|

市場調查報告書

商品編碼

1766245

急性冠狀動脈症候群治療市場機會、成長動力、產業趨勢分析及 2025 - 2034 年預測Acute Coronary Syndrome Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

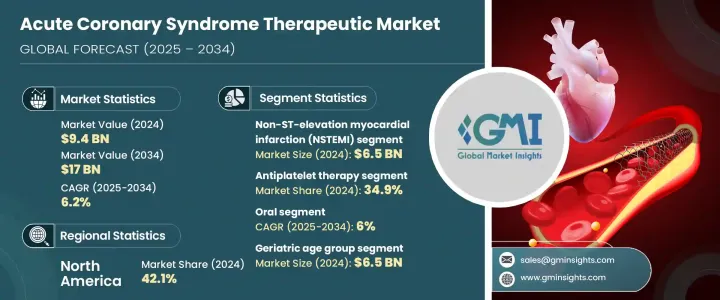

2024 年全球急性冠狀動脈綜合症治療市場價值為 94 億美元,預計到 2034 年將以 6.2% 的複合年成長率成長至 170 億美元。市場擴張的主要原因是心血管疾病發生率的上升,特別是急性冠狀動脈症候群,其包括 ST 段抬高型心肌梗塞 (STEMI)、非 ST 段抬高型心肌梗塞 (NSTEMI) 和不穩定型心絞痛等疾病。這些疾病是全球主要死亡原因之一,對先進療法的需求龐大。藥物傳輸系統的技術創新和下一代心血管藥物的開發正在增強治療選擇。此外,ACS 個人化醫療的日益成長趨勢使得可以根據個別患者情況制定更有針對性的治療方案。

聯合療法和緩釋製劑的興起正在提高治療急性冠狀動脈綜合症(ACS)的安全性和有效性。此外,在緊急情況下加強早期發現和快速診斷的努力,以及政府對心臟健康計畫的支持,也促進了市場的成長。高度重視整合各種藥物治療,包括抗血小板藥、抗凝血藥和BETA受體阻斷劑,有助於更有效控制病情。製藥公司正致力於透過區域生產、合作和新藥開發來擴大其覆蓋範圍,以滿足已開發市場和新興市場日益成長的需求。

| 市場範圍 | |

|---|---|

| 起始年份 | 2024 |

| 預測年份 | 2025-2034 |

| 起始值 | 94億美元 |

| 預測值 | 170億美元 |

| 複合年成長率 | 6.2% |

2024年,非ST段上升型心肌梗塞(NSTEMI)領域以65億美元的估值領先市場,這得益於該疾病在全球範圍內的日益成長的患病率。 NSTEMI是由冠狀動脈部分阻塞引起的,需要立即進行醫療干預,其發生率高於STEMI,但對心臟的損害較小。生活方式相關的風險因素以及診斷工具(例如高靈敏度的肌鈣蛋白檢測和心臟成像)的進步等因素提高了NSTEMI的檢出率,進一步推動了對該疾病標靶治療的需求。

2024年,抗血小板治療領域佔34.9%的市佔率。這些藥物包括阿斯匹靈、氯吡格雷和替格瑞洛等,通常用於預防血小板聚集和血栓形成,而血栓是急性冠狀動脈綜合症(ACS)動脈阻塞的關鍵原因。由於臨床指引推薦雙重抗血小板治療,尤其是針對高風險患者,抗血小板治療的應用十分廣泛。隨著起效更快、更安全的抗血小板藥物的持續開發,其在不同患者群體中的應用也不斷擴大。

2024年,美國急性冠狀動脈症候群(ACS)治療市場規模達36億美元。美國ACS的盛行率不斷上升,推動了對先進治療方案的需求。旨在應對高血壓、肥胖症和糖尿病等風險因素的公共衛生舉措,以及醫療基礎設施的改善,正在推動市場成長。此外,指南導向的藥物治療的廣泛應用,有助於改善患者預後,並降低與心臟護理相關的醫療成本。

