|

市場調查報告書

商品編碼

1773323

輪胎平衡重市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Tire Balance Weight Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

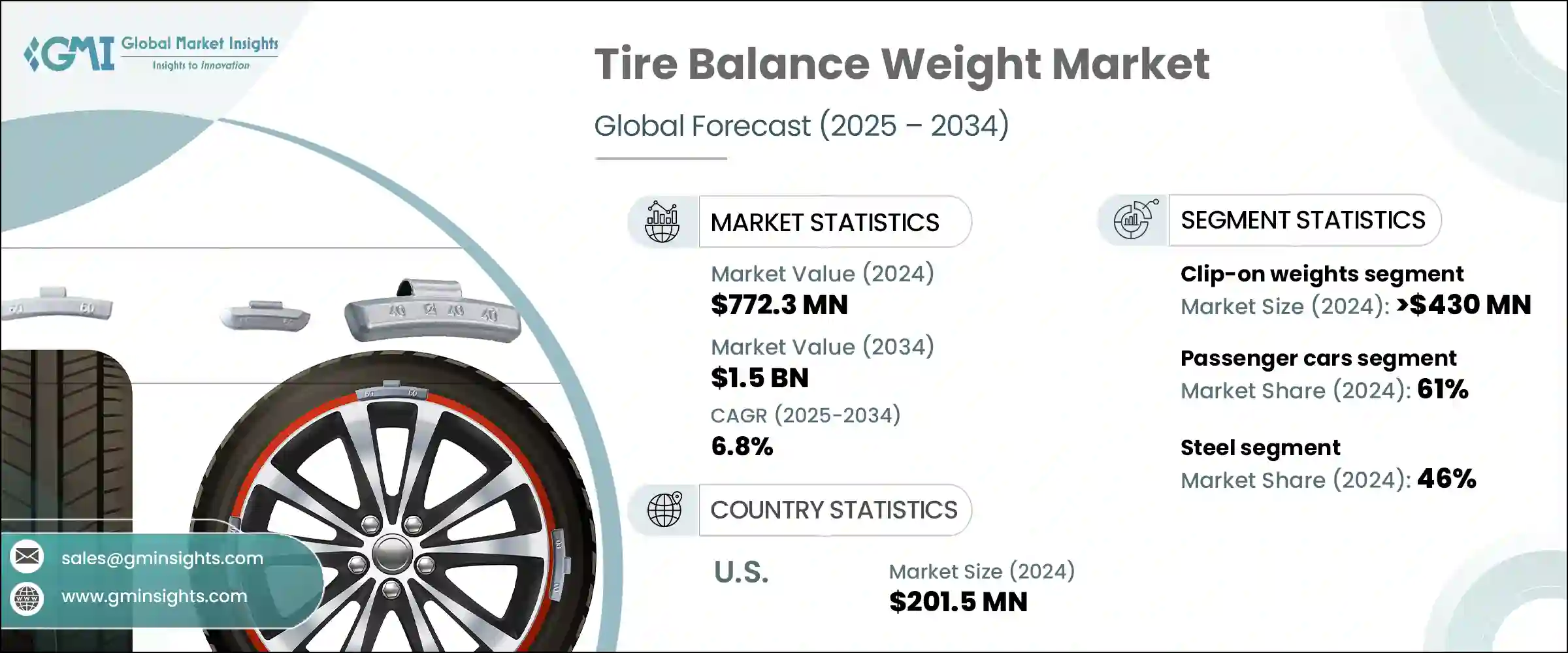

2024 年全球輪胎平衡塊市場規模達 7.723 億美元,預估年複合成長率為 6.8%,到 2034 年將達到 15 億美元。這一成長主要得益於全球汽車產量的快速成長,尤其是在新興市場。隨著汽車保有量的增加和商用車數量的擴大,包括車輪平衡在內的定期輪胎保養需求激增,尤其是在交通需求旺盛的繁華城市。此外,公共部門對基礎設施的投資不斷增加,以及物流、客運和電子商務等行業推動的交通需求不斷成長,也加劇了車隊維護活動,從而對輪胎平衡塊的需求強勁成長。由於這些零件在確保車輛安全和乘坐舒適性方面發揮關鍵作用,因此對它們的需求自然會隨著全球汽車保有量的增加而成長。

