|

市場調查報告書

商品編碼

1773245

動物診斷市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Animal Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

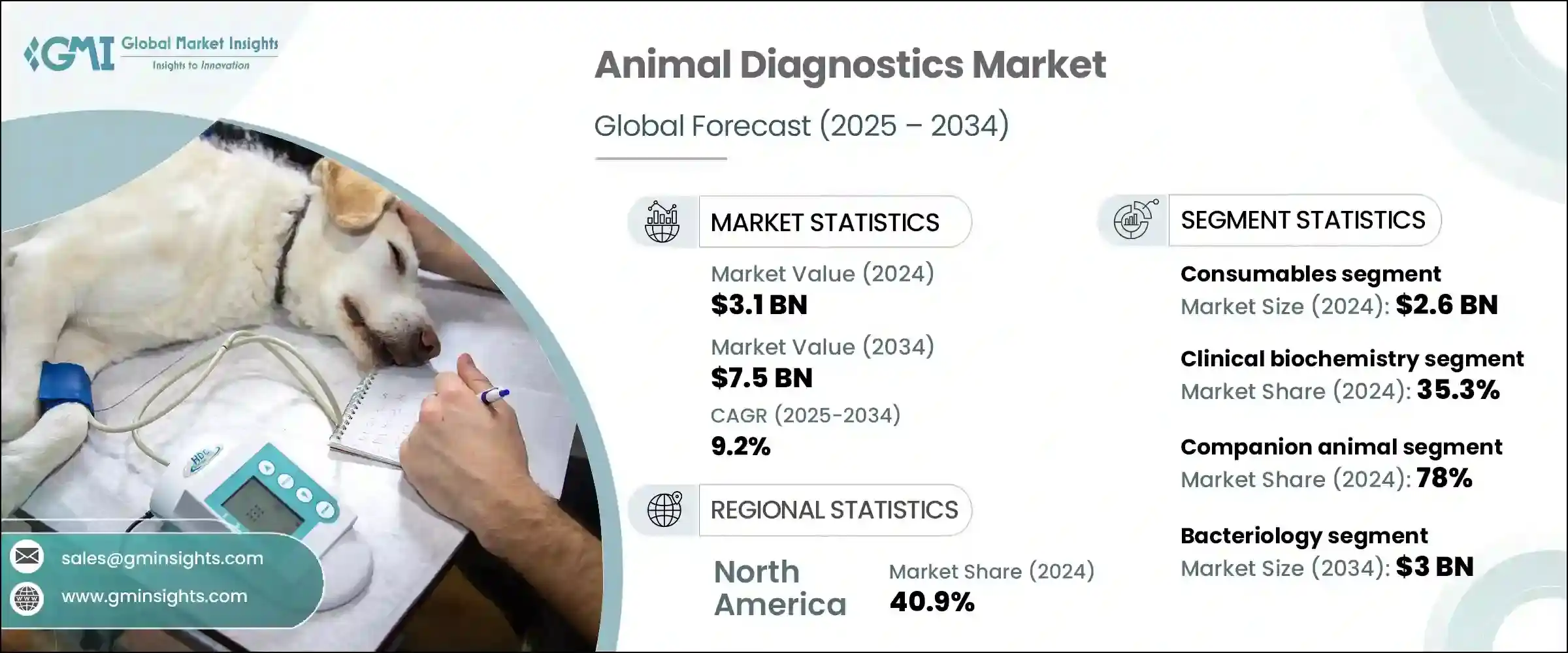

2024年,全球動物診斷市場規模達31億美元,預計2034年將以9.2%的複合年成長率成長,達到75億美元。這一成長主要源於伴侶動物和農場動物中傳染病和慢性病發病率的上升。隨著動物健康日益成為個別飼養者和農業部門的焦點,對可靠診斷解決方案的需求也持續成長。

公共和私營部門對動物衛生基礎設施的投資,加上政府對疾病預防和管理的支持性政策,正在促進整個獸醫領域對診斷技術的認知和應用。獸醫診所和診斷實驗室之間的合作,以及主要機構在服務不足地區擴大服務覆蓋範圍,正在顯著改善發展中國家獲得檢測服務的可近性。此外,寵物保險的日益普及減輕了寵物主人頻繁診斷的經濟負擔,從而鼓勵定期檢測和早期疾病發現。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 31億美元 |

| 預測值 | 75億美元 |

| 複合年成長率 | 9.2% |

動物診斷涉及一系列用於檢測和監測動物疾病或其他健康狀況的檢測方法。這些技術包括分子診斷、血清學檢測、尿液分析和臨床生物化學等。依產品類型,市場分為儀器和耗材兩大類。其中,耗材佔最大佔有率,2024 年價值 26 億美元。此細分市場的主導地位源自於診斷試劑盒、試劑、玻片和採集管等物品的高使用頻率和重複性需求。這些產品是獸醫診所和實驗室日常運作不可或缺的一部分,有助於維持其持續的需求並佔據整體市場領先地位。

