|

市場調查報告書

商品編碼

1773270

動態心電圖市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Holter ECG Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

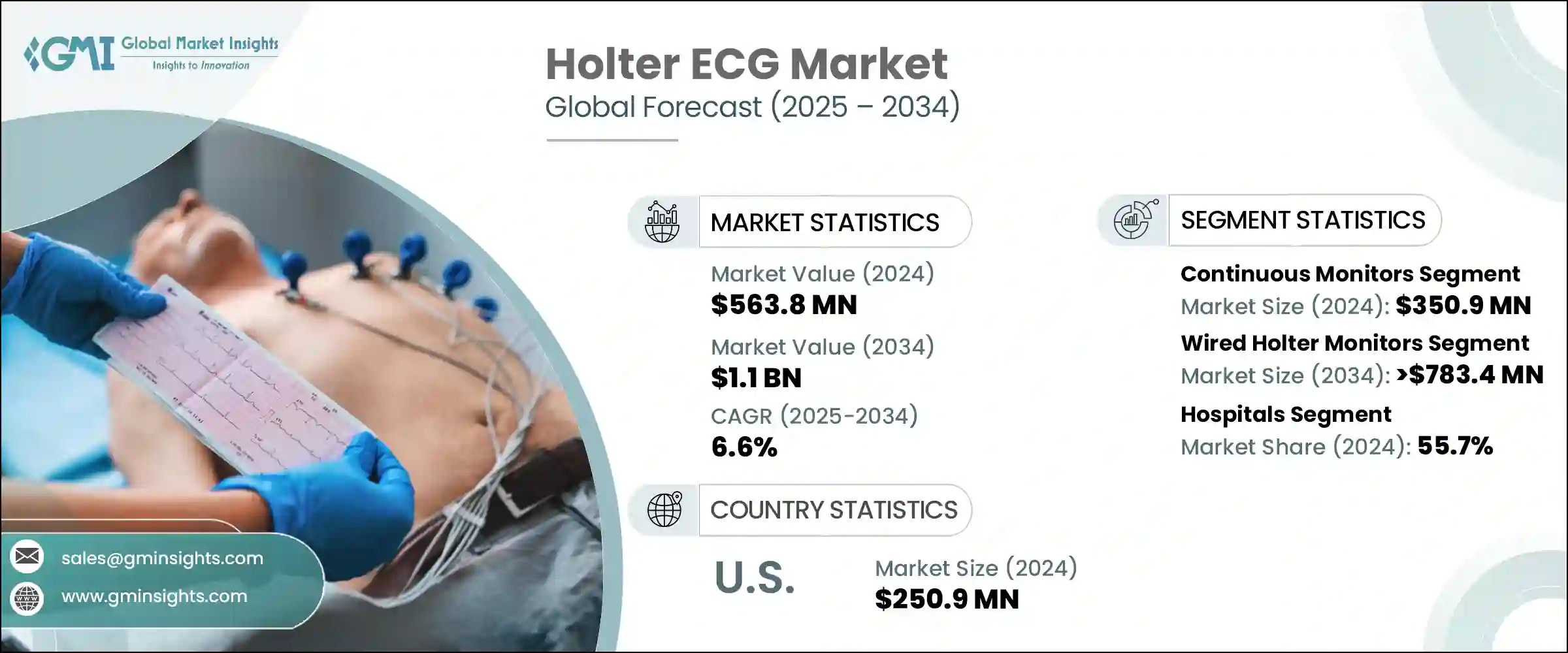

2024年,全球動態心電圖(Holter)市場規模達5.638億美元,預計到2034年將以6.6%的複合年成長率成長,達到11億美元。這一成長主要得益於心臟相關疾病發病率的上升、微創監測技術的日益普及以及遠端心臟診斷需求的不斷成長。全球心血管疾病確診人數的激增,持續推動先進診斷解決方案的需求。由於心臟病是全球死亡率的重要因素,早期精準診斷已成為醫療領域的關鍵重點。

