|

市場調查報告書

商品編碼

1773335

新能源汽車穩定器市場機會、成長動力、產業趨勢分析及2025-2034年預測New Energy Vehicle Stabilizer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

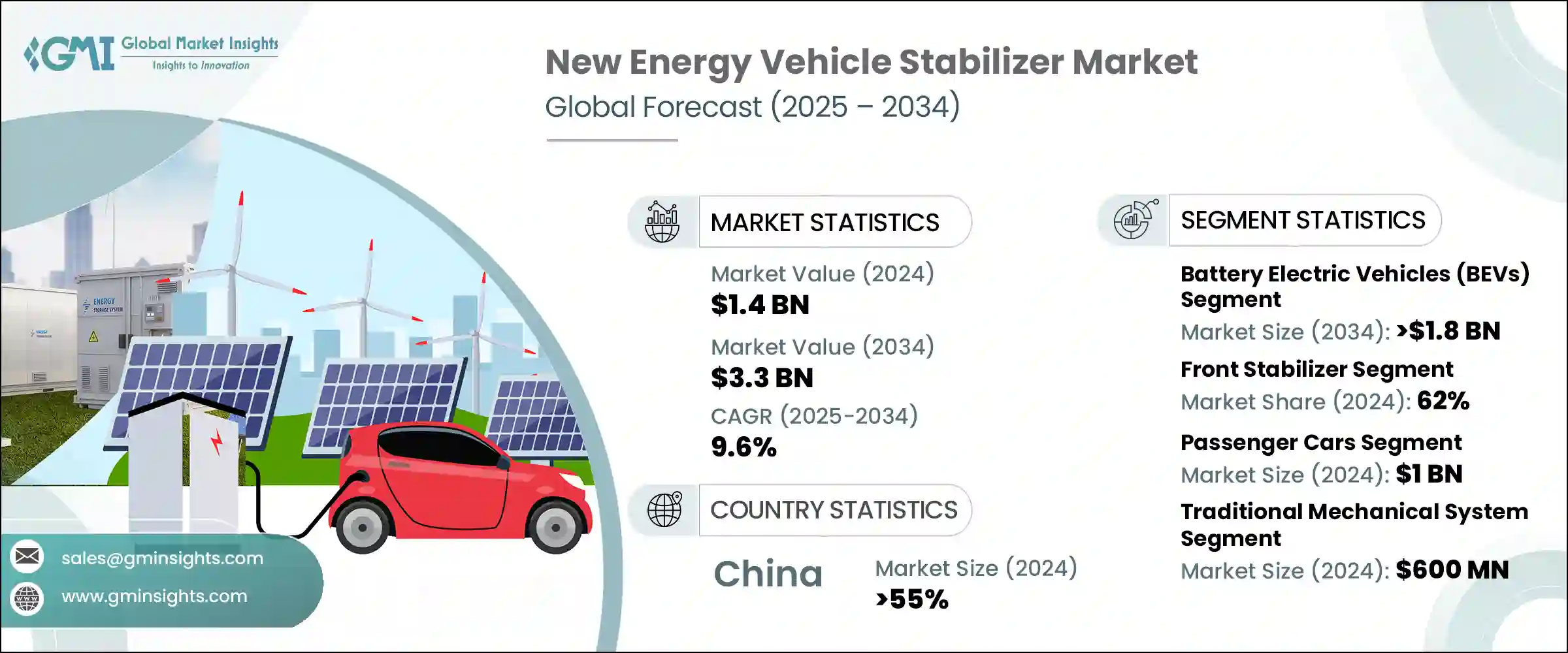

2024年,全球新能源汽車穩定器市場規模達14億美元,預計2034年將以9.6%的複合年成長率成長,達到33億美元。這一成長主要得益於全球主要市場對電動、混合動力和氫動力汽車的日益普及。隨著製造商轉向替代動力傳動系統,車輛動力學和整體駕駛體驗也日益受到重視,這直接推動了對先進穩定器技術的需求。機電式穩定器和主動式穩定器因其能夠提升懸吊性能、減少車身側傾並為乘客和駕駛員提供更平穩的操控性,正得到越來越廣泛的應用。這反映了電動車產業追求高安全性和舒適性的普遍趨勢。

