|

市場調查報告書

商品編碼

1773345

子宮肌瘤治療設備市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Uterine Fibroid Treatment Device Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

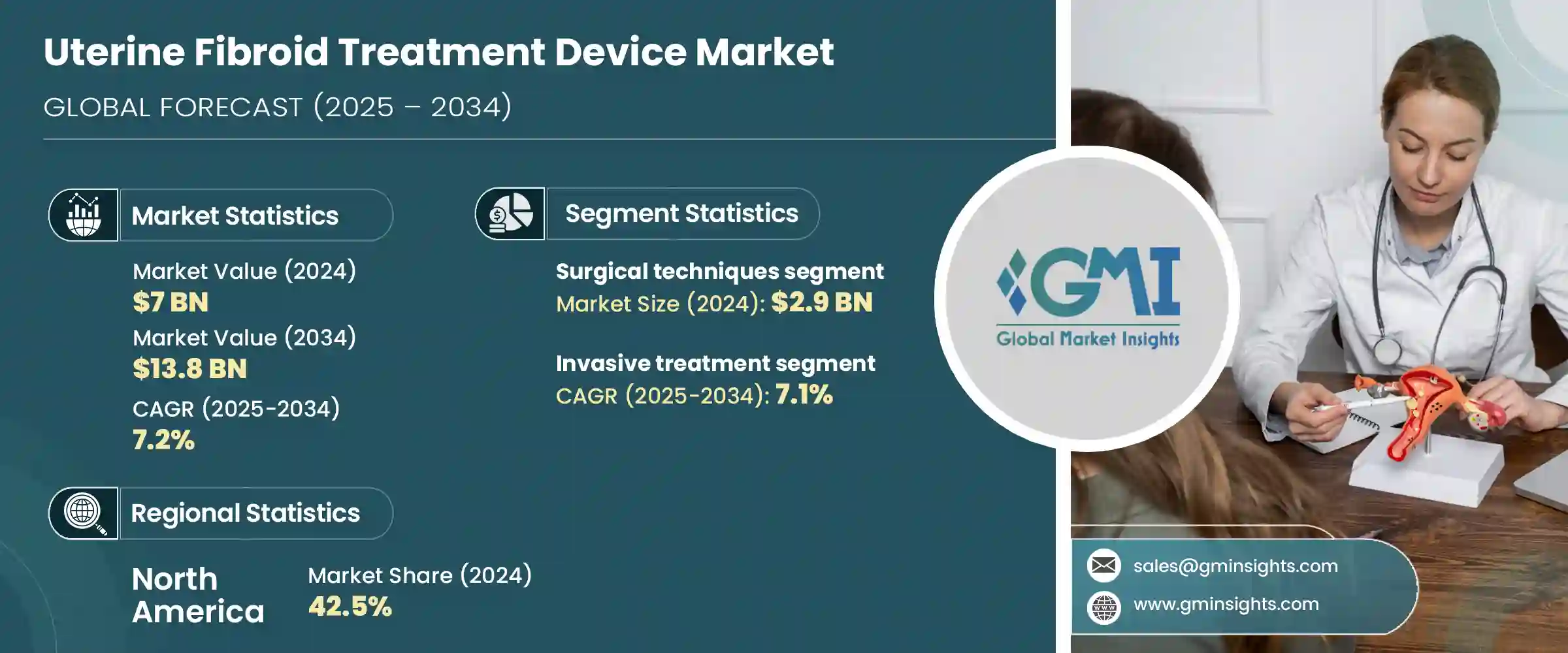

2024年,全球子宮肌瘤治療設備市場規模達70億美元,預計到2034年將以7.2%的複合年成長率成長,達到138億美元。育齡女性子宮肌瘤病例的持續成長,大大推動了對可靠安全的先進治療方案的需求。人們對微創和保留子宮手術的認知不斷提高,以及向技術先進的解決方案的顯著轉變,正在推動醫療體系更廣泛地採用這些技術。基於能量的技術因其能夠有效治療子宮肌瘤並保持子宮完整性而廣受歡迎。

非侵入性及低創傷性治療方法的持續創新正在改善患者的治療效果,尤其對於那些尋求傳統手術替代方案的患者而言。熟練執業醫師的豐富,以及已開發和新興醫療基礎設施中治療管道的擴大,也在支撐市場成長方面發揮關鍵作用。隨著月經過多等婦科疾病的盛行率不斷上升,子宮肌瘤治療器械市場也持續擴張。 Canyon Medical、Minerva Surgical、美敦力、Terumo Corporation、強生(愛惜康)等公司正透過新型治療器械推動子宮肌瘤治療領域的發展。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 70億美元 |

| 預測值 | 138億美元 |

| 複合年成長率 | 7.2% |

2024年,外科手術領域收入達29億美元。這些治療著重於消除子宮肌瘤,或在某些情況下切除子宮本身,取決於病情的嚴重程度和複雜程度。當子宮肌瘤較大、數量眾多或症狀嚴重時,通常首選肌瘤切除術和子宮切除術等手術。這些手術因其高成功率和持久的症狀緩解而受到醫護人員和患者的青睞。醫療基礎設施的不斷擴展、保險方案的改善以及經驗豐富的外科專業人員的更便捷性,支撐了該領域持續佔據主導地位。月經過多及相關婦科疾病病例的增加也加劇了對外科手術的強勁需求。

