|

市場調查報告書

商品編碼

1773268

中功率電動車母線市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Medium Power Electric Vehicle Busbar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

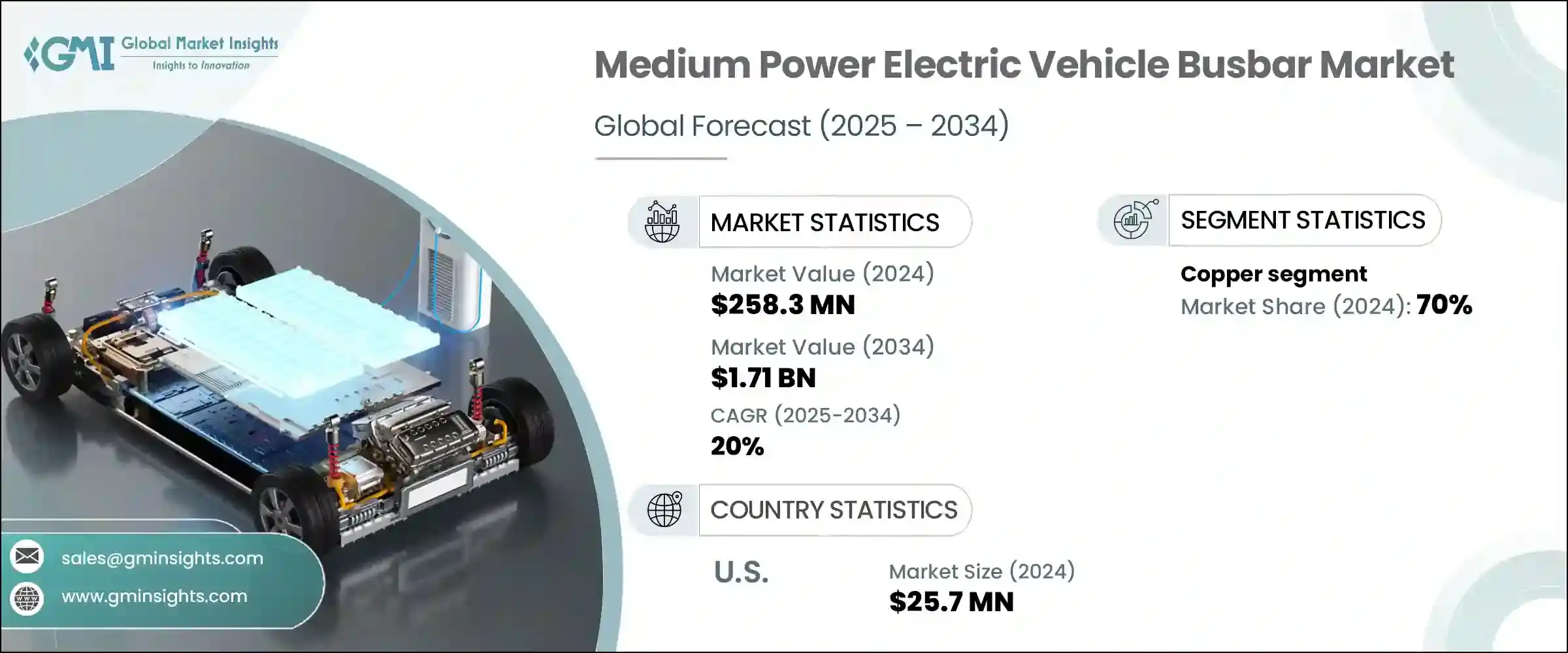

2024年,全球中功率電動車母線市場規模達2.583億美元,預計2034年將以20%的複合年成長率成長,達到17.1億美元。這一強勁的成長勢頭得益於電動車投資的不斷成長、有利的監管環境以及配電技術的顯著進步。隨著電動車持續獲得主流關注,策略合作、材料科學創新以及不斷發展的生產技術正在重塑電動車內部的能量傳輸方式。市場發展勢頭與向輕量化、高效系統的轉變日益緊密相關,該系統旨在最佳化車輛續航里程和性能。

