|

市場調查報告書

商品編碼

1766253

快速換刀系統市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Quick-change Tooling System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

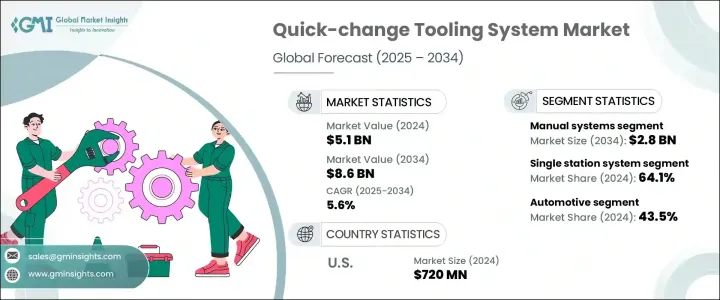

2024年,全球快速換刀系統市場規模達51億美元,預計2034年將以5.6%的複合年成長率成長,達到86億美元。對製造靈活性、營運速度、縮短設定時間和整體生產力的需求不斷成長,正推動汽車、航太、電子和醫療器材產業的公司投資於速度更快、響應更快的工具解決方案。這些產業面臨越來越大的壓力,需要在精簡營運、減少停機時間的同時,滿足不斷變化的生產目標。

快速換刀系統可以加快刀具更換速度,顯著縮短換刀時間,有助於維持穩定的產量。它們廣泛應用於數控中心、成型單元、沖壓設備和其他精密驅動環境,彰顯了其在智慧製造上的價值。隨著工業4.0的蓬勃發展,下一代系統現已整合物聯網和感測器技術,能夠即時洞察刀具性能、磨損和換刀間隔,從而實現更具預測性和數據驅動性的營運。這種日益成長的自動化和即時監控趨勢,為刀具基礎設施的創新和持續改進奠定了基礎。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 51億美元 |

| 預測值 | 86億美元 |

| 複合年成長率 | 5.6% |

2024年,手動快速更換系統以19億美元的估值領先市場,預計2034年將達到28億美元。其受歡迎程度源自於其易於與現有設備整合、成本效益高以及培訓要求低等優勢。對於不太依賴高速自動化的營運而言,這些系統仍然是理想之選,為中小型企業提供了切實可行的解決方案。此外,在木工、塑膠成型和金屬製造等注重多功能性和簡易性的領域,手動快速更換系統也備受青睞。在現代化進程較慢、基礎設施投資有限的地區,手動快速更換系統能夠在傳統機器上有效運行,這進一步增強了其重要性。

2024年,單工位刀具系統市場佔有64.1%的佔有率,預計到2034年將以5%的複合年成長率成長。這些系統在需要在固定位置換刀的應用中特別有效,例如單一CNC單元或車床。其價格實惠、設置簡單、維護方便,非常適合製造業的中型企業。這些系統在製造、塑膠和精密金屬加工等行業中應用廣泛,這些產業受益於有針對性的獨立工具機應用。

2024 年,美國快速換刀系統市值為 7.2 億美元,預估 2025 年至 2034 年期間的複合年成長率為 6.1%。該地區強勁的汽車、航太和國防製造業是採用該技術的主要驅動力。隨著製造商強調速度、客製化和精益生產方法,他們已顯著轉向自動化工具系統。美國受益於成熟的工業環境,這得益於熟練的勞動力、尖端的研發能力以及強勁的創新需求。這種結合支援快速週轉和客製化的工具應用,增加了對手動和自動快速換刀解決方案的需求。

快速換刀系統產業的領先公司包括阿美特克公司 (AMETEK, Inc.)、那智不二越公司 (Nachi-Fujikoshi Corp.)、伊利諾伊工具廠公司 (Illinois Tool Works Inc.,簡稱 ITW)、THK 有限公司和肯納金屬公司 (Kennametal Inc.)。為了鞏固市場地位,各公司正在投資創新,開發模組化、可擴展的工具系統,以提高與自動化機械的兼容性。許多公司正在與原始設備製造商 (OEM) 和機器製造商建立策略聯盟,將其技術直接整合到新的生產設備中。各公司也正在透過支援物聯網 (IoT) 的功能來增強產品線,以實現遠端診斷和即時監控。持續的升級、對人體工學設計的關注以及向新興經濟體的擴張,正在幫助主要參與者保持競爭力,同時滿足對快速、靈活和高效工具解決方案的需求。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 利潤率

- 每個階段的增值

- 影響價值鏈的因素

- 中斷

- 產業衝擊力

- 成長動力

- 產業陷阱與挑戰

- 機會

- 成長潛力分析

- 未來市場趨勢

- 技術和創新格局

- 當前的技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品類型

- 監理框架

- 標準和認證

- 環境法規

- 進出口法規

- 貿易統計數據

- 主要進口國

- 主要出口國

- 波特五力分析

- PESTEL分析

- 消費者行為分析

- 購買模式

- 偏好分析

- 消費者行為的區域差異

- 電子商務對購買決策的影響

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 按地區

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 擴張計劃

第5章:市場估計與預測:按類型,2021 - 2034 年

- 主要趨勢

- 手動系統

- 自動系統

- 液壓系統

- 其他

第6章:市場估計與預測:按營運模式,2021 - 2034 年

- 主要趨勢

- 單站系統

- 多站系統

第7章:市場估計與預測:按應用,2021 - 2034 年

- 主要趨勢

- 射出成型

- 沖壓和壓印工具

- 機器人工具

- 焊接系統

- 組裝線

- 包裝機

- 其他

第8章:市場估計與預測:依最終用途,2021 - 2034 年

- 主要趨勢

- 汽車

- 航太和國防

- 消費性電子產品

- 醫療器材

- 包裝

- 產業機械

- 塑膠和橡膠

- 其他

第9章:市場估計與預測:按配銷通路,2021 - 2034 年

- 主要趨勢

- 直接的

- 間接

第10章:市場估計與預測:按地區,2021 - 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

第 11 章:公司簡介

- AMETEK, Inc.

