|

市場調查報告書

商品編碼

1766322

動物人工授精市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Animal Artificial Insemination Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

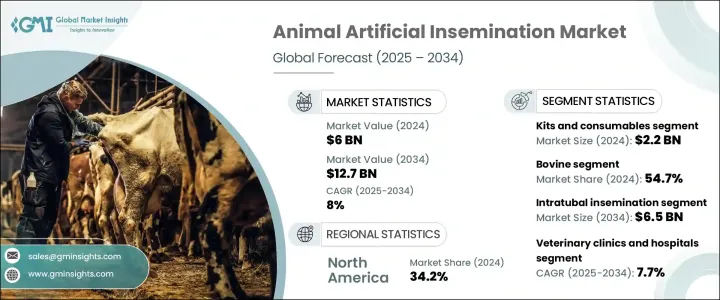

2024年,全球動物人工授精市場規模達60億美元,預計到2034年將以8%的複合年成長率成長,達到127億美元。推動這一成長的因素包括:對基因改良的日益關注、對更高品質牲畜的需求不斷成長,以及發展中地區廣泛採用先進的生殖解決方案。隨著全球人口持續成長,對高效畜牧生產的需求也日益成長,以滿足日益成長的肉類和乳製品需求。人工授精(AI)作為一種輔助生殖方法,透過提高動物的繁殖性能和生產力,在滿足這些需求方面變得越來越重要。

在世界許多地方,牲畜飼養者紛紛轉向人工智慧,不僅是為了提高畜群質量,也是為了降低飼養相關成本並提高生產力。透過選擇性育種,人工智慧有助於提高抗病性、產奶量和肉質等理想遺傳性狀,使其成為現代畜牧管理實踐的重要組成部分。獸醫保健產業投資的不斷增加,以及農民對控制育種技術長期效益的認知不斷提高,進一步推動了市場擴張。此外,人工智慧與獸醫服務的融合,以及精準育種工具的不斷發展,正在提高人工授精程序的有效性和可靠性,從而促進其在不同物種和地區的廣泛應用。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 60億美元 |

| 預測值 | 127億美元 |

| 複合年成長率 | 8% |

就產品類型而言,2024年,試劑盒和耗材細分市場以22億美元的估值領先市場。諸如授精吸管、吸管、手套和導管等耗材的頻繁使用使其成為每個人工授精週期中必不可少的部件,從而推動了強勁的需求。與資本密集型設備不同,這些產品需要持續補貨,因此對整體市場收入貢獻巨大。它們的高週轉率以及在臨床和農場環境中的必要性,進一步鞏固了其在市場上的主導地位。

依動物類型分類,牛類成為最大貢獻者,佔2024年總市場佔有率的54.7%。該領域受益於全球對乳製品和牛肉產品的巨大需求,這促使人工授精技術在牛隻育種中得到廣泛應用。持續強調改良牛群遺傳學,增強產乳量和抗病性等性狀,使得人工授精成為該領域的首選方法。龐大的牛群數量和有序的乳牛養殖進一步鞏固了該領域的領先市場佔有率。

從技術角度來看,輸卵管內授精市場預計將出現強勁成長,到2034年將達到65億美元。該技術將精液直接注入輸卵管,從而提高受精成功率,尤其是在傳統方法可能不太有效的情況下。導管設計和授精工具的進步正在提高該方法的可及性和精確度,從而擴大被追求高繁殖效率的育種者所採用。

按最終用途分析,2024年,獸醫診所和醫院佔據最大佔有率,預計到2034年將以7.7%的複合年成長率成長。這些機構提供專業的生殖服務,憑藉現代醫療設備和熟練的獸醫團隊,它們能夠處理複雜的手術,成為人工智慧生態系統的重要組成部分。生育管理意識的增強以及對專業照護的日益偏好,也促進了它們強大的市場佔有率。

從區域來看,北美在2024年以34.2%的市佔率領先全球市場。光是美國就佔了18.7億美元的佔有率,高於2023年的17.9億美元。這一成長反映了美國先進的獸醫基礎設施及其對現代育種技術的大力應用,這些技術支撐了畜牧業的高生產力。

動物人工授精市場的競爭格局以成熟的全球性公司和規模較小的區域性公司為主。四大領導企業——IMV Technologies、Genus Plc、URUS Group 和 CRV Holdings BV——在 2024 年共佔據全球約 48% 的市場佔有率。這些公司正大力投資產品創新、技術升級和策略合作,以保持競爭優勢。同時,本地製造商透過提供經濟高效的解決方案並透過合併和產品發布擴大其地域覆蓋範圍,持續加劇競爭。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 與自然交配相比,對更高繁殖效率的需求不斷增加

