|

市場調查報告書

商品編碼

1773368

完整預混料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Complete Premixes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

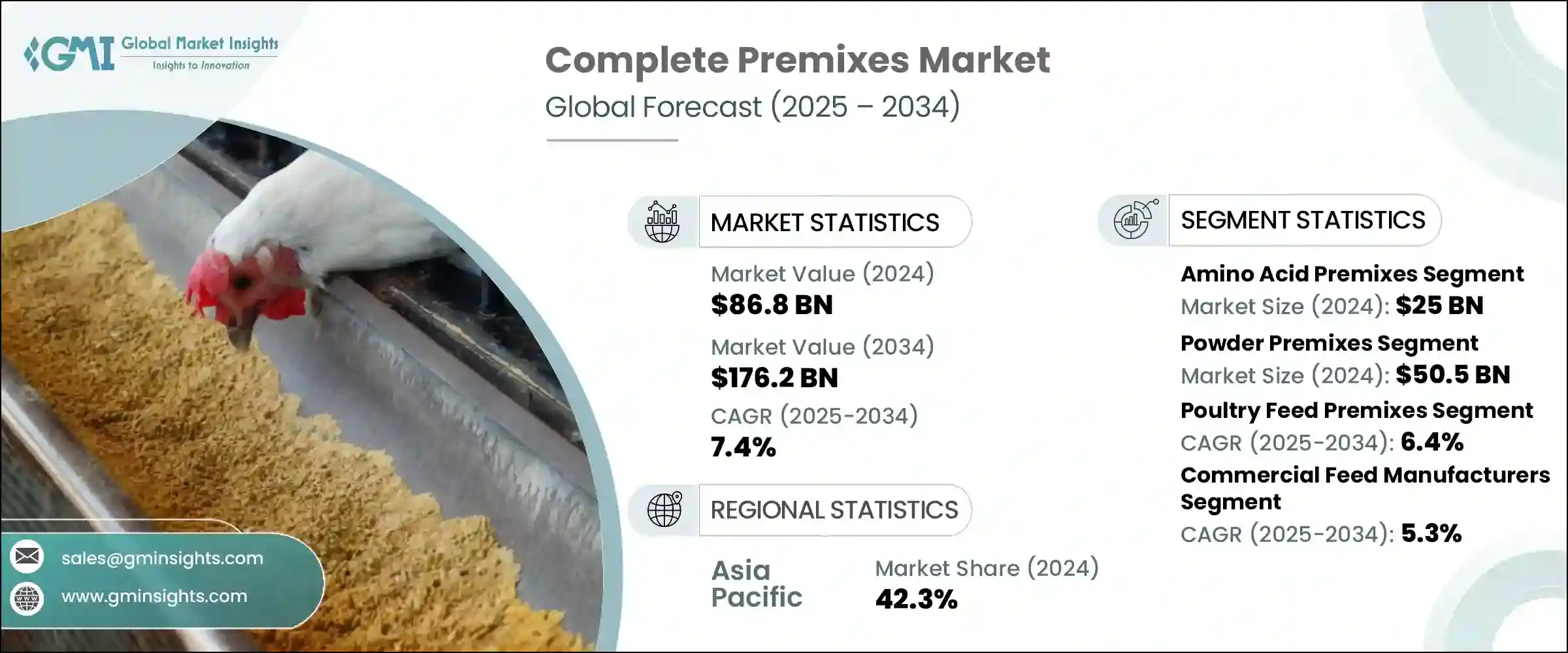

2024年,全球全價預混料市場規模達868億美元,預計2034年將以7.4%的複合年成長率成長,達到1762億美元。全價預混料是精心調配的混合料,含有維生素、礦物質、胺基酸、酵素和其他功能性成分等必需營養素,可確保寵物和人類食品的營養成分精準均衡。這些預混料在改善動物健康、促進生長、增強免疫力和提高生產力方面發揮重要作用。此外,它們也有助於解決強化食品體系中的微量營養素缺乏問題。由於技術進步、高蛋白飲食的興起以及人們對健康和營養的意識不斷增強,全球全價預混料市場正在蓬勃發展。

