|

市場調查報告書

商品編碼

1773313

鋁蜂窩板市場機會、成長動力、產業趨勢分析及2025-2034年預測Aluminum Honeycomb Panels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

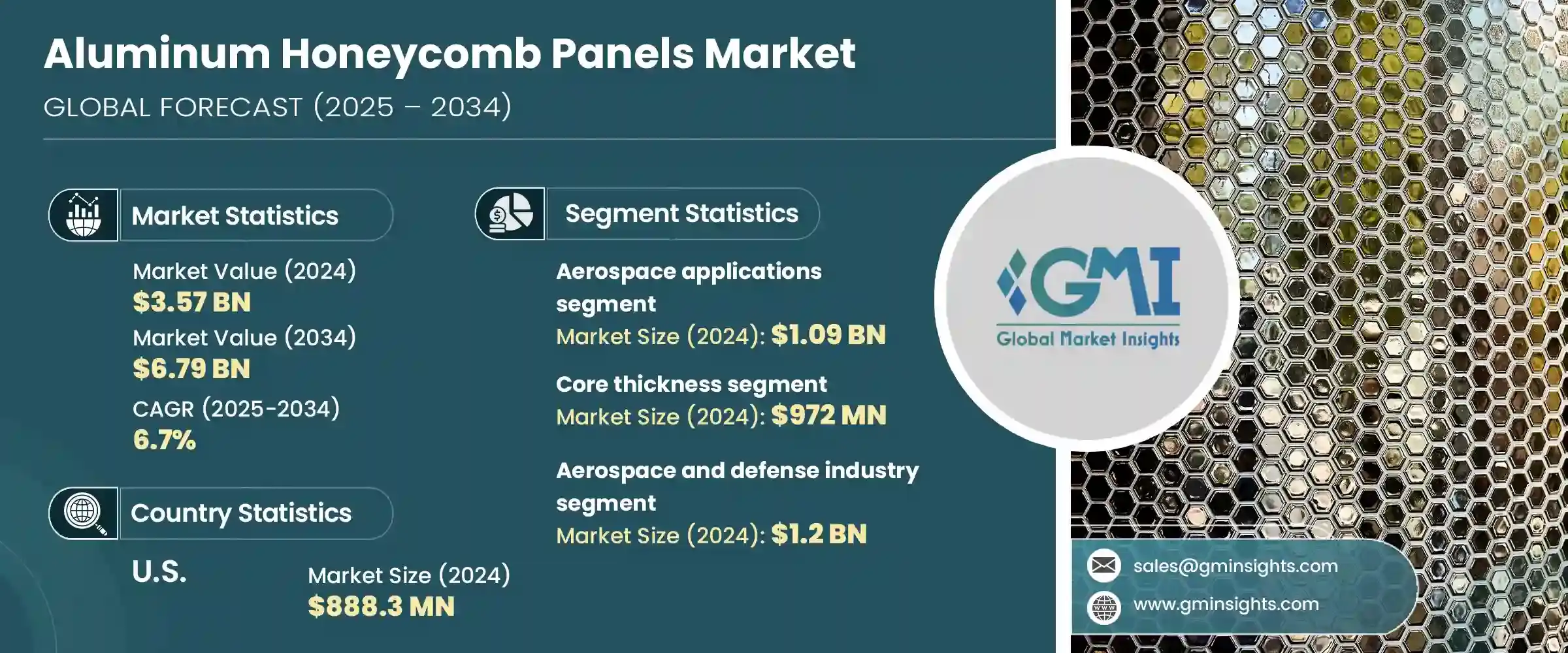

2024年,全球鋁蜂窩板市場價值為35.7億美元,預計到2034年將以6.7%的複合年成長率成長,達到67.9億美元。這一成長主要源自於多個高性能產業日益成長的應用需求,這些產業需要兼具強度和輕量化的材料。在性能效率和結構完整性至關重要的行業,例如航太、汽車、建築和工業製造,這種需求尤其突出。這些板材因其能夠滿足與能量吸收、耐久性和抗各種應力相關的嚴格要求,且不會顯著增加結構重量而廣受認可。