材料革新是市場的關鍵驅動力。雖然銅憑藉其無與倫比的導電性仍然佔據主導地位,但它也顯著增加了車輛重量,促使製造商探索替代材料。如今,鋁等更輕的材質正被整合,以降低成本並提高能源效率。採用先進複合材料的客製化工程解決方案因其卓越的熱控制性能和機械耐久性而日益普及,並可在各種電動車應用中提升性能。此外,客製化的母線系統正在幫助製造商最大限度地減少材料浪費並最佳化車輛架構。智慧技術整合、新一代生產線以及不斷發展的原始設備製造OEM)規範的融合,為整個價值鏈的市場拓展和創新打開了新的大門。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 2.583億美元 |

| 預測值 | 17.1億美元 |

| 複合年成長率 | 20% |

截至2024年,銅憑藉其卓越的導電性和熱管理性能,在中功率電動車母線市場佔據了70%的佔有率。銅能夠最大限度地降低能量損失,這對於提升電動車電池性能、確保更長的續航里程和維護系統完整性至關重要。這些特性對於努力平衡車輛效率、安全性和電力傳輸的汽車製造商來說仍然至關重要。

美國中功率電動車母線市場規模預計2024年達到2,570萬美元。聯邦政府和各州政府推出的加速電動車普及的政策,加上對先進電網基礎設施日益成長的需求,正在推動製造商擴大規模。中功率母線對於最佳化電動車配電網路、確保充電效率和負載平衡至關重要。隨著電動車產量的擴大,對可靠、緊湊且熱效率高的母線系統的需求也迅速成長。

全球中功率電動車母線市場的主要公司包括安費諾公司、英飛凌科技股份公司、Brar Elettromeccanica SpA、Littelfuse公司、Mersen SA、西門子、EMS集團、羅格朗、羅傑斯公司、三菱電機株式會社、泰科電子、施耐德電氣、EAE集團、EG Electronics和魏德米勒介面有限公司。該領域的領導企業正透過材料創新、設計最佳化和全球製造擴張等方式擴大其市場佔有率。許多公司正優先開發輕量化、高性能合金和複合材料,以滿足下一代電動車不斷發展的能源效率標準。與汽車製造商和電池製造商建立的策略合資企業有助於確保長期供應協議。各公司也正在增加對自動化和精密工具的投資,以實現複雜、車輛專用母線組件的可擴展且經濟高效的生產。同時,他們正在加強對散熱、智慧診斷和系統整合的研發力度,以提供滿足汽車製造OEM需求的增值解決方案。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 戰略儀表板

- 策略舉措

- 競爭基準測試

- 創新與技術格局

第5章:市場規模及預測:依資料,2021 - 2034 年

- 主要趨勢

- 銅

- 鋁

第6章:市場規模及預測:依地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 挪威

- 德國

- 法國

- 荷蘭

- 英國

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第7章:公司簡介

- Amphenol Corporation

- Brar Elettromeccanica SpA

- EAE Group

- EG Electronics

- EMS Group

- Infineon Technologies AG

- Legrand

- Littelfuse, Inc.

- Mersen SA

- Mitsubishi Electric Corporation

- Rogers Corporation

- Schneider Electric

- Siemens

- TE Connectivity

- Weidmuller Interface GmbH & Co. KG

The Global Medium Power Electric Vehicle Busbar Market was valued at USD 258.3 million in 2024 and is estimated to grow at a CAGR of 20% to reach USD 1.71 billion by 2034. This impressive growth trajectory is being fueled by rising investments in electric mobility, favorable regulatory landscapes, and significant advancements in power distribution technologies. As electric vehicles continue gaining mainstream traction, strategic collaborations, innovations in material sciences, and evolving production technologies are reshaping how energy is routed within these vehicles. Market momentum is increasingly tied to the shift toward lightweight, high-efficiency systems tailored to optimize vehicle range and performance.

