|

市場調查報告書

商品編碼

1766350

汽車電子燃料市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Automotive E-Fuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

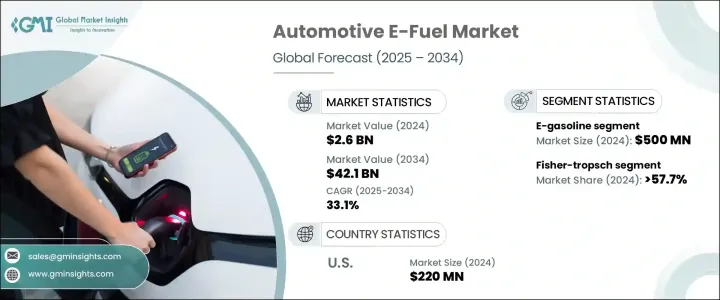

全球汽車電子燃料市場規模達26億美元,預計2034年將以33.1%的複合年成長率成長,達到421億美元。這一強勁成長的動力源於日益成長的減排壓力和向更永續的交通燃料轉型的壓力。世界各國政府正在加強排放法規,這促使人們增加對清潔燃料替代品的投資。電子燃料正逐漸成為頗具前景的解決方案,尤其適用於航空、長途貨運和海運等難以實現電氣化的產業。這些合成燃料無需改造即可在現有的內燃機(ICE)車輛上使用,只需進行少量改造,這使其成為一種極具吸引力的脫碳方案,同時又能充分利用現有基礎設施。

隨著能源轉型策略的不斷發展,電子燃料因其與傳統引擎的兼容性以及實現近乎碳中和性能的潛力而脫穎而出。支持性監管框架正在加速這些燃料的普及。相關部門正在推出財政激勵措施,例如撥款、稅收減免和資助項目,以促進永續燃料技術的研發。此外,全球致力於實現能源來源多元化並減少對化石燃料的依賴,這正推動煉油廠、汽車製造商和能源公司投資可擴展的電子燃料生產。利用再生電力、綠色氫能和捕獲的二氧化碳合成燃料的能力,為傳統汽油和柴油提供了一種循環且更清潔的替代品。這種適應性使電子燃料成為彌合當前化石燃料依賴與零排放交通運輸產業長期願景之間差距的策略選擇。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 26億美元 |

| 預測值 | 421億美元 |

| 複合年成長率 | 33.1% |

汽車電子燃料市場分為多種產品類型,包括電子汽油、電子柴油、電子煤油、乙醇和電子甲醇。其中,電子汽油細分市場在2024年的價值達到5億美元。電子汽油可以直接取代傳統汽油,無需進行技術改造即可用於現有的汽油引擎。它能夠在不進行額外基礎設施改造的情況下提供低排放的替代方案,使其成為向清潔燃料轉型的關鍵重點領域。其他細分市場,例如電子柴油和電子煤油,也展現出巨大的潛力,尤其是在重型車輛和航空應用領域,液體燃料在這些領域仍然至關重要。

就生產技術而言,市場細分為費托合成法、eRWGS 合成法和其他方法。費托合成技術在 2024 年佔據市場主導地位,佔總市佔率的 57.7% 以上。此製程利用氫氣和一氧化碳的混合物(稱為合成氣)合成液態碳氫化合物。所得燃料可取代傳統柴油和航空燃料,從而減少溫室氣體排放。費托合成法提供了一種可擴展的高品質合成燃料生產路線,其在市場上的主導地位凸顯了其商業可行性以及與現有燃料分銷網路的兼容性。

從地區來看,美國仍然是汽車電子燃料領域的主要參與者。 2022年,該市場規模為1.6億美元,2023年成長至1.7億美元,2024年將達2.2億美元。美國市場的成長得益於公共和私營部門對替代燃料技術的強勁投資,以及積極推動交通脫碳的措施。各州正在實施清潔能源政策,並鼓勵以永續航空燃料和低碳貨運解決方案為重點的試點計畫。持續的創新,加上技術開發商與汽車公司之間日益壯大的合作網路,使美國成為全球電子燃料發展的關鍵貢獻者。

競爭格局由少數幾家在合成燃料生產和商業化方面處於領先地位的公司所塑造。這些公司主要利用再生能源和碳捕集技術生產電子汽油和電子甲醇,旨在實現內燃機汽車的碳中和運作。他們的努力旨在提高產能、提升製程效率,並將電子燃料整合到主流燃料供應鏈中。透過持續投資尖端技術和策略合作,這些參與者正在幫助擴大市場規模,以滿足全球對永續汽車燃料日益成長的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 監管格局

