|

市場調查報告書

商品編碼

1773340

齲齒檢測儀市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Dental Caries Detectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

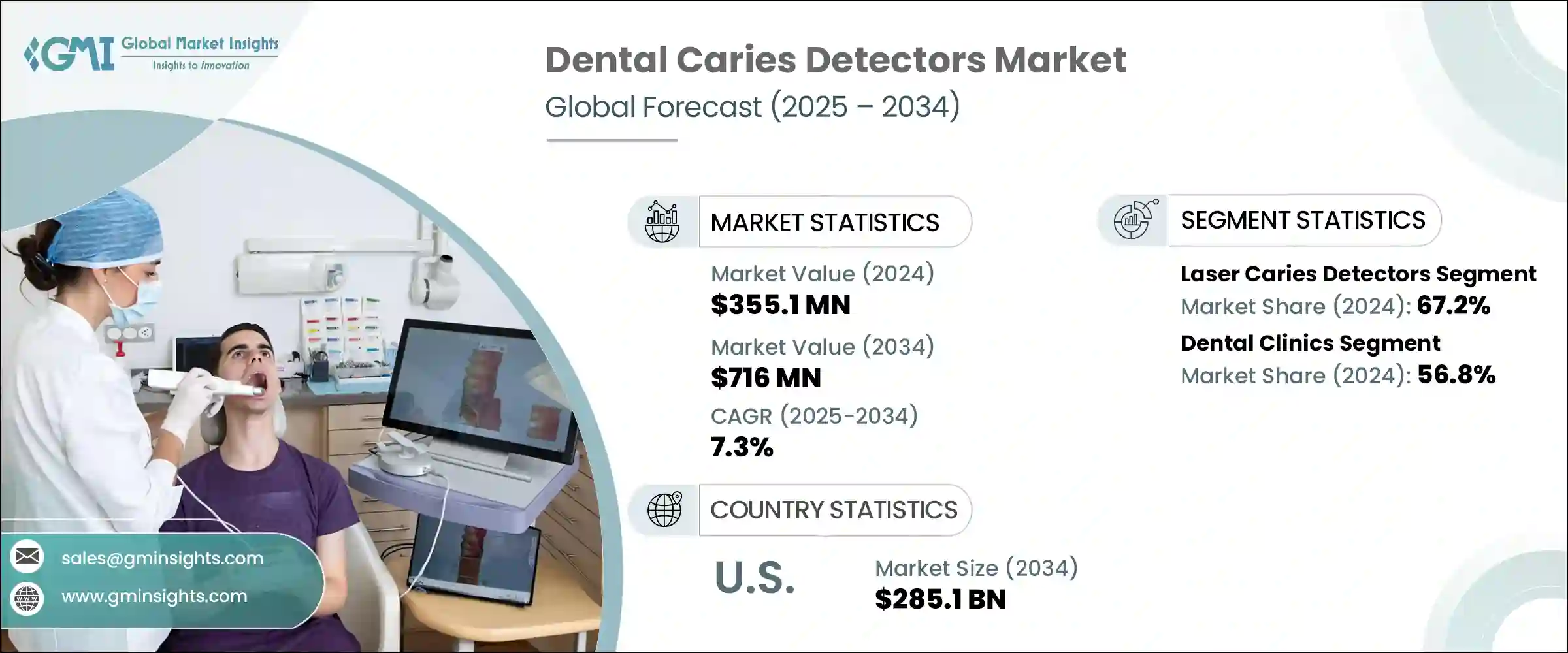

2024年,全球齲齒偵測儀市場規模達3.551億美元,預計到2034年將以7.3%的複合年成長率成長,達到7.16億美元。齲齒發生率的上升,尤其是在老化人口和年輕族群中,持續推動先進診斷工具的需求。由於未治療的齲齒往往會導致複雜的口腔健康問題和更高的治療費用,人們越來越關注早期非侵入性檢測方法。越來越多的患者和醫療機構開始使用齲齒檢測設備,以獲得更快、更準確的評估。