由於動態心電圖 (Holter ECG) 設備有助於在醫院和家中識別心律不整,因此市場對此類設備的需求正在穩步成長。技術進步帶來了體積更小、方便用戶使用的設備,其電池壽命更長,並具備無線功能,從而提高了醫護人員和患者的可用性。這些技術升級使得間歇性心律不整的檢測變得更加容易,從而提高了其普及率。遠端患者監護趨勢以及更多穿戴式診斷設備的出現,為主動健康管理打開了新的大門。加之人們意識的提升和醫療保健支出的增加,這些因素持續加速了全球市場對動態心電圖設備的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 5.638億美元 |

| 預測值 | 11億美元 |

| 複合年成長率 | 6.6% |

動態心電圖 (Holter ECG) 是一種緊湊型穿戴式系統,可在特定時長追蹤心律。電極連接到胸部和腹部的特定部位,並與攜帶式監測器相連,持續捕捉心臟的電活動。隨著新技術重塑醫療保健服務,這些設備不僅在診所中得到更快的普及,也擴大應用於家庭心臟監測系統。感測器設計和微電子技術的進步帶來了隱形、可長時間佩戴的監測器,這些監測器可以隱藏在衣服下。這些特性顯著提高了患者的舒適度和依從性,這對於有效的心律評估至關重要。這些創新也能幫助醫生發現難以捕捉的心律不整,並更有效地進行治療。長效設備的吸引力在於它們能夠在提高易用性的同時保持高品質的資料,使其成為現代心臟護理的重要工具。

2024年,連續監測細分市場收入達3.509億美元,佔據動態心電圖(Holter ECG)市場的主導地位。連續動態心電圖設備能夠提供24至48小時甚至更長的不間斷資料,為醫師觀察心臟功能提供了更佳的窗口。其更長的記錄時間提高了識別偶發性心律不整的可能性,而這些異常在短期評估中往往被忽略。因此,醫療保健專業人員通常更傾向於使用它們進行全面的動態心臟評估。這些設備通常被認為是對心律不整進行初步評估的首選。由於連續監測器在專科心臟診所和普通內科的廣泛應用,它已成為行業標準,為整體市場發展做出了巨大貢獻。

預計到2034年,有線動態心電圖 (Holter) 監測領域的複合年成長率將達到6%,市場估值將達到7.834億美元。這些系統長期以來因其強大的性能和始終如一的資料準確性而備受心臟病學領域的信賴。其維護成本低,且與數位化醫院基礎設施相容,使其成為許多醫療機構的必備設備。這些設備可與心電圖軟體、PACS(醫學影像歸檔與通訊系統)和歸檔網路等患者資料系統無縫整合,從而簡化診斷工作流程。醫生信賴其久經考驗的可靠性,這最大限度地減少了資料缺口的可能性,並確保對心律問題進行更清晰的診斷。雖然新的無線方案正在湧現,但有線解決方案由於其可靠的輸出和易於整合到現有醫院IT環境中,仍然保持著強勁的市場需求。

2024年,美國動態心電圖 (Holter ECG) 市場規模達2.509億美元,預計2025年至2034年的複合年成長率將達到5.5%。老年人族群和慢性心臟病患者的應用尤其強勁。雲端平台和人工智慧 (AI) 增強型資料解讀工具徹底改變了遠端監測心臟狀況的方式。這些數位化增強功能有助於更好地管理患者資料並改善臨床療效。此外,優惠的報銷結構和本土公司不斷推出的創新產品,也促進了美國動態心電圖市場的成長。預防保健舉措,尤其是那些專注於心血管健康的舉措,正在進一步鞏固市場地位。