Material evolution is a key market driver. While copper remains dominant due to its unmatched electrical conductivity, it adds considerable weight-leading manufacturers to explore alternative materials. Lighter options like aluminum are now being integrated to reduce cost and improve energy efficiency. Custom-engineered solutions using advanced composites are gaining popularity for their superior thermal control and mechanical durability, offering a performance boost across various EV applications. Additionally, tailored busbar systems are helping manufacturers minimize material waste and optimize vehicle architecture. The convergence of smart technology integration, next-gen production lines, and evolving OEM specifications is opening new doors for market expansion and innovation across the value chain.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $258.3 Million |

| Forecast Value | $1.71 Billion |

| CAGR | 20% |

As of 2024, the copper segment in the medium-power electric vehicle busbar market held a 70% share due to its superior conductivity and thermal management. Its ability to minimize energy loss makes it vital for enhancing EV battery performance, ensuring better range, and maintaining system integrity. These characteristics remain critical for automakers striving to balance vehicle efficiency, safety, and power delivery.

United States Medium Power Electric Vehicle Busbar Market USD 25.7 million in 2024. Federal and state-led policies to accelerate EV adoption, coupled with rising demand for advanced grid infrastructure, are pushing manufacturers to scale up. Medium power busbars are essential in optimizing EV power distribution networks, ensuring both charging efficiency and load balancing. As EV production scales, the demand for reliable, compact, and heat-efficient busbar systems is increasing rapidly.

Key companies in the Global Medium Power Electric Vehicle Busbar Market include Amphenol Corporation, Infineon Technologies AG, Brar Elettromeccanica SpA, Littelfuse, Inc., Mersen SA, Siemens, EMS Group, Legrand, Rogers Corporation, Mitsubishi Electric Corporation, TE Connectivity, Schneider Electric, EAE Group, EG Electronics, and Weidmuller Interface GmbH & Co. KG. Leading players in this space are advancing their market footprint through a combination of material innovation, design optimization, and global manufacturing expansion. Many are prioritizing the development of lightweight, high-performance alloys and composites to meet the evolving efficiency standards of next-generation EVs. Strategic joint ventures with automakers and battery manufacturers are helping secure long-term supply agreements. Companies are also boosting investments in automation and precision tooling to enable scalable, cost-effective production of complex, vehicle-specific busbar assemblies. In parallel, they are expanding R&D efforts focused on heat dissipation, smart diagnostics, and system integration to deliver value-added solutions tailored to OEM requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Material, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Copper

- 5.3 Aluminum

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 Norway

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Netherlands

- 6.3.5 UK

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Argentina

Chapter 7 Company Profiles

- 7.1 Amphenol Corporation

- 7.2 Brar Elettromeccanica SpA

- 7.3 EAE Group

- 7.4 EG Electronics

- 7.5 EMS Group

- 7.6 Infineon Technologies AG

- 7.7 Legrand

- 7.8 Littelfuse, Inc.

- 7.9 Mersen SA

- 7.10 Mitsubishi Electric Corporation

- 7.11 Rogers Corporation

- 7.12 Schneider Electric

- 7.13 Siemens

- 7.14 TE Connectivity

- 7.15 Weidmuller Interface GmbH & Co. KG

汽車匯流排全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

汽車匯流排全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 按車輛類型、材質、額定電流、製造程序和應用分類的電動汽車匯流排- 全球市場預測 2026-2032

按車輛類型、材質、額定電流、製造程序和應用分類的電動汽車匯流排- 全球市場預測 2026-2032 全球中功率電動車匯流排市場全球高功率電動車匯流排市場全球電動車匯流排市場

全球中功率電動車匯流排市場全球高功率電動車匯流排市場全球電動車匯流排市場 汽車母線市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、類型、材料、地區和競爭細分,2020-2030 年

汽車母線市場-全球產業規模、佔有率、趨勢、機會和預測,按應用、類型、材料、地區和競爭細分,2020-2030 年 高功率電動車母線市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測電動車母線市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測

高功率電動車母線市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測電動車母線市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測 EV母線的全球市場:市場佔有率與排行榜,整體銷售額與需求預測(2024年~2030年)

EV母線的全球市場:市場佔有率與排行榜,整體銷售額與需求預測(2024年~2030年)