|

市場調查報告書

商品編碼

1773318

光纖陀螺儀市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Fiber Optics Gyroscope Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

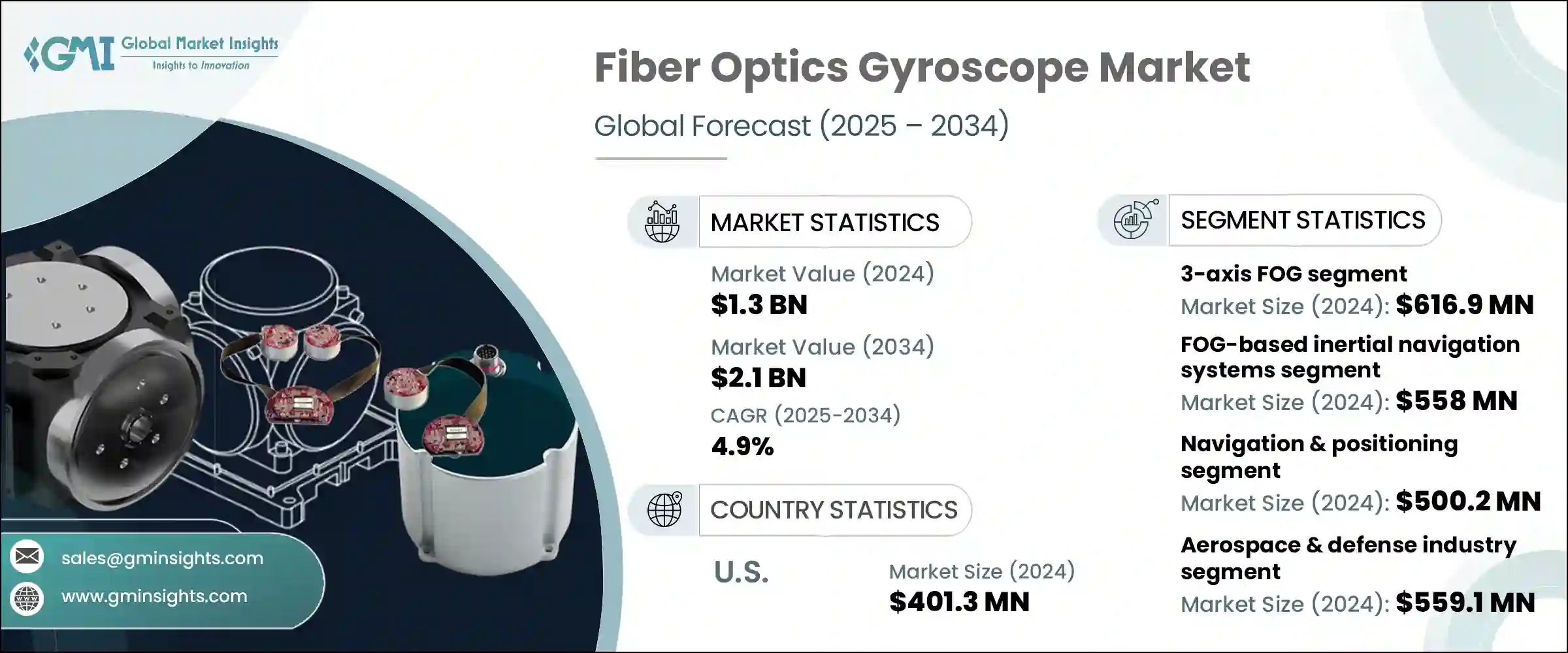

2024年,全球光纖陀螺儀市場規模達13億美元,預計2034年將以4.9%的複合年成長率成長,達到21億美元。國防和航太應用需求的持續成長,以及自動駕駛技術的快速發展,對這一成長產生了顯著影響。光纖陀螺儀 (FOG) 與環形雷射陀螺儀和MEMS陀螺儀等替代產品相比,在敏感的國防環境中具有顯著優勢。它們無需移動部件,不受電磁干擾,並提供更高的精度和長期穩定性,使其成為關鍵任務系統的理想選擇,並確保持續的市場需求。

自動駕駛汽車領域(包括無人駕駛汽車和無人機)的不斷擴張是推動成長的重要因素。這些平台需要在GPS訊號可能失效的情況下獲得可靠的方向和導航資料。光纖陀螺儀 (FOG) 的抗振性、高精度和故障安全設計使其在這些用例中不可或缺。雖然MEMS陀螺儀通常滿足低成本需求,但對於需要可靠性和冗餘性的應用,FOG仍然是高階標準。各公司擴大投資於FOG輔助導航,以支援可擴展的全天候功能,並降低安全關鍵型系統的風險。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 13億美元 |

| 預測值 | 21億美元 |

| 複合年成長率 | 4.9% |

2024年,三軸光纖陀螺(FOG)市場規模達6.169億美元。這些系統採用緊湊設計,整合X、Y和Z軸感測,從而減輕了重量和尺寸。這有利於其在飛彈、無人機、自動駕駛汽車和下一代飛行系統中的部署。隨著國防機構優先考慮高超音速和先進航太平台的多軸導航,三軸光纖陀螺變得越來越重要。電動垂直起降飛機和自主無人機的興起也加速了對這些解決方案的需求,因為它們具有高度穩定性和精確控制能力。儘管前期成本較高,但與多個單軸陀螺儀相比,其長期維護成本的降低將繼續推動其應用。

