|

市場調查報告書

商品編碼

1766369

癲癇治療藥物市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Epilepsy Treatment Drugs Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

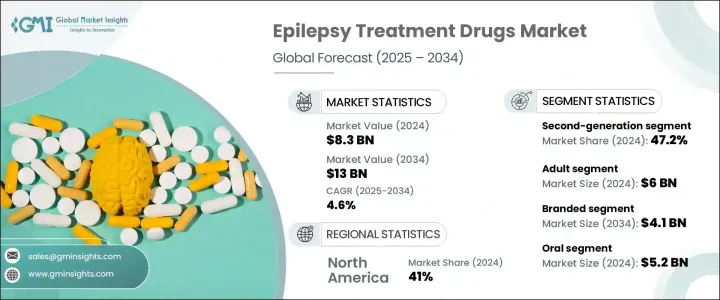

2024年,全球癲癇治療藥物市場規模達83億美元,預計到2034年將以4.6%的複合年成長率成長,達到130億美元。全球癲癇診斷數量的穩定成長是推動人們對更有效、更便捷治療方案需求的關鍵因素之一。藥物創新、副作用較少的新一代抗癲癇藥物的研發以及治療順從性的提高,都支撐著這一上升趨勢。政府和私人部門對神經病學相關研究的投入不斷增加,以及認知度和篩檢率的提高,都促進了市場的擴張。

全球老齡人口的不斷成長——更容易患上神經系統疾病——預計也將進一步提升對癲癇藥物的需求。藥物開發商正在優先考慮耐受性更好、緩釋性更強、患者依從性更高的療法。這種轉變,加上發展中國家醫療基礎設施的改善以及主要市場監管途徑的簡化,正在為創新和產品應用創造有利的環境。此外,朝向更個人化的醫療策略(尤其是針對抗藥性癲癇)的轉變,正在改善治療效果,並推動市場的長期成長。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 83億美元 |

| 預測值 | 130億美元 |

| 複合年成長率 | 4.6% |

抗癲癇藥物 (AED),也稱為抗驚厥藥,透過穩定大腦中不規則的電訊號發揮作用,有助於預防癲癇發作並控制癲癇的整體症狀。根據藥物類別,市場分為第一代、第二代和第三代藥物。 2024 年,第二代 AED 佔據最大收入佔有率,為全球市場貢獻了 47.2%。預計該細分市場在 2025 年至 2034 年期間的複合年成長率將達到 4.6%。與老一代療法相比,第二代 AED 被更廣泛地接受,這歸因於其藥物交互作用發生率更低、副作用更少以及患者依從性更高。

就產品類型而言,市場分為品牌藥和學名藥。 2024年,品牌藥的銷售額為26億美元,預計到2034年將達到41億美元。製藥公司越來越注重生產具有更優藥物動力學、更少不良反應和更大療效的品牌藥物。對新型療法的需求日益成長,尤其是在對傳統療法無反應的患者群體中,這也推動了對品牌抗癲癇藥物的需求。

依給藥途徑分析,口服製劑在2024年佔最大佔有率,達52億美元。預計該細分市場在預測期內的複合年成長率將達到4.9%。口服藥物因其便捷易用以及緩釋劑型的推出而受到青睞,緩釋劑型可以改善給藥方案並提高患者依從性。多樣化口服製劑的出現也加速了其在已開發市場和新興市場的普及。

根據患者人口統計數據,市場細分為成人和兒童族群。成人群體佔據主導地位,2024 年市場價值達 60 億美元,預計到 2034 年將以 4.5% 的複合年成長率成長。成人癲癇發生率的上升與中風、腦損傷和退化性疾病等與年齡相關的神經系統疾病有關。因此,對可靠且有針對性的治療方法的需求日益成長,多重藥物聯合治療方案和長期治療也越來越受到重視,以改善癲癇發作的控制。