隨著各行各業不斷追求節能和永續發展的目標,對輕質且堅固耐用材料的需求日益成長,而鋁蜂窩板正是理想的解決方案。這些材料在現代基礎設施、交通運輸系統和專用設備外殼中的應用日益成長,進一步鞏固了其在全球市場中日益成長的重要性。其可回收性、防火性和隔熱性能使其更具吸引力,適用於兼顧功能性和環保性的各類應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 35.7億美元 |

| 預測值 | 67.9億美元 |

| 複合年成長率 | 6.7% |

在航太領域,鋁蜂窩板因其滿足輕質、高強度等關鍵標準而迅速受到青睞。光是航太應用領域,其市場規模在2024年就已達10.9億美元,預計2025年至2034年的複合年成長率將達到7.5%。這些面板有助於提高燃油效率並增強設計靈活性,這在航空製造中至關重要。它們的應用範圍擴展到室內隔間、地板系統和結構構件,在這些領域,減輕重量至關重要,同時又不影響性能。隨著飛機製造商越來越重視成本效益和省油技術,對鋁蜂巢結構的偏好也日益增強。

這些材料在建築業也越來越受歡迎。它們兼具輕量和高剛度,安裝更便捷、使用壽命更長,並在結構性能方面表現出色。此外,它們的防火隔音特性也使其在覆層系統、天花板和隔間中的應用日益廣泛,尤其是在商業和機構建築中。綠色建築規範和永續建築的轉變,使得鋁蜂窩板在建築實踐中的應用越來越廣泛,尤其是在已開發經濟體中。

從產品規格的角度來看,市場正透過芯材厚度、合金類型和單元配置方面的創新不斷發展。芯材厚度細分市場在2024年的市值為9.72億美元,預計在預測期內將以7%的複合年成長率成長。不同的芯材尺寸可為各種應用提供客製化的承重能力,而特定的合金則可增強耐腐蝕性並最佳化結構性能。製造商也在開發客製化的面板形狀和尺寸,以滿足特定的設計或技術要求。這些創新使鋁蜂窩板能夠更好地適應多個行業的複雜環境。

就最終用途而言,航太和國防工業在2024年佔據了最大的市場佔有率,價值12億美元,佔32.4%的市場佔有率。預計到2034年,該領域的複合年成長率將達到7.2%。這一成長主要得益於國防項目投資的增加,以及先進國防系統對輕質材料的日益重視。在汽車產業,尤其是電動車領域,太陽能板透過減輕車輛總重量,有助於延長續航里程並提高性能。

此外,由於耐腐蝕性、熱穩定性和易於製造等需求,其在船舶、鐵路和物流等領域的應用也日益廣泛。這些特性使板材非常適合用於船舶內部、火車車廂和貨運系統。工業製造商也依賴這些板材來建造敏感設備的結構框架和外殼,這凸顯了其多功能性和性能的一致性。

在美國,2024年鋁蜂窩板市場規模達8.883億美元,預計2025年至2034年期間的複合年成長率將達到6.5%。美國作為全球飛機生產中心的地位,以及對電動車和軍事升級的投資不斷增加,為市場擴張創造了有利條件。商業建築對環保建築實踐和能源效率的重視,進一步支撐了國內需求。

在競爭格局中,主要的複合材料和材料生產商憑藉先進的製造流程、多樣化的產品組合以及跨供應鏈的策略合作夥伴關係佔據市場主導地位。這些公司持續投資研發,以提高產品強度、耐火性和適應性,以滿足不斷發展的行業標準。透過使生產符合全球監管規範和永續發展目標,這些公司保持了競爭優勢,並滿足了大批量和高規格的市場需求。他們與原始設備製造商和承包商建立的良好關係確保了長期的業務連續性,而他們對自動化和品質控制的承諾則鞏固了他們在關鍵終端應用領域的領先地位。

目錄

第1章:方法論

- 市場範圍和定義

- 研究設計

- 研究方法

- 資料收集方法

- 資料探勘來源

- 全球的

- 地區/國家

- 基礎估算與計算

- 基準年計算

- 市場評估的主要趨勢

- 初步研究和驗證

- 主要來源

- 預測模型

- 研究假設和局限性

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商概況

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL分析

- 價格趨勢

- 按地區

- 按產品

- 未來市場趨勢

- 科技與創新格局

- 當前的技術趨勢

- 新興技術

- 專利態勢

- 貿易統計(HS編碼)(註:僅提供重點國家的貿易統計資料)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測、應用,2021-2034

