|

市場調查報告書

商品編碼

1773312

壓制和吹製玻璃市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Pressed and Blown Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

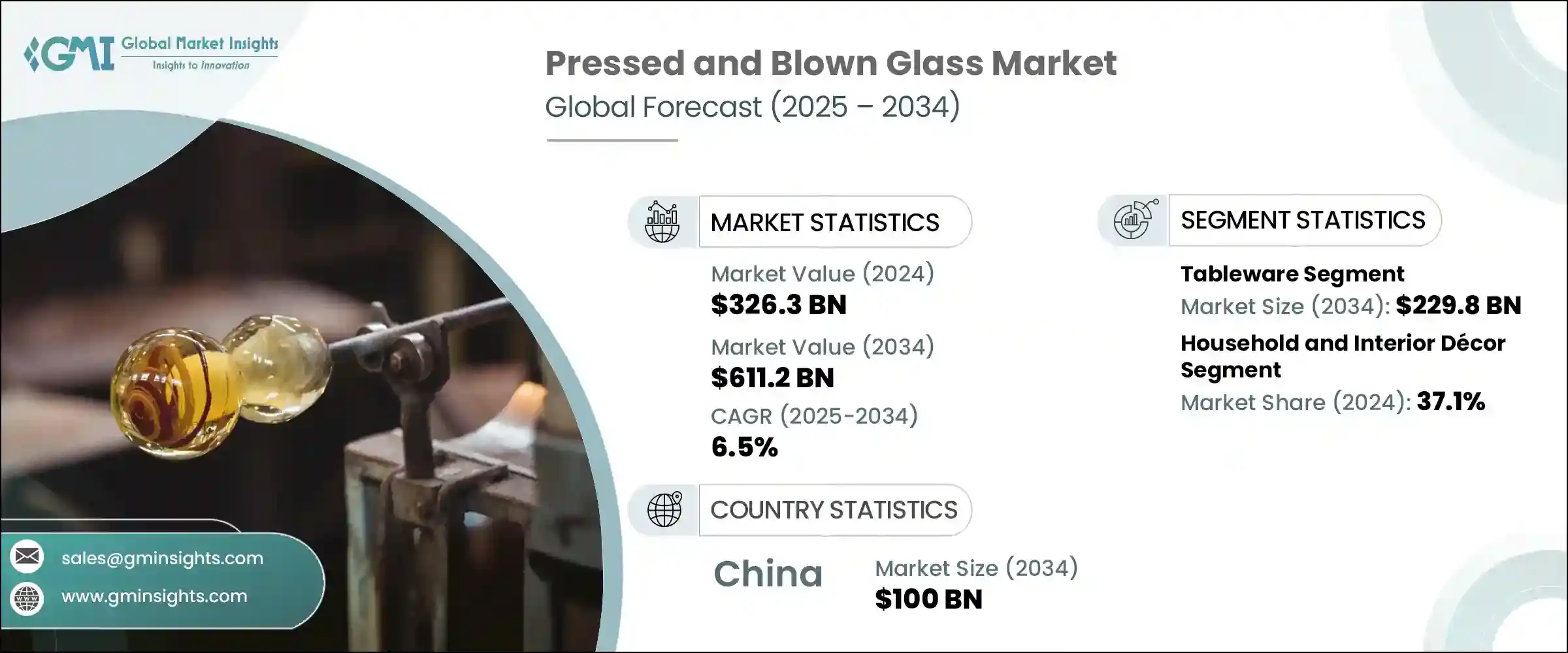

2024年,全球壓制和吹製玻璃市場規模達3,263億美元,預計到2034年將以6.5%的複合年成長率成長,達到6,112億美元。成型技術的進步、建築應用的不斷擴展以及裝飾和包裝用途需求的不斷成長,共同推動著該市場的發展。亞太市場正呈現出強勁成長勢頭,工業擴張和消費者日益富裕的消費群體正在推動玻璃產品在多個垂直領域的普及。

隨著消費者偏好的轉變,玻璃因其功能多樣性和視覺吸引力在現代設計中日益受到青睞,並更加重視性能和美觀。在包裝和內飾等領域,耐用且可回收的玻璃材料正在取代永續性較差的替代品。此外,自動化吹塑和壓制製程的技術升級使製造商能夠實現規模化生產,同時滿足客製化需求。人工智慧整合監控和機器人成型等先進工具正日益受到青睞,從而改善了生產成果和品質控制。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 3263億美元 |

| 預測值 | 6112億美元 |

| 複合年成長率 | 6.5% |

歐洲和北美的營運已開始採用自動化技術,提高速度和效率,並幫助企業滿足日益成長的消費者期望。隨著該產業與全球永續發展目標保持一致,對環保生產方法的持續投資也進一步支持了市場。隨著個人化和高階裝飾產品需求的不斷成長,吹製玻璃正日益受到青睞。同時,壓制玻璃仍然是容器製造的主要材料,在製藥、美容和飲料等行業中發揮著至關重要的作用。