2024年,基於光纖陀螺(FOG)的慣性導航系統市場規模達5.58億美元。這些系統在GPS訊號不可靠或受損的環境中至關重要。軍用飛機、水下航行器和飛彈系統都依賴基於光纖陀螺的慣性導航系統(INS)來實現抗干擾和長時間導航性能。這種需求也延伸到了商業領域,例如城市自動駕駛汽車、物流無人機和智慧空中交通解決方案,它們都使用光纖陀螺在隧道或城市景觀等受阻環境中進行定位。

2024年,德國光纖陀螺儀市場規模達7,340萬美元。該國強勁的汽車製造和工業自動化產業是其發展的關鍵驅動力。光纖陀螺儀因其高精度運動感測特性,正被應用於高階駕駛輔助系統(ADAS)開發和自動駕駛汽車研發專案。此外,德國在航太和國防製造業的強大實力,以及專注於開發先進導航技術的國內企業,也支撐著其在該市場的不斷擴張。

著名的市場參與者包括 iMAR Navigation、KVH Industries、SkyMEMS、Optolink、Tamagawa Seiki、Advanced Navigation、Emcore、Exail、Safran、Mostatech、Northrop Grumman Litef、Cielo Inertial Solutions、Honeywell International 和 Nedaero Components。光纖陀螺儀市場的領先公司專注於將創新、產品差異化和長期國防合約結合起來,以建立自己的市場地位。許多公司投入巨資進行研發,以開發更輕、更緊湊、穩定性和精度更高的多軸 FOG 裝置,使其適合整合到先進的航太、海軍和自主平台中。與政府機構和私人國防承包商建立戰略合作夥伴關係有助於確保重複業務。一些公司也在國防預算不斷增加的地區擴大製造足跡。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 成本結構

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 國防和航太領域的需求不斷成長

- 自動駕駛汽車的擴張

- 石油和天然氣探勘的成長

- 光纖陀螺技術的進步

- 太空探索活動不斷增多

- 產業陷阱與挑戰

- 製造成本高

- 來自替代技術的競爭

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 未來市場趨勢

- 波特的分析

- PESTEL分析

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 按產品

- 定價策略

- 新興商業模式

- 合規性要求

- 永續性措施

- 消費者情緒分析

- 專利和智慧財產權分析

- 地緣政治與貿易動態

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 市場集中度分析

- 按地區

- 關鍵參與者的競爭基準

- 財務績效比較

- 收入

- 利潤率

- 研發

- 產品組合比較

- 產品範圍廣度

- 科技

- 創新

- 地理位置比較

- 全球足跡分析

- 服務網路覆蓋

- 各區域市場滲透率

- 競爭定位矩陣

- 領導者

- 挑戰者

- 追蹤者

- 利基市場參與者

- 戰略展望矩陣

- 財務績效比較

- 2021-2024 年關鍵發展

- 併購

- 夥伴關係和合作

- 技術進步

- 擴張和投資策略

- 永續發展舉措

- 數位轉型舉措

- 新興/新創企業競爭對手格局

第5章:市場估計與預測:按軸類型,2021 年至 2034 年

- 主要趨勢

- 單軸光纖陀螺

- 雙軸光纖陀螺

- 三軸光纖陀螺

第6章:市場估計與預測:按設備,2021 年至 2034 年

- 主要趨勢

- 基於光纖陀螺羅盤

- 基於光纖陀螺的慣性測量單元

- 基於光纖陀螺的慣性導航系統

- 基於光纖陀螺的姿態航向參考系統

- 其他

第7章:市場估計與預測:按應用,2021 年至 2034 年

- 主要趨勢

- 導航定位

- 穩定系統

- 機器人與自動化

- 引導系統

- 其他

第8章:市場估計與預測:按最終用途產業,2021 年至 2034 年

- 主要趨勢

- 航太與國防

- 汽車

- 海洋和海底

- 石油和天然氣

- 其他

第9章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第10章:公司簡介

- Advanced Navigation

- Cielo Inertial Solutions

- Emcore

- Exail

- Honeywell International

- iMAR Navigation

- KVH Industries

- Mostatech

- Nedaero Components

- Northrop Grumman Litef

- Optolink

- Safran

- SkyMEMS

- Tamagawa Seiki

The Global Fiber Optics Gyroscope Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 2.1 billion by 2034. This growth is strongly influenced by increased demand from defense and aerospace applications, along with rapid strides being made in autonomous mobility. Fiber optics gyroscopes (FOGs) offer distinct advantages over alternatives like ring laser and MEMS gyroscopes, particularly in sensitive defense environments. They operate without moving parts, are immune to electromagnetic interference, and deliver greater accuracy and long-term stability-making them ideal for mission-critical systems and ensuring sustained market demand.