全球急性冠狀動脈綜合症治療市場的主要參與者包括默克、輝瑞、阿斯特捷利康、百時美施貴寶、禮來、基因泰克(羅氏)、賽諾菲、楊森製藥和勃林格殷格翰等。急性冠狀動脈綜合症治療市場的公司正在透過對新藥研發的策略性投資來鞏固其地位,尤其是那些提供更快起效和更高安全性的藥物。許多製藥公司正在透過聯合療法和個人化治療方案來擴展其產品組合,以滿足患者的獨特需求。與醫療保健提供者和政府計劃的合作也是其策略的重要組成部分,使他們能夠進入服務不足的市場。此外,該公司正在利用數位健康技術來改善患者監測和治療依從性。擴大區域製造能力和獲得新療法的監管批准也是在已開發市場和新興市場保持競爭優勢的關鍵策略。

目錄

第1章:方法論與範圍

第2章:執行摘要

第3章:行業洞察

- 產業生態系統分析

- 供應商格局

- 每個階段的增值

- 影響價值鏈的因素

- 產業衝擊力

- 成長動力

- 心血管疾病發生率上升

- ACS 藥物治療的進展

- 更重視早期診斷和緊急護理

- 人口老化加劇和復發事件

- 產業陷阱與挑戰

- 治療費用高且難以取得

- 臨床實務和依從性的差異

- 市場機會

- 心血管負擔較重的新興市場

- 公私醫療合作

- 成長動力

- 成長潛力分析

- 監管格局

- 北美洲

- 歐洲

- 亞太地區

- 未來市場趨勢

- 定價分析

- 管道分析

- 消費者行為分析

- 波特的分析

- PESTEL分析

第4章:競爭格局

- 介紹

- 公司市佔率分析

- 公司矩陣分析

- 主要市場參與者的競爭分析

- 競爭定位矩陣

- 關鍵進展

- 併購

- 夥伴關係和合作

- 新產品發布

第5章:市場估計與預測:按類型,2021 年至 2034 年

- 主要趨勢

- 非 ST 段上升型心肌梗塞 (NSTEMI)

- ST 段上升型心肌梗塞 (STEMI)

- 不穩定型心絞痛

第6章:市場估計與預測:依藥物類別,2021 年至 2034 年

- 主要趨勢

- 抗血小板治療

- 抗凝血劑

- BETA受體阻斷劑

- 硝酸鹽

- 血栓溶解劑

- 其他藥物

第7章:市場估計與預測:依管理路線,2021 年至 2034 年

- 主要趨勢

- 口服

- 注射劑

第8章:市場估計與預測:按年齡層,2021 年至 2034 年

- 主要趨勢

- 成人

- 老年

第9章:市場估計與預測:依最終用途,2021 年至 2034 年

- 主要趨勢

- 醫院

- 心臟病診所

- 門診手術中心

- 其他最終用途

第10章:市場估計與預測:按地區,2021 年至 2034 年

- 主要趨勢

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第 11 章:公司簡介

- AstraZeneca

- Azurity Pharmaceuticals

- Baxter Healthcare

- Boehringer Ingelheim

- Bristol Myers Squibb

- Cipla

- Eli Lilly

- Genentech (Roche)

- Intas Pharmaceuticals

- Janssen Pharmaceuticals

- Merck

- Novartis

- Pfizer

- Ranbaxy Laboratories

- Sanofi

The Global Acute Coronary Syndrome Therapeutics Market was valued at USD 9.4 billion in 2024 and is estimated to grow at a CAGR of 6.2% to reach USD 17 billion by 2034. The market expansion is primarily driven by the rising incidence of cardiovascular diseases, particularly acute coronary syndrome, which encompasses conditions such as ST-elevation myocardial infarction (STEMI), non-ST-elevation myocardial infarction (NSTEMI), and unstable angina. These conditions are among the leading causes of death worldwide, creating significant demand for advanced therapies. Technological innovations in drug delivery systems and the development of next-generation cardiovascular drugs are enhancing treatment options. Additionally, the growing trend of personalized medicine for ACS allows for more targeted treatments tailored to individual patient profiles.