餐具領域在2024年佔據了最大的市場佔有率,產值達到1,212億美元,預計到2034年將達到2,298億美元,複合年成長率為6.7%。玻璃餐具(包括飲具、盤子和盛裝餐具)因其衛生、耐熱和耐用性而持續受到熱捧。環保用餐習慣的興起正促使消費者逐漸遠離塑膠和陶瓷。專注於手工工藝和簡約透明餐具的設計趨勢,推動了北美和歐洲等主要市場的玻璃餐具銷售成長。

2024年,家居及室內裝潢類別的市佔率將達到37.1%。城市發展、人們對現代生活美學日益成長的興趣以及對多功能裝飾品的客製化需求推動了這一成長。玻璃花瓶、燈具、藝術品和裝飾面板等產品越來越受歡迎,尤其是手工製作或永續生產的。消費者對耐用、環保的室內裝飾元素的偏好,推動了包括亞太地區、歐洲和北美在內的多個地區更多地使用壓制和手工吹製的設計。

2024年,中國壓制和吹製玻璃市場產值達527億美元,預計複合年成長率將達到6.7%,到2034年將達到1000億美元。這一成長與消費成長、機械化製造的改進以及向更智慧的生產系統轉型息息相關。中國生產商越來越重視永續性,在生產過程中更多地使用回收碎玻璃,以降低成本並最大限度地減少對環境的影響。年輕一代正在引領客製化和數位玻璃器皿的潮流,推動對獨特美學和實用優雅的需求。

市場領導者包括 Krosno Glass SA、Libbey Inc.、Arc Holdings、Bormioli Rocco 和 Sisecam 集團旗下的 Pasabahce。壓制和吹製玻璃市場的主要公司正在優先考慮技術整合,以提高生產力並減少錯誤。機器人成型系統和人工智慧品質檢測工具正在廣泛部署,以提高一致性並縮短生產時間。為了滿足日益成長的永續解決方案需求,許多公司正在轉向使用再生原料並採用節能製程。對數位設計平台的投資使這些品牌能夠快速製作原型並客製化產品,以滿足工業客戶和注重設計的消費者的需求。與設計師和零售分銷商建立策略合作夥伴關係進一步使公司在風格和功能方面保持領先地位。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 市場機會

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- Pestel 分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 專利格局

- 貿易統計(註:僅提供重點國家的貿易統計)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續實踐

- 減少廢棄物的策略

- 生產中的能源效率

- 環保舉措

- 碳足跡考量

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- MEA

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 餐具

- 飲水杯

- 不倒翁

- 高腳杯

- 馬克杯和杯子

- 小酒杯

- 其他

- 餐具

- 盤子

- 碗

- 上菜

- 其他

- 餐具

- 水罐和醒酒器

- 托盤和大淺盤

- 其他

- 飲水杯

- 容器

- 瓶子

- 飲料瓶

- 藥用瓶

- 化妝品和香水瓶

- 其他

- 罐子

- 食品罐

- 化妝品罐

- 其他

- 小瓶和安瓿瓶

- 其他

- 瓶子

- 裝飾玻璃

- 小雕像和雕塑

- 花瓶和碗

- 裝飾品

- 其他

- 照明產品

- 燈罩

- 枝形吊燈和吊墜

- 其他

- 技術和工業玻璃

- 實驗室玻璃器皿

- 技術組件

- 其他

- 其他

第6章:市場估計與預測:按玻璃類型,2021 - 2034 年

- 主要趨勢

- 鈉鈣玻璃

- 硼矽酸鹽玻璃

- 水晶玻璃

- 鉛水晶

- 無鉛水晶

- 耐熱玻璃

- 彩色玻璃

- 其他

第7章:市場估計與預測:按製造程序,2021 - 2034 年

- 主要趨勢

- 壓制過程

- 單料滴

- 雙料

- 三重料

- 吹塑工藝

- 吹啊吹

- 按壓並吹氣

- 窄頸按壓吹氣(NNPB)

- 組合工藝

- 手工製作流程

- 其他

第8章:市場估計與預測:按最終用途產業,2021 - 2034 年

- 主要趨勢

- 食品和飲料

- 酒精飲料

- 非酒精飲料

- 食品包裝

- 其他

- 製藥

- 包裝

- 實驗室設備

- 其他

- 化妝品和個人護理

- 香水和香料

- 保養產品

- 其他

- 家居和室內裝飾

- 餐具

- 裝飾品

- 燈光

- 其他

- 飯店及餐飲服務

- 飯店和餐廳

- 酒吧和酒館

- 餐飲服務

- 其他

- 其他

第9章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- B2B/直銷

- 製造商到零售商

- 製造商到批發商

- 製造商最終使用

- 零售

- 大賣場/超市

- 專賣店

- 百貨公司

- 其他

- 網路零售

- 公司網站

- 電子商務平台

- 其他

- 其他

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

第 11 章:公司簡介

- Anchor Hocking LLC

- Arc International

- Ardagh Group SA

- Beatson Clark Ltd.