- 主要趨勢

- 航太應用

- 商業航空

- 飛機地板系統

- 內裝面板和零件

- 結構應用

- 軍事和國防航空

- 太空和衛星應用

- 商業航空

- 汽車應用

- 電動汽車零件

- 碰撞吸收系統

- 結構加固

- 內部和外部面板

- 建築與建築

- 帷幕牆系統

- 外牆覆層

- 室內設計應用

- 屋頂和結構構件

- 船舶應用

- 造船和海軍應用

- 遊艇和休閒船製造

- 海上平台建造

- 工業應用

- 機械設備製造業

- 工裝和夾具

- 無塵室與實驗室應用

- 交通運輸及鐵路

- 高鐵應用

- 城市交通系統

- 商用車應用

- 其他

- 家具與設計

- 再生能源應用

- 體育和娛樂設備

第6章:市場估計與預測:依核心類型和規格,2021-2034

- 主要趨勢

- 芯材厚度

- 超薄(5mm-10mm)

- 標準(11毫米-25毫米)

- 中號(26毫米-50毫米)

- 厚(51毫米-100毫米)

- 重型(100mm以上)

- 鋁合金型

- 3003合金(商業級)

- 5052合金(航太級)

- 5056合金(高性能應用)

- 其他特種合金

- 單元尺寸和配置

- 標準六角形細胞

- 微蜂巢配置

- 客製化電池幾何形狀

- 面板材質

- 鋁面板

- 複合面板

- 混合配置

- 面板尺寸和尺寸

- 標準面板

- 大尺寸面板

- 客製尺寸的應用程式

第7章:市場估計與預測:按最終用途產業,2021-2034 年

- 主要趨勢

- 航太和國防工業

- 汽車產業

- 建築業

- 商業建築

- 住宅應用

- 基礎建設發展

- 海洋和造船業

- 商業運輸

- 海軍和國防應用

- 休閒海洋市場

- 海上能源領域

- 運輸和物流

- 軌道交通

- 商用車

- 大眾運輸系統

- 工業製造

- 機械設備

- 潔淨室應用

- 專業工業用途

- 其他

- 能源和發電

- 體育和娛樂

- 家具和室內設計

第8章:市場估計與預測:按地區,2021-2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 歐洲其他地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 中東和非洲其他地區

第9章:公司簡介

- 3A Composites Holding AG

- Hexcel Corporation

- Plascore Inc.

- Alcoa Corporation

- Novelis Inc.

- Hunter Douglas NV

- Toray Advanced Composites

- Euro-Composites SA

- Collins Aerospace (Raytheon Technologies)

- Argosy International Inc.

- Alucoil SL

- Pacific Panels Inc.

- Benecor Inc.

- Liming Honeycomb Composites Co., Ltd.

- KUMZ (Kamensk-Uralsky Metallurgical Works)

- Eco Earth Solutions

- Renoxbell Group

- Foshan Alucrown Building Materials Co., Ltd.

- Mass Transit Equipment LLP

- UACJ Corporation

- Schweiter Technologies AG

- Shinko-North Co., Ltd.

- Guangzhou Aloya Renoxbell Aluminum Co., Ltd.

- Advanced Custom Manufacturing

- Zodiac Aerospace (Safran)

- B/E Aerospace

- Triumph Group Inc.

- The NORDAM Group LLC

- Flatiron Panel Products

- Corex-Honeycomb

- 3M Company

- Armacell International SA

- MC Gill Corporation

- TenCate Advanced Composites

- Oerlikon Metco

- Boeing Encore Interiors LLC

- Safran SA

- Rockwell Collins (Collins Aerospace)

- Avcorp Industries Inc.

- Yamaton Corporation

- Shuangdie Group

- SPEE3D

- Zimmermann Group

- BoDo Plastics

- Duramax

- LIDA PLASTIC INDUSTRY

- Gayatri Corporation

- Viva Composite Panel Pvt Ltd

- Go Alubuild Pvt Ltd

- Kukreja Brothers

- Uniwell International Enterprises Corp.

