|

市場調查報告書

商品編碼

1773350

醫療、法律和監管審查軟體市場機會、成長動力、行業趨勢分析和 2025 - 2034 年預測Medical, Legal, and Regulatory Review Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

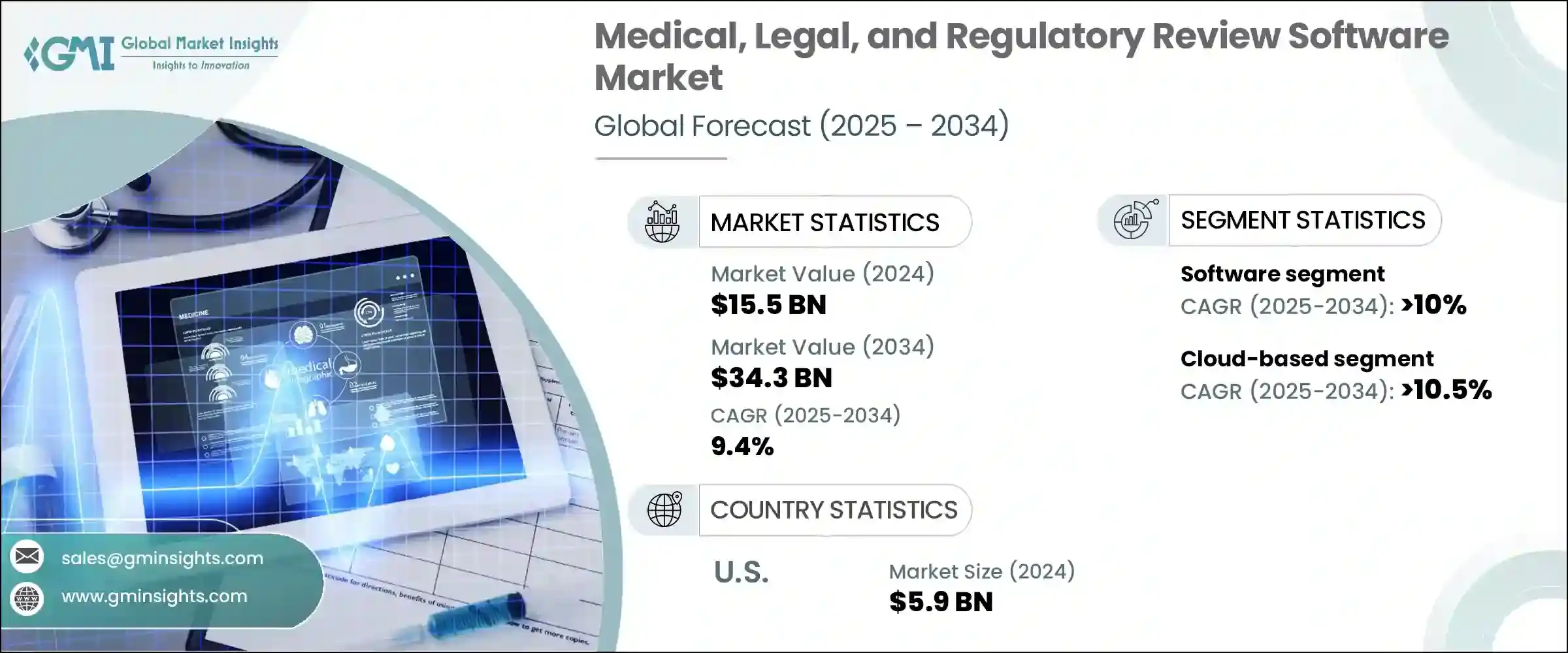

2024 年,全球醫療、法律和監管審查軟體市場規模達 155 億美元,預計到 2034 年將以 9.4% 的複合年成長率成長,達到 343 億美元。製藥和生命科學領域對合規、協作和情境感知內容審查流程日益成長的需求,推動了這一穩步成長軌跡。隨著企業加速數位化策略並應對複雜的監管框架,對能夠簡化審查工作流程的整合 MLR 平台的需求顯著成長。傳統上,許多生命科學組織依賴手動、紙本或電子郵件驅動的 MLR 審查流程。然而,這些過時的系統正迅速被提供即時協作、基於人工智慧的合規性驗證和自動審計追蹤的智慧軟體工具所取代。這些功能正在幫助 MLR 團隊提高營運效率,降低法律風險,並更迅速、更自信地將產品推向市場。