- Bormioli Rocco SpA

- Borosil Limited

- Garbo Glassware Co., Ltd.

- Gerresheimer AG

- Glass Dynamics LLC

- Kopp Glass, Inc.

- Libbey Inc.

- OI Glass, Inc. (Owens-Illinois)

- Piramal Glass Limited

- Rayotek Scientific Inc.

- Saverglass SAS

- SCHOTT AG

- Sisecam Group

- Steelite International

- Stoelzle Glass Group

- Verallia

- Vetropack Holding Ltd.

- Vidrala SA

- Vitro, SAB de CV

- Wiegand-Glas GmbH

- Zwiesel Kristallglas AG

The Global Pressed and Blown Glass Market was valued at USD 326.3 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 611.2 billion by 2034. The market is being propelled by the evolution of molding technologies, expanding architectural applications, and heightened demand for decorative and packaging uses. Significant momentum is being generated in Asia-Pacific markets, where industrial expansion and growing consumer affluence are supporting glass product adoption across multiple verticals.

Glass is increasingly favored for its functional versatility and visual appeal in modern design, with shifting consumer preferences emphasizing both performance and aesthetics. In sectors like packaging and interiors, durable and recyclable glass materials are replacing less sustainable alternatives. Additionally, technological upgrades in automated blowing and pressing processes allow manufacturers to produce at scale while meeting custom requirements. Advanced tools like AI-integrated monitoring and robotic forming are gaining traction, improving production outcomes and quality control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $326.3 Billion |

| Forecast Value | $611.2 Billion |

| CAGR | 6.5% |

European and North American operations have embraced automation, enhanced speed and efficiency, and helping companies meet rising consumer expectations. The market is further supported by ongoing investments in eco-conscious production methods, as the industry aligns itself with global sustainability goals. Blown glass is gaining traction due to rising demand for personalized and high-end decorative products. Meanwhile, pressed glass remains a dominant material in container manufacturing, playing a crucial role in industries such as pharmaceuticals, beauty, and beverages.

The tableware segment held the largest market share in 2024, generating USD 121.2 billion, and is projected to hit USD 229.8 billion by 2034, growing at a CAGR of 6.7%. Glass tableware-including drinkware, plates, and serving items-continues to be in high demand for its hygiene, thermal resistance, and long-term usability. The movement toward environmentally friendly dining habits is steering consumers away from plastics and ceramics. Design trends favoring artisan craftsmanship and minimal, transparent serveware have helped accelerate glass tableware sales in key markets such as North America and Europe.

The household and interior decor category captured a 37.1% share in 2024. This growth is being fueled by urban development, increased interest in modern living aesthetics, and custom orders for multifunctional decorative pieces. Items like glass vases, lighting fixtures, art pieces, and accent panels are seeing a rise in popularity, especially those that are handcrafted or sustainably produced. Consumer preference for long-lasting, eco-friendly interior elements is promoting greater use of both pressed and hand-blown designs across several regions including parts of Asia-Pacific, Europe, and North America.

China Pressed and Blown Glass Market generated USD 52.7 billion in 2024 and is expected to grow at a CAGR of 6.7%, reaching USD 100 billion by 2034. This expansion is tied to rising consumption, improvements in mechanized manufacturing, and a transition to more intelligent production systems. Chinese producers are placing greater emphasis on sustainability, integrating more recycled cullet into production to cut costs and minimize environmental impact. Younger generations are shaping trends in custom and digital glassware, fostering demand for unique aesthetics and functional elegance.