2024年,侵入性手術領域引領市場,預計2034年將以7.1%的複合年成長率成長。這些治療方法對複雜或嚴重的子宮肌瘤尤其有效,能夠全面緩解症狀。當藥物或非侵入性療法無法達到預期效果時,這些方法就成為首選。與非侵入性技術相比,開放式手術方法能夠提供更明確的治療結果,從而解決諸如骨盆腔不適、異常出血和生育相關併發症等長期存在的問題。此外,由於能夠治療深層或多發性子宮肌瘤,開放式手術領域也成為子宮肌瘤治療器械市場的重要組成部分。

2024年,美國子宮肌瘤治療設備市場規模達30億美元。推動這一成長的關鍵因素之一是擁有大量專注於女性健康和婦科手術的醫療專家。每年,美國都會進行數千例能量療法和栓塞手術,以有效治療子宮肌瘤。隨著治療設備技術的不斷進步以及人們對微創治療方案的日益了解,美國將繼續成為整體市場擴張的重要貢獻者。此外,圍繞新型治療技術的教育以及醫療服務模式的改進也有助於提高患者對基於設備的子宮肌瘤治療方案的接受度和信任度。

業界知名企業包括奧林巴斯、Insightec、深圳邁瑞生物醫療電子、Conmed、Merit Medical Systems、CooperSurgical、波士頓科學、Karl Storz、Hologic、Canyon Medical、美敦力、Minerva Surgical、Terumo Corporation、Nesa Medtech 和強生 (Ethicon)。這些公司透過持續的產品開發和創新,在塑造市場方向方面發揮著重要作用。為了鞏固其在子宮肌瘤治療設備市場的地位,領先公司正在積極投資研發,以推出安全性更高的微創技術。許多公司正專注於透過合併、策略合作和收購來擴展其產品組合,以獲得創新的治療平台。一些公司正在努力透過將即時成像和基於人工智慧的導航系統整合到他們的設備中來改善患者的治療效果。此外,主要參與者正在透過進入尚未開發的市場和與區域醫療保健提供者結盟來擴大其全球影響力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 子宮肌瘤盛行率不斷上升

- 子宮和腹腔鏡設備的技術進步

- 微創手術需求不斷成長

- 產業陷阱與挑戰

- 先進治療設備成本高

- 農村和發展中地區的可用性有限

- 市場機會

- 一次性使用設備的採用率不斷提高

- 保留生育能力的治療方案的需求增加

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 定價分析

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按技術,2021 年至 2034 年

- 主要趨勢

- 手術技術

- 子宮切除術

- 肌瘤切除術

- 腹腔鏡技術

- 腹腔鏡子宮肌瘤切除術

- 肌溶解症

- 消融技術

- 微波消融

- 水熱燒蝕

- 冷凍消融

- 超音波消融

- 高強度聚焦超音波(HIFU)

- MRI導引聚焦超音波(MRGFUS)

- 栓塞技術

第6章:市場估計與預測:依治療方式,2021 年至 2034 年

- 主要趨勢

- 侵入性治療

- 微創治療

- 非侵入性治療

第7章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Boston Scientific

- Canyon Medical

- Conmed

- CooperSurgical

- Hologic

- Insightec

- Johnson & Johnson (Ethicon)

- Karl Storz

- Medtronic

- Merit Medical Systems

- Minerva Surgical

- Nesa Medtech

- Olympus

- Shenzhen Mindray Bio-Medical Electronics

- Terumo Corporation

The Global Uterine Fibroid Treatment Device Market was valued at USD 7 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 13.8 billion by 2034. The consistent rise in fibroid cases among women of childbearing age is significantly fueling the demand for advanced treatment options that are both reliable and safe. Greater awareness about minimally invasive and uterus-sparing procedures, along with a noticeable shift towards technologically sophisticated solutions, is driving broader adoption across healthcare systems. Energy-based technologies have gained popularity for their ability to manage fibroids efficiently while maintaining uterine integrity.