- Prance Building Materials

- DJ Aluminum

- Alumetal

- TOPCOMB

- Chaluminium

- Jixiang Aluminum

The Global Aluminum Honeycomb Panels Market was valued at USD 3.57 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 6.79 billion by 2034. This growth is primarily driven by increasing applications across multiple high-performance industries that require materials combining strength with low weight. The demand is particularly pronounced in sectors where performance efficiency and structural integrity are key, such as aerospace, automotive, construction, and industrial manufacturing. These panels are widely recognized for their ability to meet stringent requirements related to energy absorption, durability, and resistance to various stresses without significantly increasing the weight of structures.

As industries continue to pursue energy-saving and sustainability goals, the demand for lightweight yet robust materials is rising, which makes aluminum honeycomb panels an ideal solution. The rising trend of using these materials in modern infrastructure, transportation systems, and specialized equipment housing further supports their growing relevance in global markets. Their appeal is enhanced by their recyclability, fire resistance, and thermal insulation properties, making them suitable for a wide range of applications that require both functionality and environmental responsibility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.57 billion |

| Forecast Value | $6.79 billion |

| CAGR | 6.7% |

In the aerospace segment, aluminum honeycomb panels are gaining rapid traction as they fulfill essential criteria such as lightweight and high strength. The aerospace applications segment alone was valued at USD 1.09 billion in 2024 and is projected to register a CAGR of 7.5% from 2025 to 2034. These panels help enhance fuel efficiency and enable improved design flexibility, which is critical in aviation manufacturing. Their usage extends to interior partitions, flooring systems, and structural elements, where weight reduction is crucial without compromising performance. As aircraft manufacturers increase focus on cost-efficient and fuel-saving technologies, the preference for aluminum honeycomb structures continues to strengthen.

These materials are also finding growing acceptance in the building and construction industry. Their combination of low weight and high rigidity allows for easier installation, longer lifespan, and superior performance in structural roles. Their fire-resistant and sound-insulating features further contribute to their use in cladding systems, ceilings, and partitions, particularly in commercial and institutional buildings. The shift toward green building codes and sustainable architecture has led to higher adoption of aluminum honeycomb panels in construction practices, especially in developed economies.

From a product specification standpoint, the market is advancing through innovations in core thickness, alloy types, and cell configurations. The core thickness segment, which was valued at USD 972 million in 2024, is expected to grow at a CAGR of 7% over the forecast period. Varying core dimensions offer customized load-bearing capabilities across applications, while specific alloys enhance corrosion resistance and optimize structural performance. Manufacturers are also developing tailored panel shapes and sizes to cater to specific design or technical requirements. These innovations are making aluminum honeycomb panels more adaptable to complex environments across multiple industries.

In terms of end-use, the aerospace and defense industry accounted for the largest share of the market in 2024, valued at USD 1.2 billion and holding a 32.4% market share. This segment is expected to expand at a CAGR of 7.2% through 2034. The growth is fueled by increased investment in national defense programs and a growing emphasis on lightweight materials for advanced defense systems. In the automotive industry, particularly in the electric vehicle segment, the panels contribute to extended range and better performance by reducing overall vehicle weight.

Additionally, their growing usage in sectors like marine, rail, and logistics is driven by the need for corrosion resistance, thermal stability, and ease of fabrication. These characteristics make the panels well-suited for use in ship interiors, train compartments, and cargo systems. Industrial manufacturers also rely on these panels to build structural frames and enclosures for sensitive equipment, which highlights their versatility and performance consistency.

In the United States, the aluminum honeycomb panels market was valued at USD 888.3 million in 2024 and is projected to grow at a CAGR of 6.5% from 2025 to 2034. The country's position as a global hub for aircraft production, along with rising investments in electric vehicles and military upgrades, is creating favorable conditions for market expansion. The emphasis on environmentally friendly construction practices and energy efficiency in commercial buildings further supports domestic demand.