從技術面來看,臨床生物化學領域在2024年引領全球動物診斷市場,佔35.3%的佔有率。該領域憑藉其透過血液、尿液和其他體液評估重要生理指標的能力,持續獲得發展,從而能夠早期發現動物的肝腎疾病、代謝性疾病和激素失衡等疾病。隨著人們對寵物預防保健意識的不斷增強,對常規健康篩檢(通常包含生物化學檢測)的需求激增。寵物慢性病病例的增加也推動了臨床化學工具在獸醫領域的應用。

從應用角度來看,市場細分為細菌學、病理學、寄生蟲學和其他診斷應用。細菌學領域佔據了相當大的市場佔有率,預計到2034年將達到30億美元。該領域對於識別導致多種動物疾病的細菌病原體仍然至關重要。細菌學檢測使獸醫能夠準確診斷感染並及時實施治療方案。檢測方法的創新以及對人畜共患疾病控制和食品安全標準提高的日益重視,正推動該領域繼續佔據主導地位。

依動物類型細分,伴侶動物類別在2024年佔據78%的市場佔有率,佔據市場主導地位。這包括針對狗、貓、馬和其他家養動物的診斷服務。寵物擁有量的激增,尤其是在城市地區,導致了對獸醫服務(包括診斷)的需求增加。此外,隨著寵物健康意識的增強以及動物癌症和糖尿病等疾病發生率的上升,寵物主人也開始尋求定期的健康檢查和診斷支持。

依最終用途分類,診斷實驗室在2024年成為領先細分市場,預計2025年至2034年的複合年成長率將達到9.3%。這些實驗室提供全面的檢測服務,配備先進的設備和熟練的技術人員,能夠精確處理大量樣本。它們能夠進行即時PCR和基因定序等高級檢測,成為尋求精準結果的獸醫的首選。對集中式高通量檢測的需求日益成長,使這些設施繼續佔據市場前沿。

從區域來看,北美在2024年繼續保持其最大市場的地位,佔據全球40.9%的佔有率。該地區受益於廣泛的寵物飼養、先進的獸醫保健基礎設施以及日益增強的預防性動物護理意識。光是在美國,動物診斷市場在2024年就達到了11.4億美元,並呈現持續的逐年成長。寵物保險普及率的提高以及動物保健支出的增加是該地區領先地位的支撐因素之一。

全球動物診斷市場的競爭格局由主要參與者主導,他們控制約65%至70%的市場佔有率。這些公司利用其廣泛的產品組合和國際影響力,保持穩固的市場地位。在這個快速發展的市場中,收購、新產品發布和設施擴建等策略性舉措是推動成長和提陞技術能力的常用策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 收養寵物的趨勢日益成長

- 食源性疾病和人畜共通傳染病的發生率不斷上升

- 有利的政府舉措

- 伴隨診斷的進展

- 寵物保險的普及率不斷提高

- 產業陷阱與挑戰

- 動物試驗成本過高

- 獸醫護理自付費用低

- 市場機會

- 技術進步和即時診斷分子工具

- 畜牧業的擴張和對食品安全的需求

- 成長動力

- 成長潛力分析

- 定價分析

- 監管格局

- 技術格局

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與協作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按產品,2021 - 2034 年