隨著數位化和多通路行銷的日益普及,生命科學公司面臨快速審查和批准各種內容格式的壓力,同時還要確保符合區域監管要求。無論是網站、電子郵件或社群媒體平台的內容,人們越來越重視確保每項宣傳或科研資產都經過全面的合規性審查。 MLR 軟體系統作為一個集中式平台,可以管理這種複雜性,確保任何內容在公開發布之前均符合準確性、合法性和法規要求。向這些系統的轉變不僅是為了實現自動化,而是為了滿足快節奏、數位化互聯、不容有任何差錯的生態系統的期望。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 155億美元 |

| 預測值 | 343億美元 |

| 複合年成長率 | 9.4% |

從組件來看,軟體領域在2024年引領了全球MLR審查軟體市場,佔總市場價值的近68%。預計到2034年,該領域的複合年成長率將超過10%。提供版本控制、整合審計功能和協作內容審查功能的端到端數位工具的廣泛採用正在推動這一趨勢。企業擴大投資於基於雲端的平台,這些平台可以擴展到全球團隊,減少人工審查錯誤,並實現即時回饋循環。數位轉型的趨勢進一步鼓勵組織從分散的系統轉向統一的軟體生態系統,以支援跨多個利害關係人和團隊的大量內容。

從部署角度來看,基於雲端的解決方案在2024年佔據了市場主導地位,約佔總市場佔有率的64%。預計該細分市場在整個預測期內的複合年成長率將超過10.5%。向雲端基礎設施的廣泛遷移使製藥和生物技術公司能夠集中內容管理,簡化監管工作流程,並顯著降低內部IT維護成本。雲端平台提供跨部門和跨地區的一致、安全的訪問,確保利害關係人始終符合最新的監管指南。隨著公司拓展新市場,基於雲端的MLR工具提供了在多樣化且不斷變化的合規環境中運作所需的適應性和回應能力。

從功能角度來看,監管審查在2024年成為領先的細分市場。與主要關注科學可信度或智慧財產權保護的法律或醫學評估相比,監管審查的核心在於確保與特定地區的行銷、推廣和提交規則完全一致。為了滿足這些監管要求,越來越多的組織開始採用具備自動化功能的軟體解決方案,例如版本追蹤、內容標記、審計文件和監管資訊系統整合。這些功能不僅提高了審查週期的準確性和速度,還能確保所有資料都得到完整記錄且易於檢索,從而幫助組織為可能面臨的監管審計做好準備。

從地理分佈來看,美國在2024年佔據市場主導地位,貢獻了約59億美元的收入,佔北美地區88.3%的佔有率。這種主導地位可以歸因於聯邦機構施加的嚴格監管要求,這些要求要求內容在公開傳播之前必須經過嚴格驗證。隨著製藥和醫療器材公司尋求管理大量行銷和科研材料,同時最大限度地降低法律和合規風險,對先進的MLR軟體工具的依賴日益成長。先進的雲端系統和人工智慧整合平台的出現極大地支持了這一轉變。

MLR 審查軟體領域的領先供應商正在積極尋求策略合作夥伴關係、收購和產品創新,以擴展其能力和市場版圖。隨著監管複雜性的日益增加,各公司正在加倍投入研發,以建立更智慧的平台,從而支援更高的自動化程度、可追溯性和即時協作能力。關鍵投資領域包括基於人工智慧的合規性檢查、模組化內容工作流程以及雲端原生架構,這些架構使公司能夠適應全球監管的細微差別。供應商正致力於創建可配置的平台,以適應特定司法管轄區的準則,同時保持全球一致性,從而幫助生命科學組織最大限度地降低風險、加快核准速度並隨時準備跨地區審計。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率分析

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 轉向數位化和多通路行銷

- 雲端平台的採用率不斷上升

- 審查流程中的人工智慧和自動化

- 中小企業合規意識不斷增強

- 產業陷阱與挑戰

- 複雜的監管格局

- 資料隱私和合規風險

- 市場機會

- 製藥和生技研發線激增

- 遠端和分散協作日益增多

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 成本細分分析

- 軟體開發和授權成本

- 部署和整合成本

- 維護和支援成本

- 網路安全與合規成本

- 培訓和變更管理成本

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

- 用例

- 最佳情況

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按組件,2021 - 2034 年

- 主要趨勢

- 軟體

- 服務

- 專業的

- 託管

第6章:市場估計與預測:依部署模式,2021 - 2034 年

- 主要趨勢

- 基於雲端

- 本地

第7章:市場估計與預測:依功能分類,2021 - 2034 年

- 主要趨勢

- 醫療審查

- 法律審查

- 監管審查

第8章:市場估計與預測:依企業規模,2021 - 2034 年

- 主要趨勢

- 中小企業

- 大型企業

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 製藥公司

- 生技公司

- 醫療器材製造商

- 合約研究組織(CRO)