- 牲畜和伴侶動物對增強遺傳基因的需求不斷增加

- 精液採集與保存技術的技術進步

- 動物性傳染病盛行率上升

- 產業陷阱與挑戰

- 手術失敗和併發症的風險

- 缺乏熟練的技術人員

- 監管和道德問題

- 設定和設備成本高

- 市場機會

- 牲畜遺傳改良需求不斷增加

- 發展中國家日益採用人工智慧

- 成長動力

- 成長潛力分析

- 監管格局

- 技術格局

- 當前的技術趨勢

- 新興技術

- 未來市場趨勢

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 策略儀表板

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 服務

- 精液

- 正常精液

- 性控精液

- 儀器

- 套件和耗材

第6章:市場估計與預測:依動物類型,2021 - 2034 年

- 主要趨勢

- 牛

- 豬

- 綿羊

- 山羊

- 馬

- 其他動物類型

第7章:市場估計與預測:按技術,2021 - 2034 年

- 主要趨勢

- 輸卵管內授精

- 子宮腔內授精

- 子宮頸內授精

- 子宮腔內輸卵管腹腔授精

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 獸醫診所和醫院

- 動物養殖中心

- 科學研究院所及大學

- 其他最終用途

第9章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第10章:公司簡介

- Bovine Elite

- CRV Holdings

- Geno SA

- Genus Plc

- IMV Technologies

- Minitube Group

- SEMEX

- Select Sires

- Swine Genetics International

- Shipley Swine Genetics

- Stallion AI Services

- STgenetics

- URUS Group

- VikingGenetics

The Global Animal Artificial Insemination Market was valued at USD 6 billion in 2024 and is estimated to grow at a CAGR of 8% to reach USD 12.7 billion by 2034. This growth is being driven by a rising focus on genetic improvement, increased demand for higher quality livestock, and the widespread adoption of advanced reproductive solutions across developing regions. As the global population continues to grow, so does the need for efficient livestock production to meet escalating demands for meat and dairy products. Artificial insemination (AI), as a method of assisted reproduction, is becoming increasingly important in meeting these needs by enhancing the reproductive performance and productivity of animals.

In many parts of the world, livestock breeders are turning to AI not only to improve herd quality but also to reduce breeding-related costs and boost productivity. By enabling selective breeding, AI helps increase desirable genetic traits such as disease resistance, milk yield, and meat quality, which makes it a vital component of modern livestock management practices. Market expansion is further influenced by the rising investments in the veterinary healthcare industry and the growing awareness among farmers about the long-term benefits of controlled breeding techniques. Additionally, the integration of AI with veterinary services, along with the continuous development of precision breeding tools, is enhancing the effectiveness and reliability of artificial insemination procedures, encouraging its widespread use across species and regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 8% |

In terms of product type, in 2024, the kits and consumables segment led the market with a valuation of USD 2.2 billion. The frequent use of consumables like insemination pipettes, straws, gloves, and catheters makes them essential components in every AI cycle, driving strong demand. Unlike capital-intensive equipment, these products require consistent replenishment, thereby contributing significantly to overall market revenue. Their high turnover rate and necessity in both clinical and farm settings further reinforce their dominant position in the market.

By animal type, the bovine segment emerged as the top contributor, accounting for 54.7% of the total market share in 2024. This segment benefits from the substantial global demand for dairy and beef products, which has led to the large-scale adoption of artificial insemination techniques in cattle breeding. The consistent emphasis on improving herd genetics and enhancing traits like milk production and disease resistance has made AI a preferred method in this segment. Large cattle populations and organized dairy operations further contribute to the segment's leading share.

Based on technique, the intratubal insemination segment is projected to witness strong growth, reaching USD 6.5 billion by 2034. This technique involves placing semen directly into the fallopian tubes, allowing for improved fertilization success, especially in cases where conventional approaches may not be as effective. Advances in catheter design and insemination tools are enhancing the accessibility and precision of this method, increasing its adoption among breeders aiming for high reproductive efficiency.

When analyzed by end use, in 2024, veterinary clinics and hospitals held the largest share and are expected to grow at a 7.7% CAGR through 2034. These facilities provide specialized reproductive services, and their ability to handle complex procedures, aided by modern medical equipment and skilled veterinary staff, makes them an essential part of the AI ecosystem. Increased awareness of fertility management and the rising preference for professional care also contribute to their strong market presence.

Regionally, North America led the global market in 2024 with a 34.2% share. The United States alone accounted for USD 1.87 billion in 2024, growing from USD 1.79 billion in 2023. This growth reflects the country's advanced veterinary infrastructure and its strong adoption of modern breeding technologies, which support high livestock productivity.