各地區政府和監管機構正在加強安全和道路合規標準,這也推動了市場的發展。透過輪胎平衡塊實現的正確車輪平衡可以消除不必要的振動,延長輪胎使用壽命,提高高速行駛安全性,並降低整體維護成本。尤其是在北美、歐洲和亞洲,對這些法規的嚴格遵守促使車輛營運商進行常規輪胎維護,從而刺激了需求。此外,法規合規性以及消費者和車隊營運商對車輛性能和安全意識的不斷提升,仍然是市場穩定擴張的根本驅動力。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 7.723億美元 |

| 預測值 | 15億美元 |

| 複合年成長率 | 6.8% |

2024年,卡式平衡塊市場產值達4.3億美元,持續維持市場主導地位。傳統平衡塊由鉛製成,但由於監管限制,許多地區已轉向使用鋅或鋼作為替代品,這增加了與重新設計製造流程和採購新材料相關的生產成本。發展中經濟體嚴重依賴商用車隊和經濟型汽車,仍主要使用卡式平衡塊,尤其是在合金輪圈較不常見的地區,例如南美洲、東歐和亞洲部分地區。為了滿足這些需求,製造商正專注於開發新材料,包括先進合金、聚合物塗層鋼和鍍鋅鋼。

乘用車市場在2024年佔據了61%的市場佔有率,預計在預測期內將顯著成長。合金輪圈在乘用車中的日益普及,帶動了對創新平衡技術的需求成長,例如黏貼式平衡塊,這種技術可以防止車輪表面損壞並提升車輛外觀。這一趨勢在城市地區和高階汽車領域尤其明顯,因為這些地區的消費者兼顧性能和美觀。隨著乘用車的老化,其轉售價值和維護價值的提升,也刺激了售後市場對平衡服務的需求持續成長。

2024年,北美輪胎平衡重市場佔30%的市場佔有率,其中美國貢獻了2.015億美元。該地區受益於自動化平衡機械的進步,這些機械融合了雷射測量、兩點最佳化和數位診斷技術。這些創新不僅提高了服務的準確性和效率,還能與胎壓監測系統整合,從而提升車輛的整體安全性和性能。 Hunter Engineering和CEMB等產業領導者處於市場數位轉型的前沿,推動北美朝向更智慧、更精確的平衡技術邁進。此外,嚴格的環境法規已促使該地區全面淘汰鉛基平衡重,從而加速了更安全、更環保的替代方案的採用。

主導全球輪胎平衡重市場的主要參與者包括寶龍汽車公司、3M 公司、亨特工程公司、軒尼詩工業公司(現為高士公司)、東邦工業公司、Plombco 和 WEGMANN 汽車公司。

輪胎平衡重領域的領導企業採用多種策略方法來鞏固其市場地位並擴大市場影響力。材料和製造流程的創新是主要關注點,企業大力投資開發環保、輕巧且耐用的傳統鉛塊替代品。這不僅符合不斷變化的環境法規,還能滿足客戶對更高效能的需求。此外,企業正在將自動化和數位技術整合到生產和服務設備中,從而提高精度並縮短週轉時間,對原始設備製造商和車隊營運商都具有吸引力。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 售後服務和輪胎更換業務的興起

- 更嚴格的車輛安全法規

- 從鉛到無毒材料的環保轉變

- 輪胎和車輪設計的技術進步

- 產業陷阱與挑戰

- 發展中地區缺乏意識

- 已開發經濟體的市場飽和

- 市場機會

- 無鉛環保材料需求激增

- 電動車和混合動力車的普及率不斷上升

- 汽車後市場服務快速擴張的新趨勢

- 智慧車間技術整合

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 生產統計

- 生產中心

- 消費中心

- 匯出和匯入

- 成本細分分析

- 專利分析

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃和資金

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 夾式砝碼

- 黏性/黏貼式配重塊

第6章:市場估計與預測:依資料,2021 - 2034 年

- 主要趨勢

- 鋼

- 鋅

- 帶領

- 其他

第7章:市場估計與預測:依車型,2021 - 2034 年

- 主要趨勢

- 搭乘用車

- 掀背車

- 轎車

- SUV(運動型多用途車)

- 商用車

- 輕型商用車(LCV)

- 中型商用車(MCV)

- 重型商用車(HCV)

- 二輪車

- 越野車

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 汽車修理廠

- 輪胎店

- 汽車製造商

- 車隊營運商

第9章:市場估計與預測:依銷售管道,2021 - 2034 年

- 主要趨勢

- 原始設備製造商

- 售後市場

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐人

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 馬來西亞

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第 11 章:公司簡介

- 3M Company

- Alpha Autoparts

- Baolong Automotive Corp.