- 監理顧問公司

- 醫療保健行銷機構

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐人

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- 3M Health Information Systems

- Allscripts

- Change Healthcare

- Epic Systems

- Experian Health

- GE Healthcare

- Health Catalyst

- IBM Watson Health

- Inovalon Holdings

- LexisNexis Risk Solutions

- McKesson Corporation

- Medtronic

- Nuance Communications

- Optum

- Oracle Health

- Philips Healthcare

- Siemens Healthineers

- Thomson Reuters

- Verisk Analytics

- Wolters Kluwer

The Global Medical, Legal, and Regulatory Review Software Market was valued at USD 15.5 billion in 2024 and is estimated to grow at a CAGR of 9.4% to reach USD 34.3 billion by 2034. This steady growth trajectory is fueled by the rising need for compliant, collaborative, and context-aware content review processes within the pharmaceutical and life sciences sectors. As companies accelerate their digital strategies and navigate complex regulatory frameworks, the demand for integrated MLR platforms that streamline review workflows has grown significantly. Traditionally, many life sciences organizations relied on manual, paper-based, or email-driven MLR review processes. However, those outdated systems are rapidly being replaced by intelligent software tools offering real-time collaboration, AI-based compliance verification, and automated audit trails. These capabilities are helping MLR teams boost operational efficiency, reduce legal exposure, and bring products to market more swiftly and confidently.

With the increasing push for digital and multichannel marketing, life sciences companies are under pressure to rapidly review and approve diverse content formats while staying aligned with regional regulatory requirements. Whether it's content for websites, emails, or social media platforms, there is a growing emphasis on ensuring every promotional or scientific asset undergoes a thorough compliance review. MLR software systems serve as a centralized platform to manage this complexity, ensuring accuracy, legality, and regulatory adherence before any content reaches the public domain. The shift toward these systems is not just about automation; it's about meeting the expectations of a fast-paced, digitally connected ecosystem that leaves no room for error.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 9.4% |

In terms of components, the software segment led the global MLR review software market in 2024, accounting for nearly 68% of the total market value. This segment is anticipated to grow at a CAGR of over 10% through 2034. The expanding adoption of end-to-end digital tools that offer version control, integrated audit functionality, and collaborative content review features is driving this trend. Enterprises are increasingly investing in cloud-based platforms that can scale across global teams, reduce manual review errors, and enable real-time feedback loops. The preference for digital transformation has further encouraged organizations to move away from fragmented systems toward unified software ecosystems that support higher volumes of content across multiple stakeholders and teams.

From a deployment perspective, cloud-based solutions dominated the market in 2024, capturing approximately 64% of the total share. This segment is projected to register a CAGR exceeding 10.5% throughout the forecast period. The widespread shift to cloud infrastructure is allowing pharmaceutical and biotech companies to centralize content management, streamline regulatory workflows, and significantly reduce internal IT maintenance costs. Cloud platforms provide consistent, secure access across departments and geographies, ensuring that stakeholders remain aligned with current regulatory guidance at all times. As companies expand into new markets, cloud-based MLR tools provide the adaptability and responsiveness needed to operate within diverse and evolving compliance landscapes.

Functionality-wise, regulatory review emerged as the leading segment in 2024. Compared to legal or medical assessments, which primarily focus on scientific credibility or intellectual property protection, regulatory review is centered on ensuring full alignment with region-specific marketing, promotion, and submission rules. To meet these regulatory expectations, more organizations are turning to software solutions equipped with automation capabilities such as version tracking, content tagging, audit documentation, and regulatory information system integration. These features not only improve the accuracy and speed of the review cycle but also prepare organizations for possible regulatory audits by ensuring that all materials are thoroughly documented and easily retrievable.