口腔護理意識的提升以及預防措施被納入個人和公共衛生系統,正在重塑口腔疾病的管理方式。隨著現代科技的普及以及早期介入的趨勢,牙科護理正變得更加主動而非被動。人們對整體健康的普遍關注也推動了這個市場的成長,促使牙醫採用前瞻性工具,幫助有效地檢測、監測和預防口腔健康問題。此外,數位平台和不斷發展的患者護理模式正在改變牙醫的診斷方式,從而為患者群體帶來更好的臨床療效並降低長期成本。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3.551億美元 |

| 預測值 | 7.16億美元 |

| 複合年成長率 | 7.3% |

技術驅動的創新是該市場的核心,各種設備透過數位X光攝影、雷射螢光和近紅外線成像等方法,提供更快的診斷速度和更精確的診斷精度。這些進步使執業醫師能夠在病變進展之前發現病變,從而能夠採取以保留病灶和微創治療為重點的干涉措施。隨著人們對補充護理和整體健康的興趣日益成長,牙科診所正在整合符合更廣泛治療目標的早期檢測工具,包括舒適度、壽命和患者滿意度。隨著人們日益重視長期健康儲蓄和口腔衛生教育,這些檢測技術正成為常規檢查的關鍵組成部分,改善了診療可及性,並最佳化了早期護理策略。

2024年,雷射齲齒偵測工具市場佔有67.2%的市場佔有率,鞏固了其在全球市場的領先地位。這些系統因其能夠在可見的齲齒出現之前識別病變,正成為首選。微創手術的趨勢推動了對能夠保護天然琺瑯質並進行早期預防干涉的設備的需求。雷射技術通常依賴螢光,提供一種可靠、無痛的方法來區分健康和齲齒組織。隨著人們對螢光在識別咬合面和鄰面齲齒方面的臨床可靠性的信心不斷增強,基於雷射的系統在各個診所中越來越被廣泛接受。牙醫投資這些工具不僅是為了提高診斷精確度,也是為了提升患者在常規檢查中的舒適度和體驗。

2024年,牙科診所細分市場佔據56.8%的市場。診所面臨越來越大的壓力,需要透過實證實踐來驗證其診斷的準確性,尤其是在保險和醫療服務體係不斷發展的情況下。整合先進的檢測系統有助於服務提供者遵循現代護理方案,同時增強患者信任並降低過度治療的風險。許多診所正在轉向數據驅動的治療計劃,其中精準的檢測支持齲病的保守治療和個人化護理方法。鑑於早期診斷是有效治療的關鍵,診所正在將自己定位為預防性牙科護理領域的領導者。

預計到2034年,美國齲齒偵測儀市場規模將達2.851億美元。儘管美國是一個高收入國家,但其口腔健康負擔依然沉重,尤其是在兒童、老年人和弱勢群體中。預防性牙科就診的障礙(例如費用高昂和就診管道有限)使得早期檢測對於控制普遍存在的齲齒至關重要。私人診所和公共衛生機構擴大採用診斷工具,以控制長期醫療保健成本並支持更廣泛的預防保健目標。診斷創新在緩解未治療的牙科問題和改善全國範圍內的口腔健康狀況方面發揮關鍵作用。

齲齒檢測儀市場的知名企業包括 Ivoclar Vivadent、Quantum Dental Technologies、Planmeca、AdDent、Biolase、Dentsply Sirona、Centrix、Kuraray、Acteon Group、Hu-Friedy、DentLight、KaVo Kerr、Vatech、Air Techniques 和Air Techniques 和。齲齒檢測儀市場的領先公司致力於提高診斷精度和方便用戶使用型設計,以最佳化臨床工作流程。

許多公司正在整合人工智慧分析和即時成像技術,以改進齲齒識別並支援實證牙科。研發方面的策略性投資旨在提供適用於各種臨床環境的緊湊、非侵入式且經濟高效的設備。各公司也與牙醫學校和醫療系統建立合作夥伴關係,以提高產品的採用率和教育推廣。擴展產品組合以涵蓋多功能診斷工具,進一步增強了其競爭地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 全球齲齒盛行率不斷上升