The competitive landscape features major composite and material producers who dominate the market through a combination of advanced manufacturing, diverse product portfolios, and strategic partnerships across supply chains. These companies continuously invest in research and development to improve product strength, fire resistance, and adaptability to meet evolving industrial standards. By aligning production with global regulatory norms and sustainability targets, these firms maintain their competitive edge and cater to both high-volume and high-specification market demands. Their established relationships with OEMs and contractors ensure long-term business continuity, while their commitment to automation and quality control reinforces their leadership in critical end-use segments.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Application

- 2.2.3 Core Type and Specifications

- 2.2.4 End use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Application, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aerospace applications

- 5.2.1 Commercial aviation

- 5.2.1.1 Aircraft flooring systems

- 5.2.1.2 Interior panels and components

- 5.2.1.3 Structural applications

- 5.2.2 Military and defense aviation

- 5.2.3 Space and satellite applications

- 5.2.1 Commercial aviation

- 5.3 Automotive applications

- 5.3.1 Electric vehicle components

- 5.3.2 Crash absorption systems

- 5.3.3 Structural reinforcements

- 5.3.4 Interior and exterior panels

- 5.4 Construction and architecture

- 5.4.1 Curtain wall systems

- 5.4.2 Facade cladding

- 5.4.3 Interior design applications

- 5.4.4 Roofing and structural elements

- 5.5 Marine applications

- 5.5.1 Ship building and naval applications

- 5.5.2 Yacht and recreational boat manufacturing

- 5.5.3 Offshore platform construction

- 5.6 Industrial applications

- 5.6.1 Machinery and equipment manufacturing

- 5.6.2 Tooling and fixtures

- 5.6.3 Clean room and laboratory applications

- 5.7 Transportation and rail

- 5.7.1 High-speed rail applications

- 5.7.2 Urban transit systems

- 5.7.3 Commercial vehicle applications

- 5.8 Others

- 5.8.1 Furniture and design

- 5.8.2 Renewable energy applications

- 5.8.3 Sports and recreation equipment

Chapter 6 Market Estimates & Forecast, By Core Type and Specifications, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Core thickness

- 6.2.1 Ultra-thin (5mm-10mm)

- 6.2.2 Standard (11mm-25mm)

- 6.2.3 Medium (26mm-50mm)

- 6.2.4 Thick (51mm-100mm)

- 6.2.5 Heavy-duty (above 100mm)

- 6.3 Aluminum alloy type

- 6.3.1 3003 alloy (commercial grade)

- 6.3.2 5052 alloy (aerospace grade)

- 6.3.3 5056 alloy (high-performance applications)

- 6.3.4 Other specialized alloys

- 6.4 Cell size and configuration

- 6.4.1 Standard hexagonal cells

- 6.4.2 Micro-cell configurations

- 6.4.3 Custom cell geometries

- 6.5 Face sheet material

- 6.5.1 Aluminum face sheets

- 6.5.2 Composite face sheets

- 6.5.3 Hybrid configurations

- 6.6 Panel size and dimensions

- 6.6.1 Standard panels

- 6.6.2 Large format panels

- 6.6.3 Custom-sized applications

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Aerospace and defense industry

- 7.3 Automotive industry

- 7.4 Building and construction industry

- 7.4.1 Commercial construction

- 7.4.2 Residential applications

- 7.4.3 Infrastructure development

- 7.5 Marine and shipbuilding industry

- 7.5.1 Commercial shipping

- 7.5.2 Naval and defense applications

- 7.5.3 Recreational marine market

- 7.5.4 Offshore energy sector

- 7.6 Transportation and logistics

- 7.6.1 Rail transportation

- 7.6.2 Commercial vehicles

- 7.6.3 Public transportation systems

- 7.7 Industrial manufacturing

- 7.7.1 Machinery and equipment

- 7.7.2 Clean room applications

- 7.7.3 Specialized industrial uses

- 7.8 Others

- 7.8.1 Energy and power generation

- 7.8.2 Sports and recreation

- 7.9 Furniture and interior design

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East & Africa

Chapter 9 Company Profiles

- 9.1 3A Composites Holding AG

- 9.2 Hexcel Corporation

- 9.3 Plascore Inc.

- 9.4 Alcoa Corporation

- 9.5 Novelis Inc.

- 9.6 Hunter Douglas N.V.

- 9.7 Toray Advanced Composites

- 9.8 Euro-Composites S.A.

- 9.9 Collins Aerospace (Raytheon Technologies)

- 9.10 Argosy International Inc.

- 9.11 Alucoil S.L.

- 9.12 Pacific Panels Inc.

- 9.13 Benecor Inc.

- 9.14 Liming Honeycomb Composites Co., Ltd.