穩定桿(通常稱為防傾桿或防側傾桿)在支撐新能源車的懸吊系統中發揮著至關重要的作用,尤其是在電池放置導致重量分佈改變的情況下。與傳統的內燃機 (ICE) 汽車不同,新能源汽車通常會將電池組安裝在車輛地板上,這會導致重心偏移,需要重新設計穩定桿系統。這些系統旨在確保車輛的最佳性能和轉彎穩定性,尤其是在高速操控或快速轉向時。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 14億美元 |

| 預測值 | 33億美元 |

| 複合年成長率 | 9.6% |

2024年,純電動車 (BEV) 佔據了46%的市場佔有率,預計到2034年該細分市場將創造18億美元的市場價值。純電動車在穩定器市場佔據穩固地位,得益於產量激增以及消費者對純電動平台的需求。這一成長得益於政策支援、充電基礎設施的擴展以及現代、大眾、特斯拉和比亞迪等全球汽車製造商的大力投資。由於純電動車電池重量增加,需要專門設計的懸吊系統,這進一步增加了對先進穩定器組件的依賴。

2024年,前穩定桿市場佔據全球新能源汽車穩定桿市場62%的佔有率,並預計到2034年將以8.2%的複合年成長率成長。這種主導地位源於其在管理前軸穩定性和維持車輛平衡方面的關鍵作用。由於電動車通常採用前輪驅動配置,並將電池重量集中在前軸上,前穩定桿已成為確保即時駕駛條件下精準操控和減少車身晃動的不可或缺的部件。

亞太地區新能源汽車穩定器市場佔55%的市場佔有率,2024年市場規模達3億美元。新能源汽車製造業的快速發展、持續的監管支持以及不斷成長的國內需求是推動這一成長的關鍵因素。中國已成為全球最大的新能源汽車市場,而積極的國家戰略和投資進一步鞏固了這一地位。蔚來、小鵬、比亞迪和吉利等本土品牌,以及特斯拉和大眾等全球汽車製造商,都在持續擴大其在該地區的生產佈局,以滿足日益成長的需求。

新能源汽車穩定器市場的領導者包括索格菲集團、蒂森克虜伯、大元、採埃孚、東風、日本國際、SwayTec、瀚瑞森、康斯博格汽車和慕貝爾。新能源汽車穩定器領域的公司正在積極追求創新並與下一代電動車平台整合。大多數公司都在投資研發,以開發更輕、強度更高的穩定器零件,以適應電動傳動系統不斷變化的動態。與電動車製造商合作進行早期設計參與,可以實現客製化懸吊系統。該公司還採用了自適應和機電技術,與車載感測器和控制單元配合使用,以實現即時性能。透過在地化生產中心和與原始設備製造商簽訂的長期供應商協議進行全球擴張,有助於這些公司擴大其市場覆蓋範圍。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 原物料供應商

- 零件製造商

- 技術提供者

- 售後市場供應商

- 系統整合商

- 成本結構

- 利潤率

- 每個階段的增值

- 影響供應鏈的因素

- 破壞者

- 供應商格局

- 對部隊的影響

- 成長動力

- 政府法規和消費者對電動和混合動力汽車的需求不斷增加

- 對新能源汽車增強行駛控制和操控性能的需求

- 從機械穩定器轉向智慧感測器整合穩定器

- 對自適應和斷開穩定器系統的需求增加

- 產業陷阱與挑戰

- 特別是機電和主動系統

- 空間限制導致的包裝挑戰

- 市場機會

- 電動越野車性能部件和客製化的成長

- 為無線 (OTA) 穩定器調整和控制解決方案打開大門

- 成長動力

- 成長潛力分析

- 波特的分析

- PESTEL分析

- 技術與創新格局

- 現有技術

- 新興技術

- 專利分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本細分分析

- 永續性分析

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 純電動車(BEV)

- 插電式混合動力電動車(PHEV)

- 混合動力電動車(HEV)

- 燃料電池電動車(FCEV)

第6章:市場估計與預測:按穩定器,2021 - 2034 年

- 主要趨勢

- 前穩定器

- 後穩定器

第7章:市場估計與預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 液壓穩定器系統

- 機電穩定器系統

- 電子控制穩定桿

- 傳統機械系統

第8章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 轎車

- 掀背車

- 越野車

- 中紫外線

- 商用車

- 輕型商用車

- 中型商用車

- 重型商用車

第9章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- OEM

- 售後市場

第10章:市場估計與預測:按地區,2021 - 2034 年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 烏克蘭