- 主要趨勢

- 耗材

- 儀器

第6章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 臨床生物化學

- 血糖監測

- 血氣和電解質分析

- 其他臨床生化檢查

- 免疫診斷

- 橫向流動試驗

- 酵素連結免疫吸附試驗

- 免疫分析儀

- 其他免疫診斷測試

- 分子診斷

- 聚合酶連鎖反應

- 微陣列

- 其他分子診斷測試

- 血液學

- 尿液分析

- 其他技術

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 細菌學

- 病理

- 寄生蟲學

- 其他應用

第8章:市場估計與預測:按動物類型,2021 - 2034 年

- 主要趨勢

- 伴侶動物

- 狗

- 貓

- 馬匹

- 其他伴侶動物

- 農場動物

- 牛

- 豬

- 家禽

- 其他農場動物

第9章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 獸醫醫院和診所

- 診斷實驗室

- 居家照護環境

- 其他最終用途

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 波蘭

- 荷蘭

- 瑞典

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 菲律賓

- 泰國

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 秘魯

- 智利

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 埃及

- 以色列

第 11 章:公司簡介

- bioMerieux

- BioNote

- Bio-Rad Laboratories

- Boehringer Ingelheim International

- Heska Corporation

- Idexx laboratories

- KogeneBiotech

- Median Diagnostics

- Neogen Corporation

- Randox

- Thermo Fischer Scientific

- Virbac

- VetAll Laboratories

- Qiagen

- Zoetis

The Global Animal Diagnostics Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 7.5 billion by 2034. This growth is primarily driven by the rising prevalence of both infectious and chronic diseases in companion and farm animals. As animal health becomes a growing concern for both individual owners and the agricultural sector, the demand for reliable diagnostic solutions continues to increase.

Public and private investments in animal health infrastructure, coupled with supportive government policies targeting disease prevention and management, are fostering greater awareness and adoption of diagnostics across the veterinary landscape. Collaborations between veterinary clinics and diagnostic labs, as well as expanded outreach by major players in underserved regions, are significantly improving access to testing services in developing countries. Moreover, the growing popularity of pet insurance is easing the financial burden of frequent diagnostics for pet owners, thereby encouraging regular testing and early disease detection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 9.2% |

Animal diagnostics involves a range of testing methods used to detect and monitor diseases or other health conditions in animals. These techniques include molecular diagnostics, serological testing, urinalysis, and clinical biochemistry, among others. Based on product type, the market is divided into instruments and consumables. Among these, the consumables segment held the largest share, valued at USD 2.6 billion in 2024. The dominance of this segment is due to the high usage frequency and recurring need for items such as diagnostic kits, reagents, slides, and collection tubes. These products are integral to daily operations in veterinary clinics and labs, contributing to their consistent demand and overall market leadership.

By technology, the clinical biochemistry segment led the global animal diagnostics market in 2024 with a 35.3% share. This segment continues to gain traction due to its ability to assess vital physiological markers through blood, urine, and other bodily fluids, allowing for the early detection of conditions such as liver and kidney disorders, metabolic diseases, and hormonal imbalances in animals. As awareness about preventive care in pets grows, the demand for routine health screenings, which often include biochemistry panels, has surged. The increasing cases of chronic conditions in pets have also played a key role in boosting the use of clinical chemistry tools in veterinary settings.

In terms of application, the market is segmented into bacteriology, pathology, parasitology, and other diagnostic applications. The bacteriology segment accounted for a significant portion of the market and is projected to reach USD 3 billion by 2034. This segment remains crucial for identifying bacterial pathogens that are responsible for a wide range of animal diseases. Bacteriological testing enables veterinarians to diagnose infections accurately and implement timely treatment protocols. Innovations in testing methodologies and the growing emphasis on controlling zoonotic diseases and improving food safety standards are contributing to the segment's continued dominance.

When segmented by animal type, the companion animals category led the market with a substantial 78% share in 2024. This includes diagnostics for dogs, cats, horses, and other household animals. The surge in pet ownership, especially in urban areas, has led to higher demand for veterinary services, including diagnostics. Furthermore, rising awareness about pet health and the increasing incidence of diseases like cancer and diabetes in animals are pushing pet owners to seek regular health checkups and diagnostic support.

By end use, diagnostic laboratories emerged as the leading segment in 2024 and are projected to grow at a CAGR of 9.3% from 2025 to 2034. These labs offer comprehensive testing services, supported by sophisticated equipment and skilled technicians capable of processing large sample volumes with precision. Their ability to perform advanced testing, such as real-time PCR and genetic sequencing, has made them the preferred choice for veterinarians seeking accurate results. Growing demand for centralized, high-throughput testing continues to position these facilities at the forefront of the market.

Regionally, North America maintained its position as the largest market in 2024, commanding 40.9% of the global share. The region benefits from widespread pet ownership, advanced veterinary healthcare infrastructure, and growing awareness of preventive animal care. The animal diagnostics market in the United States alone reached USD 1.14 billion in 2024, showing consistent year-over-year growth. Increased adoption of pet insurance and high spending on animal health are among the factors supporting this regional leadership.