根據癲癇發作類型,市場細分為局部癲癇、全身性癲癇和混合性癲癇。全身性癲癇發作市場在2024年創收25億美元,預計2034年將達到40億美元。全身性癲癇病例(包括強直陣攣性癲癇和失神性癲癇)的不斷增加,促使人們需要更有效的治療方案。政府加強對神經病學研究的投入、擴大保險覆蓋範圍以及旨在提高癲癇治療可及性的政策舉措,都為這一趨勢提供了支持。

就分銷管道而言,醫院藥房、零售藥房和線上藥房是主要細分市場。零售藥局在2024年的收入為23億美元,預計預測期內的複合年成長率為4.9%。在零售環境中,尤其是在中低收入國家,具成本效益學名藥的供應日益增多,有助於患者以更經濟的方式管理癲癇。此外,保險覆蓋和補貼計劃也使患者更容易透過零售店獲得必需藥物。

從區域來看,北美在2024年以41%的市佔率引領全球癲癇治療藥物市場。僅美國一國就貢獻了31億美元的收入,這得益於其較高的認知度、完善的醫療保健體係以及持續改善患者獲得先進神經系統治療途徑的努力。美國市場呈現逐年穩定成長,從2021年的28億美元成長至2023年的30億美元,並在2024年達到31億美元。該地區癲癇盛行率的不斷上升,加上有利的監管條件和全球製藥巨頭的參與,將繼續推動市場發展。

主要行業參與者正在積極投資先進的配方和聯合療法,旨在改善患者的治療效果並減輕癲癇對醫療保健系統的整體負擔。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 產業衝擊力

- 成長動力

- 癲癇盛行率上升

- 增加對研發活動的投資

- 對新型癲癇治療方法的需求日益成長

- 提高認知和早期診斷

- 產業陷阱與挑戰

- 與抗癲癇藥物相關的不良反應

- 專利到期

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 美國[食品藥物管理局(FDA)]

- 加拿大(加拿大衛生部法規)

- 歐洲

- 亞太地區

- 日本(PMDA)

- 中國(國家藥品監督管理局)

- 印度(CDSCO)

- 澳洲(TGA)

- 北美洲

- 管道分析

- 未來市場趨勢

- 差距分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按藥物類別,2021 - 2034 年

- 主要趨勢

- 第一代

- 第二代

- 第三代

第6章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 品牌

- 泛型

第7章:市場估計與預測:按管理路線,2021 - 2034 年

- 主要趨勢

- 口服

- 鼻腔

- 注射劑

- 直腸

第8章:市場估計與預測:按年齡層,2021 - 2034 年

- 主要趨勢

- 兒科

- 成人

第9章:市場估計與預測:按扣押類型,2021 - 2034 年

- 主要趨勢

- 局部性癲癇

- 全身性癲癇

- 合併癲癇

第 10 章:市場估計與預測:按配銷通路,2021 年至 2034 年

- 主要趨勢

- 醫院藥房

- 零售藥局

- 網路藥局

第 11 章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第12章:公司簡介

- AbbVie

- Bausch Health Companies

- Dr. Reddy's Laboratories

- Eisai

- GSK

- Jazz Pharmaceuticals

- Lupin Pharmaceuticals

- Neurelis

- Novartis

- Pfizer

- Sanofi

- SK Biopharmaceuticals

- Sumitomo Pharma

- Sun Pharmaceutical Industries

- UCB

The Global Epilepsy Treatment Drugs Market was valued at USD 8.3 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13 billion by 2034. The steady rise in epilepsy diagnoses globally is one of the key factors driving demand for more effective and accessible treatment options. Pharmaceutical innovations, the development of new-age anti-epileptic drugs with fewer side effects, and enhanced treatment adherence are all supporting this upward trend. Growing government and private investments in neurology-related research, alongside increasing awareness and screening rates, are contributing to the expanding market.