- 俄羅斯

- 北歐的

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東南亞

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

- MEA

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- AAM

- ADDCO

- Chuo Spring

- DAEWON

- Dongfeng

- JAMNA AUTO INDUSTRIES LIMITED

- Sogefi Group

- Kongsberg Automotive

- Mubea

- NHK International

- Hendrickson

- Sogefi

- SwayTec

- Tata

- Thyssenkrupp

- Tinsley Bridge

- TMT(CSR)

- Tower

- Wanxiang

- Yangzhou Dongsheng

- ZF

The Global New Energy Vehicle Stabilizer Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 9.6% to reach USD 3.3 billion by 2034. This growth is largely fueled by the increasing adoption of electric, hybrid, and hydrogen-powered vehicles across major global markets. As manufacturers shift to alternative drivetrains, there is a rising emphasis on vehicle dynamics and overall ride quality, which directly boosts the demand for advanced stabilizer technologies. Electromechanical and active stabilizers are becoming more widely adopted due to their ability to enhance suspension performance, reduce body roll, and provide smoother handling for both passengers and drivers. This reflects a broader trend in the EV sector to deliver high levels of safety and comfort.

Stabilizers-often called sway or anti-roll bars-play a crucial role in supporting the suspension systems of NEVs, especially given the altered weight distribution brought on by battery placement. Unlike conventional internal combustion engine (ICE) vehicles, NEVs tend to house battery packs on the vehicle floor, shifting the center of gravity and requiring reimagined stabilizer systems. These systems are designed to ensure optimal performance and cornering stability, particularly during high-speed maneuvers or rapid direction changes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 9.6% |

Battery Electric Vehicles (BEVs) commanded a 46% share in 2024, and the segment is anticipated to generate USD 1.8 billion by 2034. The strong foothold of BEVs in the stabilizer market is backed by surging production and consumer demand for all-electric platforms. This increase is due to supportive policy environments, expanded charging infrastructure, and significant investment from global OEMs like Hyundai, Volkswagen, Tesla, and BYD. Heavier battery weights in BEVs necessitate specially engineered suspension systems, increasing the reliance on advanced stabilizer components.

In 2024, the front stabilizer bars segment led the global new energy vehicle stabilizer market, accounting for 62% share, and is forecasted to grow at a CAGR of 8.2% through 2034. This dominance stems from their critical role in managing front-axle stability and maintaining vehicle balance. As electric vehicles frequently adopt front-wheel drive configurations and concentrate battery mass on the front axle, front stabilizers have become indispensable in ensuring precise handling and reduced body movement in real-time driving conditions.

Asia Pacific New Energy Vehicle Stabilizer Market held a 55% share and generated USD 300 million in 2024. The rapid acceleration of NEV manufacturing sustained regulatory support, and increasing domestic demand are key drivers of this growth. China has established itself as the largest NEV market worldwide, a position reinforced by aggressive national strategies and investment. Local brands like NIO, XPeng, BYD, and Geely, as well as global automakers such as Tesla and Volkswagen, have continued to expand their production footprints in the region to meet this surging demand.

Leading players operating in the New Energy Vehicle Stabilizer Market include Sogefi Group, Thyssenkrupp, DAEWON, ZF, Dongfeng, NHK International, SwayTec, Hendrickson, Kongsberg Automotive, and Mubea. Companies in the NEV stabilizer segment are aggressively pursuing innovation and integration with next-gen EV platforms. Most are investing in R&D to develop lighter, high-strength stabilizer components that match the evolving dynamics of electric drivetrains. Collaborations with EV manufacturers for early-stage design involvement allow for customized suspension systems. Firms are also incorporating adaptive and electromechanical technologies that work with onboard sensors and control units for real-time performance. Global expansion through localized production hubs and long-term supplier agreements with OEMs helps these players strengthen their market reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Stabilizer

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 Technology providers

- 3.1.1.4 Aftermarket suppliers

- 3.1.1.5 System integrators

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing government mandates and consumer demand for electric and hybrid vehicles

- 3.2.1.2 Demand for enhanced ride control and handling performance in NEVs

- 3.2.1.3 Shift from mechanical to intelligent, sensor-integrated stabilizers

- 3.2.1.4 Increased need for adaptive and disconnecting stabilizer systems

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Especially electromechanical and active systems