- Bharat Balancing Weights Pvt.

- Cangzhou Yaqiya Auto Parts (Yaqiya)

- Hatco / HARTEC sal

- HEBEI FANYA

- HEBEI XST

- Hennessy Industries (now Coats Company)

- Holman

- Hunter Engineering Company

- John Bean Technologies Corp.

- Micro-Poise Measurement Systems (AMETEK)

- Plombco Inc.

- Shengshi Weiye (Cangzhou Shengshiweiye)

- Snap-on Incorporated

- TOHO KOGYO Co.

- Trax JH

- WEGMANN Automotive

- Wurth USA

The Global Tire Balance Weight Market was valued at USD 772.3 million in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 1.5 billion by 2034. This growth is largely fueled by the rapid increase in automobile production worldwide, particularly in emerging markets. As car ownership rises and commercial vehicle fleets expand, the demand for regular tire maintenance, including wheel balancing, has surged, especially in bustling urban centers with high mobility needs. Furthermore, growing investments by public sectors in infrastructure and the rising transportation demands driven by logistics, passenger transit, and e-commerce sectors have intensified fleet servicing activities, creating a robust need for tire balance weights. Since these components play a critical role in ensuring vehicle safety and ride comfort, their demand naturally scales alongside the global vehicle population.

Governments and regulatory bodies across various regions are tightening safety and road compliance standards, which also drives the market. Proper wheel balancing-made possible through tire balance weights-eliminates unwanted vibrations, extends tire lifespan, improves driving safety at high speeds, and reduces overall maintenance costs. Enhanced adherence to these regulations, especially in North America, Europe, and Asia, is compelling vehicle operators to adopt routine tire maintenance, thereby bolstering demand. Moreover, the combination of regulatory compliance and rising consumer and fleet operator awareness about vehicle performance and safety continues to be a fundamental driver behind the market's steady expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $772.3 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 6.8% |

In 2024, the clip-on weights segment generated USD 430 million in 2024, maintaining a dominant position in the market. Traditionally manufactured from lead, many regions have shifted toward zinc or steel alternatives due to regulatory restrictions, which have increased production costs related to redesigning manufacturing processes and sourcing new materials. Developing economies, which rely heavily on commercial fleets and budget vehicles, still predominantly use clip-on weights, especially where alloy wheels are less common, such as in South America, Eastern Europe, and parts of Asia. To meet these demands, manufacturers are focusing on developing new materials including advanced alloys, polymer-coated steel, and zinc-coated steel.

The passenger car segment held a 61% share in 2024 and is expected to experience considerable growth over the forecast period. The rising popularity of alloy wheels in passenger vehicles has led to increased demand for innovative balancing techniques such as stick-on weights, which prevent damage to the wheel surface and enhance vehicle appearance. This trend is strong in urban areas and higher-end vehicle segments, where consumers prioritize both performance and aesthetics. As passenger cars age, their resale and maintenance values encourage sustained aftermarket demand for balancing services.

North America Tire Balance Weight Market held a 30% share in 2024, with the United States contributing USD 201.5 million. The region benefits from advancements in automated balancing machinery that incorporate laser measurement, two-point optimization, and digital diagnostics. These innovations not only improve service accuracy and efficiency but also enable integration with tire pressure monitoring systems, enhancing overall vehicle safety and performance. Industry leaders like Hunter Engineering and CEMB are at the forefront of digital transformation in the market, pushing North America toward smarter, more precise balancing technologies. Additionally, strict environmental regulations have led to a complete phase-out of lead-based weights in the region, accelerating the adoption of safer, eco-friendly alternatives.

Key players dominating the Global Tire Balance Weight Market include Baolong Automotive Corp., 3M Company, Hunter Engineering Company, Hennessy Industries (now Coats Company), TOHO KOGYO Co., Plombco, and WEGMANN Automotive.