- 產業衝擊力

- 成長潛力分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 策略舉措

- 競爭基準測試

- 戰略儀表板

- 創新與技術格局

第5章:市場規模及預測:按再生能源,2021 - 2034 年

- 主要趨勢

- 現場太陽能

- 風

第6章:市場規模及預測:依技術分類,2021 - 2034 年

- 主要趨勢

- 費托合成

- 增強型多普勒雷達系統

- 其他

第7章:市場規模及預測:依產品,2021 - 2034

- 主要趨勢

- 電子汽油

- 電動柴油

- 電子煤油

- 乙醇

- 電子甲醇

- 其他

第8章:市場規模及預測:按地區,2021 - 2034

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 荷蘭

- 西班牙

- 亞太地區

- 中國

- 澳洲

- 印度

- 日本

- 韓國

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第9章:公司簡介

- Archer Daniels Midland

- Arcadia eFuels

- Ballard Power Systems

- Ceres Power Holding

- Clean Fuels Alliance America

- Climeworks

- eFuel Pacific

- Electrochaea

- ExxonMobil

- FuelCell Energy

- HIF Global

- INFRA Synthetic Fuels

- LanzaJet

- Liquid Wind

- MAN Energy Solutions

- Norsk e-Fuel

- Porsche

- Sunfire

The Global Automotive E-Fuel Market was valued at USD 2.6 billion and is estimated to grow at a CAGR of 33.1% to reach USD 42.1 billion by 2034. This robust growth is driven by mounting pressure to reduce carbon emissions and shift toward more sustainable transportation fuels. Governments worldwide are tightening emissions regulations, prompting increased investment in cleaner fuel alternatives. E-fuels are emerging as a promising solution, especially for sectors that are difficult to electrify, such as aviation, long-haul freight, and maritime transport. These synthetic fuels can be used in existing internal combustion engine (ICE) vehicles with minimal or no modification, which makes them an attractive option for decarbonization while leveraging the current infrastructure.

As energy transition strategies evolve, e-fuels stand out due to their compatibility with traditional engines and their potential to deliver near carbon-neutral performance. Supportive regulatory frameworks are accelerating the adoption of these fuels. Authorities are rolling out financial incentives such as grants, tax breaks, and funding programs to promote research and development of sustainable fuel technologies. Additionally, global efforts to diversify energy sources and reduce dependence on fossil fuels are pushing refiners, automakers, and energy firms to invest in scalable e-fuel production. The ability to synthesize fuels from renewable electricity, green hydrogen, and captured carbon dioxide offers a circular and cleaner alternative to conventional gasoline and diesel. This adaptability positions e-fuels as a strategic option to bridge the gap between current fossil fuel dependency and the long-term vision of a zero-emissions transportation sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $42.1 Billion |

| CAGR | 33.1% |

The automotive e-fuel market is categorized into several product types, including e-gasoline, e-diesel, e-kerosene, ethanol, and e-methanol. Among these, the e-gasoline segment recorded a value of USD 500 million in 2024. E-gasoline acts as a direct replacement for conventional petrol, which allows it to be used in current gasoline engines without the need for technical modifications. Its ability to offer a lower-emission alternative without additional infrastructure changes makes it a key focus area in the transition to cleaner fuels. Other segments like e-diesel and e-kerosene also show promising potential, especially for heavy-duty vehicles and aviation applications, respectively, where liquid fuels remain essential.

In terms of production technology, the market is segmented into Fischer-Tropsch, eRWGS, and other methods. Fischer-Tropsch technology led the market in 2024, accounting for over 57.7% of the total share. This process synthesizes liquid hydrocarbons from a mixture of hydrogen and carbon monoxide, known as synthesis gas. The resulting fuels can serve as substitutes for traditional diesel and jet fuel, enabling reductions in greenhouse gas emissions. Fischer-Tropsch offers a scalable route for producing high-quality synthetic fuels, and its dominance in the market underscores its commercial viability and compatibility with current fuel distribution networks.

Regionally, the United States remains a major player in the automotive e-fuel space. The market was valued at USD 160 million in 2022, grew to USD 170 million in 2023, and reached USD 220 million in 2024. Growth in the U.S. market is underpinned by strong public and private investment in alternative fuel technologies and a proactive approach toward decarbonizing transportation. Various states are implementing clean energy policies and incentivizing pilot projects that focus on sustainable aviation fuels and low-carbon solutions for freight mobility. Continuous innovation, coupled with a growing network of partnerships between technology developers and automotive companies, positions the U.S. as a key contributor to global e-fuel development.

The competitive landscape is shaped by a handful of leading companies that are pioneering the production and commercialization of synthetic fuels. These companies are primarily involved in producing e-gasoline and e-methanol using renewable energy sources and captured carbon, targeting the carbon-neutral operation of ICE vehicles. Their efforts are geared toward increasing production capacity, enhancing process efficiency, and integrating e-fuels into mainstream fuel supply chains. Through ongoing investment in cutting-edge technology and strategic collaborations, these players are helping scale up the market to meet the rising global demand for sustainable automotive fuels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiative

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Renewable Source, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 On-site solar

- 5.3 Wind

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Fischer-Tropsch

- 6.3 eRWGS

- 6.4 Others

Chapter 7 Market Size and Forecast, By Product, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 E-gasoline

- 7.3 E-diesel

- 7.4 E-kerosene

- 7.5 Ethanol

- 7.6 E-methanol

- 7.7 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Netherlands

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland

- 9.2 Arcadia eFuels

- 9.3 Ballard Power Systems

- 9.4 Ceres Power Holding

- 9.5 Clean Fuels Alliance America

- 9.6 Climeworks

- 9.7 eFuel Pacific

- 9.8 Electrochaea

- 9.9 ExxonMobil

- 9.10 FuelCell Energy

- 9.11 HIF Global

- 9.12 INFRA Synthetic Fuels

- 9.13 LanzaJet

- 9.14 Liquid Wind

- 9.15 MAN Energy Solutions

- 9.16 Norsk e-Fuel

- 9.17 Porsche

- 9.18 Sunfire