- 3.2.2.2 Packaging challenges due to space constraints

- 3.2.3 Market Opportunities

- 3.2.3.1 Growth in performance parts and customization in electric off-road vehicles

- 3.2.3.2 Opens door for over-the-air (OTA) stabilizer tuning and control solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Battery Electric Vehicles (BEVs)

- 5.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 5.4 Hybrid Electric Vehicles (HEVs)

- 5.5 Fuel Cell Electric Vehicles (FCEVs)

Chapter 6 Market Estimates & Forecast, By Stabilizer, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Front Stabilizer

- 6.3 Rear Stabilizer

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Hydraulic stabilizer system

- 7.3 Electromechanical stabilizer system

- 7.4 Electronically controlled stabilizer bar

- 7.5 Traditional mechanical system

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.1.1 Passenger Car

- 8.1.2 Sedan

- 8.1.3 Hatchback

- 8.1.4 SUV

- 8.1.5 MUV

- 8.2 Commercial Vehicle

- 8.2.1 Light Commercial Vehicle

- 8.2.2 Medium Commercial Vehicle

- 8.2.3 Heavy Commercial Vehicle

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Ukraine

- 10.2.7 Russia

- 10.2.8 Nordic

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 South Korea

- 10.3.6 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.4.4 Chile

- 10.5 MEA

- 10.5.1 South Africa

- 10.5.2 Saudi Arabia

- 10.5.3 UAE

Chapter 11 Company Profiles

- 11.1 AAM

- 11.2 ADDCO

- 11.3 Chuo Spring

- 11.4 DAEWON

- 11.5 Dongfeng

- 11.6 JAMNA AUTO INDUSTRIES LIMITED

- 11.7 Sogefi Group

- 11.8 Kongsberg Automotive

- 11.9 Mubea

- 11.10 NHK International

- 11.11 Hendrickson

- 11.12 Sogefi

- 11.13 SwayTec

- 11.14 Tata

- 11.15 Thyssenkrupp

- 11.16 Tinsley Bridge

- 11.17 TMT(CSR)

- 11.18 Tower

- 11.19 Wanxiang

- 11.20 Yangzhou Dongsheng

- 11.21 ZF

新能源汽車電源市場按推進類型、車輛類型、輸出功率類型和分銷管道分類,全球預測(2026-2032年)新能源汽車靜音輪胎市場:依輪胎設計類型、胎面花紋、降噪技術、車輛類型和應用分類-2026-2032年全球預測新能源汽車驅動馬達定子和轉子市場(按馬達類型、車輛類型、功率輸出、冷卻方式、材料類型和銷售管道),全球預測,2026-2032年靜音棉質輪胎市場:按棉質材料類型、輪胎類型、輪胎結構、應用和最終用戶分類,全球預測,2026-2032年

新能源汽車電源市場按推進類型、車輛類型、輸出功率類型和分銷管道分類,全球預測(2026-2032年)新能源汽車靜音輪胎市場:依輪胎設計類型、胎面花紋、降噪技術、車輛類型和應用分類-2026-2032年全球預測新能源汽車驅動馬達定子和轉子市場(按馬達類型、車輛類型、功率輸出、冷卻方式、材料類型和銷售管道),全球預測,2026-2032年靜音棉質輪胎市場:按棉質材料類型、輪胎類型、輪胎結構、應用和最終用戶分類,全球預測,2026-2032年 新能源汽車匯流排:全球市佔率及排名、總銷售量及需求預測(2025-2031年)

新能源汽車匯流排:全球市佔率及排名、總銷售量及需求預測(2025-2031年) 2025年新能源汽車(NEV)保險全球市場報告

2025年新能源汽車(NEV)保險全球市場報告 全球新能源汽車(NEV)計程車市場

全球新能源汽車(NEV)計程車市場 全球新能源汽車市場:預測(2025-2030)

全球新能源汽車市場:預測(2025-2030) 新能源汽車(NEV)計程車市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測

新能源汽車(NEV)計程車市場:2024-2031年全球產業分析、規模、佔有率、成長、趨勢、預測 中國新能源汽車電力驅動電源領域產業(2024年)

中國新能源汽車電力驅動電源領域產業(2024年)