Leading players in the market include Krosno Glass S.A., Libbey Inc., Arc Holdings, Bormioli Rocco, and Pasabahce under the Sisecam Group. Major companies in the pressed and blown glass market are prioritizing technological integration to enhance productivity and reduce errors. Robotic forming systems and AI-powered quality inspection tools are being widely deployed to improve consistency and cut production time. To meet the growing demand for sustainable solutions, many firms are shifting toward using recycled raw materials and adopting energy-efficient processes. Investments in digital design platforms allow these brands to quickly prototype and customize products, catering to both industrial clients and design-conscious consumers. Strategic partnerships with designers and retail distributors further enable companies to stay ahead in style and function.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics(Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 LATAM

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Tableware

- 5.2.1 Drinking glasses

- 5.2.1.1 Tumblers

- 5.2.1.2 Stemware

- 5.2.1.3 Mugs and cups

- 5.2.1.4 Shot glasses

- 5.2.1.5 Others

- 5.2.2 Dinnerware

- 5.2.2.1 Plates

- 5.2.2.2 Bowls

- 5.2.2.3 Serving dishes

- 5.2.2.4 Others

- 5.2.3 Serveware

- 5.2.3.1 Pitchers and decanters

- 5.2.3.2 Trays and platters

- 5.2.3.3 Others

- 5.2.1 Drinking glasses

- 5.3 Containers

- 5.3.1 Bottles

- 5.3.1.1 Beverage bottles

- 5.3.1.2 Pharmaceutical bottles

- 5.3.1.3 Cosmetic and perfume bottles

- 5.3.1.4 Others

- 5.3.2 Jars

- 5.3.2.1 Food jars

- 5.3.2.2 Cosmetic jars

- 5.3.2.3 Others

- 5.3.3 Vials and ampoules

- 5.3.4 Others

- 5.3.1 Bottles

- 5.4 Decorative glass

- 5.4.1 Figurines and sculptures

- 5.4.2 Vases and bowls

- 5.4.3 Ornaments

- 5.4.4 Others

- 5.5 Lighting products

- 5.5.1 Lamp shades

- 5.5.2 Chandeliers and pendants

- 5.5.3 Others

- 5.6 Technical and industrial glass

- 5.6.1 Laboratory glassware

- 5.6.2 Technical components

- 5.6.3 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Glass Type, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Soda-lime glass

- 6.3 Borosilicate glass

- 6.4 Crystal glass

- 6.4.1 Lead crystal

- 6.4.2 Lead-free crystal

- 6.5 Heat-resistant glass

- 6.6 Colored glass

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Press process

- 7.2.1 Single gob

- 7.2.2 Double gob

- 7.2.3 Triple gob

- 7.3 Blow process

- 7.3.1 Blow and blow

- 7.3.2 Press and blow

- 7.3.3 Narrow neck press and blow (NNPB)

- 7.4 Combined processes

- 7.5 Hand-crafted processes

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Food and beverage

- 8.2.1 Alcoholic beverages

- 8.2.2 Non-alcoholic beverages

- 8.2.3 Food packaging

- 8.2.4 Others

- 8.3 Pharmaceutical

- 8.3.1 Packaging

- 8.3.2 Laboratory equipment

- 8.3.3 Others

- 8.4 Cosmetics and personal care

- 8.4.1 Perfumes and fragrances

- 8.4.2 Skincare products

- 8.4.3 Others

- 8.5 Household and interior decor

- 8.5.1 Tableware

- 8.5.2 Decorative items

- 8.5.3 Lighting

- 8.5.4 Others

- 8.6 Hospitality and foodservice

- 8.6.1 Hotels and restaurants

- 8.6.2 Bars and pubs

- 8.6.3 Catering services

- 8.6.4 Others

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 B2b/direct sales

- 9.2.1 Manufacturers to retailers

- 9.2.2 Manufacturers to wholesalers

- 9.2.3 Manufacturers to end use

- 9.3 Retail

- 9.3.1 Hypermarkets/supermarkets

- 9.3.2 Specialty stores

- 9.3.3 Department stores

- 9.3.4 Others

- 9.4 Online retail

- 9.4.1 Company websites

- 9.4.2 E-commerce platforms

- 9.4.3 Others

- 9.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anchor Hocking LLC

- 11.2 Arc International

- 11.3 Ardagh Group S.A.

- 11.4 Beatson Clark Ltd.

- 11.5 Bormioli Rocco S.p.A.

- 11.6 Borosil Limited

- 11.7 Garbo Glassware Co., Ltd.

- 11.8 Gerresheimer AG

- 11.9 Glass Dynamics LLC

- 11.10 Kopp Glass, Inc.

- 11.11 Libbey Inc.

- 11.12 O-I Glass, Inc. (Owens-Illinois)

- 11.13 Piramal Glass Limited

- 11.14 Rayotek Scientific Inc.

- 11.15 Saverglass SAS

- 11.16 SCHOTT AG

- 11.17 Sisecam Group

- 11.18 Steelite International

- 11.19 Stoelzle Glass Group

- 11.20 Verallia

- 11.21 Vetropack Holding Ltd.

- 11.22 Vidrala S.A.

- 11.23 Vitro, S.A.B. de C.V.

- 11.24 Wiegand-Glas GmbH

- 11.25 Zwiesel Kristallglas AG