The rise of combination therapies and extended-release formulations is improving both safety and effectiveness in treating ACS. Furthermore, efforts to enhance early detection and rapid diagnosis in emergency settings, along with government support for heart health initiatives, are also contributing to market growth. A strong emphasis on integrating various pharmacological treatments, including antiplatelets, anticoagulants, and beta-blockers, is helping to manage the condition more effectively. Pharmaceutical companies are focusing on expanding their reach through regional production, collaborations, and new drug development to meet the growing demand across both developed and emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.4 Billion |

| Forecast Value | $17 Billion |

| CAGR | 6.2% |

The NSTEMI segment led the market in 2024 with a valuation of USD 6.5 billion, driven by the growing prevalence of this condition globally. NSTEMI, which results from partial blockage of coronary arteries, demands immediate medical intervention and is more common than STEMI, though it causes less damage to the heart. Factors like lifestyle-related risk factors and advancements in diagnostic tools, such as sensitive troponin assays and cardiac imaging, have increased the detection rates of NSTEMI, further driving the demand for targeted therapeutics for the condition.

The antiplatelet therapies segment held a 34.9% share in 2024. These therapies, including drugs like aspirin, clopidogrel, and ticagrelor, are commonly used to prevent platelet aggregation and thrombus formation, which are key causes of artery blockage in ACS. Their use is widespread due to clinical guidelines recommending dual antiplatelet therapy, especially for high-risk patients. The ongoing development of faster-acting and safer antiplatelet medications continues to expand their use across diverse patient populations.

U.S. Acute Coronary Syndrome Therapeutics Market was valued at USD 3.6 billion in 2024. The growing prevalence of ACS in the U.S. is driving demand for advanced treatment options. Public health initiatives addressing risk factors such as hypertension, obesity, and diabetes, as well as improving healthcare infrastructure, are contributing to market growth. Additionally, the widespread adoption of guideline-directed medical therapy is helping improve patient outcomes and reduce healthcare costs related to cardiac care.

Key players in the Global Acute Coronary Syndrome Therapeutics Market include Merck, Pfizer, AstraZeneca, Bristol Myers Squibb, Eli Lilly, Genentech (Roche), Sanofi, Janssen Pharmaceuticals, and Boehringer Ingelheim, among others. Companies in the acute coronary syndrome therapeutics market are strengthening their position through strategic investments in research and development of new drugs, especially those offering faster action and improved safety profiles. Many pharmaceutical firms are expanding their portfolios with combination therapies and personalized treatment options to address the unique needs of patients. Collaborations with healthcare providers and government initiatives are also a significant part of their strategy, enabling them to reach underserved markets. Additionally, companies are leveraging digital health technologies to improve patient monitoring and treatment adherence. Expanding regional manufacturing capabilities and securing regulatory approvals for novel therapies are also key strategies to maintain competitive advantage in both developed and emerging markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Drug class

- 2.2.4 Route of administration

- 2.2.5 Age group

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of cardiovascular diseases

- 3.2.1.2 Advancements in pharmacological treatments for ACS

- 3.2.1.3 Increasing emphasis on early diagnosis and emergency care

- 3.2.1.4 Growing aging population and recurrent events

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs and accessibility issues

- 3.2.2.2 Variability in clinical practice and adherence

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets with high cardiovascular burden

- 3.2.3.2 Public-private healthcare collaborations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pricing analysis

- 3.7 Pipeline analysis

- 3.8 Consumer behaviour analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Non-ST-elevation myocardial infarction (NSTEMI)

- 5.3 ST-elevation MI (STEMI)

- 5.4 Unstable angina

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Antiplatelet therapy

- 6.3 Anticoagulants

- 6.4 Beta blockers

- 6.5 Nitrates

- 6.6 Thrombolytics

- 6.7 Other medications

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectables

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Adult

- 8.3 Geriatric

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Cardiology clinics

- 9.4 Ambulatory surgical centers

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AstraZeneca

- 11.2 Azurity Pharmaceuticals

- 11.3 Baxter Healthcare

- 11.4 Boehringer Ingelheim

- 11.5 Bristol Myers Squibb

- 11.6 Cipla

- 11.7 Eli Lilly

- 11.8 Genentech (Roche)

- 11.9 Intas Pharmaceuticals

- 11.10 Janssen Pharmaceuticals

- 11.11 Merck

- 11.12 Novartis

- 11.13 Pfizer

- 11.14 Ranbaxy Laboratories

- 11.15 Sanofi