Geographically, the United States dominated the market in 2024, contributing around USD 5.9 billion in revenue, which translates to a commanding 88.3% share of the North American region. This dominance can be attributed to the stringent regulatory requirements imposed by federal agencies, which demand that content undergo rigorous validation before public dissemination. The reliance on advanced MLR software tools is growing as pharmaceutical and medical device companies seek to manage high volumes of marketing and scientific materials while minimizing legal and compliance risks. The availability of sophisticated cloud-based systems and AI-integrated platforms has significantly supported this transformation.

Leading vendors in the MLR review software landscape are actively pursuing strategic partnerships, acquisitions, and product innovation to expand their capabilities and market footprint. With increasing regulatory complexity, companies are doubling down on R&D to build smarter platforms that support greater automation, traceability, and real-time collaboration. Key areas of investment include AI-powered compliance checks, modular content workflows, and cloud-native architectures that allow companies to adapt to global regulatory nuances. Vendors are focusing on creating configurable platforms that accommodate jurisdiction-specific guidelines while maintaining global consistency, helping life sciences organizations minimize risk, speed up approvals, and stay audit-ready across regions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Functionality

- 2.2.5 Enterprise Size

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift towards digital and multichannel marketing

- 3.2.1.2 Rising adoption of cloud-based platforms

- 3.2.1.3 AI and automation in review processes

- 3.2.1.4 Growing compliance awareness among SMEs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex regulatory landscape

- 3.2.2.2 Data privacy and compliance risks

- 3.2.3 Market opportunities

- 3.2.3.1 Surging pharma and biotech pipelines

- 3.2.3.2 Growing remote and decentralized collaboration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

- 5.3.1 Professional

- 5.3.2 Managed

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Functionality, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Medical review

- 7.3 Legal review

- 7.4 Regulatory review

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Pharmaceutical companies

- 9.3 Biotechnology companies

- 9.4 Medical device manufacturers

- 9.5 Contract Research Organizations (CROs)

- 9.6 Regulatory consulting firms

- 9.7 Healthcare marketing agencies

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M Health Information Systems

- 11.2 Allscripts

- 11.3 Change Healthcare

- 11.4 Epic Systems

- 11.5 Experian Health

- 11.6 GE Healthcare

- 11.7 Health Catalyst

- 11.8 IBM Watson Health

- 11.9 Inovalon Holdings

- 11.10 LexisNexis Risk Solutions

- 11.11 McKesson Corporation

- 11.12 Medtronic

- 11.13 Nuance Communications

- 11.14 Optum

- 11.15 Oracle Health

- 11.16 Philips Healthcare

- 11.17 Siemens Healthineers

- 11.18 Thomson Reuters

- 11.19 Verisk Analytics

- 11.20 Wolters Kluwer

2032 年綜合學習與隱私保護 AI 市場預測:按組件、部署模式、組織規模、應用和地區進行的全球分析

2032 年綜合學習與隱私保護 AI 市場預測:按組件、部署模式、組織規模、應用和地區進行的全球分析 機器學習即服務 (MLaaS) 市場按服務模式、使用類型、行業垂直、部署和組織規模分類 - 全球預測,2025 年至 2032 年

機器學習即服務 (MLaaS) 市場按服務模式、使用類型、行業垂直、部署和組織規模分類 - 全球預測,2025 年至 2032 年 2025年金融服務機器學習全球市場報告2025年全球機器學習市場報告2025年機器學習(ML)智慧流程自動化全球市場報告以生成式人工智慧應用的向量資料庫市場(按資料庫類型、儲存資料類型、技術、部署模式和產業垂直分類)-2025 年至 2030 年全球預測

2025年金融服務機器學習全球市場報告2025年全球機器學習市場報告2025年機器學習(ML)智慧流程自動化全球市場報告以生成式人工智慧應用的向量資料庫市場(按資料庫類型、儲存資料類型、技術、部署模式和產業垂直分類)-2025 年至 2030 年全球預測 全球物流市場機器學習全球自監學習市場全球自動化機器學習解決方案市場人工智慧和機器學習操作化軟體市場規模、佔有率、趨勢分析報告:按部署、功能、應用、公司規模、最終用途、地區和細分市場進行預測,2025 年至 2033 年

全球物流市場機器學習全球自監學習市場全球自動化機器學習解決方案市場人工智慧和機器學習操作化軟體市場規模、佔有率、趨勢分析報告:按部署、功能、應用、公司規模、最終用途、地區和細分市場進行預測,2025 年至 2033 年