The rising global aging population-more vulnerable to neurological disorders-is also expected to further elevate the demand for epilepsy medications. Drug developers are prioritizing therapies that offer better tolerability, sustained release, and improved patient compliance. This shift, paired with improved healthcare infrastructure in developing nations and streamlined regulatory pathways in key markets, is creating a favorable environment for innovation and product adoption. Moreover, the transition toward more personalized medicine strategies, particularly for drug-resistant epilepsy, is improving treatment outcomes and driving long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $13 Billion |

| CAGR | 4.6% |

Anti-epileptic drugs (AEDs), also referred to as anticonvulsants, work by stabilizing irregular electrical signals in the brain, helping to prevent seizures and manage the overall symptoms of epilepsy. Based on drug class, the market is divided into first-generation, second-generation, and third-generation drugs. In 2024, second-generation AEDs accounted for the largest revenue share, contributing 47.2% to the global market. This segment is forecasted to expand at a CAGR of 4.6% from 2025 to 2034. Their broader acceptance is attributed to lower incidences of drug interactions, improved side effect profiles, and better patient adherence compared to older-generation therapies.

In terms of product type, the market is categorized into branded and generic drugs. Branded drugs generated USD 2.6 billion in 2024 and are projected to reach USD 4.1 billion by 2034. Pharmaceutical firms are increasingly focusing on producing branded treatments with improved pharmacokinetics, fewer adverse reactions, and greater therapeutic benefits. The rising need for novel treatments, especially among individuals who do not respond to conventional therapies, is also driving the demand for branded anti-epileptic medications.

When analyzing the route of administration, oral formulations held the largest share in 2024, accounting for USD 5.2 billion. This segment is projected to grow at a CAGR of 4.9% over the forecast period. Oral medications are preferred due to their convenience, ease of use, and the introduction of extended-release versions that improve dosage scheduling and patient adherence. The availability of diverse oral formulations is also accelerating adoption in both developed and emerging markets.

Based on patient demographics, the market is segmented into adult and pediatric populations. The adult segment led with a market value of USD 6 billion in 2024 and is expected to expand at a CAGR of 4.5% through 2034. The increasing incidence of epilepsy among adults is linked to age-related neurological conditions such as strokes, brain injuries, and degenerative disorders. As a result, the demand for reliable and targeted treatment approaches is rising, with a growing emphasis on multi-drug regimens and long-term therapy for improved seizure control.

According to seizure type, the market is segmented into focal seizures, generalized seizures, and combined seizures. The generalized seizure segment generated USD 2.5 billion in 2024 and is estimated to reach USD 4 billion by 2034. A rising number of generalized seizure cases, including tonic-clonic and absence seizures, is prompting the need for more robust therapeutic solutions. This trend is being supported by greater government funding for neurological research, insurance coverage expansions, and policy initiatives aimed at enhancing access to epilepsy care.

In terms of distribution channels, hospital pharmacies, retail pharmacies, and online pharmacies are the major segments. Retail pharmacies captured USD 2.3 billion in revenue in 2024 and are expected to register a CAGR of 4.9% during the forecast period. The growing availability of cost-effective generic drugs in retail settings, especially in low- and middle-income countries, is helping patients manage epilepsy more affordably. Additionally, insurance coverage and subsidy programs are making it easier for patients to access essential medications via retail outlets.

Regionally, North America led the global epilepsy treatment drugs market with a 41% share in 2024. The U.S. alone contributed USD 3.1 billion in revenue that year, driven by high awareness, well-developed healthcare systems, and consistent efforts to improve patient access to advanced neurological treatments. The U.S. market has shown steady year-on-year growth, moving from USD 2.8 billion in 2021 to USD 3 billion in 2023 and reaching USD 3.1 billion in 2024. The increasing prevalence of epilepsy in the region, coupled with favorable regulatory conditions and the presence of global pharmaceutical leaders, continues to push market development.