- 9.15 KUMZ (Kamensk-Uralsky Metallurgical Works)

- 9.16 Eco Earth Solutions

- 9.17 Renoxbell Group

- 9.18 Foshan Alucrown Building Materials Co., Ltd.

- 9.19 Mass Transit Equipment LLP

- 9.20 UACJ Corporation

- 9.21 Schweiter Technologies AG

- 9.22 Shinko-North Co., Ltd.

- 9.23 Guangzhou Aloya Renoxbell Aluminum Co., Ltd.

- 9.24 Advanced Custom Manufacturing

- 9.25 Zodiac Aerospace (Safran)

- 9.26 B/E Aerospace

- 9.27 Triumph Group Inc.

- 9.28 The NORDAM Group LLC

- 9.29 Flatiron Panel Products

- 9.30 Corex-Honeycomb

- 9.31 3M Company

- 9.32 Armacell International S.A.

- 9.33 MC Gill Corporation

- 9.34 TenCate Advanced Composites

- 9.35 Oerlikon Metco

- 9.36 Boeing Encore Interiors LLC

- 9.37 Safran S.A.

- 9.38 Rockwell Collins (Collins Aerospace)

- 9.39 Avcorp Industries Inc.

- 9.40 Yamaton Corporation

- 9.41 Shuangdie Group

- 9.42 SPEE3D

- 9.43 Zimmermann Group

- 9.44 BoDo Plastics

- 9.45 Duramax

- 9.46 LIDA PLASTIC INDUSTRY

- 9.47 Gayatri Corporation

- 9.48 Viva Composite Panel Pvt Ltd

- 9.49 Go Alubuild Pvt Ltd

- 9.50 Kukreja Brothers

- 9.51 Uniwell International Enterprises Corp.

- 9.52 Prance Building Materials

- 9.53 DJ Aluminum

- 9.54 Alumetal

- 9.55 TOPCOMB

- 9.56 Chaluminium

- 9.57 Jixiang Aluminum

全球Nomex蜂窩市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球Nomex蜂窩市場規模、佔有率、趨勢和成長分析報告(2026-2034年) Nomex蜂巢芯材市場按產品類型、芯材厚度、單元尺寸、原料、終端用戶產業和應用分類-全球預測,2026-2032年蜂窩密封件市場按分銷管道、產品類型、材料、最終用戶和應用分類-2026-2032年全球預測金屬蜂窩支撐材料市場:按應用、終端用戶產業、材質、製造程序和塗層類型分類-2026-2032年全球預測

Nomex蜂巢芯材市場按產品類型、芯材厚度、單元尺寸、原料、終端用戶產業和應用分類-全球預測,2026-2032年蜂窩密封件市場按分銷管道、產品類型、材料、最終用戶和應用分類-2026-2032年全球預測金屬蜂窩支撐材料市場:按應用、終端用戶產業、材質、製造程序和塗層類型分類-2026-2032年全球預測 聚丙烯蜂窩市場規模、佔有率、成長分析(按產品類型、孔徑、密度、應用、終端用戶產業、銷售管道和地區分類)-2026-2033年產業預測

聚丙烯蜂窩市場規模、佔有率、成長分析(按產品類型、孔徑、密度、應用、終端用戶產業、銷售管道和地區分類)-2026-2033年產業預測 蜂窩芯材市場規模、佔有率及成長分析(依材料類型、終端用戶產業、應用及地區分類)-2026-2033年產業預測

蜂窩芯材市場規模、佔有率及成長分析(依材料類型、終端用戶產業、應用及地區分類)-2026-2033年產業預測 航太用鋁蜂巢芯材:全球市場佔有率及排名、總收入及需求預測(2025-2031年)

航太用鋁蜂巢芯材:全球市場佔有率及排名、總收入及需求預測(2025-2031年) Nomex 紙蜂窩芯市場報告:2031 年趨勢、預測與競爭分析

Nomex 紙蜂窩芯市場報告:2031 年趨勢、預測與競爭分析 蜂窩芯材市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭細分,2020-2030 年)國防蜂窩核心市場報告:2030 年趨勢、預測與競爭分析

蜂窩芯材市場-全球產業規模、佔有率、趨勢、機會及預測(按類型、應用、地區和競爭細分,2020-2030 年)國防蜂窩核心市場報告:2030 年趨勢、預測與競爭分析