A significant contributor to growth is the expanding autonomous vehicle landscape, including self-driving cars and unmanned aerial vehicles. These platforms require dependable orientation and navigation data in conditions where GPS signals may fail. The vibration resistance, high accuracy, and fail-safe design of FOGs make them indispensable in such use cases. While MEMS gyroscopes often serve low-cost needs, FOGs remain the premium standard for applications requiring reliability and redundancy. Companies are increasingly investing in FOG-assisted navigation to support scalable, all-weather functionality and to reduce risk in safety-critical systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 4.9% |

In 2024, the 3-axis FOG segment generated USD 616.9 million. These systems offer integrated X, Y, and Z-axis sensing within a compact design that reduces weight and size. This benefits deployment in missiles, UAVs, autonomous vehicles, and next-gen flight systems. As defense organizations prioritize multi-axis navigation in hypersonic and advanced aerospace platforms, 3-axis FOGs are becoming more essential. The rise of electric vertical takeoff and landing aircraft and autonomous drones is also accelerating demand for these solutions, due to their altitude stability and precise control. Despite their upfront cost, the long-term reduction in maintenance costs compared to multiple single-axis gyros continues to drive adoption.

The FOG-based inertial navigation systems segment generated USD 558 million in 2024. These systems are critical in environments where GPS is unreliable or compromised. Military-grade aircraft, underwater vessels, and missile systems rely on FOG-based INS for jam-resistant and long-duration navigation performance. This demand also extends to the commercial sector, where urban autonomous vehicles, logistics drones, and smart air mobility solutions use FOGs for positioning in obstructed environments like tunnels or cityscapes.

Germany Fiber Optics Gyroscope Market was valued at USD 73.4 million in 2024. The nation's robust automotive manufacturing and industrial automation sectors are key drivers. FOGs are being adopted in ADAS development and autonomous vehicle R&D programs for their high-precision motion sensing. Additionally, Germany's strong presence in aerospace and defense manufacturing, along with domestic companies focused on developing advanced navigation technologies, supports the country's expanding footprint in this market.

Prominent market players include iMAR Navigation, KVH Industries, SkyMEMS, Optolink, Tamagawa Seiki, Advanced Navigation, Emcore, Exail, Safran, Mostatech, Northrop Grumman Litef, Cielo Inertial Solutions, Honeywell International, and Nedaero Components. Leading companies in the fiber optics gyroscope market focus on a blend of innovation, product differentiation, and long-term defense contracts to build their market presence. Many invest heavily in R&D to develop lighter, more compact multi-axis FOG units with enhanced stability and precision, making them suitable for integration into advanced aerospace, naval, and autonomous platforms. Strategic partnerships with government agencies and private defense contractors help secure repeat business. Some firms are also expanding their manufacturing footprint in regions with rising defense budgets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Axis type trends

- 2.2.2 Device trends

- 2.2.3 Application trends

- 2.2.4 End use Industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO Perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical Success Factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand in defense & aerospace

- 3.2.1.2 Expansion of autonomous vehicles

- 3.2.1.3 Growth in oil & gas exploration

- 3.2.1.4 Advancements in FOG technology

- 3.2.1.5 Rising space exploration activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs

- 3.2.2.2 Competition from alternative technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Future market trends

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technological trends

- 3.8.2 Emerging technologies

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By product

- 3.10 Pricing strategies

- 3.11 Emerging business models

- 3.12 Compliance requirements

- 3.13 Sustainability measures

- 3.14 Consumer sentiment analysis

- 3.15 Patent and IP analysis

- 3.16 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Axis Type, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 1-Axis FOG

- 5.3 2-Axis FOG

- 5.4 3-Axis FOG

Chapter 6 Market Estimates and Forecast, By Device, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 FOG-based gyrocompass

- 6.3 FOG-based inertial measurement unit

- 6.4 FOG-based inertial navigation system

- 6.5 FOG-based attitude heading reference system

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Navigation & positioning

- 7.3 Stabilization systems

- 7.4 Robotics & automation

- 7.5 Guidance system

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 Marine & subsea

- 8.5 Oil & gas

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Advanced Navigation

- 10.2 Cielo Inertial Solutions

- 10.3 Emcore

- 10.4 Exail

- 10.5 Honeywell International

- 10.6 iMAR Navigation

- 10.7 KVH Industries

- 10.8 Mostatech

- 10.9 Nedaero Components

- 10.10 Northrop Grumman Litef

- 10.11 Optolink

- 10.12 Safran

- 10.13 SkyMEMS

- 10.14 Tamagawa Seiki