The competitive landscape of the animal artificial insemination market is characterized by the presence of a mix of established global companies and smaller regional firms. Four leading players- IMV Technologies,Genus Plc, URUS Group, and CRV Holdings B.V.-collectively held around 48% of the global market in 2024. These companies are heavily investing in product innovation, technological upgrades, and strategic collaborations to maintain their competitive edge. Meanwhile, local manufacturers continue to intensify competition by offering cost-effective solutions and expanding their geographic presence through mergers and product launches.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Animal type

- 2.2.4 Technique

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for higher reproductive efficiency compared to natural mating

- 3.2.1.2 Increasing demand for enhanced genetics in both livestock and companion animals

- 3.2.1.3 Technological advancements in semen collection and preservation techniques

- 3.2.1.4 Rising prevalence of sexually transmitted diseases among animals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Risk of procedural failures and complications

- 3.2.2.2 Lack of skilled technicians

- 3.2.2.3 Regulatory and ethical concerns

- 3.2.2.4 High set-up and equipment cost

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for genetic improvement in livestock

- 3.2.3.2 Growing adoption of artificial intelligence in developing countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Services

- 5.3 Semen

- 5.3.1 Normal semen

- 5.3.2 Sexed semen

- 5.4 Instruments

- 5.5 Kits and consumables

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Bovine

- 6.3 Swine

- 6.4 Ovine

- 6.5 Caprine

- 6.6 Equine

- 6.7 Other animal types

Chapter 7 Market Estimates and Forecast, By Technique, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Intratubal insemination

- 7.3 Intrauterine insemination

- 7.4 Intracervical insemination

- 7.5 Intrauterine tuboperitoneal insemination

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary clinics and hospitals

- 8.3 Animal breeding centers

- 8.4 Research institutes and universities

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bovine Elite

- 10.2 CRV Holdings

- 10.3 Geno SA

- 10.4 Genus Plc

- 10.5 IMV Technologies

- 10.6 Minitube Group

- 10.7 SEMEX

- 10.8 Select Sires

- 10.9 Swine Genetics International

- 10.10 Shipley Swine Genetics

- 10.11 Stallion AI Services

- 10.12 STgenetics

- 10.13 URUS Group

- 10.14 VikingGenetics

2026-2034年全球獸醫人工授精市場規模、佔有率、趨勢和成長分析報告全球動物人工授精市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026-2034年全球獸醫人工授精市場規模、佔有率、趨勢和成長分析報告全球動物人工授精市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 獸用人工授精市場規模、佔有率和成長分析(按動物類型、產品、最終用戶和地區分類)-2026-2033年產業預測

獸用人工授精市場規模、佔有率和成長分析(按動物類型、產品、最終用戶和地區分類)-2026-2033年產業預測 豬隻人工授精市場規模、佔有率和趨勢分析報告:按解決方案、分銷管道、地區和細分市場預測(2026-2033 年)美國馬人工授精市場:市場規模、佔有率、趨勢分析(按解決方案、馬匹品種和分銷管道分類)、細分市場預測(2025-2033 年)馬匹人工授精市場規模、佔有率和趨勢分析報告:按解決方案、馬匹、分銷管道、地區和細分市場預測,2025 年至 2033 年

豬隻人工授精市場規模、佔有率和趨勢分析報告:按解決方案、分銷管道、地區和細分市場預測(2026-2033 年)美國馬人工授精市場:市場規模、佔有率、趨勢分析(按解決方案、馬匹品種和分銷管道分類)、細分市場預測(2025-2033 年)馬匹人工授精市場規模、佔有率和趨勢分析報告:按解決方案、馬匹、分銷管道、地區和細分市場預測,2025 年至 2033 年 動物用人工授精的全球市場:各解決方案,動物類別,各終端用戶,各地區,機會,預測,2018年~2032年

動物用人工授精的全球市場:各解決方案,動物類別,各終端用戶,各地區,機會,預測,2018年~2032年 動物人工授精市場,規模,佔有率,趨勢,產業分析報告:各解決方案,類別,各流通管道,各地區,2025年~2034年的市場預測美國動物人工授精市場規模、佔有率、趨勢分析報告:按解決方案、動物類型、分銷管道、細分市場、預測,2025-2030 年

動物人工授精市場,規模,佔有率,趨勢,產業分析報告:各解決方案,類別,各流通管道,各地區,2025年~2034年的市場預測美國動物人工授精市場規模、佔有率、趨勢分析報告:按解決方案、動物類型、分銷管道、細分市場、預測,2025-2030 年 馬匹人工授精市場-全球產業規模、佔有率、趨勢、機會和預測,按解決方案、馬匹類型、配銷通路、地區和競爭細分,2020-2030 年

馬匹人工授精市場-全球產業規模、佔有率、趨勢、機會和預測,按解決方案、馬匹類型、配銷通路、地區和競爭細分,2020-2030 年