- BIG DAISHOWA

- Destaco

- Diebold Goldring-Werkzeugfabrik

- Erowa AG

- Illinois Tool Works Inc. (ITW)

- Jergens Inc.

- Kennametal Inc. Co., Ltd

- LANG Technik GmbH

- Mate Precision Technologies

- Nachi-Fujikoshi Corp

- Rohm GmbH

- SCHUNK GmbH & Co. KG

- SMW Autoblok

- THK Co., Ltd.

The Global Quick-change Tooling System Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 8.6 billion by 2034. The rise in demand for manufacturing flexibility, operational speed, reduced setup times, and overall productivity is pushing companies across the automotive, aerospace, electronics, and medical device sectors to invest in quicker, more responsive tooling solutions. These industries face increasing pressure to streamline operations and reduce downtime while meeting evolving production goals.

Quick-change tooling systems allow faster tool replacements and significantly cut changeover durations, helping maintain consistent output levels. Their widespread use in CNC centers, molding units, stamping facilities, and other precision-driven environments underscores their value in smart manufacturing. As Industry 4.0 gains momentum, next-generation systems now integrate IoT and sensor technologies to enable real-time insights into tool performance, wear, and change intervals, allowing more predictive and data-driven operations. This growing shift toward automation and real-time monitoring is setting the stage for innovation and continuous improvement in tooling infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.6% |

Manual quick-change systems led the market in 2024 with a valuation of USD 1.9 billion and are projected to hit USD 2.8 billion by 2034. Their popularity stems from easy integration with existing machinery, cost efficiency, and minimal training requirements. These systems remain ideal for operations that do not depend heavily on high-speed automation, offering a practical solution for small and medium businesses. They're also favored in segments like woodworking, plastic molding, and metal fabrication, where versatility and simplicity matter. The ability to function effectively in legacy machines further enhances their relevance in regions where modernization is slower and infrastructure investments are limited.

In 2024, the single-station tooling systems segment held a 64.1% share and is forecasted to grow at a CAGR of 5% through 2034. These systems are especially effective in applications requiring tool changes at fixed points, such as with individual CNC units or lathes. Their affordability, minimal setup complexity, and easy maintenance make them well-suited for mid-sized enterprises across manufacturing sectors. The use of these systems is prominent in industries like fabrication, plastics, and precision metalwork, which benefit from targeted and standalone machine applications.

United States Quick-change Tooling System Market was valued at USD 720 million in 2024 and is anticipated to grow at a CAGR of 6.1% between 2025 and 2034. The region's robust automotive, aerospace, and defense manufacturing sectors are major drivers of adoption. As manufacturers emphasize speed, customization, and lean production methods, there has been a notable shift toward automation-ready tooling systems. The U.S. benefits from a sophisticated industrial environment supported by skilled labor, cutting-edge R&D capabilities, and a strong demand for innovation. This combination supports rapid turnaround and tailored tooling applications, increasing demand for both manual and automated quick-change solutions.

Leading companies in the Quick-change Tooling System Industry include AMETEK, Inc., Nachi-Fujikoshi Corp, Illinois Tool Works Inc. (ITW), THK Co., Ltd., and Kennametal Inc. To reinforce their market positions, companies are investing in innovation by developing modular and scalable tooling systems that offer greater compatibility with automated machinery. Many are forming strategic alliances with OEMs and machine manufacturers to integrate their technologies directly into new production equipment. Firms are also enhancing product lines with IoT-enabled features for remote diagnostics and real-time monitoring. Continuous upgrades, focus on ergonomic designs and expansion into emerging economies are helping key players stay competitive while meeting demand for fast, flexible, and efficient tooling solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Operation mode

- 2.2.4 Application

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Manual systems

- 5.3 Automatic systems

- 5.4 Hydraulic systems

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Operation mode, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Single-station systems

- 6.3 Multi-station systems

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Injection molding

- 7.3 Stamping & press tools

- 7.4 Robotic tooling

- 7.5 Welding systems

- 7.6 Assembly lines

- 7.7 Packaging machines

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace and defense

- 8.4 Consumer electronics

- 8.5 Medical devices

- 8.6 Packaging

- 8.7 Industrial machinery

- 8.8 Plastics and rubber

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 UAE

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AMETEK, Inc.

- 11.2 BIG DAISHOWA

- 11.3 Destaco

- 11.4 Diebold Goldring-Werkzeugfabrik

- 11.5 Erowa AG

- 11.6 Illinois Tool Works Inc. (ITW)

- 11.7 Jergens Inc.

- 11.8 Kennametal Inc. Co., Ltd

- 11.9 LANG Technik GmbH

- 11.10 Mate Precision Technologies

- 11.11 Nachi-Fujikoshi Corp

- 11.12 Rohm GmbH

- 11.13 SCHUNK GmbH & Co. KG

- 11.14 SMW Autoblok

- 11.15 THK Co., Ltd.