在 Holter 心電圖市場競爭的主要公司包括 GE HealthCare、SPACELABS HEALTHCARE、ScottCare、VIVALINK、PHILIPS、SCHILLER、iRHYTHM、FUKUDA、Bittium 和 Baxter。為了鞏固其在 Holter 心電圖產業的地位,主要參與者正在實施廣泛的產品創新、有針對性的收購和技術整合等策略。許多公司正在投資人工智慧心電圖解釋工具,以提高診斷準確性並支援遠端分析。公司還透過與醫療保健提供者建立策略夥伴關係和合作來擴大其地理覆蓋範圍。產品組合正在多樣化,包括長時間和無線穿戴式監視器,旨在滿足消費者對舒適性和可用性日益成長的期望。此外,製造商正在努力簡化與醫院 IT 生態系統的兼容性,確保無縫的資料共享和解釋。這些方法正在幫助品牌保持競爭力並在這個快速發展的市場中佔據更大的佔有率。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 心臟病盛行率不斷上升

- 技術進步

- 微創設備的採用日益增多

- 遠端心臟監測需求激增

- 產業陷阱與挑戰

- 嚴格的監理政策

- 動態心電圖成本高

- 市場機會

- 遠距病人監護 (RPM) 和遠距心臟病學的擴展

- 成長動力

- 成長潛力分析

- 監管格局

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 定價分析

- 差距分析

- 波特的分析

- 報銷場景

- PESTEL分析

- 價值鏈分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 按地區

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:依產品類型,2021 - 2034 年

- 主要趨勢

- 連續監測

- 間歇性監測器

第6章:市場估計與預測:按方式,2021 - 2034 年

- 主要趨勢

- 有線動態心電圖監測儀

- 3導程動態心電圖監測儀

- 12導程動態心電圖監測儀

- 其他有線動態心電圖監測儀

- 無線動態心電圖監測儀

第7章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 醫院

- 門診手術中心

- 其他最終用途

第8章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第9章:公司簡介

- Baxter

- Bittium

- FUKUDA

- GE HealthCare

- iRHYTHM

- PHILIPS

- SCHILLER

- ScottCare

- SPACELABS HEALTHCARE

- VIVALINK

The Global Holter ECG Market was valued at USD 563.8 million in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 1.1 billion by 2034. This growth is largely fueled by the rising incidence of heart-related conditions, the increasing acceptance of less invasive monitoring technologies, and the growing demand for remote cardiac diagnostics. The surging number of individuals diagnosed with cardiovascular diseases worldwide continues to drive the need for sophisticated diagnostic solutions. With heart ailments contributing significantly to global mortality rates, early and accurate diagnosis has become a critical medical priority.

Demand for Holter ECGs is rising steadily as these devices help identify cardiac irregularities in both hospital and at-home settings. Technological progress has led to smaller, user-friendly devices with improved battery life and wireless features, enhancing usability for both healthcare providers and patients. These technological upgrades have made it easier to detect intermittent arrhythmia, increasing adoption. Remote patient monitoring trends and the availability of more wearable diagnostic devices have opened new doors for proactive health management. Combined with broader awareness and healthcare spending, these factors continue to accelerate the demand for Holter ECG devices across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $563.8 Million |

| Forecast Value | $1.1 Billion |

| CAGR | 6.6% |

Holter ECGs are compact wearable systems that track heart rhythms for a defined duration. Electrodes are attached to specific parts of the chest and abdomen, linked to a portable monitor that continuously captures the heart's electrical activity. As newer technologies reshape healthcare delivery, these devices are seeing faster adoption not just in clinics but also in home-based cardiac monitoring setups. Advances in sensor design and microelectronics have led to discreet, long-wear monitors that remain hidden under clothing. These features significantly increase patient comfort and compliance, which are essential for effective cardiac rhythm assessment. These innovations also support physicians in detecting hard-to-catch arrhythmias and managing treatment more effectively. The appeal of extended-use devices lies in their ability to maintain high data quality while improving ease of use, making them an essential tool in modern cardiac care.