商業化畜牧養殖的興起、客製化寵物營養需求的不斷成長以及發展中國家食品強化計畫的實施,推動了市場的成長機會。此外,對有機、專用和非基因改造預混料(包括藥物混合料)的需求也不斷成長。由於城鎮化和營養計畫對健康食品產業的支持,亞太、非洲和拉丁美洲等新興市場的需求正在不斷成長。預計在整個預混料行業配方和自動化創新的推動下,市場將實現長期成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 868億美元 |

| 預測值 | 1762億美元 |

| 複合年成長率 | 7.4% |

2024年,胺基酸預混料市場佔28.8%的市場佔有率,價值250億美元。由於對離胺酸、蛋氨酸和蘇氨酸等必需氨基酸的需求不斷成長,該市場將繼續佔據主導地位。這些氨基酸用於家禽和豬飼料中,以提高生長率和飼料轉換率。非必需胺基酸也因其在支持代謝過程中的作用而越來越受歡迎。農業領域對蛋白質平衡和精準營養的日益關注,促進了該市場的擴張。

2024年,粉末預混料市場以58.1%的市佔率領先市場,價值達505億美元。粉末預混料因其保存期限長、運輸便捷、配料精準和成本效益高而備受青睞。它們廣泛應用於牲畜飼料、寵物食品和人類營養,特別用於乾飼料和速食配方。粉末預混料也相容於批量混合系統,使其成為商業飼料製造商和農場混合作業的理想選擇。

2024年,亞太地區全功能預混料市場佔據42.3%的市佔率。該地區畜牧業的蓬勃發展、對強化營養產品的需求以及政府支持的旨在改善食品安全和飼料效率的項目,是推動市場成長的關鍵因素。此外,可支配收入的提高、人口的成長以及水產養殖和寵物食品的日益普及等因素,也推動了食品和飼料行業對高品質功能性預混料的需求。

Nutreco NV、帝斯曼-芬美意、嘉吉公司、巴斯夫和阿徹丹尼爾斯米德蘭公司 (ADM) 等公司憑藉創新和分銷引領市場。他們持續投入研發,並建立強大的全球分銷管道,鞏固了在全價預混料市場的地位。為了鞏固市場地位,全價預混料產業的領先公司專注於多種策略,包括與關鍵供應商建立策略合作夥伴關係、加強研發力度以打造客製化和有機預混料,以及透過收購和合併擴大地域覆蓋範圍。他們還透過非基因改造和藥物混合等專業解決方案來增強產品供應。生產流程的自動化和智慧混合技術的引入進一步幫助企業簡化營運並提高效率。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 維生素預混料

- 脂溶性與水溶性

- 礦物質預混料

- 宏觀與微觀礦物分割

- 螯合物與無機物形式

- 氨基酸預混料

- 必需胺基酸與非必需胺基酸

- 完整的維生素礦物質預混料

- 定製配方與標準配方

- 特種預混料

- 有機預混料

- 非基因改造預混料

- 藥物預混料

- 效能增強預混料

第6章:市場估計與預測:依形式,2021 - 2034 年

- 主要趨勢

- 粉末預混料

- 液體預混料

- 顆粒預混料

- 顆粒狀預混料

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 家禽飼料預混料

- 豬飼料預混料

- 反芻動物飼料預混料

- 水產養殖飼料預混料

- 寵物食品預混料

- 其他應用

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 商業飼料製造商

- 畜牧業整合商

- 農場攪拌機

- 寵物食品製造商

- 特種飼料生產商

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第10章:公司簡介

- DSM-Firmenich

- Cargill, Incorporated

- Archer Daniels Midland Company (ADM)

- Nutreco NV

- BASF SE

- Glanbia Nutritionals

- Alltech Inc.

- Kemin Industries

- Biomin Holding GmbH

- Lallemand Inc.

The Global Complete Premixes Market was valued at USD 86.8 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 176.2 billion by 2034. Complete premixes are meticulously blended mixtures containing essential nutrients such as vitamins, minerals, amino acids, enzymes, and other functional ingredients that ensure precise and uniform nutrition in both pet and human foods. These premixes play a significant role in improving animal health, supporting growth, enhancing immunity, and boosting productivity. Additionally, they help address micronutrient deficiencies in fortified food systems. The market for complete premixes is gaining momentum globally due to advancements in technology, a rise in protein-rich diets, and increased awareness surrounding health and nutrition.