- 提高人們對口腔健康和預防牙科的認知

- 成像和雷射檢測技術的進步

- 牙科診所和專業人員的數量不斷增加

- 產業陷阱與挑戰

- 先進齲齒檢測設備成本高

- 缺乏報銷政策

- 市場機會

- 用於早期齲齒檢測的人工智慧診斷解決方案

- 攜帶式和遠端牙科相容齲齒檢測設備

- 成長動力

- 成長潛力分析

- 監管格局

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 報銷場景

- 報銷政策對市場成長的影響

- 未來市場趨勢

- 消費者行為分析

- 專利分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 競爭市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 年至 2034 年

- 主要趨勢

- 雷射齲齒檢測儀

- 光纖透照(FOTI)設備

第6章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 牙醫診所

- 醫院

- 學術和研究機構

- 診斷中心

第7章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 日本

- 中國

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 墨西哥

- 巴西

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第8章:公司簡介

- Acteon Group

- AdDent

- Air Techniques

- Biolase

- Centrix

- DentLight

- Dentsply Sirona

- GreenMark Biomedical

- Hu-Friedy

- Ivoclar Vivadent

- KaVo Kerr

- Kuraray

- Planmeca

- Quantum Dental Technologies

- Vatech

The Global Dental Caries Detectors Market was valued at USD 355.1 million in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 716 million by 2034. Rising incidences of dental caries, particularly among aging populations and younger age groups, continue to drive the need for advanced diagnostic tools. As untreated cavities often lead to complex oral health issues and higher treatment costs, there is a growing focus on early-stage, non-invasive detection methods. Patients and providers alike are increasingly turning to caries detection devices for faster, more accurate assessments.

Advancements in oral care awareness and the integration of preventive measures into both individual and public health systems are reshaping how oral diseases are managed. With improved access to modern technologies and a shift toward early intervention, dental care is becoming more proactive than reactive. This market's growth is also supported by a wider interest in overall well-being, encouraging dentists to implement forward-thinking tools that help detect, monitor, and prevent oral health issues efficiently. Additionally, digital platforms and evolving patient care models are transforming the way dental practitioners approach diagnosis, enabling better clinical outcomes and long-term cost reduction across patient populations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $355.1 Million |

| Forecast Value | $716 Million |

| CAGR | 7.3% |

Technology-driven innovation is at the core of this market, with devices offering enhanced speed and diagnostic precision through methods like digital radiography, laser fluorescence, and near-infrared imaging. These advancements are empowering practitioners to identify lesions before they progress, enabling interventions that prioritize preservation and minimal invasion. As interest in complementary care and holistic health grows, dental offices are incorporating early detection tools that align with broader treatment goals, including comfort, longevity, and patient satisfaction. With a rising emphasis on long-term health savings and education around oral hygiene, these detection technologies are becoming key components in routine exams, improving access and optimizing early-stage care strategies.

The laser caries detection tools segment accounted for a 67.2% share in 2024, solidifying its lead within the global market. These systems are becoming the preferred choice due to their ability to identify lesions before visible decay develops. The trend toward minimally invasive procedures is fueling demand for devices that preserve natural enamel and allow early preventive intervention. Laser technologies often rely on fluorescence, providing a reliable, pain-free method to differentiate between healthy and decayed tissue. As confidence grows in the clinical reliability of fluorescence for identifying occlusal and interproximal caries, laser-based systems are gaining broader acceptance across practices. Dentists are investing in these tools not only to increase diagnostic precision but also to enhance patient comfort and experience during routine checkups.

The dental clinics segment held a 56.8% share in 2024. Clinics are under increasing pressure to validate their diagnostic accuracy with evidence-based practices, particularly as insurance and care delivery systems evolve. Integrating advanced detection systems helps providers align with modern care protocols while reinforcing patient trust and reducing the risk of overtreatment. Many clinics are shifting toward data-driven treatment planning, where accurate detection supports conservative management of carious lesions and personalized care approaches. With early diagnosis being key to effective treatment, clinics are positioning themselves as leaders in preventive dental care.