The competitive landscape of the global animal diagnostics market is dominated by key players that control around 65% to 70% of the industry. These companies leverage their expansive product portfolios and international presence to maintain a strong foothold. Strategic initiatives, including acquisitions, new product launches, and facility expansions, are common tactics used to drive growth and enhance technological capabilities in this rapidly evolving market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 Animal type

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing trend of adopting pet animals

- 3.2.1.2 Rising prevalence of foodborne and zoonotic diseases

- 3.2.1.3 Favorable government initiatives

- 3.2.1.4 Advancements in companion diagnostics

- 3.2.1.5 Increasing adoption of pet insurance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Prohibitive cost associated with animal tests

- 3.2.2.2 Low out of pocket expenditure on veterinary care

- 3.2.3 Market opportunities

- 3.2.3.1 Technological advancements and point-of-care molecular tools

- 3.2.3.2 Expanding livestock industry and demand for food safety

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pricing analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical biochemistry

- 6.2.1 Glucose monitoring

- 6.2.2 Blood gas and electrolyte analysis

- 6.2.3 Other clinical biochemistry tests

- 6.3 Immunodiagnostics

- 6.3.1 Lateral flow assays

- 6.3.2 ELISA

- 6.3.3 Immunoassay analyzers

- 6.3.4 Other immunodiagnostic tests

- 6.4 Molecular diagnostics

- 6.4.1 PCR

- 6.4.2 Microarrays

- 6.4.3 Other molecular diagnostic tests

- 6.5 Hematology

- 6.6 Urinalysis

- 6.7 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Bacteriology

- 7.3 Pathology

- 7.4 Parasitology

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Companion animals

- 8.2.1 Dogs

- 8.2.2 Cats

- 8.2.3 Horses

- 8.2.4 Other companion animals

- 8.3 Farm animals

- 8.3.1 Cattle

- 8.3.2 Swine

- 8.3.3 Poultry

- 8.3.4 Other farm animals

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals and clinics

- 9.3 Diagnostic labs

- 9.4 Home care settings

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Columbia

- 10.5.5 Peru

- 10.5.6 Chile

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

- 10.6.5 Egypt

- 10.6.6 Israel

Chapter 11 Company Profiles

- 11.1 bioMerieux

- 11.2 BioNote

- 11.3 Bio-Rad Laboratories

- 11.4 Boehringer Ingelheim International

- 11.5 Heska Corporation

- 11.6 Idexx laboratories

- 11.7 KogeneBiotech

- 11.8 Median Diagnostics

- 11.9 Neogen Corporation

- 11.10 Randox

- 11.11 Thermo Fischer Scientific

- 11.12 Virbac

- 11.13 VetAll Laboratories

- 11.14 Qiagen

- 11.15 Zoetis

獸醫診斷市場按產品類型、動物類型、檢測類型、樣本類型、技術、疾病類型和最終用戶分類 - 全球預測 2025-2030

獸醫診斷市場按產品類型、動物類型、檢測類型、樣本類型、技術、疾病類型和最終用戶分類 - 全球預測 2025-2030 全球馬匹診斷服務市場

全球馬匹診斷服務市場 2025年全球動物治療與診斷市場報告2025年全球牲畜保健市場報告2025年全球獸醫診斷設備市場報告

2025年全球動物治療與診斷市場報告2025年全球牲畜保健市場報告2025年全球獸醫診斷設備市場報告 獸醫診斷市場(按產品、技術、動物類型、應用和地區分類)- 預測至 2030 年

獸醫診斷市場(按產品、技術、動物類型、應用和地區分類)- 預測至 2030 年 2025 年至 2033 年獸醫診斷市場報告(按產品、技術、動物類型、疾病類型、最終用戶和地區)

2025 年至 2033 年獸醫診斷市場報告(按產品、技術、動物類型、疾病類型、最終用戶和地區) 寵物用血壓監測設備的全球市場:動物類別,各產品,檢測類別,各種模式,各技術,各終端用戶,各地區,機會,預測,2018年~2032年全球寵物血壓計市場

寵物用血壓監測設備的全球市場:動物類別,各產品,檢測類別,各種模式,各技術,各終端用戶,各地區,機會,預測,2018年~2032年全球寵物血壓計市場 動物治療和診斷市場,按產品類型、動物類型、最終用戶、國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

動物治療和診斷市場,按產品類型、動物類型、最終用戶、國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測