Continuous innovation in non-invasive and less aggressive treatment methods is enhancing patient outcomes, particularly for those seeking alternatives to traditional surgery. The availability of skilled practitioners and expanded access to treatment across developed and emerging healthcare infrastructures also play a critical role in supporting market growth. As the prevalence of conditions like menorrhagia and other gynecologic disorders increases, the market for uterine fibroid treatment devices continues to expand. Companies like Canyon Medical, Minerva Surgical, Medtronic, Terumo Corporation, Johnson & Johnson (Ethicon), and others are key players advancing the landscape of fibroid management with novel therapeutic devices.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7 Billion |

| Forecast Value | $13.8 Billion |

| CAGR | 7.2% |

The surgical procedures segment generated USD 2.9 billion in 2024. These treatments focus on eliminating fibroids or, in certain situations, removing the uterus itself, depending on the extent and complexity of the condition. Procedures such as myomectomy and hysterectomy are often preferred when fibroids are large, numerous, or highly symptomatic. Their popularity among both healthcare providers and patients stems from high success rates and long-lasting relief from symptoms. The continued dominance of this segment is supported by an expanding healthcare infrastructure, improved insurance options, and better access to experienced surgical professionals. Factors like rising cases of excessive menstrual bleeding and related gynecological issues also contribute to the strong demand for surgical intervention.

In 2024, the invasive procedures segment led the market and is anticipated to grow at a CAGR of 7.1% through 2034. These treatments are especially effective for complicated or severe fibroid conditions, offering comprehensive symptom relief. When medications or non-invasive therapies fail to deliver the expected results, these methods become the preferred option. Open surgical approaches address persistent issues such as pelvic discomfort, abnormal bleeding, and fertility-related complications by providing more definitive outcomes compared to non-invasive techniques. The ability to treat deeply embedded or multiple fibroids also makes this segment a critical part of the uterine fibroid treatment device market.

U.S. Uterine Fibroid Treatment Device Market was valued at USD 3 billion in 2024. A key factor contributing to this growth is the availability of medical experts specializing in women's health and gynecologic procedures. Thousands of energy-based and embolization procedures are carried out annually to treat fibroids effectively. With continual technological advancements in treatment devices and broader awareness of less invasive alternatives, the U.S. continues to be a significant contributor to overall market expansion. Education around newer treatment techniques and improvements in healthcare delivery models are also helping to increase patient uptake and trust in device-based fibroid solutions.

Prominent industry players include Olympus, Insightec, Shenzhen Mindray Bio-Medical Electronics, Conmed, Merit Medical Systems, CooperSurgical, Boston Scientific, Karl Storz, Hologic, Canyon Medical, Medtronic, Minerva Surgical, Terumo Corporation, Nesa Medtech, and Johnson & Johnson (Ethicon). These companies are instrumental in shaping the market's direction through ongoing product development and innovation. To reinforce their position in the uterine fibroid treatment device market, leading companies are actively investing in research and development to introduce minimally invasive technologies with improved safety profiles. Many are focusing on expanding their product portfolios through mergers, strategic partnerships, and acquisitions to access innovative treatment platforms. Several firms are working to enhance patient outcomes by integrating real-time imaging and AI-based navigation systems into their devices. Additionally, key players are increasing their global footprint by entering untapped markets and aligning with regional healthcare providers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology

- 2.2.3 Treatment

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of uterine fibroids

- 3.2.1.2 Technological advancements in uterine & laparoscopic devices

- 3.2.1.3 Rising demand for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced treatment devices

- 3.2.2.2 Limited availability in rural and developing areas

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing adoption of disposable and single-use devices

- 3.2.3.2 Increased demand for fertility-preserving treatment options

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical techniques

- 5.2.1 Hysterectomy

- 5.2.2 Myomectomy

- 5.3 Laparoscopic techniques

- 5.3.1 Laparoscopic myomectomy

- 5.3.2 Myolysis

- 5.4 Ablation techniques

- 5.4.1 Microwave ablation

- 5.4.2 Hydrothermal ablation

- 5.4.3 Cryoablation

- 5.4.4 Ultrasound ablation

- 5.4.4.1 High intensity focused ultrasound (HIFU)

- 5.4.4.2 MRI-guided focused ultrasound (MRGFUS)

- 5.5 Embolization techniques

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Invasive treatment

- 6.3 Minimally invasive treatment

- 6.4 Non-invasive treatment

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Boston Scientific

- 8.2 Canyon Medical

- 8.3 Conmed

- 8.4 CooperSurgical

- 8.5 Hologic

- 8.6 Insightec

- 8.7 Johnson & Johnson (Ethicon)

- 8.8 Karl Storz

- 8.9 Medtronic

- 8.10 Merit Medical Systems

- 8.11 Minerva Surgical

- 8.12 Nesa Medtech

- 8.13 Olympus

- 8.14 Shenzhen Mindray Bio-Medical Electronics

- 8.15 Terumo Corporation