In 2024, the continuous monitoring segment brought in USD 350.9 million, dominating the Holter ECG landscape. Continuous Holter ECG devices deliver uninterrupted data for 24 to 48 hours or even longer, giving doctors an enhanced window to observe heart function. Their extended recording duration increases the likelihood of identifying sporadic rhythm disorders that would often go unnoticed in shorter evaluations. As a result, healthcare professionals often prefer them for thorough ambulatory cardiac assessment. These devices are often considered the primary option for initial evaluations of irregular heartbeat conditions. Due to their consistent use across both specialized cardiac practices and general medicine, continuous monitors have become an industry standard, contributing substantially to overall market development.

The wired Holter monitors segment is anticipated to witness a CAGR of 6% through 2034, reaching a market valuation of USD 783.4 million. These systems have long been trusted in cardiology for their robust performance and consistent data accuracy. Their low maintenance requirements and compatibility with digital hospital infrastructure make them a staple in many healthcare settings. These devices seamlessly integrate with patient data systems like ECG software, PACS, and archiving networks, which streamlines diagnostic workflows. Physicians rely on their proven reliability, which minimizes the chance of data gaps and ensures a clearer diagnosis of heart rhythm issues. While newer wireless options are emerging, wired solutions still retain strong market demand due to their dependable output and ease of integration into current hospital IT environments.

United States Holter ECG Market was worth USD 250.9 million in 2024 and is set to grow at a CAGR of 5.5% from 2025 to 2034. Adoption is especially robust among elderly populations and individuals living with chronic heart disease. Cloud-based platforms and AI-enhanced data interpretation tools have revolutionized the way cardiac conditions are monitored remotely. These digital enhancements allow for better management of patient data and improved clinical outcomes. Additionally, favorable reimbursement structures and the continuous launch of innovative products by local companies are contributing to the growth of Holter ECGs in the country. Preventive care initiatives, particularly those focusing on cardiovascular wellness, are further strengthening the market's position.

Major companies competing in the Holter ECG Market include GE HealthCare, SPACELABS HEALTHCARE, ScottCare, VIVALINK, PHILIPS, SCHILLER, iRHYTHM, FUKUDA, Bittium, and Baxter. To reinforce their position in the Holter ECG industry, key players are implementing strategies such as extensive product innovation, targeted acquisitions, and technology integration. Many are investing in AI-powered ECG interpretation tools to enhance diagnostic accuracy and support remote analysis. Companies are also expanding their geographic reach through strategic partnerships and collaborations with healthcare providers. Product portfolios are being diversified to include long-duration and wireless wearable monitors, tailored to meet rising consumer expectations for comfort and usability. Additionally, manufacturers are working to streamline compatibility with hospital IT ecosystems, ensuring seamless data sharing and interpretation. These approaches are helping brands to stay competitive and capture a larger share of this rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Modality

- 2.2.4 End use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of cardiac diseases

- 3.2.1.2 Technological advancements

- 3.2.1.3 Growing adoption of minimally invasive devices

- 3.2.1.4 Surging preference for remote patient cardiac monitoring

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory policies

- 3.2.2.2 High cost of the Holter ECG

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of remote patient monitoring (RPM) and telecardiology

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 Reimbursement scenario

- 3.10 PESTEL analysis

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Continuous monitors

- 5.3 Intermittent monitors

Chapter 6 Market Estimates and Forecast, By Modality, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Wired Holter monitors

- 6.2.1 3 lead Holter monitors

- 6.2.2 12 lead Holter monitors

- 6.2.3 Other wired Holter monitors

- 6.3 Wireless Holter monitors

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Baxter

- 9.2 Bittium

- 9.3 FUKUDA

- 9.4 GE HealthCare

- 9.5 iRHYTHM

- 9.6 PHILIPS

- 9.7 SCHILLER

- 9.8 ScottCare

- 9.9 SPACELABS HEALTHCARE

- 9.10 VIVALINK