Growth opportunities in the market are being driven by the rise of commercial livestock farming, the growing demand for customized pet nutrition, and food fortification initiatives in developing nations. There is also an increasing demand for organic, specialized, and non-GMO premixes, including medicated blends. Emerging markets in regions such as Asia-Pacific, Africa, and Latin America are seeing rising demand due to urbanization and nutritional initiatives supporting the health food sector. The market is expected to experience long-term growth fueled by innovations in formulation and automation within the complete premixes industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $86.8 Billion |

| Forecast Value | $176.2 Billion |

| CAGR | 7.4% |

The amino acid premixes segment held a 28.8% share in 2024, valued at USD 25 billion. This segment continues to dominate due to the rising need for essential amino acids, such as lysine, methionine, and threonine, used in poultry and swine feeds to improve growth and feed conversion rates. Non-essential amino acids are also gaining popularity for their role in supporting metabolic processes. The increasing focus on protein balance and precision nutrition within the agricultural sector has contributed to the segment's expansion.

The powder premixes segment led the market with a 58.1% share in 2024, valued at USD 50.5 billion. Powdered premixes are highly favored due to their long shelf life, ease of transportation, precise dosing, and cost-effectiveness. They are extensively used in livestock feed, pet foods, and human nutrition, particularly in dry feed and instant food formulations. Powdered premixes are also compatible with bulk mixing systems, making them ideal for commercial feed manufacturers and on-farm mixing operations.

Asia-Pacific Complete Premixes Market held a 42.3% share in 2024. The region's growing livestock sector, demand for fortified nutrition products, and government-backed programs aimed at improving food security and feed efficiency are key factors driving the market's growth. Additionally, factors such as rising disposable incomes, an expanding population, and the increasing popularity of aquaculture and pet foods contribute to the demand for high-quality functional premixes in both the food and feed sectors.

Companies like Nutreco N.V., DSM-Firmenich, Cargill Incorporated, BASF SE, and Archer Daniels Midland Company (ADM) lead the market through innovation and distribution. Their continued investment in research and development, along with the establishment of strong global distribution channels, has helped solidify their presence in the complete premixes market. To strengthen their market positions, leading companies in the complete premixes industry focus on a variety of strategies. These include strategic partnerships with key suppliers, increasing their R&D efforts to create customized and organic premixes, and expanding their geographic reach through acquisitions and mergers. They are also enhancing product offerings with specialized solutions such as non-GMO and medicated blends. Automation of production processes and the introduction of smart blending technologies further help companies streamline operations and improve efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Form

- 2.2.4 Application

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Vitamin premixes

- 5.2.1 Fat-soluble vs water-soluble

- 5.3 Mineral premixes

- 5.3.1 Macro vs micro mineral segmentation

- 5.3.2 Chelated vs inorganic forms

- 5.4 Amino acid premixes

- 5.4.1 Essential vs non-essential amino acids

- 5.5 Complete vitamin-mineral premixes

- 5.5.1 Customized vs standard formulations

- 5.6 Specialty premixes

- 5.6.1 Organic premixes

- 5.6.2 Non-GMO premixes

- 5.6.3 Medicated premixes

- 5.6.4 Performance enhancement premixes

Chapter 6 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Powder premixes

- 6.3 Liquid premixes

- 6.4 Granular premixes

- 6.5 Pelletized premixes

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Poultry feed premixes

- 7.3 Swine feed premixes

- 7.4 Ruminant feed premixes

- 7.5 Aquaculture feed premixes

- 7.6 Pet food premixes

- 7.7 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Commercial feed manufacturers

- 8.3 Livestock integrators

- 8.4 On-farm mixers

- 8.5 Pet food manufacturers

- 8.6 Specialty feed producers

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 DSM-Firmenich

- 10.2 Cargill, Incorporated

- 10.3 Archer Daniels Midland Company (ADM)

- 10.4 Nutreco N.V.

- 10.5 BASF SE

- 10.6 Glanbia Nutritionals

- 10.7 Alltech Inc.

- 10.8 Kemin Industries

- 10.9 Biomin Holding GmbH

- 10.10 Lallemand Inc.