Major industry players are actively investing in advanced formulations and combination therapies, aiming to enhance patient outcomes and reduce the overall burden of epilepsy on healthcare systems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Drug class

- 2.2.2 Type

- 2.2.3 Route of administration

- 2.2.4 Age group

- 2.2.5 Seizure type

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of epilepsy

- 3.2.1.2 Increasing investments in research and development activities

- 3.2.1.3 Increasing demand for novel treatment for epilepsy

- 3.2.1.4 Growing awareness and early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects associated with the antiepileptic drugs

- 3.2.2.2 Patent expiration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. [Food and Drug Administration (FDA)]

- 3.4.1.2 Canada (Health Canada Regulation)

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.3.1 Japan (PMDA)

- 3.4.3.2 China (NMPA)

- 3.4.3.3 India (CDSCO)

- 3.4.3.4 Australia (TGA)

- 3.4.1 North America

- 3.5 Pipeline analysis

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 First-generation

- 5.3 Second-generation

- 5.4 Third-generation

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Branded

- 6.3 Generics

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Nasal

- 7.4 Injectable

- 7.5 Rectal

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Pediatric

- 8.3 Adult

Chapter 9 Market Estimates and Forecast, By Seizure Type, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Focal seizure

- 9.3 Generalized seizure

- 9.4 Combined seizure

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospital pharmacies

- 10.3 Retail pharmacies

- 10.4 Online pharmacies

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 AbbVie

- 12.2 Bausch Health Companies

- 12.3 Dr. Reddy’s Laboratories

- 12.4 Eisai

- 12.5 GSK

- 12.6 Jazz Pharmaceuticals

- 12.7 Lupin Pharmaceuticals

- 12.8 Neurelis

- 12.9 Novartis

- 12.10 Pfizer

- 12.11 Sanofi

- 12.12 SK Biopharmaceuticals

- 12.13 Sumitomo Pharma

- 12.14 Sun Pharmaceutical Industries

- 12.15 UCB

兒童失神性癲癇治療市場:依治療方法、藥物類別、最終用戶和分銷管道分類-2026-2032年全球市場預測癲癇治療市場:2026年至2032年全球市場預測(依產品類型、病患群體、治療方法、藥物類別和分銷管道分類)

兒童失神性癲癇治療市場:依治療方法、藥物類別、最終用戶和分銷管道分類-2026-2032年全球市場預測癲癇治療市場:2026年至2032年全球市場預測(依產品類型、病患群體、治療方法、藥物類別和分銷管道分類) 2026-2034年全球癲癇治療藥物市場規模、佔有率、趨勢和成長分析報告Douce症候群市場:依治療方法、產品類型、最終用戶、通路和年齡層別分類-2026-2032年全球市場預測

2026-2034年全球癲癇治療藥物市場規模、佔有率、趨勢和成長分析報告Douce症候群市場:依治療方法、產品類型、最終用戶、通路和年齡層別分類-2026-2032年全球市場預測 大腸桿菌市場分析及至2035年預測:依類型、產品類型、服務、技術、應用、最終用戶、形態、製程、設備分類幽門螺旋桿菌市場分析與預測(至2035年):類型、產品類型、服務、技術、應用、形式、設備、製程、最終用戶癲癇藥物市場分析及預測(至2035年):類型、產品、技術、應用、最終用戶、劑型、部署、功能、階段

大腸桿菌市場分析及至2035年預測:依類型、產品類型、服務、技術、應用、最終用戶、形態、製程、設備分類幽門螺旋桿菌市場分析與預測(至2035年):類型、產品類型、服務、技術、應用、形式、設備、製程、最終用戶癲癇藥物市場分析及預測(至2035年):類型、產品、技術、應用、最終用戶、劑型、部署、功能、階段 LKS治療市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、治療方法、診斷、最終用戶、地區和競爭格局分類,2021-2031年癲癇藥物市場-全球產業規模、佔有率、趨勢、機會、預測:按藥物、分銷管道、地區和競爭格局分類,2021-2031年拉考沙胺藥物市場按適應症、劑型、劑量強度、通路和最終用戶分類-2026-2032年全球預測

LKS治療市場-全球產業規模、佔有率、趨勢、機會和預測:按類型、治療方法、診斷、最終用戶、地區和競爭格局分類,2021-2031年癲癇藥物市場-全球產業規模、佔有率、趨勢、機會、預測:按藥物、分銷管道、地區和競爭格局分類,2021-2031年拉考沙胺藥物市場按適應症、劑型、劑量強度、通路和最終用戶分類-2026-2032年全球預測