United States Dental Caries Detectors Market is projected to reach USD 285.1 million by 2034. Despite being a high-income nation, the U.S. faces a significant oral health burden, particularly among children, seniors, and underrepresented communities. Barriers to preventive dental visits-such as cost and limited access-make early detection critical in managing widespread decay. The adoption of diagnostic tools is increasing across both private clinics and public health settings to control long-term healthcare costs and support broader preventive care goals. The role of diagnostic innovation is pivotal in mitigating untreated dental issues and improving oral health outcomes nationwide.

Prominent players operating in the Dental Caries Detectors Market include Ivoclar Vivadent, Quantum Dental Technologies, Planmeca, AdDent, Biolase, Dentsply Sirona, Centrix, Kuraray, Acteon Group, Hu-Friedy, DentLight, KaVo Kerr, Vatech, Air Techniques, and GreenMark Biomedical. Leading companies in the dental caries detectors market are focusing on advancing diagnostic precision and user-friendly designs to enhance clinical workflows.

Many are integrating AI-powered analytics and real-time imaging to improve caries identification and support evidence-based dentistry. Strategic investments in R&D aim to deliver compact, non-invasive, and cost-effective devices suited for diverse clinical environments. Companies are also forming partnerships with dental schools and health systems to increase product adoption and educational outreach. Expanding product portfolios to include multifunctional diagnostic tools further strengthens their competitive position.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of dental caries globally

- 3.2.1.2 Rising awareness about oral health and preventive dentistry

- 3.2.1.3 Technological advancements in imaging and laser-based detection

- 3.2.1.4 Growing number of dental clinics and professionals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced caries detection devices

- 3.2.2.2 Lack of reimbursement policies

- 3.2.3 Market opportunities

- 3.2.3.1 AI-Powered Diagnostic Solutions for Early Caries Detection

- 3.2.3.2 Portable and Teledentistry-Compatible Caries Detection Devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Reimbursement scenario

- 3.7.1 Impact of reimbursement policies on market growth

- 3.8 Future market trends

- 3.9 Consumer behaviour analysis

- 3.10 Patent analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Laser caries detectors

- 5.3 Fiber optic transillumination (FOTI) devices

Chapter 6 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dental clinics

- 6.3 Hospitals

- 6.4 Academic and research institutes

- 6.5 Diagnostic centers

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 Japan

- 7.4.2 China

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Mexico

- 7.5.2 Brazil

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Acteon Group

- 8.2 AdDent

- 8.3 Air Techniques

- 8.4 Biolase

- 8.5 Centrix

- 8.6 DentLight

- 8.7 Dentsply Sirona

- 8.8 GreenMark Biomedical

- 8.9 Hu-Friedy

- 8.10 Ivoclar Vivadent

- 8.11 KaVo Kerr

- 8.12 Kuraray

- 8.13 Planmeca

- 8.14 Quantum Dental Technologies

- 8.15 Vatech

齲齒治療市場:依產品類型、治療類型、應用和最終用戶分類-2026年至2032年全球市場預測

齲齒治療市場:依產品類型、治療類型、應用和最終用戶分類-2026年至2032年全球市場預測 齲病治療市場:依產品類型、按地區分類

齲病治療市場:依產品類型、按地區分類 2026年全球人工智慧(AI)齲齒檢測市場報告牙科離心鑄造機市場(按機器類型、應用、最終用戶和分銷管道分類),全球預測(2026-2032)

2026年全球人工智慧(AI)齲齒檢測市場報告牙科離心鑄造機市場(按機器類型、應用、最終用戶和分銷管道分類),全球預測(2026-2032) 齲齒治療市場規模、佔有率及成長分析(按產品類型、最終用戶和地區分類)-產業預測(2026-2033 年)2025年全球齲齒治療市場報告

齲齒治療市場規模、佔有率及成長分析(按產品類型、最終用戶和地區分類)-產業預測(2026-2033 年)2025年全球齲齒治療市場報告 全球齲齒治療市場全球齲齒檢測儀市場

全球齲齒治療市場全球齲齒檢測儀市場 齲齒檢測器市場預測(至 2032 年):按產品類型、檢測模式、光源、應用、最終用戶和地區進行的全球分析

齲齒檢測器市場預測(至 2032 年):按產品類型、檢測模式、光源、應用、最終用戶和地區進行的全球分析 窩溝封閉劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

窩溝封閉劑市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測