Leading companies in the tire balance weight sector employ several strategic approaches to strengthen their market presence and expand their foothold. Innovation in materials and manufacturing processes is a primary focus, with firms investing heavily in developing eco-friendly, lightweight, and durable alternatives to traditional lead weights. This enables compliance with evolving environmental regulations while meeting customer demand for higher performance. Additionally, companies are embracing automation and digital technology integration in production and service equipment, which enhances precision and reduces turnaround times, appealing to OEMs and fleet operators alike.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 End use

- 2.2.6 Sales channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in aftermarket services & tire replacement

- 3.2.1.2 Stricter regulations for vehicle safety

- 3.2.1.3 Environmental shift from lead to non-toxic materials

- 3.2.1.4 Technological advancements in tire & wheel design

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of awareness in developing regions

- 3.2.2.2 Market saturation in developed economies

- 3.2.3 Market opportunities

- 3.2.3.1 Surging demand for lead-free and eco-friendly materials

- 3.2.3.2 Rising EV and hybrid vehicle adoption

- 3.2.3.3 Emerging trends of rapid expansion in automotive aftermarket services

- 3.2.3.4 Integration of smart workshop technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Clip-on weights

- 5.3 Adhesive/Stick-on weights

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Million, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Zinc

- 6.4 Lead

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Million, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUVs (Sport utility vehicles)

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCVs)

- 7.3.2 Medium commercial vehicles (MCVs)

- 7.3.3 Heavy commercial vehicles (HCVs)

- 7.4 Two-wheelers

- 7.5 Off-road vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 Automotive workshops

- 8.3 Tire shops

- 8.4 Vehicle manufacturers

- 8.5 Fleet operators

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 3M Company

- 11.2 Alpha Autoparts

- 11.3 Baolong Automotive Corp.

- 11.4 Bharat Balancing Weights Pvt.

- 11.5 Cangzhou Yaqiya Auto Parts (Yaqiya)

- 11.6 Hatco / HARTEC s.a.l.

- 11.7 HEBEI FANYA

- 11.8 HEBEI XST

- 11.9 Hennessy Industries (now Coats Company)

- 11.10 Holman

- 11.11 Hunter Engineering Company

- 11.12 John Bean Technologies Corp.

- 11.13 Micro-Poise Measurement Systems (AMETEK)

- 11.14 Plombco Inc.

- 11.15 Shengshi Weiye (Cangzhou Shengshiweiye)

- 11.16 Snap-on Incorporated

- 11.17 TOHO KOGYO Co.

- 11.18 Trax JH

- 11.19 WEGMANN Automotive

- 11.20 Wurth USA

汽車輪胎的全球市場(~2035年):各輪胎類型,各輪圈尺寸,季節,各車輛類型,各用途,各流通管道,各地區,產業趨勢,市場成長的預測(~2035年)

汽車輪胎的全球市場(~2035年):各輪胎類型,各輪圈尺寸,季節,各車輛類型,各用途,各流通管道,各地區,產業趨勢,市場成長的預測(~2035年) 輪胎化學品市場-全球產業規模、佔有率、趨勢、機會及預測,依車輛類型、需求類別、輪胎結構類型、地區及競爭格局細分,2020-2030 年預測

輪胎化學品市場-全球產業規模、佔有率、趨勢、機會及預測,依車輛類型、需求類別、輪胎結構類型、地區及競爭格局細分,2020-2030 年預測 2025年全球汽車輪胎市場報告

2025年全球汽車輪胎市場報告 全球可充電輪胎市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測2025年全球汽車輪胎OEM市場報告

全球可充電輪胎市場研究報告-產業分析、規模、佔有率、成長、趨勢及2025年至2033年預測2025年全球汽車輪胎OEM市場報告 全球充氣輪胎市場

全球充氣輪胎市場 無內胎輪胎的全球市場的評估,車輛類別,各技術類型,各輪圈尺寸,各銷售管道,各地區,機會,預測,2018年~2032年實心輪胎市場(按產品類型和地區分類)2032 年飛機輪胎翻新市場預測:按類型、工藝、輪胎類型、應用、最終用戶和地區進行的全球分析

無內胎輪胎的全球市場的評估,車輛類別,各技術類型,各輪圈尺寸,各銷售管道,各地區,機會,預測,2018年~2032年實心輪胎市場(按產品類型和地區分類)2032 年飛機輪胎翻新市場預測:按類型、工藝、輪胎類型、應用、最終用戶和地區進行的全球分析 2025 年至 2033 年日本輪胎市場報告(按設計、最終用途、車輛類型(乘用車、輕型商用車、中型和重型商用車、二輪車、三輪車、非公路車)、配銷通路、季節和地區分類)

2025 年至 2033 年日本輪胎市場報告(按設計、最終用途、車輛類型(乘用車、輕型商用車、中型和重型商用車、二輪車、三輪車、非公路車)、配銷通路、季節和地區分類)