maintenance and the integration of next-generation systems. The U.S. also hosts one of the world's most comprehensive MRO networks, supporting regular service cycles and system upgrades for large civilian and military fleets. Rising defense expenditures, focused on strategic air capabilities such as next-gen bombers and hypersonic aircraft, have intensified demand for specialized fasteners made from titanium alloys, high-temperature Inconel, and carbon-based composites.

Key players actively shaping the Aerospace Fasteners Market include TriMas Corporation, Boeing, LISI Aerospace, Wurth Group, B&B Specialties Inc., Cherry Aerospace, Precision Castparts Corp., National Aerospace Fasteners Corporation, Preci-Manufacturing, Stanley Black & Decker Inc., M.S Aerospace, Bollhoff Group, and Howmet Aerospace Inc. To enhance their competitive edge, companies in the aerospace fasteners industry are adopting several key strategies. They're investing heavily in R&D to develop lighter, corrosion-resistant fasteners that perform reliably under extreme conditions. Strategic collaborations with aircraft OEMs help ensure early integration into new platform designs. Additionally, firms are focusing on supply chain optimization through localized manufacturing and digital procurement systems to minimize disruptions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Material trends

- 2.2.3 Platform trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO Perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing global air traffic & fleet expansion

- 3.2.1.2 Surge in military aircraft modernization

- 3.2.1.3 Growth in MRO (maintenance, repair, and overhaul) services

- 3.2.1.4 Adoption of advanced manufacturing technologies

- 3.2.1.5 Rising space exploration & satellite launches

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced fastener materials

- 3.2.2.2 Stringent regulatory and certification requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Defense budget analysis

- 3.14 Global defense spending trends

- 3.15 Regional defense budget allocation

- 3.15.1 North America

- 3.15.2 Europe

- 3.15.3 Asia Pacific

- 3.15.4 Middle East and Africa

- 3.15.5 Latin America

- 3.16 Key defense modernization programs

- 3.17 Budget forecast (2025-2034)

- 3.17.1 Impact on industry growth

- 3.17.2 Defense budgets by country

- 3.18 Supply chain resilience

- 3.19 Geopolitical analysis

- 3.20 Workforce analysis

- 3.21 Digital transformation

- 3.22 Mergers, acquisitions, and strategic partnerships landscape

- 3.23 Risk assessment and management

- 3.24 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Rivets

- 5.3 Screws

- 5.4 Nuts & bolts

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 Aluminum

- 6.3 Steel

- 6.4 Superalloys

- 6.5 Titanium

Chapter 7 Market Estimates and Forecast, By Platform, 2021 – 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Commercial aircraft

- 7.2.1 Narrow-body

- 7.2.2 Wide-body

- 7.2.3 Regional jets

- 7.3 Military aircraft

- 7.4 Business jets

- 7.5 Helicopters

- 7.6 Unmanned aerial vehicles (UAVs)

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 Airframe

- 8.3 Interiors

- 8.4 Engine

- 8.5 Control surfaces

- 8.6 Landing gear

- 8.7 Other

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Million & Million Units)

- 9.1 Key trends

- 9.2 OEM (Original Equipment Manufacturers)

- 9.3 MRO (Maintenance, Repair, and Overhaul)

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 B&B Specialties Inc.

- 11.2 Boeing

- 11.3 Bollhoff Group

- 11.4 Cherry Aerospace

- 11.5 Howmet Aerospace Inc.

- 11.6 LISI Aerospace

- 11.7 M.S Aerospace

- 11.8 National Aerospace Fasteners Corporation

- 11.9 Preci-Manufacturing

- 11.10 Precision Castparts Corp.

- 11.11 Stanley Black & Decker, Inc.

- 11.12 TriMas Corporation

- 11.13 Wurth Group

航太緊固件市場:按緊固件類型、材質、應用、飛機類型、最終用途和分銷管道分類-2026-2032年全球市場預測

航太緊固件市場:按緊固件類型、材質、應用、飛機類型、最終用途和分銷管道分類-2026-2032年全球市場預測 2026年全球航太緊固件市場報告

2026年全球航太緊固件市場報告 全球航太緊固件市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球航太緊固件市場規模、佔有率、趨勢和成長分析報告(2026-2034) 飛機內裝緊固件市場-全球產業規模、佔有率、趨勢、機會和預測:按飛機類型、應用類型、緊固件類型、地區和競爭格局分類,2021-2031年飛機塑膠緊固件市場 - 全球產業規模、佔有率、趨勢、機會及預測(按飛機類型、材料類型、產品類型、地區和競爭格局分類,2021-2031年)

飛機內裝緊固件市場-全球產業規模、佔有率、趨勢、機會和預測:按飛機類型、應用類型、緊固件類型、地區和競爭格局分類,2021-2031年飛機塑膠緊固件市場 - 全球產業規模、佔有率、趨勢、機會及預測(按飛機類型、材料類型、產品類型、地區和競爭格局分類,2021-2031年) 航太緊固件市場按產品、材質、平台和地區分類航太緊固件市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、材料類型、地區和競爭格局分類,2021-2031年預測

航太緊固件市場按產品、材質、平台和地區分類航太緊固件市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、材料類型、地區和競爭格局分類,2021-2031年預測 航太緊固件市場規模、佔有率和成長分析(按產品類型、材料、應用和地區分類):產業預測(2026-2033 年)

航太緊固件市場規模、佔有率和成長分析(按產品類型、材料、應用和地區分類):產業預測(2026-2033 年) 太陽能緊固件市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場預測,2025 年至 2033 年美國航太緊固件市場規模、佔有率和趨勢分析報告:按飛機類型、產品和細分市場預測,2025 年至 2033 年

太陽能緊固件市場規模、佔有率和趨勢分析報告:按產品、最終用途、地區和細分市場預測,2025 年至 2033 年美國航太緊固件市場規模、佔有率和趨勢分析報告:按飛機類型、產品和細分市場預測,2025 年至 2033 年